Controlled emulation of payment cards

Templeton , et al.

U.S. patent number 10,614,450 [Application Number 14/455,287] was granted by the patent office on 2020-04-07 for controlled emulation of payment cards. This patent grant is currently assigned to Squre, Inc.. The grantee listed for this patent is Square, Inc.. Invention is credited to Paul Aaron, Andrew Borovsky, Jesse L. Dorogusker, Alexey Kalinichenko, Thomas Templeton.

| United States Patent | 10,614,450 |

| Templeton , et al. | April 7, 2020 |

Controlled emulation of payment cards

Abstract

A technique for a proxy card to emulate each of a plurality of payment cards according to emulation rules associated with the payment card. The proxy card initially selects one of the plurality of payment cards for emulation based on one or more selection rules or a user instruction. Next, the proxy card emulates the selected payment card according to one or more emulation rule associated with the selected payment card, each relating to how emulation is performed with respect to time, location, business, or other factors.

| Inventors: | Templeton; Thomas (San Francisco, CA), Kalinichenko; Alexey (San Francisco, CA), Borovsky; Andrew (New York, NY), Aaron; Paul (San Francisco, CA), Dorogusker; Jesse L. (Palo Alto, CA) | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Applicant: |

|

||||||||||

| Assignee: | Squre, Inc. (San Francisco,

unknown) |

||||||||||

| Family ID: | 70056355 | ||||||||||

| Appl. No.: | 14/455,287 | ||||||||||

| Filed: | August 8, 2014 |

| Current U.S. Class: | 1/1 |

| Current CPC Class: | G06Q 20/105 (20130101); G06Q 20/34 (20130101); G06Q 20/405 (20130101); G06Q 20/351 (20130101); G06Q 20/367 (20130101); G06Q 20/204 (20130101); G06Q 20/354 (20130101); G06Q 20/3572 (20130101) |

| Current International Class: | G06Q 20/00 (20120101); G06Q 20/34 (20120101); G06Q 20/10 (20120101); G06Q 20/20 (20120101) |

| Field of Search: | ;705/16,41 ;235/492 |

References Cited [Referenced By]

