Systems And Methods For Projecting Data Trends

Vick; Emma Nicolette ; et al.

U.S. patent application number 17/128429 was filed with the patent office on 2021-04-22 for systems and methods for projecting data trends. The applicant listed for this patent is ICE Benchmark Administration Limited. Invention is credited to Charles Abboud, Timothy Joseph Bowler, Thomas Evans, Andrew John Hill, Gary David Hooper, Paul Anderson Rhodes, Stelios Etienne Tselikas, Emma Nicolette Vick.

| Application Number | 20210117832 17/128429 |

| Document ID | / |

| Family ID | 1000005305603 |

| Filed Date | 2021-04-22 |

View All Diagrams

| United States Patent Application | 20210117832 |

| Kind Code | A1 |

| Vick; Emma Nicolette ; et al. | April 22, 2021 |

SYSTEMS AND METHODS FOR PROJECTING DATA TRENDS

Abstract

Systems and methods for projecting one or more trends in electronic data and generating enhanced data. A system includes a data forecasting system is in electronic communication with one or more electronic data sources via an electronic network. The data forecasting system is configured to: monitor the electronic data source(s) for data that meet one or more predetermined criteria; obtain at least a portion of the monitored data from electronic data source(s) based on the predetermined criteria; create a data set from the obtained data; derive one or more data values associated with the data set over a predetermined period according to a forward-looking term methodology; and utilize the data set and the derived value(s) over the predetermined period to derive at least one data forecast metric associated with the data set.

| Inventors: | Vick; Emma Nicolette; (Middlesex, GB) ; Hill; Andrew John; (Hertfordshire, GB) ; Hooper; Gary David; (Kent, GB) ; Rhodes; Paul Anderson; (London, GB) ; Bowler; Timothy Joseph; (London, GB) ; Abboud; Charles; (London, GB) ; Tselikas; Stelios Etienne; (St. Albans, GB) ; Evans; Thomas; (Surrey, GB) | ||||||||||

| Applicant: |

|

||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Family ID: | 1000005305603 | ||||||||||

| Appl. No.: | 17/128429 | ||||||||||

| Filed: | December 21, 2020 |

Related U.S. Patent Documents

| Application Number | Filing Date | Patent Number | ||

|---|---|---|---|---|

| 16662173 | Oct 24, 2019 | 10891551 | ||

| 17128429 | ||||

| 62752732 | Oct 30, 2018 | |||

| Current U.S. Class: | 1/1 |

| Current CPC Class: | G06N 5/046 20130101; G06Q 10/04 20130101 |

| International Class: | G06N 5/04 20060101 G06N005/04; G06Q 10/04 20060101 G06Q010/04 |

Claims

1. A system for projecting one or more trends in electronic data and generating enhanced data, comprising: a dedicated website portal configured to generate at least one webpage comprising an input selection portion for selecting a time period, a benchmark data portion for publishing benchmark data associated with a selected time period and a projected data portion; a data forecasting system in electronic communication with one or more electronic data sources and the dedicated website portal via an electronic network, the data forecasting system comprising non-transitory memory storing computer readable instructions and at least one processor configured to execute the computer readable instructions, the data forecasting system configured to: monitor the one or more electronic data sources for data that meet one or more predetermined criteria; obtain at least a portion of the monitored data from among the one or more electronic data sources based on the one or more predetermined criteria; create a data set from the obtained data, the data set comprising a combination of futures price data, overnight index swap price data, and rate data; derive one or more data values associated with the combination over a predetermined period according to a forward-looking term methodology, the predetermined period comprising the selected time period received via the input selection portion of the dedicated website portal, the forward-looking term methodology comprising execution of a series of calculations involving at least one of the rate data, the futures price data and the overnight index swap price data, the results of which produce projected expected rate data that is predictive of future rate changes over the predetermined period, said projected expected rate data comprising said derived one or more data values; utilize the data set and the one or more derived data values over the predetermined period to derive at least one data forecast metric associated with the data set; and disseminate the at least one data forecast metric to the dedicated website portal, such that at least the projected data portion of the at least one webpage is updated to display the at least one data forecast metric reflecting the selected time period.

2. The system of claim 1, wherein the data set includes the futures price data but not the overnight index swap price data.

3. The system of claim 1, wherein the data set includes the overnight index swap price data but not the futures price data.

4. The system of claim 3, wherein the rate data comprises at least one of fixed rate data and floating rate data.

5. The system of claim 1, wherein the data set includes both the overnight index swap price data and the futures price data.

6. The system of claim 1, wherein the forward-looking term methodology, performed by the data forecasting system, is customized according to the combination.

7. The system of claim 1, wherein the combination includes the futures price data and the rate data includes risk free rate data, the data forecasting system, as part of the forward-looking term mythology, is further configured to: identify and select each of relevant risk free rate data and relevant futures price data associated with the predetermined period from among the data set, based on predetermined eligibility criteria; determine, for the futures price data, one or more sub-periods within the predetermined period associated with at least one predicted change in the rate data; imply, for each of the one or more sub-periods, one or more implied rates based on the selected risk free rate data and the selected futures price data; and compound the one or more implied rates to derive a forward-looking term setting for the predetermined period, the one or more data values comprising the one or more implied rates and the at least one data forecast metric comprising the forward-looking term setting.

8. The system of claim 7, wherein the risk free rate data includes overnight rate data.

9. The system of claim 1, wherein the combination includes the overnight index swap price data and the one or more electronic data sources include multiple central limit order books, the data forecasting system, as part of the forward-looking term methodology, is further configured to: obtain one or more snapshots of the overnight index swap price data from among the multiple central limit order books at one or more randomized times; exclude one or more among said obtained snapshots via integrity testing; combine remaining snapshots among said one or more snapshots into a global synthetic order book, responsive to said exclude; calculate, for said combined snapshots, one or more volume-weighted average mid-price (VWAMP) values; and quality weight the one or more VWAMP values by spread to derive the forward-looking term setting for the predetermined period.

10. The system of claim 1, wherein: the series of calculations executed by the forward-looking term methodology further involves at least one of executed transaction data, firm quote data, indicative quote data, and settlement price data.

11. The system of claim 1, wherein: the data set includes both the overnight index swap price data and the futures price data, and wherein the series of calculations executed by the forward-looking term methodology further involves at least one of executed transaction data, firm quote data, indicative quote data, and settlement price data, specific to each of the overnight index swap price data and the futures price data.

12. The system of claim 1, wherein: when the data set includes the futures price data, said futures price data is obtained during predetermined time intervals based on one or more predetermined conditions, specific to said futures price data, and when the data set includes the overnight index swap price data, said overnight index swap price data is obtained during predetermined time intervals based on one or more predetermined conditions, specific to said overnight index swap price data.

13. A method for projecting one or more trends in electronic data and generating enhanced data, the method comprising: providing a dedicated website portal configured to generate at least one webpage comprising an input selection portion for selecting a time period, a benchmark data portion for publishing benchmark data associated with a selected time period and a projected data portion; providing a data forecasting system in electronic communication with one or more electronic data sources and the dedicated website portal via an electronic network, the data forecasting system comprising non-transitory memory storing computer readable instructions and at least one processor configured to execute the computer readable instructions; monitoring, by the data forecasting system, the one or more electronic data sources for data that meet one or more predetermined criteria; obtaining, by the data forecasting system, at least a portion of the monitored data from among the one or more electronic data sources based on the one or more predetermined criteria; creating, by the data forecasting system, a data set from the obtained data, the data set comprising a combination of futures price data, overnight index swap price data, and rate data; deriving, by the data forecasting system, one or more data values associated with the combination over a predetermined period according to a forward-looking term methodology, the predetermined period comprising the selected time period received via the input selection portion of the dedicated website portal, the forward-looking term methodology comprising executing a series of calculations involving at least one of the rate data, the futures price data and the overnight index swap price data, the results of which produce projected expected rate data that is predictive of future rate changes over the predetermined period, said projected expected rate data comprising said derived one or more data values; utilizing, by the data forecasting system, the data set and the one or more derived data values over the predetermined period to derive at least one data forecast metric associated with the data set; and disseminating the at least one data forecast metric to the dedicated website portal, such that at least the projected data portion of the at least one webpage is updated to display the at least one data forecast metric reflecting the selected time period.

14. The method of claim 13, wherein the data set includes the futures price data but not the overnight index swap price data.

15. The method of claim 13, wherein the data set includes the overnight index swap price data but not the futures price data.

16. The method of claim 15, wherein the rate data comprises at least one of fixed rate data and floating rate data.

17. The method of claim 13, wherein the data set includes both the overnight index swap price data and the futures price data.

18. The method of claim 13, wherein the forward-looking term methodology is customized according to the combination.

19. The method of claim 13, wherein the combination includes the futures price data and the rate data includes risk free rate data, the forward-looking term methodology further comprising: identifying and selecting, by the data forecasting system, each of relevant risk free rate data and relevant futures price data associated with the predetermined period from among the data set, based on predetermined eligibility criteria; determining, by the data forecasting system, for the futures price data, one or more sub-periods within the predetermined period associated with at least one predicted change in the rate data; implying, by the data forecasting system, for each of the one or more sub-periods, one or more implied rates based on the selected risk free rate data and the selected futures price data; and compounding, by the data forecasting system, the one or more implied rates to derive a forward-looking term setting for the predetermined period, the one or more data values comprising the one or more implied rates and the at least one data forecast metric comprising the forward-looking term setting.

20. The method of claim 19, wherein the risk free rate data includes overnight rate data.

21. The method of claim 13, wherein the combination includes the overnight index swap price data and the one or more electronic data sources include multiple central limit order books, the forward-looking term methodology further comprising: obtaining, by the data forecasting system, one or more snapshots of the overnight index swap price data from among the multiple central limit order books at one or more randomized times; excluding, by the data forecasting system, one or more among said obtained snapshots via integrity testing; combining, by the data forecasting system, remaining snapshots among said one or more snapshots into a global synthetic order book, responsive to said excluding; calculating, for said combined snapshots, by the data forecasting system, one or more volume-weighted average mid-price (VWAMP) values; and quality weighting, by the data forecasting system, the one or more VWAMP values by spread to derive the forward-looking term setting for the predetermined period.

