Machine Learning Portfolio Simulating and Optimizing Apparatuses, Methods and Systems

Walia; Samarjit ; et al.

U.S. patent application number 17/383329 was filed with the patent office on 2022-04-07 for machine learning portfolio simulating and optimizing apparatuses, methods and systems. The applicant listed for this patent is FMR LLC. Invention is credited to Deepak Bhaskaran, Jiawen Dai, Aaron Gao, Yongsheng Gao, Niyu Jia, Songyang Li, Peng Sun, Christine Thompson, Samarjit Walia, Xiao Zhang.

| Application Number | 20220108401 17/383329 |

| Document ID | / |

| Family ID | 1000006066977 |

| Filed Date | 2022-04-07 |

View All Diagrams

| United States Patent Application | 20220108401 |

| Kind Code | A1 |

| Walia; Samarjit ; et al. | April 7, 2022 |

Machine Learning Portfolio Simulating and Optimizing Apparatuses, Methods and Systems

Abstract

The Machine Learning Portfolio Simulating and Optimizing Apparatuses, Methods and Systems ("MLPO") transforms machine learning simulation request, decision tree ensembles training request, expected returns calculation request, portfolio construction request, predefined scenario construction request, portfolio returns visualization request inputs via MLPO components into machine learning simulation response, decision tree ensembles training response, expected returns calculation response, portfolio construction response, predefined scenario construction response, portfolio returns visualization response outputs. An asset return metrics calculation request datastructure is obtained. The number of sessions to utilize for calculating asset return metrics data is determined. An assets range for a session is determined and asset database table records from the assets range are processed in batches using an assets batch database table, a factor simulations batch database table, and a factor exposures batch database table. Expected returns for each batch of the assets range are calculated using the batch tables via a parallel SQL query.

| Inventors: | Walia; Samarjit; (Lextington, MA) ; Gao; Aaron; (Wayland, MA) ; Bhaskaran; Deepak; (Cary, NC) ; Dai; Jiawen; (Somerville, MA) ; Zhang; Xiao; (Norwood, MA) ; Sun; Peng; (Morrisville, NC) ; Thompson; Christine; (Bedford, MA) ; Jia; Niyu; (Revere, MA) ; Li; Songyang; (Somerville, MA) ; Gao; Yongsheng; (Shrewsbury, MA) | ||||||||||

| Applicant: |

|

||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Family ID: | 1000006066977 | ||||||||||

| Appl. No.: | 17/383329 | ||||||||||

| Filed: | July 22, 2021 |

Related U.S. Patent Documents

| Application Number | Filing Date | Patent Number | ||

|---|---|---|---|---|

| 63055876 | Jul 23, 2020 | |||

| Current U.S. Class: | 1/1 |

| Current CPC Class: | G06N 3/0454 20130101; G06F 16/26 20190101; G06F 16/2433 20190101; G06Q 30/0206 20130101; G06Q 40/06 20130101; G06F 16/2386 20190101 |

| International Class: | G06Q 40/06 20060101 G06Q040/06; G06F 16/242 20060101 G06F016/242; G06F 16/23 20060101 G06F016/23; G06F 16/26 20060101 G06F016/26; G06Q 30/02 20060101 G06Q030/02; G06N 3/04 20060101 G06N003/04 |

Claims

1. A database calculation engine apparatus, comprising: a memory; a component collection in the memory; a processor disposed in communication with the memory and configured to issue a plurality of processor-executable instructions from the component collection, the processor-executable instructions structured as: obtain, via at least one processor, an asset return metrics calculation request datastructure, the asset return metrics calculation request datastructure structured to specify a set of assets and a set of simulated market scenarios, each simulated market scenario in the set of simulated market scenarios structured to comprise a set of simulated market factor values corresponding to a set of market factors; determine, via at least one processor, a number of sessions to utilize for calculating asset return metrics data; determine, via at least one processor, an assets range for a session based on the determined number of sessions to utilize, the assets range comprising a set of asset database table records for the set of assets to be processed by the session; create, via at least one processor, an assets batch database table, the assets batch database table structured to comprise a set of asset database table records of a specified batch size from the assets range for the session; create, via at least one processor, a factor simulations batch database table, the factor simulations batch database table structured to comprise a set of simulated market factor return values for the set of asset database table records in the assets batch database table; create, via at least one processor, a factor exposures batch database table, the factor exposures batch database table structured to comprise a set of factor exposure database table records matching the set of asset database table records in the assets batch database table; and calculate, via at least one processor, via a parallel SQL query, expected returns for the set of asset database table records in the assets batch database table, using the factor simulations batch database table and the factor exposures batch database table.

2. The apparatus of claim 1, further, comprising: the set of simulated market factor values for a simulated market scenario is configured as generated using a set of deep learning neural networks.

3. The apparatus of claim 1, further, comprising: the set of simulated market factor values for a simulated market scenario is configured as generated using a set of multi-variate mixture datastructures.

4. The apparatus of claim 1, further, comprising: the processor-executable instructions structured as: filter, via at least one processor, asset database table records associated with the set of assets, based on available factor exposure database table records, using a SQL statement.

5. The apparatus of claim 4, further, comprising: the processor-executable instructions structured as: filter, via at least one processor, simulated market scenario database table records associated with the set of simulated market scenarios, based on a subset of market factors from the set of market factors to which the filtered asset database table records have exposure, using a SQL statement.

6. The apparatus of claim 1, further, comprising: the number of sessions to utilize for calculating asset return metrics data is determined based on the number of available server processors and a specified degree of parallelism per session.

7. The apparatus of claim 1, further, comprising: the assets batch database table, the factor simulations batch database table, and the factor exposures batch database table are temporary database tables.

8. The apparatus of claim 4, further, comprising: the processor-executable instructions structured as: filter, via at least one processor, at least one of call schedule database table records and put schedule database table records based on the filtered asset database table records.

9. The apparatus of claim 8, further, comprising: the processor-executable instructions structured as: adjust, via at least one processor, via a parallel SQL query, the calculated expected returns for the set of asset database table records in the assets batch database table, based on at least one of the filtered call schedule database table records and the filtered put schedule database table records.

10. The apparatus of claim 1, further, comprising: the processor-executable instructions structured as: transpose, via at least one processor, the calculated expected returns for the set of asset database table records in the assets batch database table into a wide array format; and write, via at least one processor, via a parallel SQL query, the transposed expected returns to an asset simulation wide table.

11. The apparatus of claim 10, further, comprising: the asset simulation wide table formatted to facilitate efficient calculation of portfolio return metrics; and the asset simulation wide table structured to be written to in parallel by query server processes from a plurality of utilized sessions.

12. The apparatus of claim 1, further, comprising: the processor-executable instructions structured as: calculate, via at least one processor, via a parallel SQL query, an asset return metric based on the calculated expected returns for the set of asset database table records in the assets batch database table; transpose, via at least one processor, the calculated asset return metric for the set of asset database table records in the assets batch database table into a wide array format; and write, via at least one processor, via a parallel SQL query, the transposed asset return metric to an asset simulation wide table.

13. The apparatus of claim 1, further, comprising: the processor-executable instructions structured as: write, via at least one processor, via a parallel SQL query, the calculated expected returns to an asset measure table.

14. The apparatus of claim 1, further, comprising: the processor-executable instructions structured as: calculate, via at least one processor, via a parallel SQL query, an asset return metric based on the calculated expected returns for the set of asset database table records in the assets batch database table; and write, via at least one processor, via a parallel SQL query, the calculated asset return metric to an asset measure table.

15. The apparatus of claim 14, further, comprising: the asset measure table formatted to facilitate efficient calculation of security return metrics; and the asset measure table structured to be written to in parallel by query server processes from a plurality of utilized sessions.

16. The apparatus of claim 1, further, comprising: the set of simulated market factor values for a simulated market scenario is configured as generated using a set of deep learning neural networks and using a set of multi-variate mixture datastructures.

17. The apparatus of claim 1, further, comprising: each expected return configured as calculated for an asset during a simulated market scenario using: the respective asset's conditional Beta during the respective simulated market scenario, determined using a set of decision tree ensembles, trained to estimate conditional Beta of the respective asset, based on a first subset of the set of simulated market factor values, and the respective asset's conditional default probability during the respective simulated market scenario, determined using a set of decision tree ensembles, trained to estimate conditional default probability of the respective asset, based on a second subset of the set of simulated market factor values.

18. A database calculation engine processor-readable, non-transient medium, comprising processor-executable instructions structured as: obtain, via at least one processor, an asset return metrics calculation request datastructure, the asset return metrics calculation request datastructure structured to specify a set of assets and a set of simulated market scenarios, each simulated market scenario in the set of simulated market scenarios structured to comprise a set of simulated market factor values corresponding to a set of market factors; determine, via at least one processor, a number of sessions to utilize for calculating asset return metrics data; determine, via at least one processor, an assets range for a session based on the determined number of sessions to utilize, the assets range comprising a set of asset database table records for the set of assets to be processed by the session; create, via at least one processor, an assets batch database table, the assets batch database table structured to comprise a set of asset database table records of a specified batch size from the assets range for the session; create, via at least one processor, a factor simulations batch database table, the factor simulations batch database table structured to comprise a set of simulated market factor return values for the set of asset database table records in the assets batch database table; create, via at least one processor, a factor exposures batch database table, the factor exposures batch database table structured to comprise a set of factor exposure database table records matching the set of asset database table records in the assets batch database table; and calculate, via at least one processor, via a parallel SQL query, expected returns for the set of asset database table records in the assets batch database table, using the factor simulations batch database table and the factor exposures batch database table.

19. A database calculation engine processor-implemented system, comprising: means to process processor-executable instructions; means to issue processor-issuable instructions from a processor-executable component collection via the means to process processor-executable instructions, the processor-issuable instructions structured as: obtain, via at least one processor, an asset return metrics calculation request datastructure, the asset return metrics calculation request datastructure structured to specify a set of assets and a set of simulated market scenarios, each simulated market scenario in the set of simulated market scenarios structured to comprise a set of simulated market factor values corresponding to a set of market factors; determine, via at least one processor, a number of sessions to utilize for calculating asset return metrics data; determine, via at least one processor, an assets range for a session based on the determined number of sessions to utilize, the assets range comprising a set of asset database table records for the set of assets to be processed by the session; create, via at least one processor, an assets batch database table, the assets batch database table structured to comprise a set of asset database table records of a specified batch size from the assets range for the session; create, via at least one processor, a factor simulations batch database table, the factor simulations batch database table structured to comprise a set of simulated market factor return values for the set of asset database table records in the assets batch database table; create, via at least one processor, a factor exposures batch database table, the factor exposures batch database table structured to comprise a set of factor exposure database table records matching the set of asset database table records in the assets batch database table; and calculate, via at least one processor, via a parallel SQL query, expected returns for the set of asset database table records in the assets batch database table, using the factor simulations batch database table and the factor exposures batch database table.