U.S. Patent Documents

| 5590038 | December 1996 | Pitroda |

| 6427911 | August 2002 | Barnes et al. |

| 8280793 | October 2012 | Kempkes et al. |

| 8317103 | November 2012 | Foo et al. |

| 8577731 | November 2013 | Cope et al. |

| 8579203 | November 2013 | Lambeth et al. |

| 8590796 | November 2013 | Cloutier et al. |

| 8622309 | January 2014 | Mullen |

| 8712854 | April 2014 | Rafferty et al. |

| 8788418 | July 2014 | Spodak et al. |

| 8939357 | January 2015 | Perry |

| 8972298 | March 2015 | Kunz et al. |

| 9010644 | April 2015 | Workley |

| 9092767 | July 2015 | Andrews et al. |

| 9135545 | September 2015 | Lamba |

| 9183480 | November 2015 | Quigley et al. |

| 9224141 | December 2015 | Lamba et al. |

| 9311585 | April 2016 | Steshenko |

| 9619792 | April 2017 | Aaron et al. |

| 9679234 | June 2017 | Wade |

| 9922321 | March 2018 | Aaron et al. |

| 10037526 | July 2018 | Campos |

| 2003/0019942 | January 2003 | Blossom |

| 2003/0061157 | March 2003 | Hirka et al. |

| 2003/0065805 | April 2003 | Barnes, Jr. |

| 2004/0138999 | July 2004 | Friedman et al. |

| 2004/0158728 | August 2004 | Kim |

| 2005/0247785 | November 2005 | Bertin |

| 2006/0032906 | February 2006 | Sines |

| 2006/0077895 | April 2006 | Wright |

| 2006/0206488 | September 2006 | Distasio |

| 2008/0078831 | April 2008 | Johnson et al. |

| 2008/0177826 | July 2008 | Pitroda |

| 2008/0197201 | August 2008 | Manessis et al. |

| 2008/0222047 | September 2008 | Boalt |

| 2009/0043702 | February 2009 | Bennett |

| 2009/0063312 | March 2009 | Hurst |

| 2009/0159663 | June 2009 | Mullen et al. |

| 2009/0159667 | June 2009 | Mullen |

| 2009/0159671 | June 2009 | Mullen |

| 2009/0159672 | June 2009 | Mullen |

| 2009/0192904 | July 2009 | Patterson et al. |

| 2010/0063906 | March 2010 | Nelsen |

| 2010/0102125 | April 2010 | Gatto |

| 2010/0218009 | August 2010 | Hoeksel et al. |

| 2011/0131128 | June 2011 | Vaananen |

| 2011/0174874 | July 2011 | Poznansky et al. |

| 2011/0180598 | July 2011 | Morgan et al. |

| 2011/0231270 | September 2011 | Dykes et al. |

| 2011/0238510 | September 2011 | Rowen et al. |

| 2011/0240748 | October 2011 | Doughty |

| 2011/0270747 | November 2011 | Xu |

| 2011/0295750 | December 2011 | Rammal |

| 2011/0313840 | December 2011 | Mason et al. |

| 2012/0059718 | March 2012 | Ramer et al. |

| 2012/0123935 | May 2012 | Brudnicki |

| 2012/0310760 | December 2012 | Phillips et al. |

| 2013/0024364 | January 2013 | Shrivastava et al. |

| 2013/0024371 | January 2013 | Hariramani et al. |

| 2013/0030997 | January 2013 | Spodak et al. |

| 2013/0036048 | February 2013 | Campos |

| 2013/0048719 | February 2013 | Bennett |

| 2013/0117155 | May 2013 | Glasgo |

| 2013/0134216 | May 2013 | Spodak et al. |

| 2013/0134962 | May 2013 | Kamel et al. |

| 2013/0204777 | August 2013 | Irwin, Jr. et al. |

| 2013/0204793 | August 2013 | Kerridge et al. |

| 2013/0228616 | September 2013 | Bhosle et al. |

| 2013/0246218 | September 2013 | Gopalan |

| 2013/0248591 | September 2013 | Look et al. |

| 2013/0254227 | September 2013 | Shim et al. |

| 2013/0256403 | October 2013 | MacKinnon |

| 2013/0284806 | October 2013 | Margalit |

| 2013/0339166 | December 2013 | Baer |

| 2014/0074655 | March 2014 | Lim et al. |

| 2014/0074716 | March 2014 | Ni |

| 2014/0084059 | March 2014 | Sierchio et al. |

| 2014/0101035 | April 2014 | Tanner et al. |

| 2014/0149282 | May 2014 | Philliou et al. |

| 2014/0159869 | June 2014 | Zumsteg et al. |

| 2014/0214567 | July 2014 | Llach et al. |

| 2014/0217174 | August 2014 | Lo |

| 2015/0058146 | February 2015 | Gaddam et al. |

| 2015/0058940 | February 2015 | Robison |

| 2015/0069126 | March 2015 | Leon |

| 2015/0073983 | March 2015 | Bartenstein |

| 2015/0127553 | May 2015 | Sundaram et al. |

| 2015/0134513 | May 2015 | Olson et al. |

| 2015/0186871 | July 2015 | Laracey |

| 2015/0205550 | July 2015 | Lee |

| 2016/0086166 | March 2016 | Pomeroy et al. |

| H05333966 | Dec 1993 | JP | |||

| 2015/061005 | Apr 2015 | WO | |||

| 2016/003831 | Jan 2016 | WO | |||

Other References

|

Non-Final Office Action dated Aug. 23, 2017, for U.S. Appl. No. 14/455,225, of Templeton, T., et al., filed Aug. 8, 2014. cited by applicant . Final Office Action dated Sep. 29, 2017, for U.S. Appl. No. 14/455,220, of Templeton, T., et al., filed Aug. 8, 2014. cited by applicant . U.S. Appl. No. 14/168,274 of Odawa, A. et al., filed Jan. 30, 2014. cited by applicant . U.S. Appl. No. 14/455,220 of Templeton, T. et al., filed Aug. 8, 2014. cited by applicant . U.S. Appl. No. 14/455,225 of Templeton, T. et al., filed Aug. 8, 2014. cited by applicant . Non-Final Office Action dated Jan. 20, 2017, for U.S. Appl. No. 14/168,274, of Odawa, A.W., et al., filed Jan. 30, 2014. cited by applicant . Non-Final Office Action dated Apr. 27, 2017, for U.S. Appl. No. 14/455,220, of Templeton, T., et al., filed Aug. 8, 2014. cited by applicant . Final Office Action dated May 19, 2017, for U.S. Appl. No. 14/168,274, of Odawa, A.W., et al., filed Jan. 30, 2014. cited by applicant . "Bluetooth Accessory Design Guidelines for Apple Products," Apple Inc., dated Sep. 18, 2013, Retrieved from the Internet URL: https://developer.apple.com/hardwaredrivers/BluetoothDesignGuidelines.pdf- , pp. 1-40. cited by applicant . Chiraag, "A payment Card that Changes Magnetic Stripe via Smartphone," published Nov. 12, 2013, Retrieved from the Internet URL: https://letstalkpayments.com/card-changes-magnetic-stripe-via-smartphone/- , on Jan. 3, 2018, pp. 1-6. cited by applicant . Non-Final Office Action dated Jan. 9, 2015, for U.S. Appl. No. 14/145,895 of Aaron, P., et al., filed Dec. 31, 2013. cited by applicant . Non-Final Office Action dated Feb. 6, 2015, for U.S. Appl. No. 14/478,522, of Lamba, K., filed Sep. 5, 2014. cited by applicant . Non-Final Office Action dated Feb. 18, 2015, for U.S. Appl. No. 14/244,632, of Quigley, O.S.C., et al., filed Apr. 3, 2014. cited by applicant . Non-Final Office Action dated May 12, 2015, for U.S. Appl. No. 14/189,869 of Lamba, K., et al., filed Feb. 25, 2014. cited by applicant . Non-Final Office Action dated May 26, 2015, for U.S. Appl. No. 14/225,338, of Aaron, P., et al., filed Mar. 25, 2014. cited by applicant . Non-Final Office Action dated May 27, 2015, for U.S. Appl. No. 14/197,704, of Lamba, K., et al., filed Mar. 5, 2014. cited by applicant . Notice of Allowance dated Jun. 3, 2015, for U.S. Appl. No. 14/478,522, of Lamba, K., filed Sep. 5, 2014. cited by applicant . Notice of Allowance dated Jul. 6, 2015, for U.S. Appl. No. 14/244,632, of Quigley, O.S.C., et al., filed Apr. 3, 2014. cited by applicant . Final Office Action dated Aug. 18, 2015, for U.S. Appl. No. 14/145,895, of Aaron, P., et al., filed Dec. 31, 2013. cited by applicant . Notice of Allowance dated Sep. 3, 2015, for U.S. Appl. No. 14/244,632, of Quigley, O.S.C., et al., filed