22. The method of claim 13, wherein: the series of calculations executed by the forward-looking term methodology further involves at least one of executed transaction data, firm quote data, indicative quote data, and settlement price data.

23. The method of claim 13, wherein: the data set includes both the overnight index swap price data and the futures price data, and wherein the series of calculations executed by the forward-looking term methodology further involves at least one of executed transaction data, firm quote data, indicative quote data, and settlement price data, specific to each of the overnight index swap price data and the futures price data.

24. The method of claim 13, wherein: when the data set includes the futures price data, said futures price data is obtained during predetermined time intervals based on one or more predetermined conditions, specific to said futures price data, and when the data set includes the overnight index swap price data, said overnight index swap price data is obtained during predetermined time intervals based on one or more predetermined conditions, specific to said overnight index swap price data.

25. A non-transitory computer readable medium storing computer readable instructions that, when executed by one or more processing devices, cause the one or more processing devices to perform the functions comprising: providing a dedicated website portal configured to generate at least one webpage comprising an input selection portion for selecting a time period, a benchmark data portion for publishing benchmark data associated with a selected time period and a projected data portion; monitoring one or more electronic data sources for data that meet one or more predetermined criteria, the one or more processing devices in communication with the one or more electronic data sources and the dedicated website portal via an electronic network; obtaining at least a portion of the monitored data from among the one or more electronic data sources based on the one or more predetermined criteria; creating a data set from the obtained data, the data set comprising a combination of futures price data, overnight index swap price data, and rate data; deriving one or more data values associated with the combination over a predetermined period according to a forward-looking term methodology, the predetermined period comprising the selected time period received via the input selection portion of the dedicated website portal, the forward-looking term methodology comprising executing a series of calculations involving at least one of the rate data, the futures price data and the overnight index swap price data, the results of which produce projected expected rate data that is predictive of future rate changes over the predetermined period, said projected expected rate data comprising said derived one or more data values; utilizing the data set and the one or more derived data values over the predetermined period to derive at least one data forecast metric associated with the data set; and disseminating the at least one data forecast metric to the dedicated website portal, such that at least the projected data portion of the at least one webpage is updated to display the at least one data forecast metric reflecting the selected time period.

26. The non-transitory computer readable medium of claim 25, wherein the combination includes the futures price data and the rate data includes risk free rate data, the computer readable instructions, when executed by one or more processing devices, further causing the one or more processing devices to perform, as part of the forward-looking term methodology, the functions of: identifying and selecting each of relevant risk free rate data and relevant futures price data associated with the predetermined period from among the data set, based on predetermined eligibility criteria; determining for the futures price data, one or more sub-periods within the predetermined period associated with at least one predicted change in the rate data; implying for each of the one or more sub-periods, one or more implied rates based on the selected risk free rate data and the selected futures price data; and compounding the one or more implied rates to derive a forward-looking term setting for the predetermined period, the one or more data values comprising the one or more implied rates and the at least one data forecast metric comprising the forward-looking term setting.

27. The non-transitory computer readable medium of claim 25, wherein the combination includes the overnight index swap price data and the one or more electronic data sources include multiple central limit order books, the computer readable instructions, when executed by one or more processing devices, further causing the one or more processing devices to perform, as part of the forward-looking term methodology, the functions of: obtaining one or more snapshots of the overnight index swap price data from among the multiple central limit order books at one or more randomized times; excluding one or more among said obtained snapshots via integrity testing; combining remaining snapshots among said one or more snapshots into a global synthetic order book, responsive to said excluding; calculating, for said combined snapshots, one or more volume-weighted average mid-price (VWAMP) values; and quality weighting the one or more VWAMP values by spread to derive the forward-looking term setting for the predetermined period.

28. The non-transitory computer readable medium of claim 25, wherein: the series of calculations executed according to the forward-looking term methodology further involves at least one of executed transaction data, firm quote data, indicative quote data, and settlement price data.

29. The non-transitory computer readable medium of claim 25, wherein: the data set includes both the overnight index swap price data and the futures price data, and wherein the series of calculations executed according to the forward-looking term methodology further involves at least one of executed transaction data, firm quote data, indicative quote data, and settlement price data, specific to each of the overnight index swap price data and the futures price data.

30. The non-transitory computer readable medium of claim 25, wherein: when the data set includes the futures price data, said futures price data is obtained during predetermined time intervals based on one or more predetermined conditions, specific to said futures price data, and when the data set includes the overnight index swap price data, said overnight index swap price data is obtained during predetermined time intervals based on one or more predetermined conditions, specific to said overnight index swap price data.

Description

TECHNICAL FIELD

[0001] The present disclosure generally relates to improving data structure management and, in particular, to data structure management systems and methods for projecting data trends.

BACKGROUND

[0002] Problems exist in the field of electronic data conversion, data projection and data distribution. Users of products, systems, processes or instruments which seek to represent, reflect or measure underlying data types/data sets that are complex or are difficult to analyze, or data types/data sets with sparse underlying electronic data, or data types/data sets with underlying data that are difficult to access or analyze often seek additional information in order to analyze, project forward or otherwise utilize these data types/data sets. One use of electronic data (e.g., input data) is in the creation of data metrics (or other statistical analyses/applications) for those data types/data sets that are complex or difficult to analyze, having sparse underlying electronic data or with underlying data that are difficult to access or analyze. Because the underlying electronic data is sparse, or difficult to access, or because the underlying data is complex or difficult to analyze, it may be difficult to generate accurate data metrics, including projecting data trends (e.g., data forecasting). In the absence of sufficient data and information, and the correct analysis and processing, conventional metrics (based on the sparse data and information) are often inaccurate and unreliable, or no appropriate conventional metric may exist. Accordingly, there is a need for improved data conversion and distribution systems which are able to generate accurate metrics, even if the underlying data being used is sparse or difficult to access or analyze, or if the data types/data sets being measured are complex or are difficult to analyze.

SUMMARY

[0003] Aspects of the present disclosure relate to systems and methods for projecting one or more trends in electronic data and generating enhanced data. A system includes a data forecasting system in electronic communication with one or more electronic data sources via an electronic network. The data forecasting system includes non-transitory memory storing computer readable instructions and at least one processor configured to execute the computer readable instructions. The data forecasting system is configured to: monitor the one or more electronic data sources for data that meet one or more predetermined criteria; obtain at least a portion of the monitored data from among the one or more electronic data sources based on the one or more predetermined criteria; create a data set from the obtained data; derive one or more data values associated with the data set over a predetermined period according to a forward-looking methodology; and utilize the data set and the one or more derived data values over the predetermined period to derive at least one data forecast metric associated with the data set.

BRIEF DESCRIPTION OF DRAWINGS

[0004] FIG. 1 is a functional block diagram of an example data structure management environment for projecting data trends, according to an aspect of the present disclosure.

[0005] FIG. 2 is a functional block diagram of an example data verifier associated with the environment shown in FIG. 1, according to an aspect of the present disclosure.

[0006] FIG. 3 is a flow chart diagram illustrating an example method for projecting one more trends in electronic data and generating enhanced data, according to an aspect of the present disclosure.

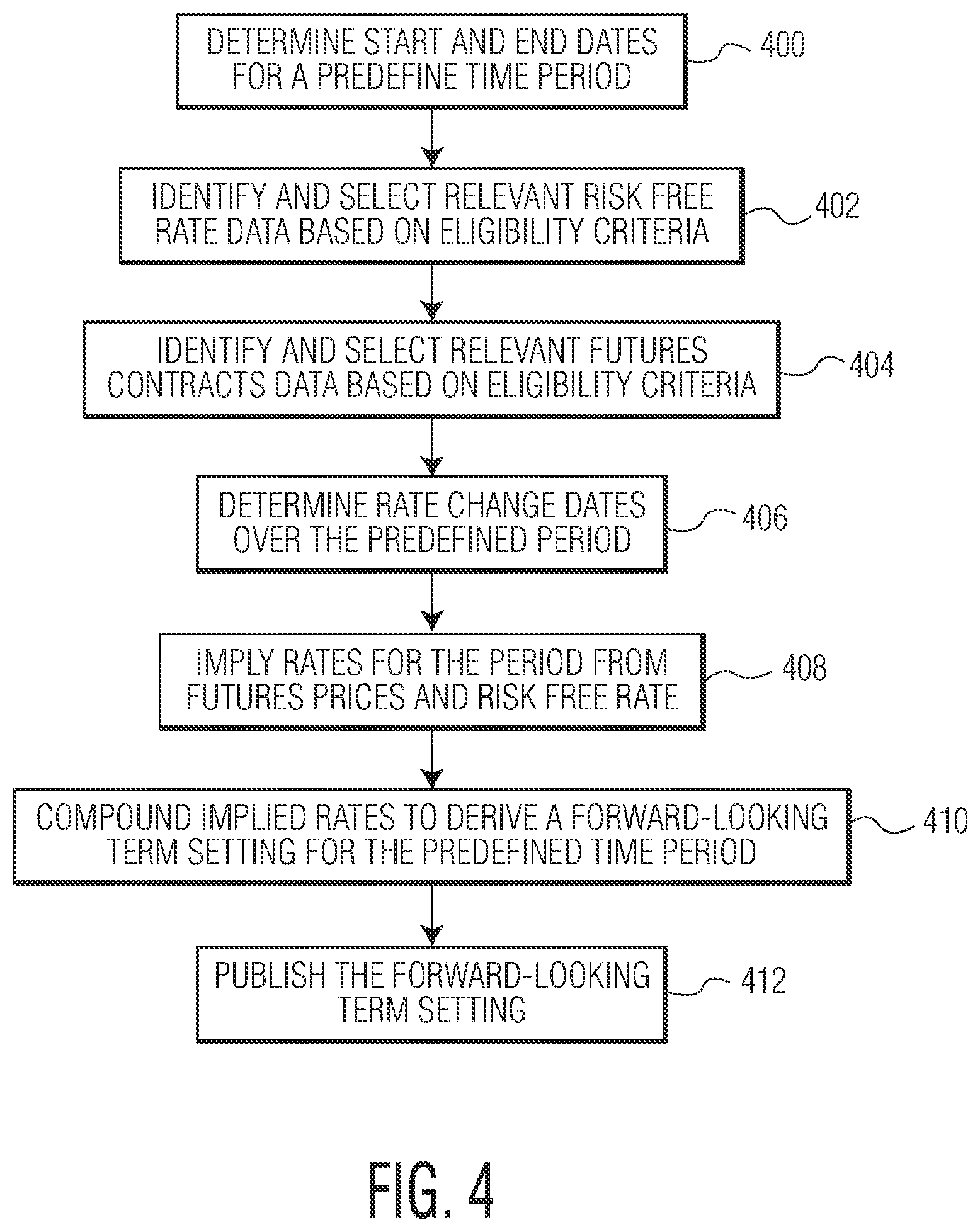

[0007] FIG. 4 is a flow chart diagram illustrating an example method for projecting data trends including forward-looking term interest rate(s), according to another aspect of the present disclosure.