20. A database calculation engine processor-implemented process, comprising executing processor-executable instructions to: obtain, via at least one processor, an asset return metrics calculation request datastructure, the asset return metrics calculation request datastructure structured to specify a set of assets and a set of simulated market scenarios, each simulated market scenario in the set of simulated market scenarios structured to comprise a set of simulated market factor values corresponding to a set of market factors; determine, via at least one processor, a number of sessions to utilize for calculating asset return metrics data; determine, via at least one processor, an assets range for a session based on the determined number of sessions to utilize, the assets range comprising a set of asset database table records for the set of assets to be processed by the session; create, via at least one processor, an assets batch database table, the assets batch database table structured to comprise a set of asset database table records of a specified batch size from the assets range for the session; create, via at least one processor, a factor simulations batch database table, the factor simulations batch database table structured to comprise a set of simulated market factor return values for the set of asset database table records in the assets batch database table; create, via at least one processor, a factor exposures batch database table, the factor exposures batch database table structured to comprise a set of factor exposure database table records matching the set of asset database table records in the assets batch database table; and calculate, via at least one processor, via a parallel SQL query, expected returns for the set of asset database table records in the assets batch database table, using the factor simulations batch database table and the factor exposures batch database table.

Description

[0001] This application for letters patent disclosure document describes inventive aspects that include various novel innovations (hereinafter "disclosure") and contains material that is subject to copyright, mask work, and/or other intellectual property protection. The respective owners of such intellectual property have no objection to the facsimile reproduction of the disclosure by anyone as it appears in published Patent Office file/records, but otherwise reserve all rights.

PRIORITY CLAIM

[0002] Applicant hereby claims benefit to priority under 35 USC .sctn. 119 as a non-provisional conversion of: U.S. provisional patent application Ser. No. 63/055,876, filed Jul. 23, 2020, entitled "Machine Learning Portfolio Simulating and Optimizing Apparatuses, Methods and Systems", (attorney docket no. Fideli 0663PV).

[0003] The entire contents of the aforementioned applications are herein expressly incorporated by reference.

Other Applications

[0004] Applications of interest include: U.S. patent application Ser. No. 14/494,443, filed Sep. 23, 2014, entitled "Life Cycle Based Portfolio Construction Platform Apparatuses, Methods and Systems", (attorney docket no. Fidelity-0148US); U.S. patent application Ser. No. 14/286,792, filed May 23, 2014, entitled "SEASONAL PORTFOLIO CONSTRUCTION PLATFORM APPARATUSES, METHODS AND SYSTEMS", (attorney docket no. Fidelity-0002US2); U.S. patent application Ser. No. 14/032,140, filed Sep. 19, 2013, entitled "SECTOR-BASED PORTFOLIO CONSTRUCTION PLATFORM APPARATUSES, METHODS AND SYSTEMS", (attorney docket no. FIDE-001/01US270718-2003), U.S. patent application Ser. No. 13/370,396, filed Feb. 10, 2012, entitled "MULTI-FACTOR RISK MODELING PLATFORM", (attorney docket no. FideliFR06US).

[0005] The entire contents of the aforementioned applications are herein expressly incorporated by reference.

FIELD

[0006] The present innovations generally address machine learning and database systems, and more particularly, include Machine Learning Portfolio Simulating and Optimizing Apparatuses, Methods and Systems.

[0007] However, in order to develop a reader's understanding of the innovations, disclosures have been compiled into a single description to illustrate and clarify how aspects of these innovations operate independently, interoperate as between individual innovations, and/or cooperate collectively. The application goes on to further describe the interrelations and synergies as between the various innovations; all of which is to further compliance with 35 U.S.C. .sctn. 112.

BACKGROUND

[0008] People own all types of assets, some of which are secured instruments to underlying assets. People have used exchanges to facilitate trading and selling of such assets. Computer information systems, such as NAICO-NET, Trade*Plus and E*Trade allowed owners to trade securities as sets electronically.

BRIEF DESCRIPTION OF THE DRAWINGS

[0009] Appendices and/or drawings illustrating various, non-limiting, example, innovative aspects of the Machine Learning Portfolio Simulating and Optimizing Apparatuses, Methods and Systems (hereinafter "MLPO") disclosure, include:

[0010] FIGS. 1A-B show a datagraph illustrating data flow(s) for the MLPO;

[0011] FIGS. 2A-B show a logic flow illustrating embodiments of a machine learning simulated scenario processing (MLSSP) component for the MLPO;

[0012] FIG. 3 shows an architecture for the MLPO;

[0013] FIG. 4 shows a logic flow illustrating embodiments of a machine learning simulated scenario processing (MLSSP) component for the MLPO;

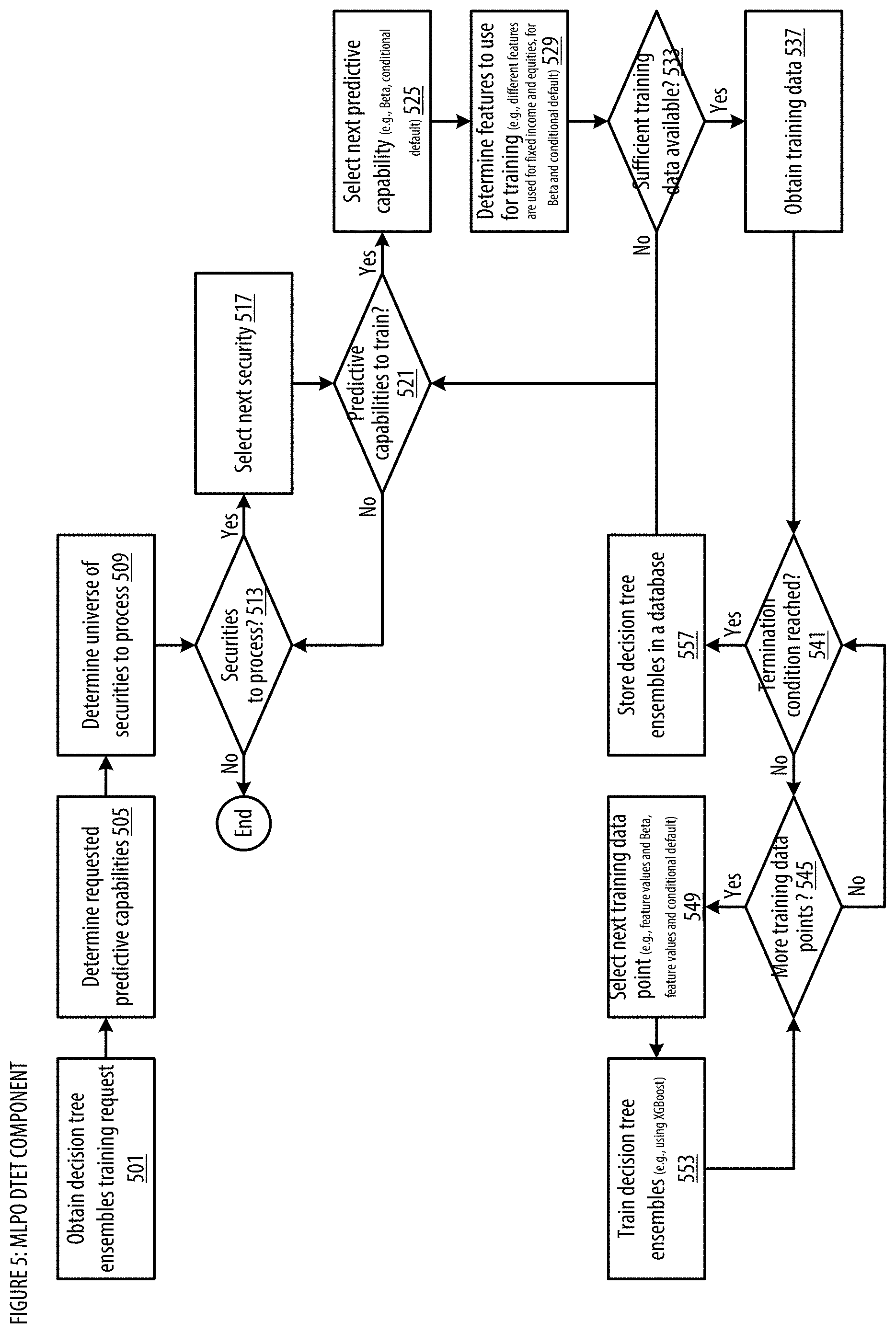

[0014] FIG. 5 show a logic flow illustrating embodiments of a decision tree ensembles training (DTET) component for the MLPO;

[0015] FIGS. 6A-D show implementation case(s) for the MLPO;

[0016] FIGS. 7A-C show a logic flow illustrating embodiments of an expected returns calculation (ERC) component for the MLPO;

[0017] FIG. 8 shows a datagraph illustrating data flow(s) for the MLPO;

[0018] FIG. 9 shows a logic flow illustrating embodiments of a portfolio constructing (PC) component for the MLPO;

[0019] FIG. 10 shows a screenshot illustrating user interface(s) of the MLPO;

[0020] FIG. 11 shows a screenshot illustrating user interface(s) of the MLPO;

[0021] FIG. 12 shows a screenshot illustrating user interface(s) of the MLPO;

[0022] FIG. 13 shows a datagraph illustrating data flow(s) for the MLPO;

[0023] FIGS. 14A-B show a logic flow illustrating embodiments of a predefined scenario constructing (PSC) component for the MLPO;

[0024] FIG. 15 shows a screenshot illustrating user interface(s) of the MLPO;

[0025] FIG. 16 shows a screenshot illustrating user interface(s) of the MLPO;

[0026] FIG. 17 shows a screenshot illustrating user interface(s) of the MLPO;

[0027] FIG. 18 shows a screenshot illustrating user interface(s) of the MLPO;

[0028] FIG. 19 shows a screenshot illustrating user interface(s) of the MLPO;

[0029] FIG. 20 shows a datagraph illustrating data flow(s) for the MLPO;

[0030] FIG. 21 shows a logic flow illustrating embodiments of a scenario based portfolio returns visualizing (SPRY) component for the MLPO;

[0031] FIG. 22 shows a screenshot illustrating user interface(s) of the MLPO;

[0032] FIG. 23 shows a screenshot illustrating user interface(s) of the MLPO;

[0033] FIG. 24 shows a screenshot illustrating user interface(s) of the MLPO;

[0034] FIG. 25 shows a screenshot illustrating user interface(s) of the MLPO;

[0035] FIG. 26 shows a datagraph illustrating data flow(s) for the MLPO;

[0036] FIG. 27 shows a logic flow illustrating embodiments of a business cycle based portfolio returns visualizing (BPRV) component for the MLPO;

[0037] FIG. 28 shows a screenshot illustrating user interface(s) of the MLPO;