Apr. 3, 2014. cited by applicant . Notice of Allowance dated Sep. 18, 2015, for U.S. Appl. No. 14/197,704, of Lamba, K., et al., filed Mar. 5, 2014. cited by applicant . Non-Final Office Action dated Sep. 23, 2015, for U.S. Appl. No. 14/478,601, of Steshenko, R.T.S. V., filed Sep. 5, 2014. cited by applicant . Final Office Action dated Oct. 2, 2015, for U.S. Appl. No. 14/225,338, of Aaron, P., et al., filed Mar. 25, 2014. cited by applicant . Advisory Action dated Dec. 31, 2015, for U.S. Appl. No. 14/225,338, of Aaron, P., et al., filed Mar. 25, 2014. cited by applicant . Non-Final Office Action dated Jan. 22, 2016, for U.S. Appl. No. 14/189,869, of Lamba, K., et al., filed Feb. 25, 2014. cited by applicant . Notice of Allowance dated Feb. 8, 2016, for U.S. Appl. No. 14/478,601, of Steshenko, R.T.S.V., filed Sep. 5, 2014. cited by applicant . Non-Final Office Action dated Mar. 24, 2016, for U.S. Appl. No. 14/145,895, of Aaron, P., et al., filed Dec. 31, 2013. cited by applicant . Non-Final Office Action dated May 9, 2016, for U.S. Appl. No. 14/225,338, of Aaron, P., et al., filed Mar. 25, 2014. cited by applicant . Final Office Action dated Jul. 18, 2016, for U.S. Appl. No. 14/189,869, of Lamba, K., et al., filed Feb. 25, 2014. cited by applicant . Non-Final Office Action dated Aug. 4, 2016, for U.S. Appl. No. 14/321,429, of Wade, J., filed Jul. 1, 2014. cited by applicant . Final Office Action dated Sep. 1, 2016, for U.S. Appl. No. 14/225,338, of Aaron, P., et al., filed Mar. 25, 2014. cited by applicant . Advisory Action dated Oct. 11, 2016, for U.S. Appl. No. 14/189,869, of Lamba, K., et al., filed Feb. 25, 2014. cited by applicant . Final Office Action dated Oct. 12, 2016, for U.S. Appl. No. 14/145,895, of Aaron, P., et al., filed Dec. 31, 2013. cited by applicant . Non-Final Office Action dated Nov. 3, 2016, for U.S. Appl. No. 14/225,342, of Lamba, K., et al., filed Mar. 25, 2014. cited by applicant . Notice of Allowance dated Nov. 8, 2016, for U.S. Appl. No. 14/225,338, of Aaron, P., et al., filed Mar. 25, 2014. cited by applicant . Advisory Action dated Dec. 22, 2016, for U.S. Appl. No. 14/145,895, of Aaron, P., et al., filed Dec. 31, 2013. cited by applicant . Notice of Allowance dated Feb. 7, 2017, for U.S. Appl. No. 14/321,429, of Wade, J., filed Jul. 1, 2014. cited by applicant . Final Office Action dated Mar. 10, 2017, for U.S. Appl. No. 14/225,342, of Lamba, K., et al., filed Mar. 25, 2014. cited by applicant . Non-Final Office Action dated Mar. 13, 2017, for U.S. Appl. No. 14/189,869, of Lamba, K., et al., filed Feb. 25, 2014. cited by applicant . Non-Final Office Action dated Apr. 12, 2017, for U.S. Appl. No. 14/145,895, of Aaron, P., et al., filed Dec. 31, 2013. cited by applicant . Advisory Action dated Jun. 9, 2017, for U.S. Appl. No. 14/225,342, of Lamba, K., et al., filed Mar. 25, 2014. cited by applicant . Non-Final Office Action dated Jun. 29, 2017, for U.S. Appl. No. 14/189,869, of Lamba, K., et al., filed Feb. 25, 2014. cited by applicant . Notice of Allowance dated Nov. 9, 2017, for U.S. Appl. No. 14/145,895, of Aaron, P., et al., filed Dec. 31, 2013. cited by applicant . Advisory Action dated Dec. 11, 2017, for U.S. Appl. No. 14/455,220, of Templeton, T., et al., filed Aug. 8, 2014. cited by applicant . Final Office Action dated Jan. 8, 2018, for U.S. Appl. No. 14/189,869, of Lamba, K., et al.al., filed Feb. 25, 2014. cited by applicant . Office Action for European Patent Application No. 14855987.5, dated Mar. 23, 2018. cited by applicant . Advisory Action dated Apr. 12, 2018, for U.S. Appl. No. 14/189,869, of Lamba, K., et al., filed Feb. 25, 2014. cited by applicant . Final Office Action dated May 2, 2018, for U.S. Appl. No. 14/455,225, of Templeton, T., et al., filed Aug. 8, 2014. cited by applicant . International Search Report and Written Opinion for International Application No. PCT/US2014/058447, dated Jan. 15, 2015. cited by applicant . International Search Report and Written Opinion for International Application No. PCT/US2015/038165, dated Sep. 17, 2015. cited by applicant . Extended European Search Report for European Patent Application No. 14855987.5, dated May 10, 2017. cited by applicant . Non-Final Office Action dated Oct. 5, 2018, for U.S. Appl. No. 14/189,869, of Lamba, K., et al., filed Feb. 25, 2014. cited by applicant . Advisory Action dated Jul. 25, 2018, for U.S. Appl. No. 14/455,225, of Templeton, T., et al., filed Aug. 8, 2014. cited by applicant . Office Action for European Patent Application No. 14855987.5, dated Sep. 14, 2018. cited by applicant . Notice of Allowance dated Dec. 27, 2018, for U.S. Appl. No. 14/455,225, of Templeton T., et al., filed Aug. 8, 2014. cited by applicant . Notice of Allowance dated Jan. 7, 2019, for U.S. Appl. No. 14/455,220, of Templeton, T., et al., filed Aug. 8, 2014. cited by applicant . Final Office Action dated Feb. 25, 2019, for U.S. Appl. No. 14/189,869, of Lamba, K., et al., filed Feb. 25, 2014. cited by applicant . Advisory Action dated May 7, 2019, for U.S. Appl. No. 14/189,869, of Lamba, K., et al., filed Feb. 25, 2014. cited by applicant . Non-Final Action dated May 30, 2019, for U.S. Appl. No. 15/436,478, of Kartik Lamba filed Feb. 17, 2017. cited by applicant. |

Primary Examiner: Iwarere; Oluseye

Attorney, Agent or Firm: Schott, P.C.

Claims

The invention claimed is:

1. A method comprising: receiving, by an electronic system, a request regarding an emulation rule of a plurality of emulation rules for one of a plurality of payment cards to be emulated by a card that is external to the electronic system; creating or modifying, by the electronic system, the emulation rule in response to the request; and transmitting, to the card, the created or modified emulation rule when an update has been made to the plurality of emulation rules, wherein the created or modified emulation rule is applied to the card in response to a trigger event, wherein application of different emulation rules, corresponding to the plurality of payment cards, to the card facilitates a user of the card with benefits from use of the plurality of payment cards with a single card, and wherein the card has an appearance of a payment card and contains a processing element and memory.

2. The method of claim 1, further comprising: receiving a second request regarding the plurality of emulation rules for one of the plurality of payment cards; and combining the plurality of emulation rules by Boolean operators in response to the second request.

3. The method of claim 1, further comprising: receiving a second request regarding the plurality of emulation rules for one of the plurality of payment cards; and prioritizing the plurality of emulation rules in response to the second request.

4. The method of claim 1, further comprising receiving a second request regarding a selection rule for selecting one of the plurality of payment cards for emulation.