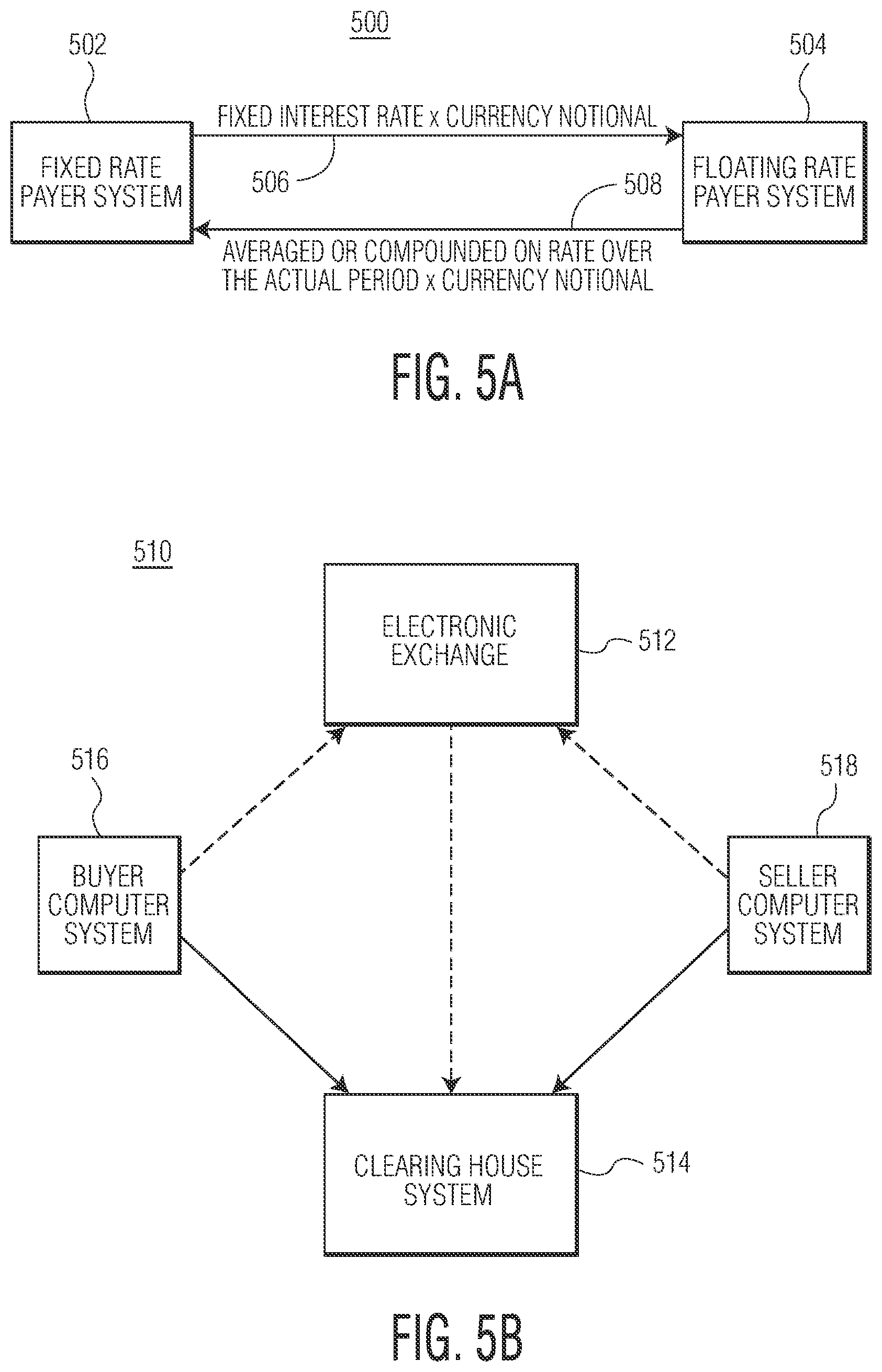

[0008] FIG. 5A is s a functional block diagram of an example overnight index swap transaction system, according to an aspect of the present disclosure.

[0009] FIG. 5B is a functional block diagram of an example futures transaction system, according to an aspect of the present disclosure.

[0010] FIG. 6A is graph illustrating an example overnight rate for index futures notional volume over a time period, according to an aspect of the present disclosure.

[0011] FIG. 6B is graph illustrating an example overnight rate for index futures open interest notional over a time period, according to an aspect of the present disclosure.

[0012] FIG. 7 is a diagram illustrating an example timeline for deriving a forward-looking term interest rate, according to an aspect of the present disclosure.

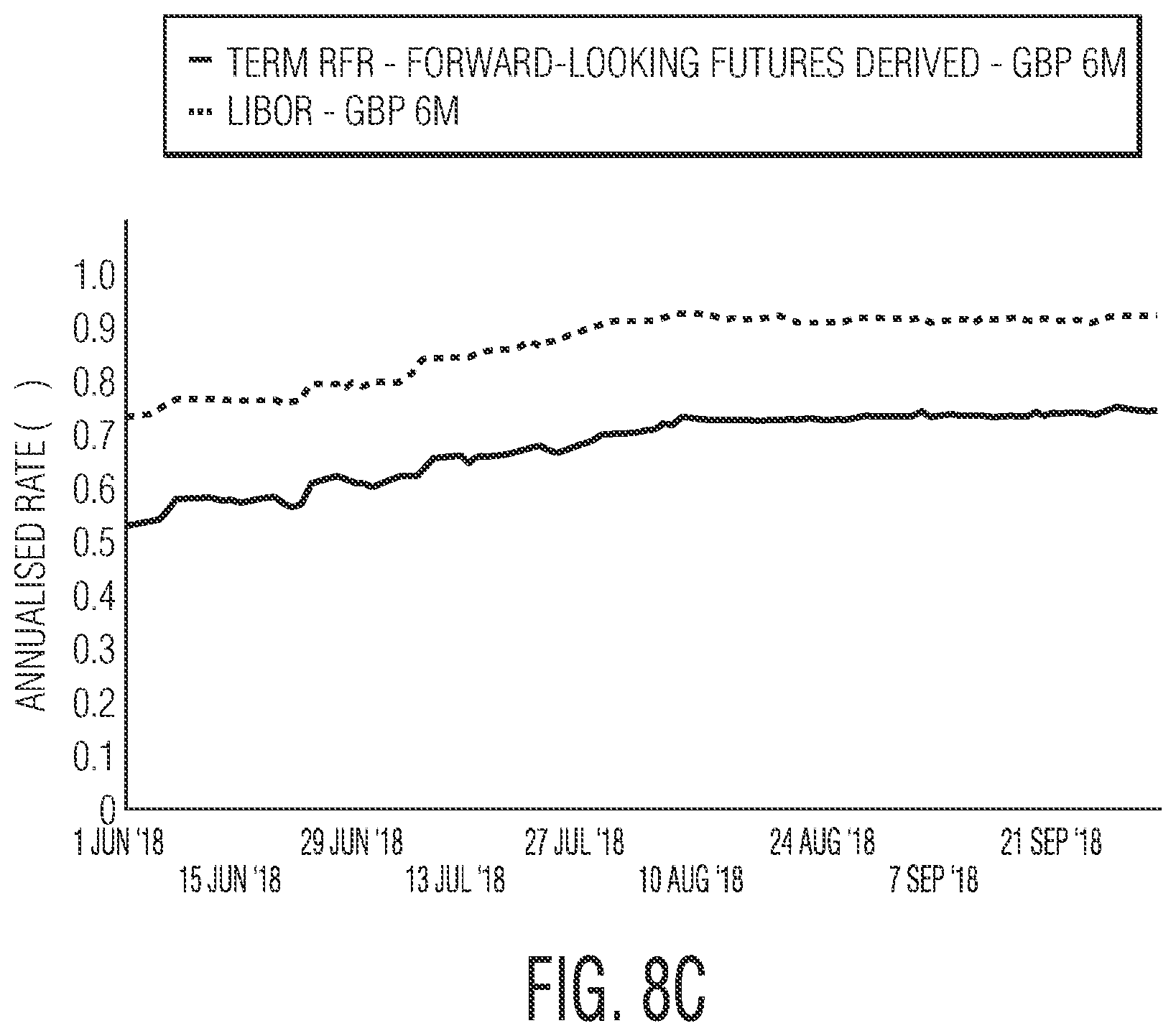

[0013] FIGS. 8A, 8B and 8C are graphs of derived forward-looking term risk free rates for various tenors and corresponding term benchmark interest rates, according to an aspect of the present disclosure.