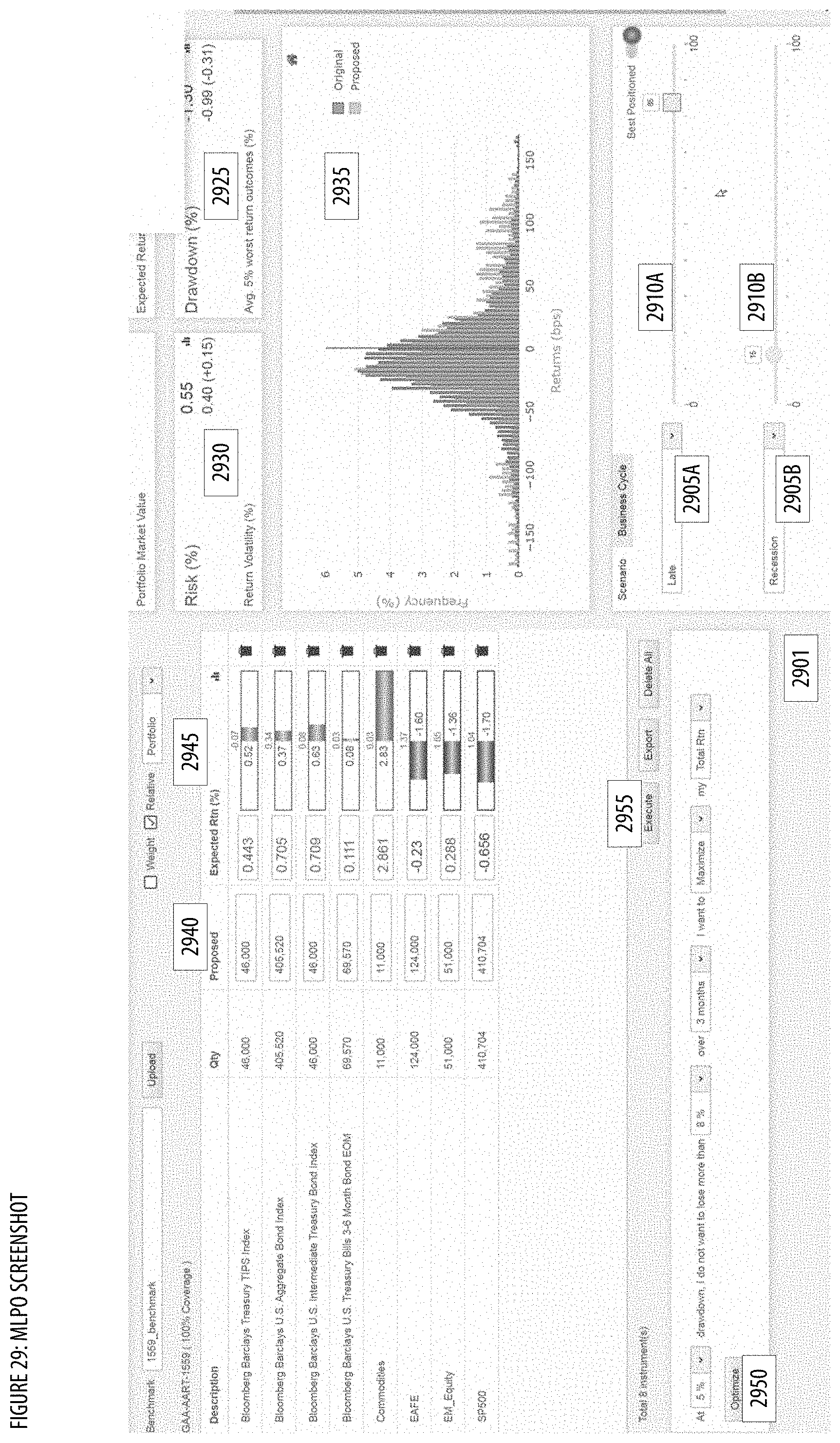

[0038] FIG. 29 shows a screenshot illustrating user interface(s) of the MLPO;

[0039] FIG. 30 shows a screenshot illustrating user interface(s) of the MLPO;

[0040] FIG. 31 shows an architecture for the MLPO;

[0041] FIG. 32 shows an architecture for the MLPO;

[0042] FIGS. 33A-B show an architecture for the MLPO;

[0043] FIG. 34 shows a datagraph illustrating data flow(s) for the MLPO;

[0044] FIG. 35 shows a logic flow illustrating embodiments of a portfolio returns visualizing (PRV) component for the MLPO;

[0045] FIG. 36 shows a logic flow illustrating embodiments of an asset return metrics calculating (ARMC) component for the MLPO;

[0046] FIG. 37 shows an architecture for the MLPO;

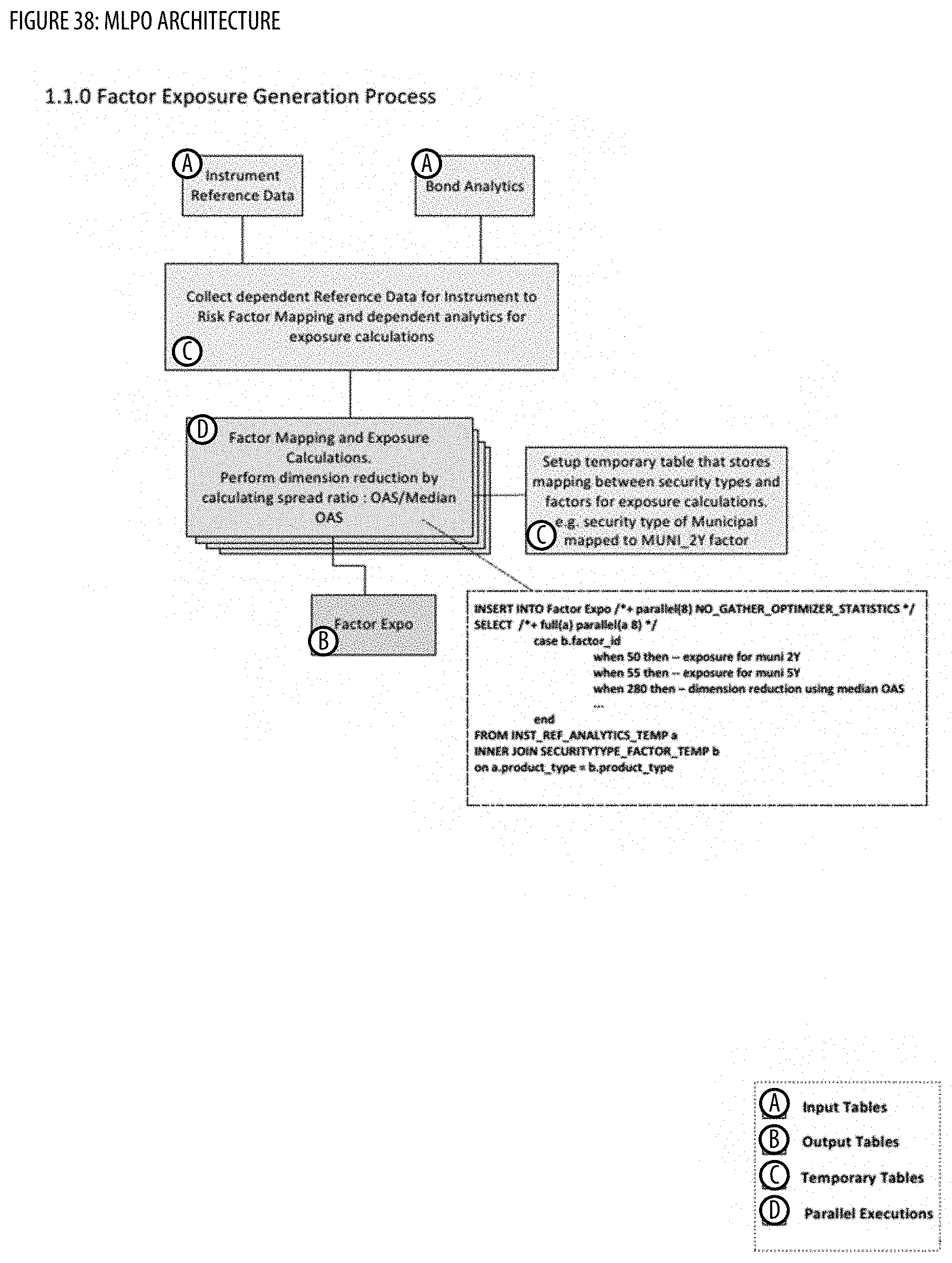

[0047] FIG. 38 shows an architecture for the MLPO;

[0048] FIG. 39 shows an architecture for the MLPO;

[0049] FIG. 40 shows an architecture for the MLPO;

[0050] FIG. 41 shows a screenshot illustrating user interface(s) of the MLPO;

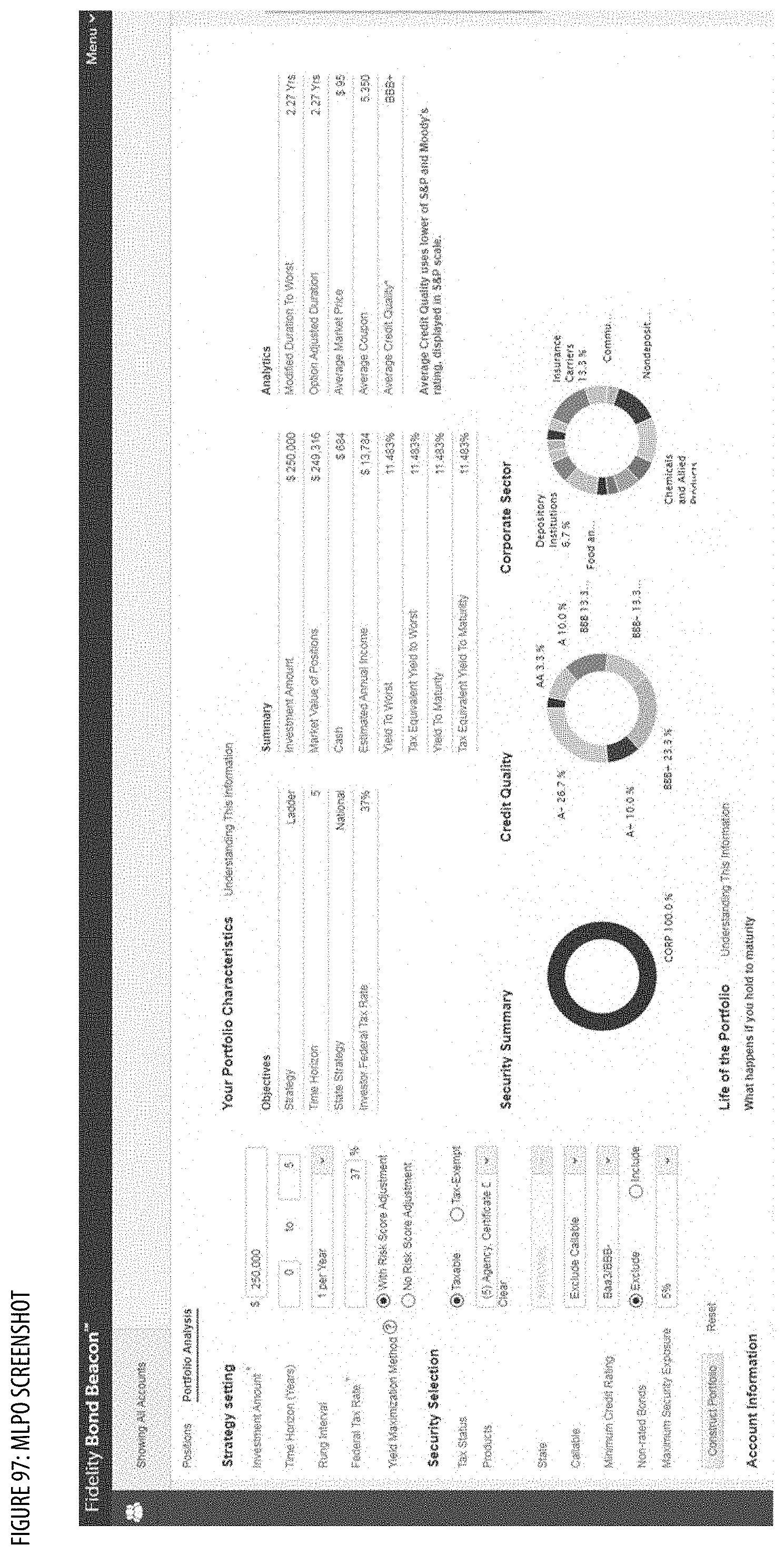

[0051] FIG. 42 shows a screenshot illustrating user interface(s) of the MLPO;