5. The method of claim 4, wherein the selection rule involves a time, a location, or a business.

6. The method of claim 4, further comprising creating, modifying, or deleting the selection rule in response to the second request.

7. The method of claim 4, further comprising: receiving a third request regarding a plurality of selection rules for one of the plurality of payment cards; and combining the plurality of selection rules or prioritizing the plurality of selection rules in response to the third request.

Description

BACKGROUND

A consumer today may use several types of payment cards, such as a credit card, a gift card, and an ATM card. Different types of payment cards may be well suited for different occasions. For example, a consumer would want to use an ATM card when no credit is accepted or use a gift card from a merchant in a business location of the merchant. It can be inconvenient and unwieldy to manage a number of payment cards. In addition, the use of each payment card often needs to be specifically controlled. For example, a consumer would want to deactivate a payment card when it is stolen, and a parent may want to limit the use of a payment card given to a child.

BRIEF DESCRIPTION OF THE DRAWINGS

Embodiments of the present invention will be described and explained through the use of the accompanying drawings in which:

FIG. 1A illustrates an example environment in which a consumer sets up a proxy card profile using an electronic device.

FIG. 1B illustrates an example proxy card profile.

FIG. 1C illustrates an example environment in which a consumer uses a proxy card for payment at a point-of-sale (POS) system in a store.

FIG. 2 is a flow diagram illustrating an example process performed by an electronic device for setting up a proxy card profile.

FIG. 3 is a flow diagram illustrating an example process performed by a proxy card for selecting and emulating one of a plurality of payment cards.

FIG. 4 is a high-level block diagram showing an example of a processing device that can implement techniques described herein.

DETAILED DESCRIPTION

In this description, references to "an embodiment", "one embodiment" or the like, mean that the particular feature, function, structure or characteristic being described is included in at least one embodiment of the technique introduced here. Occurrences of such phrases in this specification do not necessarily all refer to the same embodiment. On the other hand, the embodiments referred to also are not necessarily mutually exclusive.

Introduced here is a technique related to a proxy card which emulates different payment cards according to different rules. Using this technique, a consumer benefits from the use of multiple payment cards with the single proxy card. Furthermore, the consumer can manage the selection of a payment card for emulation and the emulation of each selected payment card with various rules based on time, location, business, or other factor(s). Specifically, the consumer can create, edit or delete the various rules for each payment card using an electronic device, such as a mobile phone, which transmits the resulting rules to the proxy card at various points in time.

In certain embodiments a "proxy card" is a card that can emulate one or more other cards/accounts (e.g., payment cards/accounts). The proxy card is essentially identical or similar in appearance to a payment card, such as a credit card, a debit card, or a gift card, being roughly of wallet size and having an identification component, such as a magnetic stripe or integrated circuit (IC) chip, which can hold information identifying one or more payment cards. In addition, in some embodiments the proxy card includes a processor and memory capable of computation, processing and storage functionalities. The proxy card may also include input and output elements, such as a button or switch for input and a liquid-crystal display (LCD) or light emitting diode (LED) display for output. Furthermore, the proxy card includes a communication interface to carry out short-range (typically less than 100 meters) wireless communication, which may be implemented by Bluetooth Low Energy (BLE), for example. These features enable the proxy card to emulate each of multiple payment cards according to specified rules.

In some embodiments, the proxy card stores in the memory one or more rules governing the emulation of each payment card. It also stores in the memory identification information for each payment card. Upon accepting a selection of one of the multiple payment cards, through the input element or the communication interface, the processor configures the identification component to correspond to the selected payment card in accordance with emulation rules associated with the payment card. The proxy card also displays any status update or error message through the output element.

FIG. 1A illustrates an example environment in which a consumer sets up a proxy card profile by using an electronic device. In some embodiments, before using a proxy card, the consumer needs to register one or more payment cards to be emulated by the proxy card and sets up a profile for the proxy card on a server system 108. One way to register each of the payment cards is through an electronic sensing device, such as a Radio-Frequency Identification (RFID) scanner or a Near Field Communication (NFC) scanner, attached to an electronic device, such as a mobile phone 104, which is capable of communicating with the server system 108. The communication between the electronic sensing device and the proxy card can be through a short-range wireless link, such as standard Bluetooth, BLE, Wi-Fi, RFID, and NFC, or direct access to the identification component on the proxy card. The communication between the electronic device and the server system 108 can be through any network link, such as the Internet. During registration, the electronic sensing device receives information from each payment card, and the electronic device forwards the received information to the server system 108, which then saves the forwarded information in databases.

In some embodiments, the server system 108 provides a client device with a graphical user interface (GUI) for the management of a proxy card profile. The GUI can be displayed on any of various client electronic devices, such as a mobile phone 104, a tablet, a laptop, or a desktop. The consumer can create, edit, or delete a proxy card profile on the server system 108. FIG. 1B illustrates an example proxy card profile. The proxy card profile includes two sections, a selection section 130 with rules for selecting one of the registered payment cards to emulate, and an emulation section 132 with rules for emulating each of the registered payment cards. The server system 108 can prepopulate the emulation section with information regarding each of the registered payment cards. The server system 108 can also add a "blank card" that corresponds to a state of no emulation to be distinguished from a real payment card. This blank card can be selected when no payment card is to be emulated by the proxy card.

In the selection section 130, each line corresponds to a selection rule. The selection rules specify how to select one or more payment cards out of a group of payment cards. The selection rules can be expressed in various forms, with regard to time, location, business, or other factors. Some examples are as follows: 1) selecting a particular payment card after normal business hours; 2) selecting a gift card from a particular merchant when the proxy card is located within a business establishment of the merchant; 3) selecting a payment card with a low foreign exchange rate when the proxy card 102 is located in a foreign country; 4) selecting a particular payment card when the proxy card is located at a business in a particular industry (e.g., entertainment, restaurant, etc.); 5) selecting a credit card instead of a debit card under a specified condition; 6) selecting a payment card in the consumer's name before selecting a payment card not in the consumer's name; 7) skipping a payment card that has been used more than a specified number of times or for transactions totaling more than a specified amount of money during a period of time.

In some embodiments, the selection rules can incorporate or be combined with Boolean operators. They can also be prioritized so that conflicts between them can be resolved. In some embodiments, while the selection rules enable an automatic selection of a payment card, they can be overridden by the consumer at the time of using the proxy card, as discussed below.