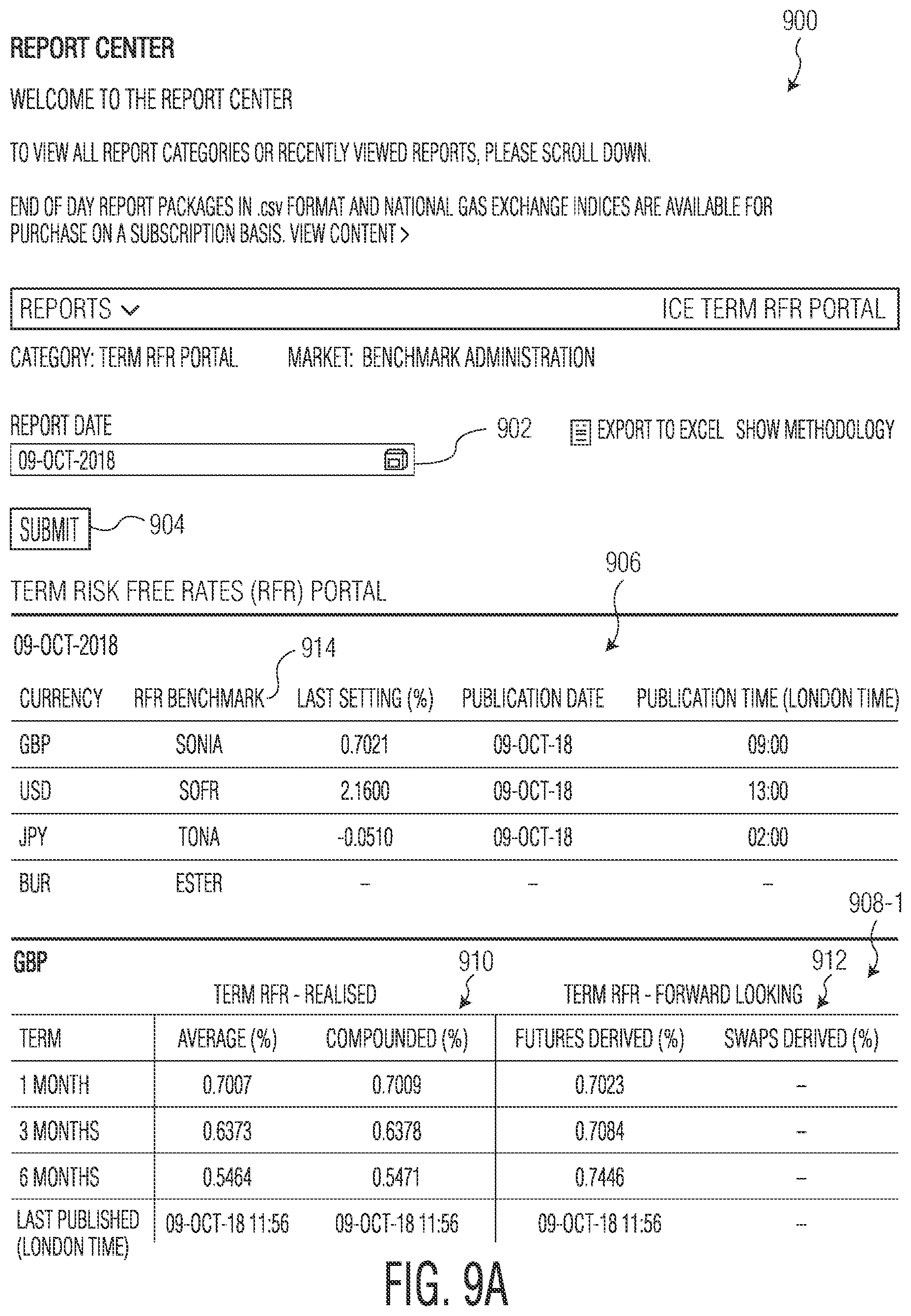

[0014] FIGS. 9A and 9B are a schematic representation of an example dedicated website portal used in connection with an aspect of the present disclosure.

[0015] FIG. 10 is a functional block diagram of an example computer system, according to an aspect of the present disclosure.

DETAILED DESCRIPTION

[0016] Aspects of the present disclosure relate to data structure management systems and methods for projecting data trends (e.g., data metrics) and/or isolating and converting the underlying data into data metrics, such as one or more forward-looking term interest rates. The data structure management systems and methods of the present disclosure may isolate, monitor and/or verify data from among one or more data sources, and convert the verified data into one or more data metrics and/or data trend projections such as, without being limited to, one or more forward-looking term interest rates. Systems and methods of the present disclosure are operationally efficient (by isolating, analyzing and appropriately processing only the verified data) and may result in the creation of more accurate data trend projections (through analysis of only the verified/monitored data).

[0017] Moreover, the data structure management systems provide technical improvements over conventional systems and techniques. This is because the data structure management systems of the present disclosure include an unconventional data forecasting technique that includes obtaining verified data from among one or more networked data sources and projecting the obtained data into forward-looking term interest rate(s) through a unique data trend projection algorithm. The unconventional technique is able to create accurate data trend projections even when the data sources provide sparse data, where the data is difficult to access or analyze, or where the trend projection is complex or difficult to analyze. The ability to create accurate data trend projections (even with sparse data or data that is difficult to access or analyze) does not exist in conventional systems/techniques and, thus, conventional systems/techniques may produce inaccurate and unreliable or inappropriate data forecasts.

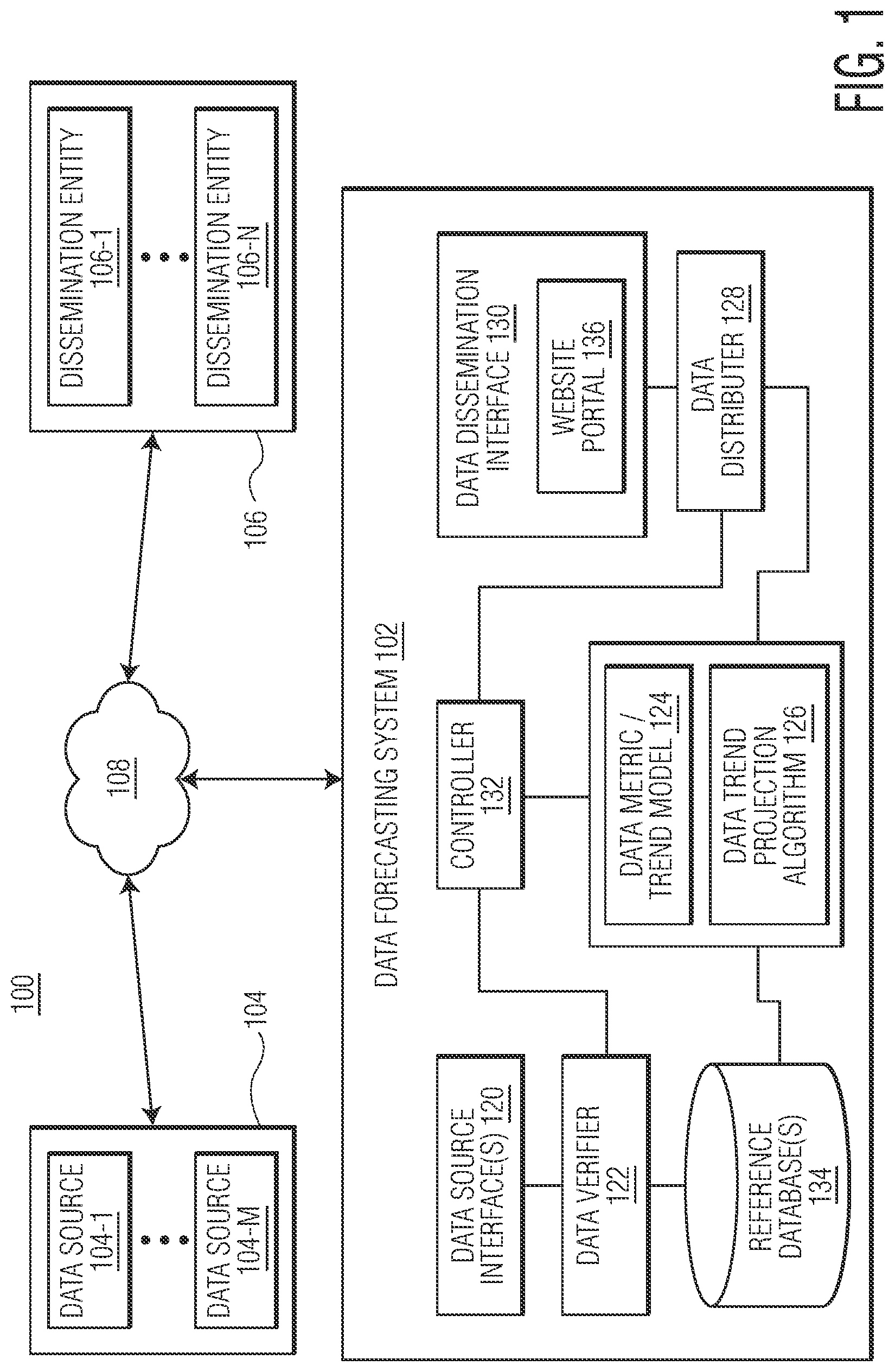

[0018] Turning now to FIG. 1, a functional block diagram of an example data structure management environment 100 for projecting data trends, according to aspects of the present disclosure, is shown. Environment 100 may include data forecasting system 102 (also referred to herein as DF system 102), one or more data sources 104-1, . . . , 104-M (designated generally as data source(s) 104, where M is greater than or equal to 1) and one or more dissemination entities 106-1, . . . , 106-N (designated generally as dissemination entity(s) 106, where N is greater than or equal to 1, and where M may or not be equal to N). DF system 102, data source(s) 104 and dissemination entity(s) 106 may be communicatively coupled via one or more communication networks 108. The one or more networks 108 may include, for example, a private network (e.g., a local area network (LAN), a wide area network (WAN), intranet, etc.) and/or a public network (e.g., the Internet).

[0019] In general, DF system 102 may be configured to communicate with data source(s) 104, obtain verified (e.g., accurate) data among data pushed and/or pulled from data source(s) 104 (e.g., input data) and convert the input data into metric data and/or create forecasted data (e.g., one or more projected data trends) from among the verified data. DF system 102 may also be configured to communicate with and distribute input data, verified data, metric data and/or forecasted data among dissemination entity(s) 106. In some examples, DF system 102 may be configured to format, filter, aggregate and/or normalize data that is disseminated to dissemination entity(s) 106.