[0052] FIG. 43 shows a screenshot illustrating user interface(s) of the MLPO;

[0053] FIG. 44 shows a screenshot illustrating user interface(s) of the MLPO;

[0054] FIG. 45 shows a screenshot illustrating user interface(s) of the MLPO;

[0055] FIG. 46 shows a screenshot illustrating user interface(s) of the MLPO;

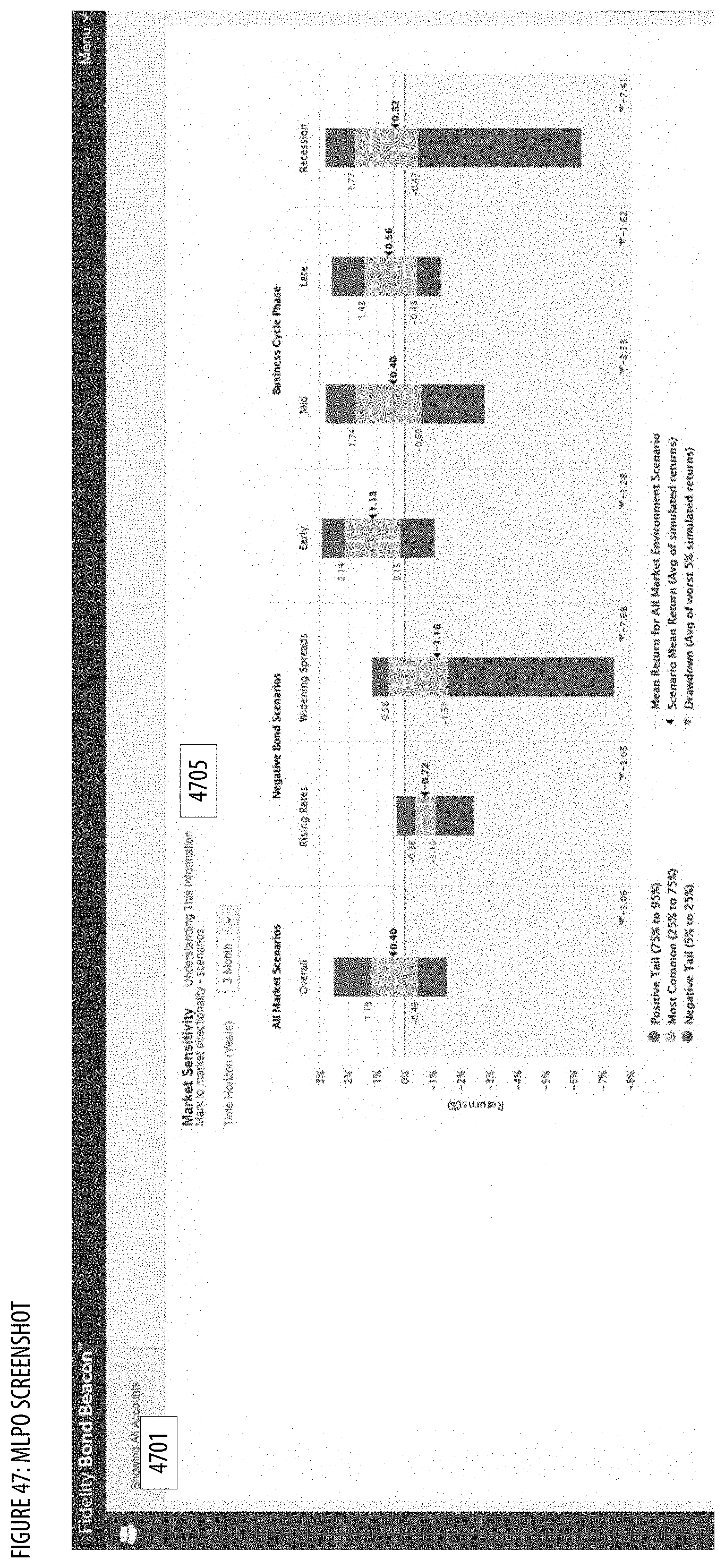

[0056] FIG. 47 shows a screenshot illustrating user interface(s) of the MLPO;

[0057] FIG. 48 shows an architecture for the MLPO;

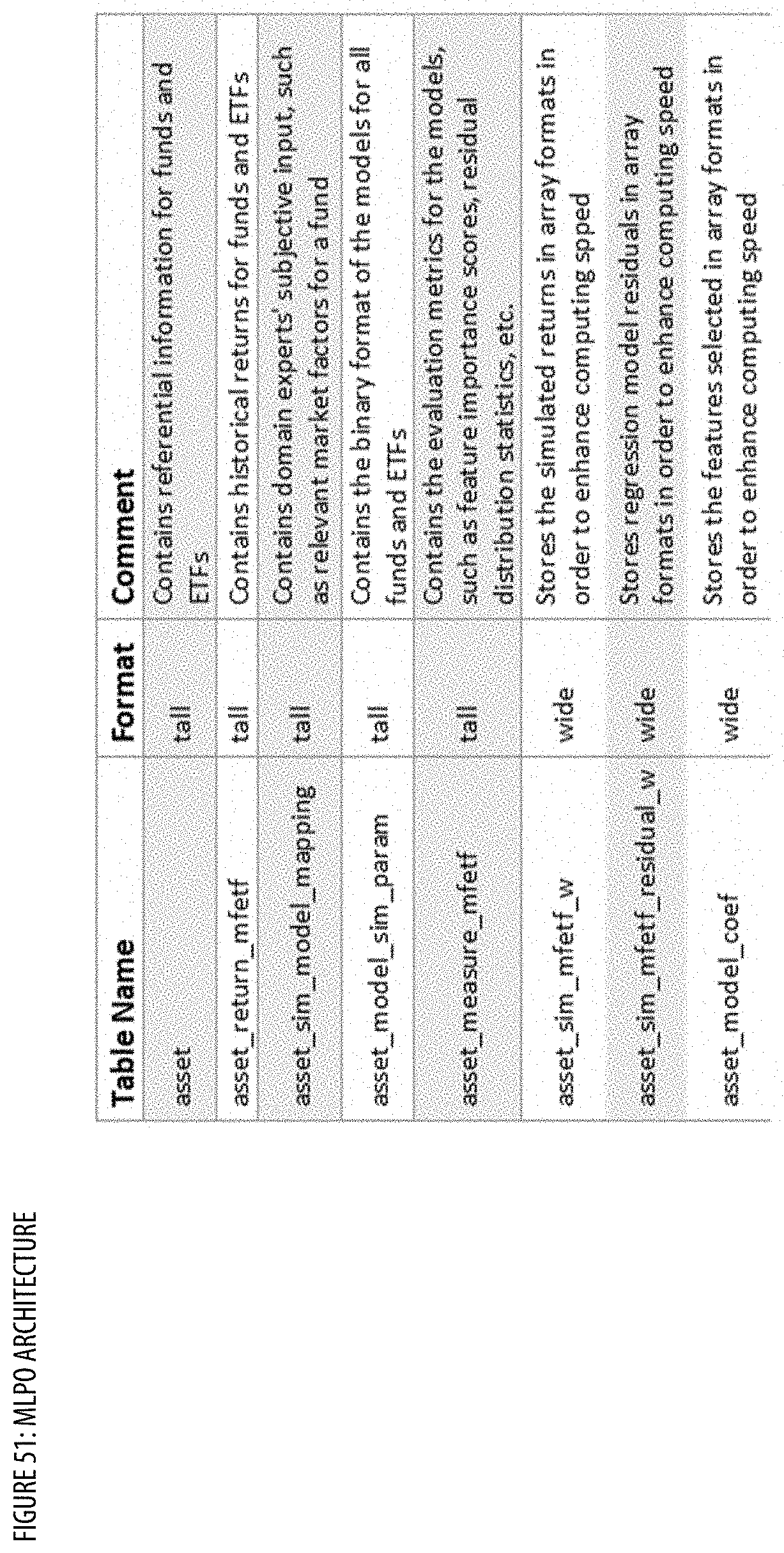

[0058] FIG. 49 shows an architecture for the MLPO (e.g., Mutual Fund/ETF Model Architecture);

[0059] FIG. 50 shows an architecture for the MLPO (e.g., Mutual Fund/ETF Pseudo Code--Parallel Computing);

[0060] FIG. 51 shows an architecture for the MLPO (e.g., Mutual Fund/ETF Database Tables);

[0061] FIG. 52 shows an architecture for the MLPO (e.g., Mutual Fund/ETF Pseudo Code--Proprietary Feature Selection);

[0062] FIG. 53 shows a screenshot illustrating user interface(s) of the MLPO (e.g., Market Risk Factor Exposure);

[0063] FIG. 54 shows a screenshot illustrating user interface(s) of the MLPO (e.g., Simulated Return Distribution Conditional on Market Scenario);

[0064] FIG. 55 shows a screenshot illustrating user interface(s) of the MLPO (e.g., Simulated Return Distribution Conditional on Business Cycle);

[0065] FIG. 56 shows an architecture for the MLPO (e.g., EQUITY RISK MODELING WORKFLOW);

[0066] FIG. 57 shows an architecture for the MLPO (e.g., PROPRIETARY FEATURE SELECTION METHOD);

[0067] FIG. 58 shows a screenshot illustrating user interface(s) of the MLPO (e.g., PMRI RISK ANALYSIS SCREENSHOT);

[0068] FIG. 59 shows a screenshot illustrating user interface(s) of the MLPO (e.g., MRI RISK ANALYSIS RETURN DRIVER SCREENSHOT);

[0069] FIG. 60 shows a screenshot illustrating user interface(s) of the MLPO (e.g., PMRI RISK ANALYSIS BUSINESS CYCLE SCREENSHOT);

[0070] FIG. 61 shows a screenshot illustrating user interface(s) of the MLPO (e.g., PMRI RISK ANALYSIS RISING VIX SCENARIO SCREENSHOT);

[0071] FIG. 62 shows an architecture for the MLPO (e.g., PARALLEL COMPUTING PSEUDOCODE);

[0072] FIG. 63 shows an architecture for the MLPO (e.g., EQUITY RISK MODELING FEATURE ENGINEERING WORKFLOW);

[0073] FIG. 64 shows an architecture for the MLPO (e.g., EQUITY IDIOSYNCRATIC RISK MODELING WORKFLOW);

[0074] FIG. 65 shows a screenshot illustrating user interface(s) of the MLPO (e.g., A VIX VS HISTORICAL UNPRECEDENTEDNESS);

[0075] FIG. 66 shows a screenshot illustrating user interface(s) of the MLPO (e.g., HISTORICAL VS VAE);

[0076] FIG. 67 shows a screenshot illustrating user interface(s) of the MLPO (e.g., HISTORICAL VS PANIC SIM);

[0077] FIG. 68 shows a screenshot illustrating user interface(s) of the MLPO (e.g., 3M VIX THRESHOLDS VS UNPRECEDENTEDNESS (MSE) 3D);