In the emulation section 132, each row corresponds to a set of emulation rules associated with a registered payment card, i.e., a payment card associated with the proxy card. These emulation rules control the emulation of a payment card, controlling how the payment card is emulated, for security, efficiency, and other purposes. The emulation rules can also be expressed in various forms, with regard to time, location, business, or other factors.

In some embodiments, regarding time, an emulation rule specifies that the emulation is on or off at a designated time or relative to the occurrence of an event, or the emulation lasts for a specified period of time, etc. Such an event can be, for example, the push of a button on the proxy card to signify the beginning of emulation, the accessing of the identification component on the proxy card, which normally signifies the end of emulation, the entering or exiting of a business location, the opening or closing of a business location, etc. Regarding location, an emulation rule specifies that the emulation is on or off at a designated location, near a particular object, etc. A designated location can be as specific as an address or the name of a business establishment or as broad as a category of businesses, such as a restaurant, or the name of a geographic area, such as New York City. An object in a scenario can be, for example, a mobile electronic device that also belongs to the consumer and communicates with the server system 108, such as a smart phone. The presence of such an object near the proxy card increases the possibility that the proxy card is in the possession of its rightful owner. Regarding business, an emulation rule specifies that the emulation is on or off depending on the nature of the business operating at the current location. Various aspects of the business can be taken into consideration, such as the size, the credit history, the customer service, etc.

In some embodiments, for each of the registered payment cards, multiple emulation rules can be combined. For example, a parent who controls the use of the proxy card by a child may create a first rule combination which indicates that a payment card is emulated for one hour from the time the button on the proxy card 102 is pushed when the business operating at the current location is a video game store, and a second rule combination which indicates that the payment card is emulated during the entire time the proxy card is on the premises of the business operating at the current location when the business is a bookstore. Furthermore, multiple emulation rules or combinations of emulation rules can be prioritized so that conflicts between them can be resolved.

In some embodiments, certain data regarding the registered payment cards, including the identification information and the proxy card profile, are transmitted from the server system 108 to the proxy card at various times. For example, the data regarding the registered payment cards can be transmitted to the proxy card 102 periodically or whenever a new payment card is registered and an existing payment card is un-registered. The proxy card profile similarly can be transmitted periodically or whenever a certain amount of update has been made to the proxy card profile. The transmission can result from a push from the server system 108 or a pull from the proxy card. Communication between the server system 108 and the proxy card can be through an electronic device that also belongs to the consumer and that communicates with the server system 108, such as the mobile phone 104. Specifically, the communication between the server system 108 and the mobile phone 104 can be through a cellular network and another network such as the Internet, for example, and the communication between the mobile phone 104 and the proxy card 102 can be through a short-range wireless link, which can be implemented by BLE.

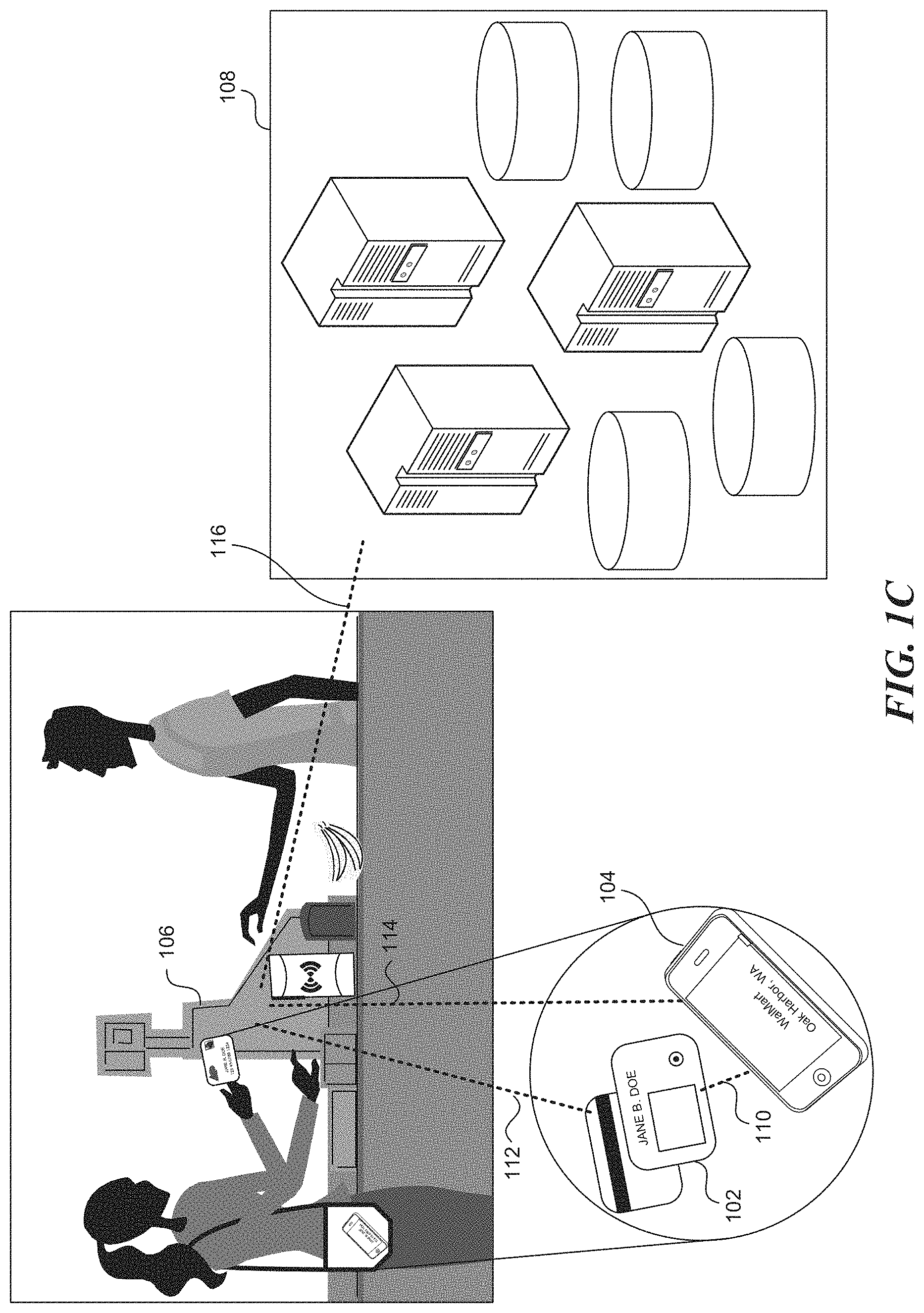

FIG. 1C illustrates an example environment in which a consumer uses a proxy card for payment at a POS system in a store. In some embodiments, when the selection rules do not determine a payment card to emulate by default, the proxy card 102 displays a prompt for the consumer to select a payment card to emulate. The proxy card 102 allows the consumer to select a payment card using a button, a navigation key or other input element on the proxy card. A consumer can also make a selection using an electronic device, such as a mobile phone 104, which then communicates the selection to the proxy card 102. Once a payment card is selected for emulation, the associated emulation rules are applied.