[0020] In some examples, DF system 102 may include one or more techniques (such as data trend projection algorithm 126) for handling data sets (including sparse data sets, or data that is difficult to access or analyze) among data source(s) 104. In some, non-limiting examples, data source(s) 104 may represent sources of financial and interest rate data, and the forecasted data may include one or more forward-looking term interest rates created from the financial and interest rate data. In some non-limiting examples, input data may include risk free rate data and futures contract data, and the metric and/or forecasted data to be determined may include expected future risk free rates over one or more specified tenor periods. In some non-limiting examples, input data may include overnight index swap data and/or futures contract data. It may be appreciated that the techniques described herein for projecting data trends may be applied to data classes associated with other technical fields aside from electronic or financial markets, such as, without being limited to, cancer research, seismic activity analysis, climate modeling, etc. In general, although DF system 102 is described in some examples below with respect to data classes associated with electronic transactional data, DF system 102 may be used with any electronic data classes associated with any type of electronic data, including those having sparse data. Examples of such data classes may include, for example, traffic data, population data, voting tendency data, and any other class of data where continuous or complete data may not always be available.

[0021] In general, data source(s) 104 may comprise a server computer, a desktop computer, a laptop, a smartphone, tablet, or any other computing device known in the art configured to capture, receive, store and/or disseminate any suitable data associated with one or more data classes. In one non-limiting example, one or more of data source(s) 104 may include sources of electronic financial data. In some examples, data sources 104 may be selected based on their perceived relevance to the data class and/or usefulness in the determination of data metrics and/or projected trends.

[0022] In general, dissemination entity(s) 106 may comprise a server computer, a desktop computer, a laptop, a smartphone, tablet, or any other computing device known in the art configured to capture, receive, store and/or disseminate any suitable data. In some examples, one or more user devices (not shown) may be configured to communicate with one or more among dissemination entity(s) 106. In some examples, one or more of dissemination entity(s) 106 may include a user device. For example, the user device may receive disseminated data directly from DF system 102 (such as via website portal 136).

[0023] In one non-limiting example, dissemination entity(s) 106 may include one or more redistribution platforms (e.g., Bloomberg, Refinitiv) for disseminating electronic data (e.g., transactional data). In some examples, dissemination entity(s) 106 may include one or more websites published on at least one web server. In one example, the disseminated data (via dissemination entity(s) 106 and/or website portal 136) may be used, for example, by data managers, data analysts, regulatory compliance teams, and the like.

[0024] In one non-limiting example, data source(s) 104 may include one or more data sources configured to provide (e.g., via push and/or pull techniques) data to DF system 102 including risk free interest rate data (e.g., data source 104-1), futures price data (e.g., data source 104-2), business day calendar information (e.g., data source 104-3), and calendar information regarding one or more scheduled central bank meeting dates (e.g., data source 104-4). Other examples may include overnight index swap trading data (not shown), futures trading data (not shown), and/or any other suitable data. In this example, the input data from among data sources 104-1, 104-2, 104-3, 104-4 may be associated with one or more currencies (e.g., British pound sterling (GBP), US dollar (USD), Swiss franc (CHF), European Union euro (EUR), Japanese yen (JPY), etc.).

[0025] For example, data source 104-1 may provide risk free interest rate data, including a rate associated with the particular day (of the submitted data). In some examples, DF system 102 (e.g., via data verifier 122) may obtain the risk free interest rate data through one or more live feeds. In some examples, DF system 102 may obtain the risk free rate data through one or more file transfers. In some examples, the file transfer may include a secure file transfer. In some examples, the risk free rate data may be obtained from a relevant administrator of data source 104-1. In some examples, the risk free rate data may be obtained from a redistributor of data source 104-1.

[0026] In some examples, data verifier 122 may apply one or more verification criteria to the risk free interest rate data obtained from data source 104-1. The verification criteria may include, for example, corroborative data source checks, date checks, holiday calendar checks, price variation checks and/or rate error checks. In some examples, data verifier 122 may verify whether the obtained data meets the verification criteria upon submission to DF system 102. When the obtained data meets the verification criteria, data verifier 122 may permit the data from data source 104-1 to be processed by DF system 102. When the obtained data does not meet the verification criteria, in some examples, data verifier 122 may permit the data from data source 104-1 to be discarded by DF system 102. In some examples, the verification criteria for data from data source 104-1 may be determined by an administrator of DF system 102.

[0027] Data source 104-2 may provide futures price data. In some examples, data source 104-2 may include one or more electronic exchanges or one or more other electronic trading venues or one or more trade repositories that may obtain, store and/or publish futures price data. In some examples, DF system 102 (e.g., data verifier 122) may obtain the futures price data from data source 104-2 through one or more live data feeds and/or one or more file transfers. In some examples, the file transfer may include a secure file transfer. In some examples, the data from data source 104-2 may represent futures settlement price data for a previous day. In some examples, the data from data source 104-2 may represent futures price data for a same day transaction or quote data, for example, from one or more electronic exchanges or at least one other electronic trading venue or at least one trade repository.

[0028] In some examples, data verifier 122 may apply one or more verification criteria to the futures price data obtained from data source 104-2. The verification criteria may include, for example, corroborative data source checks, product checks, date checks, maturity checks, holiday calendar checks, price variation checks and/or price error checks. In some examples, data verifier 122 may verify whether the obtained data meets the verification criteria upon submission to DF system 102. When the obtained data meets the verification criteria, data verifier 122 may permit the data from data source 104-2 to be processed by DF system 102. When the obtained data does not meet the verification criteria, in some examples, data verifier 122 may permit the data from data source 104-2 to be discarded by DF system 102. In some examples, the verification criteria for data from data source 104-2 may be determined by an administrator of DF system 102. In this manner, data verifier 122 may ensure that only pertinent data and information is used in the metric and data trend projection calculations, thereby improving the accuracy of any resulting calculations while at the same time reducing the amount of data and information that must be modeled (e.g., run through data trend projection algorithm 126 that executes the data forecasting calculations), thereby preserving system resources. In some examples, data verifier 122 may obtain verified data from among data source(s) 104, may verify data once obtained from data source(s) 104 and/or may perform any combination thereof.

[0029] Data source 104-3 may include one or more suitable data providers of information regarding one or more business day calendars (e.g., a business day calendar for the United States, a business day calendar for the United Kingdom, etc.). Data source 104-4 may include one or more suitable data providers of information regarding at least one calendar of scheduled central bank meeting dates (e.g., for the United Kingdom, etc.).

[0030] Data source(s) 104 may include additional electronic data and/or other information useful for supplementing and/or generating data forecasts for sparse electronic data sets (e.g., data sets that are incomplete, have corrupt data, inherently only include a limited amount of data, etc.). The electronic data and/or information may include suitable real-time data and/or archived data which may be related to a data class having sparse data and which may be useful for determining data metrics and data trend projections for the data class. Data source(s) 104 may include internal and/or external data sources which may provide the real-time and/or archived data. Internal data sources may include, for example, data sources that are a part of the particular entity or system seeking to supplement and/or generate data forecasts for a data class (having a limited amount of data points) that pertains to that particular entity/system. External data sources may include, for example, sources of data and information other than the entity or system that is seeking to supplement and/or generate the data forecasts. Data source(s) 104 may also include automated data disseminators, data streams (e.g., constant or intermittent), data aggregators (e.g., that may store information and data related to multiple data classes and which data/information may be obtained from a plurality of other internal and/or external data sources), etc. In some examples, data source(s) 104 may include news and media outlets, electronic exchanges, financial market participants, regulators' systems, etc. Data source(s) 104 may contain information related to domestic and foreign products and/or services.

[0031] Each of data source(s) 104 may generate electronic data which may, in some examples, include electronic data files. The electronic data may include additional data and information pertinent to sparse electronic data (e.g., may be useful for generating data metrics and/or data trend projections). Notably, any type of data may be included in the generated electronic data, depending on the particular industry and/or implementation of data forecasting system 102 of the present disclosure. In one example, the electronic data may be produced by data source(s) 104 at a predetermined event or time (e.g., an end of a business day). Alternatively, the electronic data may be produced periodically (e.g., on an hourly or weekly basis), or ad hoc at any other desired time interval.

[0032] In some examples, one or more among data source(s) 104 may push electronic data to DF system 102 (e.g., via a server push type of network communication) without receiving any request from DF system 102. For example, data source(s) 104 may push data to DF system 102 in near-real or real-time, periodically, based on an occurrence of predefined events (e.g., predefined time(s), predefined date(s), etc.), based on changes in data, based on an existence of new data, etc.

[0033] In some examples, DF system 102 may be configured to pull data (e.g., via a client pull type of network communication) from among one or more among data source(s) 104 by transmitting one or more data requests and/or interrogating the one or more data source(s) 104. For example, data source 104-1 may be configured to send data to DF system 102 in response to a data request from DF system 102.

[0034] In some examples, a data feed may be configured to deliver at least one data stream from among one or more of data source(s) 104 to DF system 102. The data stream(s) may be delivered, for example, automatically or on demand. In general, data feeds may be configured in one or more formats including, without being limited to, RSS (e.g., RDF Site Summary, Rich Site Summary, Really Simple Syndication), Atom, Resource Description Framework (RDF), comma-separated values (CSV), JavaScript Object Notation (JSON) and Extensible Markup Language (XML).

[0035] In some examples, DF system 102 may obtain data from among one or more of data source(s) 104 via at least one data file transfer according to a suitable file transfer protocol. To illustrate, one or more computer files may be transmitted through an electronic communication channel established between a data source (e.g., data source 104-1) and DF system 102, mediated via a suitable communications protocol. In general, the communication protocol represents a system of rules, syntax, semantics, synchronization of communication and/or error recovery methods that allow two or more computer systems to exchange information. In general, the file transfer protocol implements rules to transfer files between two computing endpoints. The file transfer protocol may include an unsecured file transfer protocol, a secure file transfer (SFT) protocol, a multicast routing protocol and/or a managed file transfer (MFT) protocol. Non-limiting examples of file transfer protocols include File Transfer Protocol (FTP), Secure Shell (SSH) file transfer protocol (SFTP), Hypertext Transfer Protocol (HTTP), HTTP Secure (HTTPS) and EForward. The communications protocol and the file transfer protocol may be implemented by hardware, software or a combination thereof.