[0078] FIG. 69 shows a screenshot illustrating user interface(s) of the MLPO (e.g., 6M VIX THRESHOLDS VS UNPRECEDENTEDNESS (MSE) 3D);

[0079] FIG. 70 shows a screenshot illustrating user interface(s) of the MLPO (e.g., 1Y VIX THRESHOLDS VS UNPRECEDENTEDNESS (MSE) 3D);

[0080] FIG. 71 shows a screenshot illustrating user interface(s) of the MLPO (e.g., CVaR FRONTIER COMPARISON WITH DIVERSIFITION OF 0.6(LEFT) AND DIVERSIFICATION OF 0.3(RIGHT));

[0081] FIG. 72 shows a screenshot illustrating user interface(s) of the MLPO (e.g., TAIL RISK OPTIMIZATION RUNNING TIME COMPARISON OF INTEGER PROGRAMMING AND NON-INTEGER PROGRAMMING);

[0082] FIG. 73 shows a screenshot illustrating user interface(s) of the MLPO (e.g., EFFICIENT FRONTIER COMPARISON WITH RISK TOLERANCE OF 7 (LEFT) AND RISK TOLERANCE OF 3(RIGHT));

[0083] FIG. 74 shows a screenshot illustrating user interface(s) of the MLPO (e.g., EFFICIENT FRONTIER COMPARISON WITH DIVERSIFICATION OF 0.7(LEFT) AND RISK DIVERSIFICATION OF 0.3(RIGHT);

[0084] FIG. 75 shows a screenshot illustrating user interface(s) of the MLPO (e.g., EFFICIENT FRONTIER COMPARISON WITH VIX RANGE OF (-3500,5500)(LEFT) AND VIX RANGE OF (-1500,3000)(RIGHT));

[0085] FIG. 76 shows an architecture for the MLPO (e.g., FACTOR EXPOSURE GENERATION PSEUDO CODE);

[0086] FIG. 77 shows an architecture for the MLPO (e.g., ASSET SIMULATION GENERATION PSEUDO CODE);

[0087] FIG. 78 shows an architecture for the MLPO (e.g., FACTOR EXPOSURE GENERATION CONCEPT DIAGRAM);

[0088] FIG. 79 shows an architecture for the MLPO (e.g., ASSET SIMULATION GENERATION CONCEPT DIAGRAM);

[0089] FIG. 80 shows an architecture for the MLPO (e.g., CONVEXITY ADJUSTMENT PSEUDO CODE (STEP 1));

[0090] FIG. 81 shows an architecture for the MLPO (e.g., CONVEXITY ADJUSTMENT PSEUDO CODE (STEP 2));

[0091] FIG. 82 shows an architecture for the MLPO (e.g., OPTIONALITY ADJUSTMENT PSEUDO CODE);

[0092] FIG. 83 shows an architecture for the MLPO (e.g., REAL-TIME ASSET SIMULATION PSEUDO CODE);

[0093] FIG. 84 shows an architecture for the MLPO (e.g., REAL-TIME ASSET SIMULATION CONCEPT DIAGRAM (ORACLE RDS ON CLOUD));

[0094] FIG. 85 shows an architecture for the MLPO (e.g., MULTIPLE USER-DEFINED SCENARIOS PSEUDO CODE);

[0095] FIG. 86 shows an architecture for the MLPO (e.g., MULTIPLE USER-DEFINED SCENARIOS CONCEPT DIAGRAM);

[0096] FIG. 87 shows an architecture for the MLPO (e.g., ASSET SIMULATION ER DIAGRAM);

[0097] FIG. 88 shows an architecture for the MLPO (e.g., BOND LADDER CONSTRUCTION FLOW);

[0098] FIG. 89 shows an architecture for the MLPO (e.g., BOND LADDER CONSTRUCTION API INPUT SAMPLE);

[0099] FIG. 90 shows an architecture for the MLPO (e.g., BOND LADDER CONSTRUCTION API OUTPUT SAMPLE);

[0100] FIG. 91 shows an architecture for the MLPO (e.g., RISK ANALYSIS API INPUT SAMPLE);

[0101] FIG. 92 shows an architecture for the MLPO (e.g., RISK ANALYSIS API OUTPUT SAMPLE);

[0102] FIG. 93 shows a screenshot illustrating user interface(s) of the MLPO (e.g., BOND LADDER CONSTRUCTION USER INPUT/SELECTION SCREEN);

[0103] FIG. 94 shows a screenshot illustrating user interface(s) of the MLPO (e.g., BOND LADDER CONSTRUCTION--SAMPLE CORPORATE LADDER);

[0104] FIG. 95 shows a screenshot illustrating user interface(s) of the MLPO (e.g., BOND LADDER CONSTRUCTION--SAMPLE MUNI LADDER);

[0105] FIG. 96 shows a screenshot illustrating user interface(s) of the MLPO (e.g., BOND LADDER CONSTRUCTION--MAXIMIZE YIELD METHOD/OPTION);

[0106] FIG. 97 shows a screenshot illustrating user interface(s) of the MLPO (e.g., BOND LADDER CONSTRUCTION--RISK SCORE ADJUSTED METHOD/OPTION);

[0107] FIG. 98 shows a screenshot illustrating user interface(s) of the MLPO (e.g., MULTIPLE USER-DEFINED SCENARIOS--MARKET SENSITIVITY ANALYSIS);

[0108] FIG. 99 shows a block diagram illustrating embodiments of a MLPO controller.

[0109] Generally, the leading number of each citation number within the drawings indicates the figure in which that citation number is introduced and/or detailed. As such, a detailed discussion of citation number 101 would be found and/or introduced in FIG. 1. Citation number 201 is introduced in FIG. 2, etc. Any citations and/or reference numbers are not necessarily sequences but rather just example orders that may be rearranged and other orders are contemplated. Citation number suffixes may indicate that an earlier introduced item has been re-referenced in the context of a later figure and may indicate the same item, evolved/modified version of the earlier introduced item, etc., e.g., server 199 of FIG. 1 may be a similar server 299 of FIG. 2 in the same and/or new context.

DETAILED DESCRIPTION

[0110] The Machine Learning Portfolio Simulating and Optimizing Apparatuses, Methods and Systems (hereinafter "MLPO") transforms machine learning simulation request, decision tree ensembles training request, expected returns calculation request, portfolio construction request, predefined scenario construction request, portfolio returns visualization request inputs, via MLPO components (e.g., MLSSP, DTET, ERC, PC, PSC, SPRV, BPRV, PRV, ARMC, etc. components), into machine learning simulation response, decision tree ensembles training response, expected returns calculation response, portfolio construction response, predefined scenario construction response, portfolio returns visualization response outputs. The MLPO components, in various embodiments, implement advantageous features as set forth below.

Introduction

[0111] The MLPO provides unconventional features (e.g., executing tradeable transactions to create an optimized portfolio based on expected returns simulated using machine learning techniques, a SQL database calculation engine) that were never before available in machine learning and database systems.

[0112] Tail-events have rare historical occurrence. They are difficult to model and forecast. However, they can be an essential part of resilient decision processes. The MLPO demonstrates unique abilities to model variations in volatilities and dependency structures across factors and over different time periods; provides rich estimates of tail-event; enables conditional outcomes of tail-events; and uses advanced linear and non-linear optimization processes for superior decision support. The optimization results provide model recommended solutions, such as for portfolio construction.

[0113] The MLPO presents the latest innovations in two core capabilities of investment management: 1) simulation driven investment insights and decision support and 2) machine driven portfolio allocation guidance. It combines the latest machine learning methods with leading-edge cloud computing techniques. It enables differentiations across many business units: analytics and insights to power a commercial electronic bond trading platform, power tools for evaluating portfolio construction bias, smart Bond Ladder products, and/or the like.

[0114] In various embodiments, the MLPO may include one or more of the following features:

[0115] 1 Maximizes the usage of high frequency historical data [0116] a. Machine learning processes to impute missing data (e.g., in order to preserve higher frequency time-series data with gaps, and maximize the utility of all available historical data) [0117] b. Flexible periodicity with overlapping techniques

[0118] 2. Combines a mixer of copulas, flexible marginal distributions, rejection sampling and parallel computing for a single simulation engine which [0119] a. Models changes in correlations and volatilities for "fat tail" events (e.g., using massive parallel computing to concurrently perform simulation and/or conditional simulation and/or stress scenario generations over cloud computing infrastructure) [0120] b. Generates insights on the conditional impact of diverse factors on tail-events and volatilities

[0121] 3. Allows calibration to forward-looking signals

[0122] 4. Allows domain experts to incorporate their subjective views

[0123] 5. Simulates longer horizon, multi-period outcomes with path dependency (e.g., using massive parallel computing frameworks in path-dependent, multi-period simulation to capture joint seasonality and mean-reversion tendencies across factors)

[0124] 6. Preserves the cadence of historical cycles in forward-looking simulation paths

[0125] 7. Allows forward-looking factor views to drive optimization results

[0126] 8. Applies "simulation-data-driven" approach for tailed-constrained portfolio optimization (e.g., to recommend solutions allowing tail-risk, tradability controls, etc.). In one embodiment, applies linear relaxation to CVaR constraints and mixed integer linear programming for optimization problem solving. In another embodiment, applies stochastic optimizer with VaR or CVaR and integer constraints to solve a non-linear optimization problem.

[0127] In some embodiments, the MLPO may implement a database calculation engine for calculating simulation data. The database calculation engine may be a SQL-based solution that effectively utilizes different data reduction and parallel execution techniques to reduce the overall response time. Instead of using a dedicated high-performance platform (e.g., IBM Netezza Data Appliance) the database calculation engine may be used for simulation calculation providing a faster, streamlined, cost effective and scalable solution (e.g., using Oracle RDS on Cloud) that provides calculation results in substantially less amount of time. Further, the database calculation engine eliminates having to maintain a complex infrastructure and applications associated with using a dedicated high-performance platform, and having to pay for additional licensing and maintenance costs.

[0128] The database calculation engine solution is faster as data does not have to be transferred outside of the database with an innovative data reduction strategy that applies to simulation generation, less complex as the solution may run entirely on a database, scalable as the solution effectively utilizes vertical scalability offered by RDS on Cloud and more maintainable.

[0129] In some implementations, the database calculation engine may provide the following features: [0130] A novel way of calculating simulation data using a SQL only solution. [0131] Application of unique data reduction techniques applicable specifically to the way data is aggregated for simulation data. [0132] Use of vertical scalability and concurrency offered by Oracle RDS on Cloud for faster execution. [0133] Processing that happens at the database level, eliminating having to transfer data outside to external systems and maximizing processing of data using cloud computing. [0134] Faster and more cost effective than using high-performance platforms.