In some embodiments, in applying the selection or emulation rules, the proxy card 102 determines whether a specific event has occurred, such as the push of a button on the proxy card 102 or the closing of a business location where the proxy card 102 is located. The proxy card 102 can detect the occurrence of an event or receive information from a nearby electronic device, such as the mobile phone 104, regarding the occurrence of an event through a short-range wireless link, such as BLE. As one example, the proxy card 102 can contain special hardware, such as an accelerometer, which detects the pressure exerted on or the speed of the proxy card 102, thereby determining whether the proxy card 102 is being swiped through a magnetic card reader. As another example, when the proxy card 102 is swiped through a magnetic card reader attached to the POS system 106, the information read from a magnetic stripe on the proxy card 102 can be transmitted from the POS system 106 through the server system 108 and the mobile phone 104 and back to the proxy card 102. The proxy card 102 also determines whether it is in a particular location or near a particular object. As one example, the proxy card 102 determines whether it is near a mobile phone of the consumer by requesting the mobile phone 104 to transmit its mobile phone number, where both the request and the response can be via a short-range wireless link, such as BLE. Next, the proxy card 102 determines whether the transmitted number matches the number for the mobile phone 104 previously stored on the proxy card 102. As another example, the proxy card 102 determines whether it is in a particular location by requesting the mobile phone 104, which has Global Positioning System (GPS) capabilities, to transmit information regarding its current location, using a short-range wireless link such as mentioned above. In addition, the proxy card 102 determines the nature of the business operating at the current location. The proxy card 102 can similarly rely on the mobile phone 104 to obtain such information directly, from a web search, for example, or by contacting the server system 108, which stores data regarding merchants and businesses. The proxy card 102 can also request a POS system 106 near the current location to transmit information regarding the business, such as a Merchant Category Code (MCC), using a short-range wireless link.

In some embodiments, as a result of applying the emulation rules, the proxy card 102 begins and ends the emulation of the selected payment card accordingly. It is possible that when the proxy card 102 is actually used, where the identification component is accessed by the POS system 106, for example, the emulation of the selected payment card is off according to the associated emulation rules. In that case, the proxy card 102 or the POS system 106 can display an error message. In response, the consumer may manually select another payment card, re-initiate an event, such as pushing a button on the proxy card 102, or take other actions to remedy the situation. The proxy card 102 can also automatically select the next payment card based on the selection rules.

In some embodiments, when the proxy card 102 is not emulating any payment card (e.g., because it is set to emulate the blank card, because the emulation is off for the selected payment card, or for some other reason), the proxy card 102 turns on a fraud protection feature. For example, the proxy card 102 displays an error message in an LCD on the proxy card 102 or sends an alert to the mobile phone 104 when the number of attempts to use the proxy card exceeds a predetermined threshold during a certain timeframe or duration.

FIG. 2 is a flow diagram illustrating an example process performed by an electronic system for managing emulation rules that are part of a proxy card profile for a proxy card. The proxy card is used to emulate a group of payment cards, each being, for example, a credit card, a debit card, a gift card, an ATM card, a fleet card, etc. In step 202, an electronic system receives a request from a user of the electronic system, typically the owner of the proxy card, regarding one or more emulation rules associated with one of the group of payment cards. The electronic system can be or include, for example, a server system that stores all the emulation rules. It can also be or include a client electronic device, such as a mobile phone, tablet computer, laptop computer, or desktop computer, which supports a GUI for managing the emulation rules. In step 204, the electronic system creates, modifies, or deletes one or more emulation rules in response to the request. In working with an emulation rule, the electronic system allows the user to specify how emulation is performed with respect to time, location, business, and other factors. In step 206, the electronic system also combines or prioritizes multiple emulation rules in response to the request. It allows the user to specify which Boolean operators to use in combining emulation rules. It also allows the user to assign weights to individual emulation rules. In another example process, this step may be optional.

In step 208, the electronic system transmits existing emulation rules associated with the payment card to the proxy card. When the electronic system, such as the mobile phone that also belongs to the user, is near the proxy card, the electronic system can transmit the emulation rules directly using a short-range wireless link, such as BLE, Bluetooth, Wi-Fi, NFC or RFID. When the electronic system is not near the user, it can transmit the emulation rules to an electronic device that is near the user using a typical network interface and relies on that electronic device for further transmission to the proxy card. The transmission can be done based on a predetermined schedule, whenever emulation rules are updated, and so on. The emulation rules associated with the payment card may be transmitted by themselves or together with additional emulation rules.