[0036] DF system 102 may include one or more data source interfaces 120, data verifier 122, data metric/trend model 124 having at least one data trend projection (DTP) algorithm 126, data distributer 128, data dissemination interface 130, controller 132 and one or more reference databases 134. In some examples, data dissemination interface 130 may include website portal 136 (described further below). In some examples, data dissemination interface 130 may disseminate data through, without being limited to, email, file transfer (e.g., secure and/or unsecure) a communications channel, a data feed, etc. In some examples, components 120-136 may communicate with each other via a data and control bus (not shown).

[0037] Data source interface(s) 120 may represent, for example, an electronic device including hardware circuitry and/or an application on an electronic device for communication with data source(s) 104. In some examples, data source interface(s) 120 may include more than one interface, with different interfaces dedicated to different data source(s) 104 depending upon the communication and/or data transfer capabilities of particular ones of data source(s) 104.

[0038] Data dissemination interface 130 may represent, for example, an electronic device including hardware circuitry and/or an application on an electronic device for communication with dissemination entity(s) 106. Although one dissemination interface 130 is shown in FIG. 1, it is understood that dissemination interface 130 may include one or more interfaces. For example, dissemination interface 130 may include more than one interface, with different interfaces dedicated to different dissemination entity(s) 106 depending upon the communication and/or data transfer capabilities of particular ones of dissemination entity(s) 106.

[0039] Controller 132 may be configured to oversee the entire technique including the creation of projected data trend(s) (e.g., forecasted data) from the verified data and dissemination of the projected data trend(s). In some examples, controller 132 may also oversee the market surveillance of data source(s) 104, inputs to DF system 102 and scrutiny of the methodology (e.g., provided by DTP algorithm 126). Controller 132 may include, for example, a processor, a microcontroller, a circuit, software and/or other hardware component(s) specially configured to control operation of data source interface(s) 120, data verifier 122, data metric/trend model 124, DTP algorithm 126, data distributer 128, data dissemination interface 130, reference database(s) 134 and website portal 136. In some examples, the market surveillance of data source(s) 104 may be conducted by data verifier 122 (described further below with respect to FIG. 2) on data inputs post publication and may be used by DF system 102 prior the creation of term risk free rates (RFRs) (described further below).

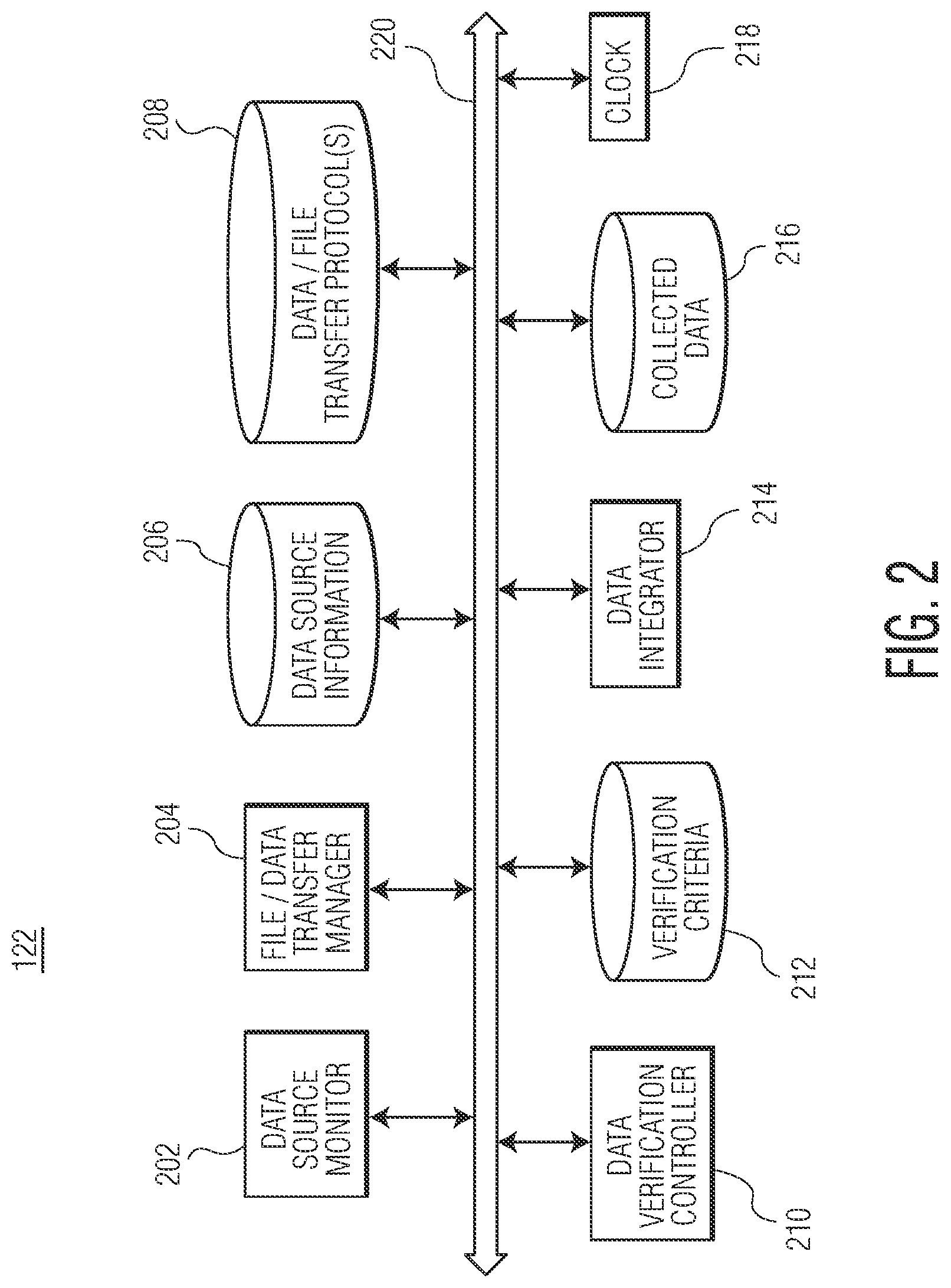

[0040] Referring next to FIG. 2, a functional block diagram of example data verifier 122 of DF system 102 is shown. Data verifier 122 may include data source monitor 202, file/data transfer manager 204, database 206 storing data source information, database 208 storing one or more data and/or file transfer protocols, data verification controller 210, database 212 storing one or more verification criteria, data integrator 214, at least one database 216 storing collected data and clock 218. Components 202-218 may communicate with each other via data and control bus 220.

[0041] Although FIG. 2 illustrates separate databases 206, 208, 212 and 216, it is understood that data verifier 122 may also be configured with more or fewer databases, including one database. In general, databases 206, 208, 212 and 216 are each configured to electronically store one or more data records and/or data files in electronic storage. Each of databases 206, 208, 212 and 216 may be configured according to a suitable architecture, including, without being limited to, a relational database, a non-relational database, a document database, a graph database, an XML, database, an object-oriented database, etc.

[0042] Data source monitor 202 may be configured to communicate with one or more of data source(s) 104 to identify new and eligible data for verification and use by data metric/trend model 124. For example, data source monitor 202 may parse and/or analyze data among data source(s) 104 and compare the analyzed data against one or more predetermined criteria. If the analyzed data meets the predetermined criteria, data source monitor 202 may cause data verifier 122 to obtain the analyzed data from the respective data source 104. For example, data source monitor 202 may cause file/data manager 204 to obtain the analyzed data, such as via a client pull, from a data feed, from a server push, via a file transfer protocol, etc.

[0043] In some examples, data verifier 122 may obtain the data (e.g., via push and/or pull techniques) prior to any comparison against the predetermined criteria, and then data verifier 122 may either accept the obtained data or reject the obtained data. In some examples, the predetermined criteria may include criteria for determining whether to actually obtain the data from among data source(s) 104 (e.g., so that only data satisfying the predetermined criteria is obtained by data verifier 122). In such examples, the obtained data may also be subject to further analysis/verification (e.g., via one or more verification criteria) before the obtained data is accepted or rejected. Accordingly, in examples where data is first obtained and then subject to criteria for acceptance or rejection, the predetermined criteria may include one or more verification criteria (as discussed further below).

[0044] In some examples, data source monitor 202 may monitor one or more data feeds among data source(s) 104. In some examples, data source monitor 202 may monitor data pushed to data verifier 122. In some examples, data source monitor 202 may monitor any data file(s) transferred to data verifier 122. In some examples, data source monitor 202 may cause file/data transfer manager 204 to pull data (e.g., via a client pull) according to one or more predetermined times and/or conditions. In some examples, data source monitor 202 may establish a dedicated communication channel with one or more of data source(s) 104 that may be different from a data feed. For example, the dedicated communication channel may be specific to data verifier 122 and may be associated with a particular portion of data of interest to data verifier 122. In some examples, the dedicated communication channel may be a secure communication channel.

[0045] Data source monitor 202 may monitor data of data source(s) 104 at one or more particular times (e.g., periodically), under one or more particular conditions, in near-real time, in real-time (e.g., continuously), etc. The frequency of monitoring performed by data source monitor 202 may depend upon a particular data source 104. For example, data source 104-1 may only update its data once a day, whereas data source 104-2 may receive rapidly changing updates over a predetermined time period (e.g., eight hours). Data source monitor 202 may, for example, use data source information stored in database 206 in order to determine the frequency of data source monitoring as well to determine the type(s) of communication to use (e.g., a data feed, a server push, etc.) or pro-actively detect (e.g., via a dedicated communication channel, a client pull, etc.).

[0046] Data source monitor 202 may use any suitable predetermined criteria for identifying new/eligible data for verification. Non-limiting examples of the predetermined criteria may include a predetermined change in a data value, a predetermined time, a new data point (e.g., not associated with any previously monitored data), metadata information associated with particular data, etc. In this manner, data source monitor 202 may be configured to obtain the most relevant, most up-to-date and newly eligible data from among data source(s) 202 without solely relying on data source(s) 104 to push data to DF system 102 (e.g., data that may be stale and/or not relevant).