[0135] In some implementations, the database calculation engine may utilize various innovative data reduction, scaling and parallel computing techniques (e.g., techniques to use global temporary tables and sessions, data reduction techniques to drastically reduce the amount of data used for processing thus lowering processing time, and several other data parallelization techniques used for generating simulation data): [0136] Use of Multiple Batches to achieve higher degree of parallelism (DOP) [0137] Use of Global Temporary Tables (GTT) to be able to run batch in multiple sessions and limit temporary storage requirements [0138] Use of Data Reduction techniques to limit full table scans for joins between Factor Exposure and Factor Simulation table [0139] Use of Parallel Query to parallelize generation of Asset Simulation and Contribution to Value at Risk data [0140] Use of Parallel DML to parallelize inserting data related to Asset Simulation and Contribution to Value at Risk [0141] Use of DDL for faster execution of delete statements to speed up cleanup of global temporary tables

MLPO

[0142] FIGS. 1A-B show a datagraph illustrating data flow(s) for the MLPO. In FIGS. 1A-B, an administrative client 102 (e.g., of an administrative user) may send a machine learning simulation request 121 to a MLPO server 106 to facilitate generating a set of simulated scenarios (e.g., a scenario may be a set of simulated market factor changes). For example, the administrative client may be a desktop, a laptop, a tablet, a smartphone, a smartwatch, and/or the like that is executing a client application. In one implementation, the machine learning simulation request may include data such as a request identifier, configuration settings, and/or the like. In one embodiment, the administrative client may provide the following example machine learning simulation request, substantially in the form of a (Secure) Hypertext Transfer Protocol ("HTTP(S)") POST message including eXtensible Markup Language ("XML") formatted data, as provided below:

TABLE-US-00001 POST /authrequest.php HTTP/1.1 Host: www.server.com Content-Type: Application/XML Content-Length: 667 <?XML version = "1.0" encoding = "UTF-8"?> <auth_request> <timestamp>2020-12-31 23:59:59</timestamp> <user_accounts_details> <user_account_credentials> <user_name>JohnDaDoeDoeDoooe@gmail.com</user_name> <password>abc123</password> //OPTIONAL <cookie>cookieID</cookie> //OPTIONAL <digital_cert_link>www.mydigitalcertificate.com/ JohnDoeDaDoeDoe@gmail.com/mycertifcate.dc</digital_cert_link> //OPTIONAL <digital_certificate>_DATA_</digital_certificate> </user_account_credentials> </user_accounts_details> <client_details> //iOS Client with App and Webkit //it should be noted that although several client details //sections are provided to show example variants of client //sources, further messages will include only on to save //space <client_IP>10.0.0.123</client_IP> <user_agent_string>Mozilla/5.0 (iPhone; CPU iPhone OS 7_1_1 like Mac OS X) AppleWebKit/537.51.2 (KHTML, like Gecko) Version/7.0 Mobile/11D201 Safari/9537.53</user_agent_string> <client_product_type>iPhone6,1</client_product_type> <client_serial_number>DNXXX1X1XXXX</client_serial_number> <client_UDID>3XXXXXXXXXXXXXXXXXXXXXXXXD</client_UDID> <client_OS>iOS</client_OS> <client_OS_version>7.1.1</client_OS_version> <client_app_type>app with webkit</client_app_type> <app_installed_flag>true</app_installed_flag> <app_name>MLPO.app</app_name> <app_version>1.0 </app_version> <app_webkit_name>Mobile Safari</client_webkit_name> <client_version>537.51.2</client_version> </client_details> <client_details> //iOS Client with Webbrowser <client_IP>10.0.0.123</client_IP> <user_agent_string>Mozilla/5.0 (iPhone; CPU iPhone OS 7_1_1 like Mac OS X) AppleWebKit/537.51.2 (KHTML, like Gecko) Version/7.0 Mobile/11D201 Safari/9537.53</user_agent_string> <client_product_type>iPhone6,1</client_product_type> <client_serial_number>DNXXX1X1XXXX</client_serial_number> <client_UDID>3XXXXXXXXXXXXXXXXXXXXXXXXD</client_UDID> <client_OS>iOS</client_OS> <client_OS_version>7.1.1</client_OS_version> <client_app_type>web browser</client_app_type> <client_name>Mobile Safari</client_name> <client_version>9537.53</client_version> </client_details> <client_details> //Android Client with Webbrowser <client_IP>10.0.0.123</client_IP> <user_agent_string>Mozilla/5.0 (Linux; U; Android 4.0.4; en-us; Nexus S Build/IMM76D) AppleWebKit/534.30 (KHTML, like Gecko) Version/4.0 Mobile Safari/534.30</user_agent_string> <client_product_type>Nexus S</client_product_type> <client_serial_number>YXXXXXXXXZ</client_serial_number> <client_UDID>FXXXXXXXXX-XXXX-XXXX-XXXX-XXXXXXXXXXXXX</client_UDI- D> <client_OS>Android</client_OS> <client_OS_version>4.0.4</client_OS_version> <client_app_type>web browser</client_app_type> <client_name>Mobile Safari</client_name> <client_version>534.30</client_version> </client_details> <client_details> //Mac Desktop with Webbrowser <client_IP>10.0.0.123</client_IP> <user_agent_string>Mozilla/5.0 (Macintosh; Intel Mac OS X 10_9_3) AppleWebKit/537.75.14 (KHTML, like Gecko) Version/7.0.3 Safari/537.75.14</user_agent_string> <client_product_type>MacPro5,1</client_product_type> <client_serial_number>YXXXXXXXXZ</client_serial_number> <client_UDID>FXXXXXXXXX-XXXX-XXXX-XXXX-XXXXXXXXXXXXX</client_UDI- D> <client_OS>Mac OS X</client_OS> <client_OS_version>10.9.3</client_OS_version> <client_app_type>web browser</client_app_type> <client_name>Mobile Safari</client_name> <client_version>537.75.14</client_version> </client_details> <machine_learning_simulation_request> <request_identifier>ID_request_1</request_identifier> <configuration_settings> <historical_data>last 30 years</historical_data> <rolling_window_period_length>6 months</rolling_window_period_length> <time_period_bucket_type>FIXED</time_period_bucket_type> <time_period_bucket_length>6 months</time_period_bucket_length> <market_factors> ID_interest_rate_5Y, ID_oil_price, ID_credit_spread, ID_SP500 </market_factors> <distribution_type>Gaussian</distribution_type> <machine_learning_structure_type> deep learning neural network </machine_learning_structure_type> <hyper_parameters_to_test> <hyper_parameters_option> <option_identifier>ID_option_1</option_identifier> <encoder>3 layers, 100 perceptrons each</encoder> <latent_space>50 variables</latent_space> <decoder>3 layers, 100 perceptrons each</decoder> </hyper_parameters_option> <hyper_parameters_option> <option_identifier>ID_option_2</option_identifier> <encoder>4 layers, 80 perceptrons each</encoder> <latent_space>60 variables</latent_space> <decoder>4 layers, 80 perceptrons each</decoder> </hyper_parameters_option> ... </hyper_parameters_to_test> <number_of_simulated_market_scenarios> 1000 scenarios per time period bucket </number_of_simulated_market_scenarios> </configuration_settings> </machine_learning_simulation_request> </auth_request>

[0143] A machine learning simulated scenario processing (MLSSP) component 123 may utilize data provided in the machine learning simulation request to train a machine learning structure and/or to generate a set of simulated scenarios. See FIGS. 2A-B and FIG. 4 for additional details regarding the MLSSP component.

[0144] The MLPO server 106 may send a scenario results store request 125 to a repository 110 to facilitate storing the generated set of simulated scenarios (e.g., a simulation) in a database. In one implementation, the scenario results store request may include data such as a request identifier, a simulation identifier, simulated scenarios, and/or the like. In one embodiment, the MLPO server may provide the following example scenario results store request, substantially in the form of a HTTP(S) POST message including XML-formatted data, as provided below:

TABLE-US-00002 POST /scenario_results_store_request.php HTTP/1.1 Host: www.server.com Content-Type: Application/XML Content-Length: 667 <?XML version = "1.0" encoding = "UTF-8"?> <scenario_results_store_request> <request_identifier>ID_request_2</request_identifier> <simulation_identifier>ID_sim_1</simulation_identifier> <simulated_scenarios> <scenario> <scenario_identifier>ID_scenario_1</scenario_identifier> <market_factor> <market_factor_identifier>ID_interest_rate_5Y</market_factor_ide- ntifier> <market_factor_change>25 basis points</market_factor_change> </market_factor> <market_factor> <market_factor_identifier>ID_oil_price</market_factor_identifier- > <market_factor_change>$10</market_factor_change> </market_factor> ... </scenario> <scenario> <scenario_identifier>ID_scenario_2</scenario_identifier> <market_factor> <market_factor_identifier>ID_interest_rate_5Y</market_factor_ide- ntifier> <market_factor_change>50 basis points</market_factor_change> </market_factor> <market_factor> <market_factor_identifier>ID_oil_price</market_factor_identifier- > <market_factor_change>$15</market_factor_change> </market_factor> ... </scenario> ... </simulated_scenarios> </scenario_results_store_request>

[0145] The repository 110 may send a scenario results store response 127 to the MLPO server 106 to confirm that the generated set of simulated scenarios was stored successfully. In one implementation, the scenario results store response may include data such as a response identifier, a status, and/or the like. In one embodiment, the repository may provide the following example scenario results store response, substantially in the form of a HTTP(S) POST message including XML-formatted data, as provided below:

TABLE-US-00003 POST /scenario_results_store_response.php HTTP/1.1 Host: www.server.com Content-Type: Application/XML Content-Length: 667 <?XML version = "1.0" encoding = "UTF-8"?> <scenario_results_store_response> <response_identifier>ID_response_2</response_identifier> <status>OK</status> </scenario_results_store_response>

[0146] The MLPO server 106 may send a machine learning simulation response 129 to the administrative client 102 to inform the administrative user that a set of simulated scenarios was generated successfully. In one implementation, the machine learning simulation response may include data such as a response identifier, a status, and/or the like. In one embodiment, the MLPO server may provide the following example machine learning simulation response, substantially in the form of a HTTP(S) POST message including XML-formatted data, as provided below:

TABLE-US-00004 POST /machine_learning_simulation_response.php HTTP/1.1 Host: www.server.com Content-Type: Application/XML Content-Length: 667 <?XML version = "1.0" encoding = "UTF-8"?> <machine_learning_simulation_response> <response_identifier>ID_response_1</response_identifier> <status>OK</status> </machine_learning_simulation_response>

[0147] The administrative client 102 may send a decision tree ensembles training request 131 to the MLPO server 106 to facilitate training decision tree ensembles for a universe of securities. For example, different decision tree ensembles may be trained for each security for different predictive capabilities (e.g., one decision tree ensemble may be trained to estimate conditional Beta for a security, and another decision tree ensemble may be trained to estimate conditional default for the security). In one implementation, the decision tree ensembles training request may include data such as a request identifier, a universe of securities, predictive capabilities configuration, training features configuration, and/or the like. In one embodiment, the administrative client may provide the following example decision tree ensembles training request, substantially in the form of a HTTP(S) POST message including XML-formatted data, as provided below:

TABLE-US-00005 POST /decision_tree_ensembles_training_request.php HTTP/1.1 Host: www.server.com Content-Type: Application/XML Content-Length: 667 <?XML version = "1.0" encoding = "UTF-8"?> <decision_tree_ensembles_training_request> <request_identifier>ID_request_3</request_identifier> <universe_of_securities>Securities in S&P 500</universe_of_securities> <predictive_capabilities_configuration> <predictive_capability> <predictive_capability_type>Conditional Beta</predictive_capability_type> <training_features> <feature>ratio of cash to market value of total assets</feature> <feature>ratio of net income to total assets</feature> <feature>size measure</feature> <feature>sector dummy variable</feature> ... </training_features> </predictive_capability> <predictive_capability> <predictive_capability_type>Conditional Default</predictive_capability_type> <training_features> <feature>ratio of cash to market value of total assets</feature> <feature>unemployment rate</feature> <feature>value of VIX index</feature> ... </training_features> </predictive_capability> </predictive_capabilities_configuration> </decision_tree_ensembles_training_request>

[0148] A decision tree ensembles training (DTET) component 133 may utilize data provided in the decision tree ensembles training request to train decision tree ensembles for the universe of securities. See FIG. 5 for additional details regarding the DTET component.