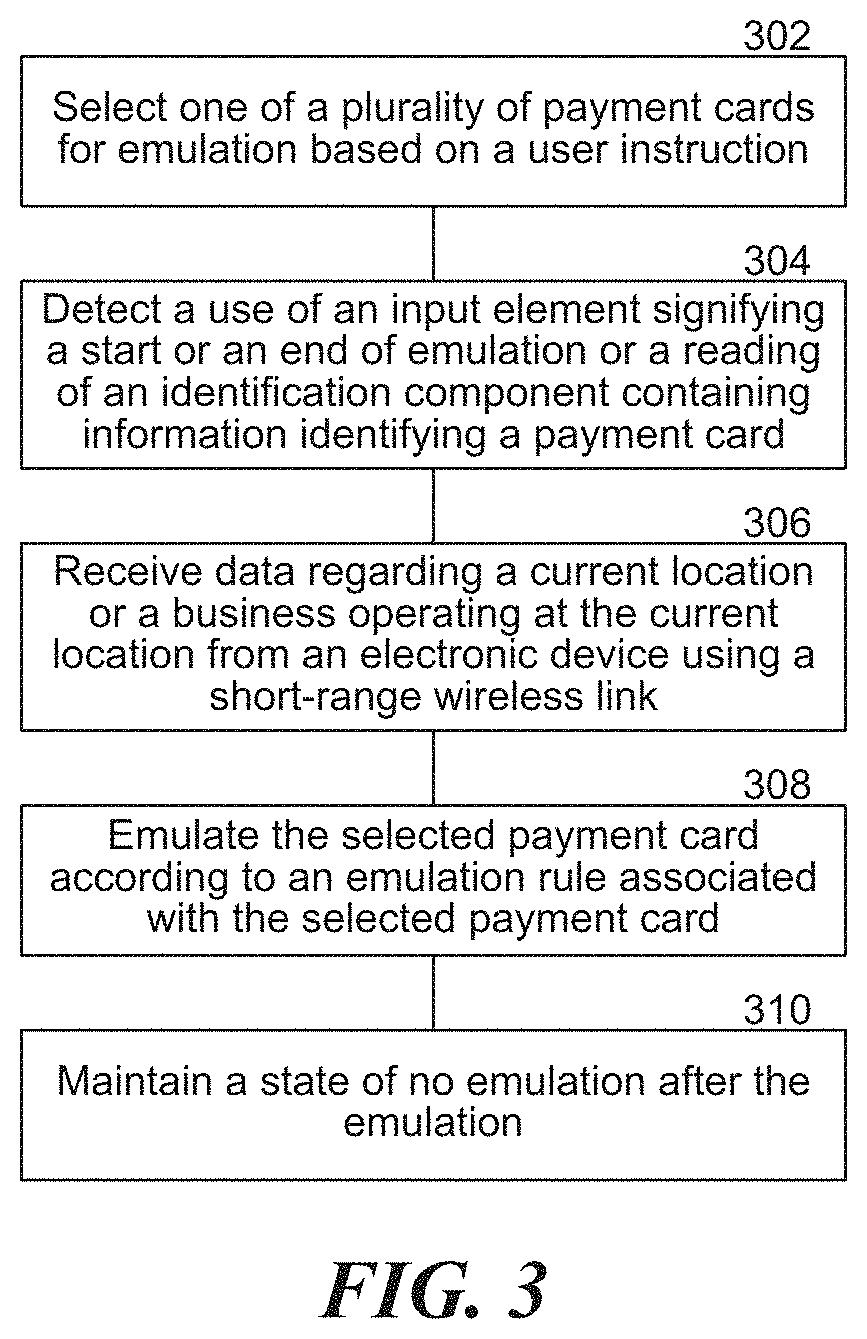

FIG. 3 is a flow diagram illustrating an example process performed by a proxy card for selecting and emulating one of a plurality of payment cards. The proxy card is used to emulate any of a group of payment cards, each being, for example, a credit card, a debit card, a gift card, an ATM card, a fleet card, etc. The proxy card contains an identification element, such as a magnetic stripe, or an IC chip (e.g., such as commonly used in a smartcard or in an RFID tag), which may hold information corresponding to a payment card. The proxy card also contains a communication element supporting short-range wireless communication. In addition, it may contain an input element, such as a button or a navigator key, and an output element, such as a display, for various purposes.

In step 302, the proxy card selects one card of the group of payment cards to emulate, based on an instruction from a user of the proxy card. The proxy card can preselect a payment card according to certain selection rules, but the user can manually select a card using the input element on the proxy card. Once a selection of a payment card is made, the proxy card needs to apply the emulation rules associated with the selected payment card. An emulation rule specifies how a payment card should be emulated with respect to time, location, business or other factors. Therefore, the proxy card identifies the current time, the current location, and the business operating at the current location in order to apply the emulation rules. In terms of time, in step 304, the proxy card detects any use of the input element for signifying a start or an end of emulation or any access of the identification component, which can correspond to an end of emulation. In terms of location and business, in step 306, the proxy card receives from a nearby electronic device, such as a mobile phone or a POS system of a store, data regarding the current location or the business operating at the current location using a short-range wireless link, such as BLE. Having identified the current time, the current location, and the business operating at the current location, in step 308, the proxy card applies the emulation rules associated with the selected payment card to determine how to emulate the selected payment card. Specifically, the proxy card configures the identification element to correspond to the selected payment card for a specific timeframe. Outside the timeframe, in step 310, the proxy card performs no emulation by keeping the identification element in a blank state that does not correspond to any payment card. This measure provides a high level of security. An alternative measure is for the proxy card to emulate a particular card by default.