[0047] File/data manager 204 may be configured to manage the handling of data into data verifier 122 in accordance with data source monitor 202. File/data manager 204 may obtain data from among data source(s) 104 in accordance with various data and/or file transfer protocols (e.g., stored in database 208). Database 208 may also store various communication protocols. As discussed above, data source(s) 104 may be configured to communicate with DF system 102 via one or more data transfer protocols (e.g., a server push, a client pull, a data feed, over a dedicated communication channel) and/or file transfer protocols. File/data manager 204 may use data source information (e.g., stored in database 206) to determine an appropriate data transfer, file transfer and/or communication protocol to use in order to obtain data and/or data file(s) from a particular data source (e.g., data source 104-1). File/data manager 204 may also be configured to transfer the obtained data to data verification controller 210. In some examples, file/data manager 204 may transfer the obtained data to database 216, for example, for temporary storage. In some examples, the obtained but not verified data may be stored in database 216 together with an indicator tagging the data as still-to be verified (or any other suitable indication).

[0048] Database 206 may be configured to store any suitable information associated with data source(s) 104 that may be useful for data source monitor 202, file/data transfer manager 204, data verification controller 210 and/or data integrator 214 for obtaining, analyzing and processing of data from among data source(s) 104. Non-limiting data source information that may be stored in database 206, for each particular data source 104 may include data transfer format(s) supported, file transfer format(s) supported, encryption/decryption information, communication channel information, metadata information associated with the data, data format(s) associated with the data, any data normalization information associated with the data (e.g., if the particular data source has unique, non-standard values and/or formats), data monitoring characteristics for the particular data source (e.g., a frequency for monitoring, predetermined criteria for identifying data), etc.

[0049] Database 208 may be configured to store one or more communication protocols, one or more data transfer protocols and one or more file transfer protocols (as discussed in the examples above) for communicating with data source(s) 104 and for transferring data and/or files from among data source(s) 104.

[0050] Data verification controller 210 may be configured to verify the obtained (e.g., incoming) data from file/data transfer manager 204 and/or from temporary storage in database 216. Data verification controller 210 may compare the incoming data to one or more verification criteria (e.g., stored in database 212). In some examples, the verification criteria may depend upon the particular data source (e.g., data source 104-1). In some examples, the verification criteria may be independent of a particular data source.

[0051] The verification criteria may include criteria related to data source verification, data format verification, file format verification, and/or data content verification. Non-limiting examples of data verification criteria may include criteria related to data type, data range, one or more allowed characters, identification of any missing records, cardinality, one or more constraints, cross-system consistency, consistency (e.g., that the data is logical, for example, a delivery date is not before an order date), file existence, data format, one or more logic checks (e.g., an input does not yield a logical error such as being 0 if is to divide with another number), validation of the presence of required data, etc. In some examples, for data trends/metrics relating to forward-looking term interest rates, the verification criteria may include corroborative data source checks, product checks, date checks, holiday calendar checks, maturity checks and/or rate/price error checks. In some examples, clock 218 (e.g., for time and/or data information) may be used along with the verification criteria to verify the incoming data.

[0052] In some examples, one or more of the verification criteria may represent a security protocol, to verify that the incoming data/files are from an appropriate data source. For example, the verification criteria may include a comparison of one or more unique identifiers associated with the received electronic data/files (e.g., a unique data file identifier and/or a unique data source identifier). Such a verification may be advantageous in preventing denial of service attacks and other malicious actions which are intended to harm DF system 102 or dissemination entity(s) 106 (e.g., by way of DF system 102).

[0053] Data verification controller 210 may be configured to verify the incoming data when the incoming data meets the verification criteria. When the incoming data does not meet the verification criteria (e.g., "disqualified data"), data verification controller 210 may discard the obtained data from data source(s) 104. For example, data verification controller 210 may discard the disqualified data from database 216 (or may update the indicator to tag the data as disqualified, for purging of database 216 at a later time). Data verification controller 210 may include, for example, a processor, a microcontroller, a circuit, software and/or other hardware component(s) specially configured to verify the incoming data.

[0054] In some examples, when data verification controller 210 verifies the incoming data, data verification controller 210 may store the verified data in database 216 and may update the indicator to tag the data as verified. In some examples, data verification controller 210 may transfer the verified data to data integrator 214. In some examples, data verification controller 210 may directly transfer the verified data to data metric/trend model 124 and/or to reference database(s) 134.

[0055] Data integrator 214 may be configured to convert the verified data to integrated data suitable for analysis by data metric/trend model 124 and dissemination via dissemination interface 130. Data integrator 214 may be configured to at least one of reformat, aggregate, decompress and/or unpack the data in order to generate integrated data.

[0056] For example, as discussed above, the electronic data/files received by data verifier 122 from among data source(s) 104 may be in a variety of formats (which formats may be known from the associated data source information stored in database 206). Additionally, the data/file formats may have different data transfer parameters, compression schemes, etc. Furthermore, in some examples, data content may correspond to different forms of data, such as different currencies, date formats, time periods, etc. In one example, data verifier 122 may receive separate electronic data/file for each request for information. In another example, data verifier 122 may receive a single data file, corresponding to one or more requests for information, from each of data source(s) 104 which it monitors.

[0057] Data integrator 214 may reformat the verified data having plural data formats by parsing/analyzing the received data to identify its data type, and then converting the received data into data having a predefined data format or type. For example, reformatting may involve converting data having different formats CSV, XML, text into data having a single format (e.g., CSV, a proprietary format, etc.).

[0058] Data integrator 214 may aggregate the verified data by combining data and/or a plurality of electronic data files from one or more of data sources 104 into a single compilation of electronic data (e.g., one electronic data file) based on certain parameters and/or criteria. For example, data may relate to a particular product or instrument, and recent observations including information regarding risk free interest rate data, futures price data, futures trading data, overnight index swap data and/or other suitable data may be combined or aggregated for each particular product or instrument.

[0059] Data integrator 214 may decompress validated data from a compressed format (where the data has been encoded using fewer bits than were used in its original representation), by returning the data to its original representation for use within DF system 102. For example, "zipped" data files (which refer to data files that have been compressed) may be "unzipped" (or decompressed) by integrator 214 into electronic data files having the same bit encoding as they did prior to their being "zipped" (or compressed).

[0060] Data integrator 214 may unpack one or more validated data files, by opening the data file(s), extracting data from the data file(s), and assembling the extracted data in a form and/or format that is suitable for further processing. The sequences for opening and/or assembling the data may be predefined (for example, data may be opened/assembled in a sequence corresponding to timestamps associated with the data).

[0061] In some examples, when data integrator 214 integrates the verified data, data integrator 214 may store the integrated data in database 216 and update the indicator to tag the data as integrated. In some examples, data integrator 214 may directly transfer the integrated data to data metric/trend model 124 and/or to reference database(s) 134.

[0062] Although the example above describes data integrator 214 converting the verified data to integrated data, in some examples, data integrator 214 may perform at least some data integration functions on the incoming data (e.g., reformatting, decompressing, etc.) prior to verification of the incoming data by data verification controller 210.

[0063] Database 216 may be configured to temporarily store incoming data, verified data and/or integrated data (e.g., from data integrator 214). In some examples, controller 132 may be configured to monitor database 216 to monitor a progress of data processing by various components of data verifier 122, based on the status of the indicator associated with the stored data in database 216 (e.g., to-be-verified, verified, integrated, discarded). Controller 132 may thus identify newly integrated data, and may transfer the integrated data to reference database(s) 134 for processing by data metric/trend model 124. In some examples, controller 132 may transfer the data upon identifying its status as integrated. In some examples, controller 132 may transfer the data at one or more times (e.g., periodically, under particular conditions, etc.).

[0064] In operation, data verifier 122 may be configured to monitor data source(s) 104 for new and eligible data (e.g., via data source monitor 202) and to verify incoming data from among data source(s) 104 (e.g., via data verification controller 210). In some examples, the verification may include comparing the incoming data to one or more verification criteria (e.g., stored in database 212). In some examples, the verification criteria may include corroborative data source checks, product checks, date checks, holiday calendar checks, maturity checks and/or rate/price error checks. In some examples, data verifier 122 may proactively pull data from among data source(s) 104 (e.g., via file/data transfer manager 204). In some examples, data from among data source(s) 104 may be pushed to DF system 102 at one or more times (e.g., periodically, under particular conditions, etc.).

[0065] In this manner, DF system 102 (via data verifier 122) may dictate receiving only the type and volume of data and information that is pertinent to supplementing and/or generating data forecasts related to one or more electronic data classes for which directly-related or historical information is sparse or unavailable. In this manner, the processing and memory requirements of DF system 102 are maximized (i.e., by avoiding receiving irrelevant or voluminous data beyond what is needed or desired), particularly in embodiments where it is envisioned that millions of data requests and/or data files are received per day.

[0066] One or more or more of the functions discussed above with respect to FIG. 2 (including, for example, monitoring data, obtaining data, verifying the data and integrating the data) as being carried out by data verifier 122 may be performed in a suitable order or sequence. Further, one or more of these functions may be performed in parallel, on all or on portions of the received data. Still further, one or more of these functions may be performed multiple times. Collectively, one or more of these functions may be performed by data verifier 122 to ultimately generate the integrated data (e.g., data having similar data characteristics (e.g., format, compression, alignment, currency, etc.)). Data verifier 122 may also perform additional and/or alternative functions to form the verified and integrated data.

[0067] Referring back to FIG. 1, it may be appreciated that, because data verifier 122 generates integrated data, data that is disseminated by data dissemination interface 130 provides electronic data to dissemination entity(s) 106 from multiple data sources 104 in an integrated form, without dissemination entity(s) 106 having to perform such integration functions. Additionally, data source(s) 104 may not have to reformat the data it generates prior to transmitting the data to DF system 102, as data verifier 122 is able to receive and process data having any of a plurality of data formats. This, in turn, preserves the system resources and improves efficiencies of the data source(s) 104.