[0149] The MLPO server 106 may send a decision tree ensembles store request 135 to the repository 110 to facilitate storing the trained decision tree ensembles. In one implementation, the decision tree ensembles store request may include data such as a request identifier, decision tree ensembles, and/or the like. In one embodiment, the MLPO server may provide the following example decision tree ensembles store request, substantially in the form of a HTTP(S) POST message including XML-formatted data, as provided below:

TABLE-US-00006 POST /decision_tree_ensembles_store_request.php HTTP/1.1 Host: www.server.com Content-Type: Application/XML Content-Length: 667 <?XML version = "1.0" encoding = "UTF-8"?> <decision_tree_ensembles_store_request> <request_identifier>ID_request_4</request_identifier> <decision_tree_ensembles> <decision_tree_ensemble> <decision_tree_ensemble_id>ID_DTE_1</decision_tree_ensemble_id&g- t; <associated_security>MSFT</associated_security> <predictive_capability_type>Conditional Beta</predictive_capability_type> <decision_tree_ensemble_data> decision tree ensemble datastructure </decision_tree_ensemble_data> </decision_tree_ensemble> <decision_tree_ensemble> <decision_tree_ensemble_id>ID_DTE_2</decision_tree_ensemble_id&g- t; <associated_security>MSFT</associated_security> <predictive_capability_type>Conditional Default</predictive_capability_type> <decision_tree_ensemble_data> decision tree ensemble datastructure </decision_tree_ensemble_data> </decision_tree_ensemble> <decision_tree_ensemble_id>ID_DTE_3</decision_tree_ensemble_id&g- t; <associated_security>AAPL</associated_security> <predictive_capability_type>Conditional Beta</predictive_capability_type> <decision_tree_ensemble_data> decision tree ensemble datastructure </decision_tree_ensemble_data> </decision_tree_ensemble> <decision_tree_ensemble> <decision_tree_ensemble_id>ID_DTE_4</decision_tree_ensemble_id&g- t; <associated_security>AAPL</associated_security> <predictive_capability_type>Conditional Default</predictive_capability_type> <decision_tree_ensemble_data> decision tree ensemble datastructure </decision_tree_ensemble_data> </decision_tree_ensemble> ... </decision_tree_ensembles> </decision_tree_ensembles_store_request>

[0150] The repository 110 may send a decision tree ensembles store response 137 to the MLPO server 106 to confirm that the trained decision tree ensembles were stored successfully. In one implementation, the decision tree ensembles store response may include data such as a response identifier, a status, and/or the like. In one embodiment, the repository may provide the following example decision tree ensembles store response, substantially in the form of a HTTP(S) POST message including XML-formatted data, as provided below:

TABLE-US-00007 POST /decision_tree_ensembles_store_response.php HTTP/1.1 Host: www.server.com Content-Type: Application/XML Content-Length: 667 <?XML version = "1.0" encoding = "UTF-8"?> <decision_tree_ensembles_store_response> <response_identifier>ID_response_4</response_identifier> <status>OK</status> </decision_tree_ensembles_store_response>

[0151] The MLPO server 106 may send a decision tree ensembles training response 139 to the administrative client 102 to inform the administrative user that decision tree ensembles were trained successfully. In one implementation, the decision tree ensembles training response may include data such as a response identifier, a status, and/or the like. In one embodiment, the MLPO server may provide the following example decision tree ensembles training response, substantially in the form of a HTTP(S) POST message including XML-formatted data, as provided below:

TABLE-US-00008 POST /decision_tree_ensembles_training_response.php HTTP/1.1 Host: www.server.com Content-Type: Application/XML Content-Length: 667 <?XML version = "1.0" encoding = "UTF-8"?> <decision_tree_ensembles_training_response> <response_identifier>ID_response_3</response_identifier> <status>OK</status> </decision_tree_ensembles_training_response>

[0152] The administrative client 102 may send an expected returns calculation request 141 to the MLPO server 106 to facilitate calculating expected returns for the universe of securities under the simulated scenarios. In one implementation, the expected returns calculation request may include data such as a request identifier, a universe of securities, a simulation identifier, a set of simulated scenarios, and/or the like. In one embodiment, the administrative client may provide the following example expected returns calculation request, substantially in the form of a HTTP(S) POST message including XML-formatted data, as provided below:

TABLE-US-00009 POST /expected_returns_calculation_request.php HTTP/1.1 Host: www.server.com Content-Type: Application/XML Content-Length: 667 <?XML version = "1.0" encoding = "UTF-8"?> <expected_returns_calculation_request> <request_identifier>ID_request_5</request_identifier> <universe_of_securities>Securities in S&P 500</universe_of_securities> <simulation_identifier>ID_sim_1</simulation_identifier> <simulated_scenarios>ID_scenario_1, ID_scenario_2, ...</simulated_scenarios> </expected_returns_calculation_request>

[0153] The MLPO server 106 may send a scenario results retrieve request 145 to the repository 110 to facilitate retrieving simulated market factor changes for a simulated scenario. In one implementation, the scenario results retrieve request may include data such as a request identifier, a simulation identifier, a scenario identifier, and/or the like. In one embodiment, the MLPO server may provide the following example scenario results retrieve request, substantially in the form of a HTTP(S) POST message including XML-formatted data, as provided below:

TABLE-US-00010 POST /scenario_results_retrieve_request.php HTTP/1.1 Host: www.server.com Content-Type: Application/XML Content-Length: 667 <?XML version = "1.0" encoding = "UTF-8"?> <scenario_results_retrieve_request> <request_identifier>ID_request_6</request_identifier> <simulation_identifier>ID_sim_1</simulation_identifier> <scenario_identifier>ID_scenario_1</scenario_identifier> </scenario_results_retrieve_request>

[0154] The repository 110 may send a scenario results retrieve response 147 to the MLPO server 106 with the requested simulated market factor changes data. In one implementation, the scenario results retrieve response may include data such as a response identifier, the requested simulated market factor changes data, and/or the like. In one embodiment, the repository may provide the following example scenario results retrieve response, substantially in the form of a HTTP(S) POST message including XML-formatted data, as provided below:

TABLE-US-00011 POST /scenario_results_retrieve_response.php HTTP/1.1 Host: www.server.com Content-Type: Application/XML Content-Length: 667 <?XML version = "1.0" encoding = "UTF-8"?> <scenario_results_retrieve_response> <response_identifier>ID_response_6</response_identifier> <scenario_data> <market_factor> <market_factor_identifier>ID_interest_rate_5Y</market_factor_ide- ntifier> <market_factor_change>25 basis points</market_factor_change> </market_factor> <market_factor> <market_factor_identifier>ID_oil_price</market_factor_identifier- > <market_factor_change>$10</market_factor_change> </market_factor> ... </scenario_data> </scenario_results_retrieve_response>

[0155] An expected returns calculation (ERC) component 149 may utilize data provided in the expected returns calculation request, data provided in the scenario results retrieve response, and/or the trained decision tree ensembles to calculate expected returns for the universe of securities under the simulated scenarios. See FIG. 7A for additional details regarding the ERC component.

[0156] The MLPO server 106 may send an expected returns store request 151 to the repository 110 to facilitate storing the calculated expected returns. In one implementation, the expected returns store request may include data such as a request identifier, expected returns, and/or the like. In one embodiment, the MLPO server may provide the following example expected returns store request, substantially in the form of a HTTP(S) POST message including XML-formatted data, as provided below:

TABLE-US-00012 POST /expected_returns_store_request.php HTTP/1.1 Host: www.server.com Content-Type: Application/XML Content-Length: 667 <?XML version = "1.0" encoding = "UTF-8"?> <expected_returns_store_request> <request_identifier>ID_request_7</request_identifier> <expected_returns> <simulation_identifier>ID_sim_1</simulation_identifier> <scenario> <scenario_identifier>ID_scenario_1</scenario_identifier> <security> <security_identifier>MSFT</security_identifier> <expected_return>10%</expected_return> </security> <security> <security_identifier>AAPL</security_identifier> <expected_return>12%</expected_return> </security> ... </scenario> <scenario> <scenario_identifier>ID_scenario_2</scenario_identifier> <security> <security_identifier>MSFT</security_identifier> <expected_return>15%</expected_return> </security> <security> <security_identifier>AAPL</security_identifier> <expected_return>13%</expected_return> </security> ... </scenario> ... </expected_returns> </expected_returns_store_request>

[0157] The repository 110 may send an expected returns store response 153 to the MLPO server 106 to confirm that the calculated expected returns were stored successfully. In one implementation, the expected returns store response may include data such as a response identifier, a status, and/or the like. In one embodiment, the repository may provide the following example expected returns store response, substantially in the form of a HTTP(S) POST message including XML-formatted data, as provided below:

TABLE-US-00013 POST /expected_returns_store_response.php HTTP/1.1 Host: www.server.com Content-Type: Application/XML Content-Length: 667 <?XML version = "1.0" encoding = "UTF-8"?> <expected_returns_store_response> <response_identifier>ID_response_7</response_identifier> <status>OK</status> </expected_returns_store_response>

[0158] The MLPO server 106 may send an expected returns calculation response 155 to the administrative client 102 to inform the administrative user that expected returns for the universe of securities under the simulated scenarios were calculated successfully. In one implementation, the expected returns calculation response may include data such as a response identifier, a status, and/or the like. In one embodiment, the MLPO server may provide the following example expected returns calculation response, substantially in the form of a HTTP(S) POST message including XML-formatted data, as provided below:

TABLE-US-00014 POST /expected_returns_calculation_response.php HTTP/1.1 Host: www.server.com Content-Type: Application/XML Content-Length: 667 <?XML version = "1.0" encoding = "UTF-8"?> <expected_returns_calculation_response> <response_identifier>ID_response_5</response_identifier> <status>OK</status> </expected_returns_calculation_response>

[0159] FIGS. 2A-B show a logic flow illustrating embodiments of a machine learning simulated scenario processing (MLSSP) component for the MLPO. In FIG. 2A, a machine learning simulated scenario processing request may be obtained at 201. For example, the machine learning simulated scenario processing request may be obtained as a result of an administrative user requesting generation of a set of simulated scenarios.

[0160] A rolling window period length may be determined at 205. In one embodiment, historical data may be analyzed to calculate changes to a set of market factors during each rolling window period of a specified rolling window period length. In one implementation, the machine learning simulated scenario processing request may be parsed (e.g., using PHP commands) to determine historical data to analyze (e.g., based on the value of the historical_data field) and/or the rolling window period length to use for analysis (e.g., based on the value of the rolling_window_period_length field). For example, the machine learning simulated scenario processing request may specify that the last 30 years of historical data should be analyzed using 6 month rolling window periods.