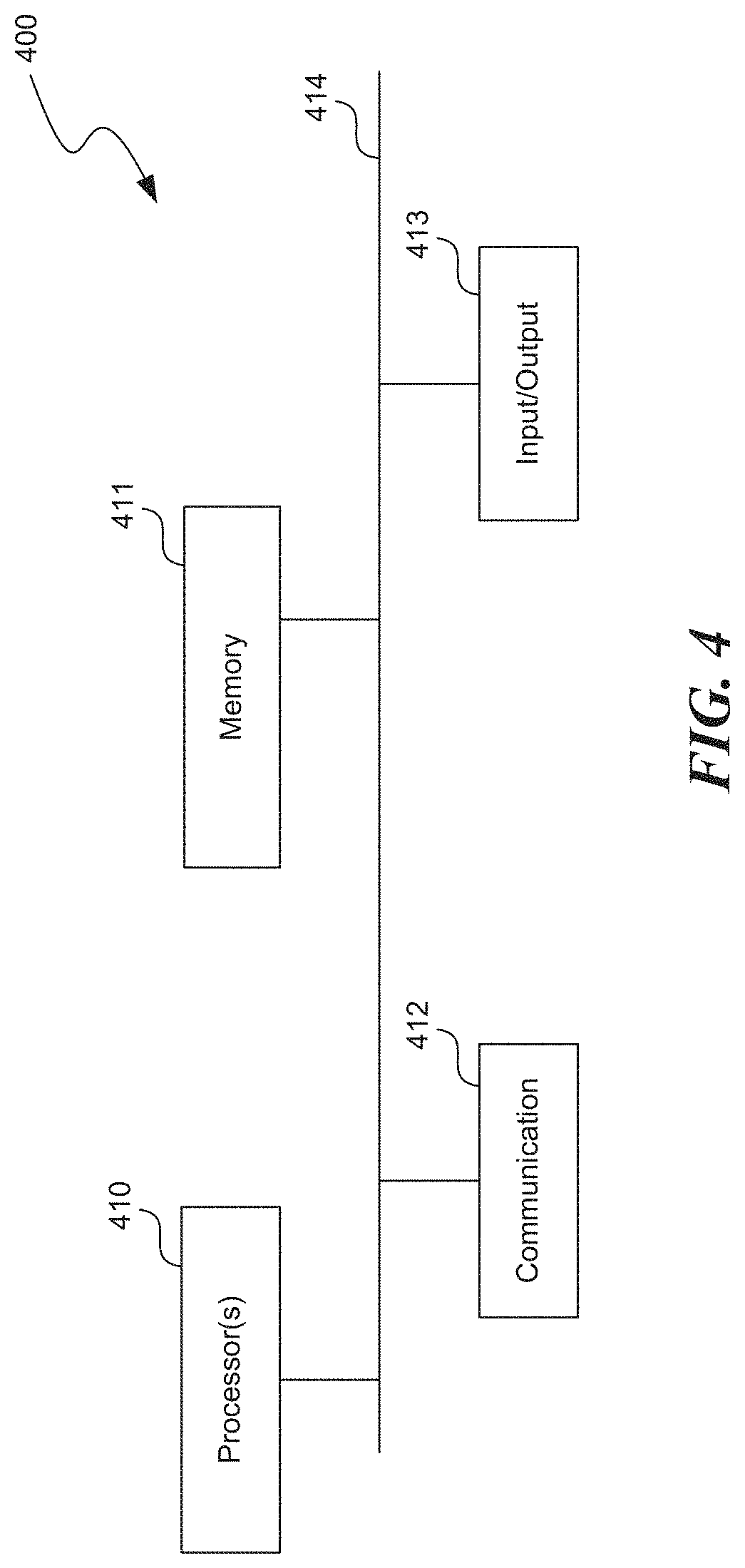

FIG. 4 is a high-level block diagram showing an example of a processing device 400 that can represent any of the devices described above, such as a proxy card, an electronic device, and a server system. Any of these systems may include two or more processing devices such as represented in FIG. 4, which may be coupled to each other via a network or multiple networks.

In the illustrated embodiment, the processing system 400 includes one or more processors 410, memory 411, a communication device 412, and one or more input/output (I/O) devices 413, all coupled to each other through an interconnect 414. In some embodiments, the processing system 400 may not have any I/O devices 413. The interconnect 414 may be or include one or more conductive traces, buses, point-to-point connections, controllers, adapters and/or other conventional connection devices. The processor(s) 410 may be or include, for example, one or more general-purpose programmable microprocessors, microcontrollers, application specific integrated circuits (ASICs), programmable gate arrays, or the like, or a combination of such devices. The processor(s) 410 control the overall operation of the processing device 400. Memory 411 may be or include one or more physical storage devices, which may be in the form of random access memory (RAM), read-only memory (ROM) (which may be erasable and programmable), non-volatile memory such as flash memory, miniature hard disk drive, or other suitable type of storage device, or a combination of such devices. Memory 411 may store data and instructions that configure the processor(s) 410 to execute operations in accordance with the techniques described above. The communication device 412 may be or include, for example, an Ethernet adapter, cable modem, Wi-Fi adapter, cellular transceiver, Bluetooth transceiver, or the like, or a combination thereof. For an electronic sensing device of a merchant, or a proxy card or mobile device of a consumer, the communication device 412 supports at least one technology for short-range wireless communication. Depending on the specific nature and purpose of the processing device 400, the I/O devices 413 can include devices such as a display (which may be a touch screen display), audio speaker, keyboard, mouse or other pointing device, microphone, camera, etc.

Unless contrary to physical possibility, it is envisioned that (i) the methods/steps described above may be performed in any sequence and/or in any combination, and that (ii) the components of respective embodiments may be combined in any manner.

The techniques introduced above can be implemented by programmable circuitry programmed/configured by software and/or firmware, or entirely by special-purpose circuitry, or by a combination of such forms. Such special-purpose circuitry (if any) can be in the form of, for example, one or more application-specific integrated circuits (ASICs), programmable logic devices (PLDs), field-programmable gate arrays (FPGAs), etc.

Software or firmware for use in implementing the techniques introduced here may be stored on a machine-readable storage medium and may be executed by one or more general-purpose or special-purpose programmable microprocessors. A "machine-readable medium", as the term is used herein, includes any mechanism that can store information in a form accessible by a machine (a machine may be, for example, a computer, network device, cellular phone, personal digital assistant (PDA), manufacturing tool, any device with one or more processors, etc.). For example, a machine-accessible medium includes recordable/non-recordable media (e.g., read-only memory (ROM); random access memory (RAM); magnetic disk storage media; optical storage media; flash memory devices; etc.), etc.

Although the present invention has been described with reference to specific exemplary embodiments, it will be recognized that the invention is not limited to the embodiments described but can be practiced with modification and alteration within the spirit and scope of the appended claims. Accordingly, the specification and drawings are to be regarded in an illustrative sense rather than a restrictive sense.

* * * * *

References

D00000

D00001

D00002

D00003

D00004

D00005

D00006

XML

uspto.report is an independent third-party trademark research tool that is not affiliated, endorsed, or sponsored by the United States Patent and Trademark Office (USPTO) or any other governmental organization. The information provided by uspto.report is based on publicly available data at the time of writing and is intended for informational purposes only.

While we strive to provide accurate and up-to-date information, we do not guarantee the accuracy, completeness, reliability, or suitability of the information displayed on this site. The use of this site is at your own risk. Any reliance you place on such information is therefore strictly at your own risk.

All official trademark data, including owner information, should be verified by visiting the official USPTO website at www.uspto.gov. This site is not intended to replace professional legal advice and should not be used as a substitute for consulting with a legal professional who is knowledgeable about trademark law.