[0068] Data metric/trend model 124 may be configured, in one exemplary embodiment, to process verified data input (e.g., from among the risk free interest rate data. futures price data, futures trading data, overnight index swap price data, overnight index swap trading data and/or any other suitable data input from among data source(s) 104) using various filtration processes and mathematical operations implemented by DTP algorithm 126, to create data metrics and/or project data trends. Data metric/trend model 124 may provide the data metrics/trends to data distributer 128 for dissemination. In some examples, the data metrics/trends may be stored in reference database(s) 134.

[0069] In one non-limiting example, the data metrics and projected data trends may include deriving implied rates and rate change dates and compounding the implied rates over one or more relevant periods. The compounded rates may then be used to determine one or more forward-looking term interest rates. Data metric/trend model 124 may also use other inputs from among data source(s) 104, such as a relevant business day calendar and a calendar, for example, of scheduled central bank meeting dates for one or more relevant currency areas. In some examples, data metric/trend model 214 may include one or more financial models. In some examples, DTP algorithm 126 of data metric/trend model 124 may include a customized variation of a step function methodology, for deriving term settings from futures and risk free rate data. In some examples, the risk free rate data may include at least one currency-specific overnight (ON) rate (e.g., for UK pound sterling, US dollar, Japanese yen, Swiss franc, European Union euro, etc.), and the currency-specific ON rate(s) together with particular futures prices (in some examples, futures settlement prices) may be used to derive forward-looking term interest rate(s). In general, the currency-specific ON rate may include any suitable existing or not yet existing currency-specific ON rate. In some examples the risk free rate data may include spot/next and/or tomorrow/next rates. In general, the risk free rate data may include any suitable risk free rate data which may be useful for deriving forward-looking term rate information.

[0070] In some examples, the data metrics and projected data trends may include combining snapshots of trading data into synthetic order books, which may be filtered and averaged to determine input values with which to derive a forward-looking term rate. In some examples, DTP algorithm 126 of data metric/trend model 124 may include a customized variation of a synthetic order book construction methodology, for deriving term settings from futures and/or overnight index swap data.

[0071] In general, DTP algorithm 126 may be configured to create an enhanced data set (e.g., forecasted data including forward-looking term interest rate(s)) from monitored, filtered, processed and verified data from among one or more data source(s) 104. DTP algorithm 126 may also be configured to push to, store in and retrieve from reference database 134 certain data inputs. An example embodiment of DTP algorithm 126 is described further below.

[0072] Data distributer 128 may be configured to identify any newly determined data metrics/data trends (e.g., via data metric/trend model 124 and/or based on data stored in reference database(s) 134). In some examples, data distributer 128 may perform one or more quality control checks and/or verification operations on the data metrics/data trends prior to dissemination via data dissemination interface 130, to confirm that the information is consistent with one or more predetermined criteria for dissemination. Data distributer 128 may also be configured to submit the data metrics/data trends (upon determining that the data meets the predetermined criteria) to data dissemination interface 130. In some examples, data distributer 128 may perform additional formatting and/or portioning of the metrics/data trends in a manner suitable for dissemination to various dissemination entity(s) 106 and/or website portal 136. For example, dissemination entity 106-1 may be configured to receive a first portion of the data to be disseminated, whereas dissemination entity 106-2 may be configured to receive a second, different portion of the data. As another example, dissemination entity 106-1 may be configured to receive data in one data format whereas dissemination entity 106-2 may be configured to receive data in a different data format.

[0073] Data dissemination interface 130 may be configured to disseminate forecasted data (e.g., data metrics/projected data trends), such as one or more forward-looking term interest rates. In some examples, data dissemination interface 130 may be communicatively coupled to one or more websites (an example of dissemination entity(s) 106), such that interface 130 may be configured to publish the disseminated data (e.g., forward-looking term interest rate(s)) through the website(s) and/or secure file transfer.

[0074] In some examples, data dissemination interface 130 may be further or alternatively be communicatively coupled to one or more redistributors (an example of dissemination entity(s) 106, for example, Bloomberg, Refinitiv, etc.). In some examples, the forward-looking term interest rate(s) may be included and published as part of one or more redistributed risk free rates (e.g., for sterling, US dollar, euro, Swiss franc, Japanese yen currency areas), one or more forward-looking term interest rate settings for these risk free rates, and/or one or more backward-looking realized (simple or compounded) average risk free rate settings for these risk free rates that are included in website portal 136 (e.g., published risk-free rate (RFR) data portal such as shown in FIGS. 9A and 9B) or released together, combining all the relevant information. Additional further risk free rate information and data may be added to the publication.

[0075] In some examples, data dissemination interface 130 may include dedicated website portal 136. Input data from any number of external data sources (e.g., including among data source(s) 104) together with data determined by DF system 102 may be transmitted directly into dedicated website portal 136 over a wired/wireless network, and periodically updated with new information and/or data as it becomes available, including in real-time. In this manner, dedicated website portal 136 may provide a "one-stop-shop" for accessing data (including, in some examples, various risk free rate data), thereby eliminating the need of having to connect to and/or access different data sources, different websites, etc. (and in some examples, conduct separate calculations). Thus, dedicated website portal 136 may interconnect users to various data sources, pipelines and/or data feeds, and provide access to all such sources, together in one location (e.g., dedicated website portal 136), thereby improving accessibility of data to users and permitting access to all relevant data in one location (from dedicated website portal 136). Since such access is provided in a single location, users may avoid having to depart dedicated website portal 136 to access the multiple data source locations (e.g., portals, websites, data source feeds, etc.) from which the data/information originates (and in some examples, perform their own calculations, etc.).

[0076] In some examples, components 120-136 of DF system 102 may be embodied on a single computing device. In other examples, components 120-136 of DF system 102 may be embodied on two or more computing devices distributed over several physical locations, connected by one or more wired and/or wireless links. It should be understood that DF system 102 refers to a computing system having sufficient processing and memory capabilities to perform the specialized functions described herein.

[0077] The solutions described herein utilize the power, speed and precision of a special purpose computer system configured precisely to execute the complex and computer-centric functions described herein. As a result, a mere generic computer will not suffice to carry out the features and functions described herein. Further, it is noted that the systems and methods described herein solve computer-centric problems specifically arising in the realm of computer networks so as to provide an improvement in the functioning of a computer, computer system and/or computer network. For example, a system according to the present disclosure includes an ordered combination of specialized computer components (e.g., data verifier, data metric/trend model, data dissemination interface include a dedicated website portal, etc.) for monitoring multiple data sources, receiving large volumes of data having varying data formats and originating from the various data sources, verifying the data from the various data sources, converting the data to have an integrated format, generating data forecasts and then disseminating the forecasts to dissemination entities. As a result, the data forecasting system detects the most up-to-date information, only processes the volume of information that is accurate (e.g., verified) and also the type of data that may be useful for projecting data trends and generating data metrics, thereby improving the overall accuracy of the data forecasts and the speed of the system to determine and disseminate data forecasts (e.g., when data from data sources rapidly changes).

[0078] Some portions of the present disclosure describe embodiments in terms of algorithms and symbolic representations of operations on information. These algorithmic descriptions and representations are used to convey the substance of this disclosure effectively to others skilled in the art. These operations, while described functionally, computationally, or logically, are to be understood as being implemented by data structures, computer programs or equivalent electrical circuits, microcode, or the like. Furthermore, at times, it may be convenient to refer to these arrangements of operations as modules or algorithms. The described operations and their associated modules may be embodied in specialized software, firmware, specially-configured hardware or any combinations thereof.

[0079] DF system 102 may be configured with more or less modules to conduct the methods described herein with reference to FIGS. 3 and 4. In particular, FIG. 3 is a flow chart diagram illustrating an example method for projecting one more trends in electronic data and generating enhanced data, according to an aspect of the present disclosure; and FIG. 4 is a flow chart diagram illustrating an example method for projecting data trends including forward-looking term interest rate(s), according to another aspect of the present disclosure. As illustrated in FIGS. 3 and 4, the methods shown may be performed by processing logic that may comprise hardware (e.g., circuitry, dedicated logic, programmable logic, microcode, etc.), software (such as instructions run on a processing device), or a combination thereof. In one embodiment, the methods shown in FIGS. 3 and 4 may be performed by one or more specialized processing components associated with components 120-136 of data structure management environment 100 of FIG. 1.

[0080] Referring next to FIG. 3, an example method for projecting data trend(s) in electronic data and generating enhanced data is shown. At step 300, electronic data and/or electronic data files may be obtained by DF system 102 from among data source(s) 104. For example, data source monitor 202 may cause file/data transfer manager 204 to obtain data/file(s) from among data source(s) 104 via data source interface(s) 120. The data may be obtained (according to any suitable communication protocol and data/file transfer protocol), for example, responsive to a server push, a client pull, data in a data feed, data from a separate dedicated communication channel, a file transfer and/or any other suitable technique. In some examples, the obtained data may be temporarily stored, such as in database 216 (e.g., with an indicator tagging the data as being to-be-verified). In some examples, data integrator 214 may perform some preliminary integration operation on the obtained data.

[0081] At step 302, data verification controller 210 may compare the obtained data to one or more verification criteria (e.g., stored in database 212). This compare function may be used to verify that only data satisfying the certain of the verification criteria is obtained, and/or verify that the obtained data is filtered by reference to the verification criteria and then either kept, discarded, or a combination thereof. At step 304, data verification controller 210 may determine whether the predetermined criteria (e.g., criteria related to data source verification, data format verification, file format verification, and/or data content verification) is met.

[0082] When, at step 304, it is determined that the obtained data fails to meet one or more of the verification criteria, step 304 proceeds to step 306 and data verification controller 210 may discard the data. In some examples, any temporarily stored data in database 216 that is determined to be un-verified may be removed. In some examples, an indicator of any temporarily stored data in database 216 that is determined to be un-verified may be updated to an un-verified status and the associated data may be removed from database 216 at a later time.

[0083] When, at step 304, it is determined that the obtained data meets the verification criteria, step 304 proceeds to step 308 and data integrator 216 may convert the verified data to integrated data. In some examples, the verified data may be stored in database 216 (e.g., with the indicator updated to tag the data as verified), after the data is verified and prior to being converted to integrated data. As discussed above, data integrator 214 may be configured to at least one of reformat, aggregate, decompress and/or unpack the data in order to generate integrated data.