[0161] Market factors to process may be determined at 209. For example, market factors may include interest rates, credit spread, oil price, equity indices, and/or the like, and changes to the market factors during a rolling window period jointly describe a market scenario (e.g., a historical market scenario for historical changes, a simulated market scenario for simulated changes). In one implementation, the machine learning simulated scenario processing request may be parsed (e.g., using PHP commands) to determine the market factors to process (e.g., based on the value of the market_factors field). In another implementation, a set of default market factors to process may be specified in a configuration setting.

[0162] A determination may be made at 213 whether there remain market factors to process. In one implementation, each of the market factors may be processed. If there remain market factors to process, the next market factor (e.g., 6 month change in interest rates) may be selected for processing at 217.

[0163] A determination may be made at 221 whether there remain rolling window periods to analyze. In one implementation, historical data for the selected market factor may be analyzed during each of the rolling window periods. If there remain rolling window periods to analyze, the next rolling window period may be selected for analysis at 225. For example, the next rolling window period may be two specific time points (e.g., days) 6 months apart.

[0164] A determination may be made at 229 whether data for the selected rolling window period is available. In one implementation, this determination may be made based on whether historical data for the selected market factor is available for both time points (e.g., for both days) of the selected rolling window period.

[0165] If historical market factor data is unavailable for one or both time points (e.g., days) of the selected rolling window period, the missing data may be imputed using a machine learning (e.g., k-Nearest Neighbors (k-NN)) method at 233 based on market factor data for other time points (e.g., for other days). In one implementation, the k-NN method may be used to match records (e.g., a record may be a set of market factors for a time point) with missing data points (e.g., a missing data point may be a missing market factor data for a time point) in a multi-dimensional space. For example, the missing data for the selected market factor for a time point may be calculated as the average of values of the selected market factor for k nearest neighbors of the time point as determined based on similarity of the other market factors.

[0166] Change to the selected market factor during the selected rolling window period may be calculated at 237. In one implementation, the change to the selected market factor during the selected rolling window period may be calculated by determining the delta between values of the selected market factor at the two time points of the selected rolling window period. For example, the 6 month change in 5 year interest rates for the rolling window period between Jan. 7, 2019 and Jul. 8, 2019, may be calculated by subtracting the US Treasury 5 Year Par Yield on Jan. 7, 2019 from the US Treasury 5 Year Par Yield on Jul. 8, 2019. In another example, the 6 month change in 5 year interest rates for the rolling window period between Jan. 8, 2019 and Jul. 9, 2019, may be calculated by subtracting the US Treasury 5 Year Par Yield on Jan. 8, 2019 from the US Treasury 5 Year Par Yield on Jul. 9, 2019.

[0167] Once changes to each of the market factors during each of the rolling window periods are calculated, a determination may be made at 241 regarding the type of time period buckets to utilize. In one embodiment, fixed length time period buckets may be utilized. In another embodiment, variable length time period buckets may be utilized. In one implementation, the machine learning simulated scenario processing request may be parsed (e.g., using PHP commands) to determine the type of time period buckets to utilize (e.g., based on the value of the time_period_bucket_type field).

[0168] If fixed length time period buckets are utilized, the length of time period buckets to utilize may be determined at 245. In one implementation, the machine learning simulated scenario processing request may be parsed (e.g., using PHP commands) to determine the length of time period buckets to utilize (e.g., based on the value of the time_period_bucket_length field). For example, the machine learning simulated scenario processing request may specify that historical market scenarios generated from the last 30 years of historical data (e.g., using calculated changes from 237) should be split using 6 month long time period buckets, resulting in 60 time period buckets to process. It is to be understood that the length of time period buckets is independent of the rolling window period length (e.g., the two lengths may be the same or may be different).

[0169] If variable length time period buckets are utilized, time period buckets reflective of changes in volatilities and correlations of the historical data may be determined at 249. In one implementation, the time period buckets may be selected by judging the overall goodness of fit between simulated data from the time period buckets and historical data. KS tests and Cramer test may be performed jointly between the simulated market scenarios and the historical market scenarios. The splitting into time period buckets may support the objective function of minimizing the KS test values of the marginal distributions and Cramer test value of the multivariate distribution of simulated market scenarios vs. realized historical market scenarios. For example, the machine learning simulated scenario processing request may specify that historical market scenarios generated from the last 30 years of historical data (e.g., using calculated changes from 237) should be split by bucketing historical market scenarios from the same economic cycle (e.g., early cycle, mid cycle, late cycle, recession) together to summarize the changes in volatilities and correlation structure. In some implementations, the number of time period buckets may be determined by balancing the amount of historical data vs. the number of market factors. For example, given that data frequency is constant, as the number of market factors increases the time duration utilized for each time period bucket increases.

[0170] The historical market scenarios may be bucketed in accordance with the determined time period buckets at 253. In one implementation, each historical market scenario may be assigned a bucket identifier that specifies the time period bucket associated with the respective historical market scenario.

[0171] A determination may be made at 257 whether there remain time period buckets to process. In one implementation, each of the time period buckets may be processed. If there remain time period buckets to process, the next time period bucket (e.g., historical market scenarios associated with the next 6 month long time period bucket) may be selected for processing at 261.

[0172] A deep learning neural network for the selected time period bucket may be trained at 281. For example, the deep learning neural network may be a Gaussian-Mixture Variational Autoencoder. In one embodiment, the deep learning neural network may be trained to map historical market factor changes to latent space variables and/or to map latent space variables to simulated market factor changes. See FIG. 2B for additional details regarding training the deep learning neural network. See FIG. 3 for an exemplary deep learning neural network architecture.

[0173] The number of market scenarios to simulate may be determined at 289. For example, 1,000 scenarios may be simulated (e.g., resulting in 60,000 total simulated scenarios over 60 time period buckets). In one implementation, the machine learning simulated scenario processing request may be parsed (e.g., using PHP commands) to determine the number of market scenarios to simulate for each of the time period buckets (e.g., based on the value of the number_of_simulated_market_scenarios field). In another implementation, the number of market scenarios to simulate for each of the time period buckets may be specified in a configuration setting. In another implementation, the number of market scenarios to simulate may differ for different time period buckets. For example, the number of market scenarios to simulate may be determined as an AI-driven weight learned by minimizing the L2 Norm between real data and simulated data.

[0174] A determination may be made at 293 whether there remain market scenarios to simulate. If so, simulated data may be generated using latent space variables at 295. In one implementation, random values for latent space variables of the trained deep learning neural network may be generated. For example, a random value for a latent space variable of the trained deep learning neural network may be generated (e.g., by optimizing the number of perceptrons, the number of layers of the encoder and decoder neural networks, and/or the number of latent space variables with the objective function of minimizing the L2 Norm between generated market factor changes and historical market factor changes) from a Gaussian or Gaussian mixture distribution (e.g., from a multivariate Gaussian distribution) using the Python NumPy library (e.g., with three inputs including the number of samples to be generated, mean and variance from the encoder).

[0175] A set of simulated market factor changes may be generated from the simulated data using a neural network decoder of the trained deep learning neural network at 297. In one implementation, the generated random values of latent space variables may be fed through the neural network decoder of the trained deep learning neural network to obtain a set of simulated market factor changes (e.g., the set of simulated market factor changes may be referred to as a simulated market scenario).

[0176] The simulated scenario may be stored in a database at 299. In one implementation, the simulated scenario may be stored (e.g., in a batch with other simulated scenarios) via a scenario results store request.

[0177] FIG. 2B shows additional details regarding training the deep learning neural network. In FIG. 2B, the historical market scenarios (e.g., a set of calculated market factor changes for each rolling window period of the selected time period bucket) may be obtained at 202. In one implementation, a reference to a historical market factor changes data structure (e.g., an array of arrays where each element of the outer array corresponds to a training data point of historical market factor changes for a rolling window period, and each element of the inner array corresponds to a historical return of a market factor during the rolling window period) with the calculated historical market factor changes may be obtained.

[0178] A determination may be made at 206 whether there remain hyper-parameters options of the deep learning neural network to analyze. For example, the hyper-parameters of the deep learning neural network may include the number of layers and/or perceptrons in each layer of encoder and/or decoder, the dimensionality of latent space, and/or the like. In one implementation, the machine learning simulated scenario processing request may be parsed (e.g., using PHP commands) to determine hyper-parameters options to test (e.g., based on the value of the hyper_parameters_to_test field). If there remain hyper-parameters options to analyze, the next set of hyper-parameters (e.g., specified in a hyper_parameters_option field) for the deep learning neural network may be selected for testing at 210.

[0179] A determination may be made at 212 whether a termination condition for training the deep learning neural network has been reached. In various implementations, the termination condition may comprise one or more of a specified number of training iterations, a specified training time, a specified minimum deep learning neural network performance rank, and/or the like.

[0180] If the termination condition for training the deep learning neural network has not been reached, a determination may be made at 214 whether there remain more training data points to use for training the deep learning neural network. In one implementation, each of the training data points in the historical market factor changes data structure may be used for training. If there remain more training data points to use, the next training data point (e.g., historical market factor changes for a rolling window period) may be selected at 218.

[0181] Input and output layers of the deep learning neural network may be set to the selected training data point at 222. In one implementation, the input and output layers may be f-dimensional layers, where f is the number of market factors. For example, the input and output layers may be set to the values of the inner array of the historical market factor changes data structure corresponding to the selected training data point.

[0182] The deep learning neural network may be trained on the selected training data point using a variational autoencoder to generate a set of Gaussian-Mixture latent variables at 226. In one embodiment, the deep learning neural network may be trained using backpropagation with a specified loss function. In one implementation, the loss function may be chosen to minimize mean squared error of the Euclidean distances of individual market factors return values to the historical realized return values, and/or to minimize the variance of joint distributions across encoded market factors between simulated and historical markets in the latent space (e.g., the KL divergence score). In one embodiment, the loss function on factor returns may be in the original factor space, while the KL divergence constraint plays the role in the latent space (lower dimensional space) to map the encoded factors to Gaussian or Gaussian mixture distribution. In one implementation, the encoder and the decoder may be set to have the same structures and during the training process their weights may be synchronized, so that half of the total weights have to be learned to reduce the complexity of deep network training

[0183] Once the deep learning neural network is trained on the training data points, performance of the trained deep learning neural network may be evaluated at 230. For example, the performance of the trained deep learning neural network may be evaluated using a set of testing data points (e.g., available data points may be split into 75% training data points and 25% testing data points). In one embodiment, the trained deep learning neural network may be assigned a performance rank (e.g., a score). In one implementation, differences between market factor changes at the input layer and market factor changes at the output layer may be evaluated using the Kolmogorov-Smirnov (KS) test for individual market factors and/or Cramer test for joint distribution to calculate a performance score for the trained deep learning neural network. For example, for the KS test and/or the Cramer test, the lower the scores, the better the performance. Accordingly, the scores may be sorted in ascending order and performance of deep learning neural networks may be ranked in the hyperparameter tuning process such that the deep learning neural network with the optimal performance is the one with the highest rank.

[0184] If the termination condition for training the deep learning neural network has been reached, the next set of hyper-parameters, if any, for the deep learning neural network may be analyzed at 206.

[0185] The neural network with the optimal performance may be selected at 234. In one implementation, the deep learning neural network with the best (e.g., highest) performance rank may be selected to simulate market scenarios.