Measuring Conversion Of An Online Advertising Campaign From An Offline Merchant

WINNER; Jeffrey ; et al.

U.S. patent application number 16/924795 was filed with the patent office on 2020-10-29 for measuring conversion of an online advertising campaign from an offline merchant. This patent application is currently assigned to Twitter,Inc.. The applicant listed for this patent is Geraud Boyer, Amit Kumar, Eckart Walther, Jeffrey WINNER. Invention is credited to Geraud Boyer, Amit Kumar, Eckart Walther, Jeffrey WINNER.

| Application Number | 20200342493 16/924795 |

| Document ID | / |

| Family ID | 1000004943077 |

| Filed Date | 2020-10-29 |

| United States Patent Application | 20200342493 |

| Kind Code | A1 |

| WINNER; Jeffrey ; et al. | October 29, 2020 |

MEASURING CONVERSION OF AN ONLINE ADVERTISING CAMPAIGN FROM AN OFFLINE MERCHANT

Abstract

A technique for tracking conversion of an online offer includes tracking online and/or offline transactions. A customer accepts an offer provided by a merchant and submits his or her account information so that he or she may receive a reward for satisfying criteria associated with the offer. Transactions of the merchant are then monitored at the payment processor level to determine whether the customer satisfies the purchase criteria. Therefore, online and offline conversion can both be tracked. Further, the merchant is able to determine the overall effectiveness of advertising campaigns by analyzing the number of offers that are both accepted and satisfied.

| Inventors: | WINNER; Jeffrey; (San Francisco, CA) ; Boyer; Geraud; (San Francisco, CA) ; Kumar; Amit; (Palo Alto, CA) ; Walther; Eckart; (Palo Alto, CA) | ||||||||||

| Applicant: |

|

||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Assignee: | Twitter,Inc. San Francisco CA |

||||||||||

| Family ID: | 1000004943077 | ||||||||||

| Appl. No.: | 16/924795 | ||||||||||

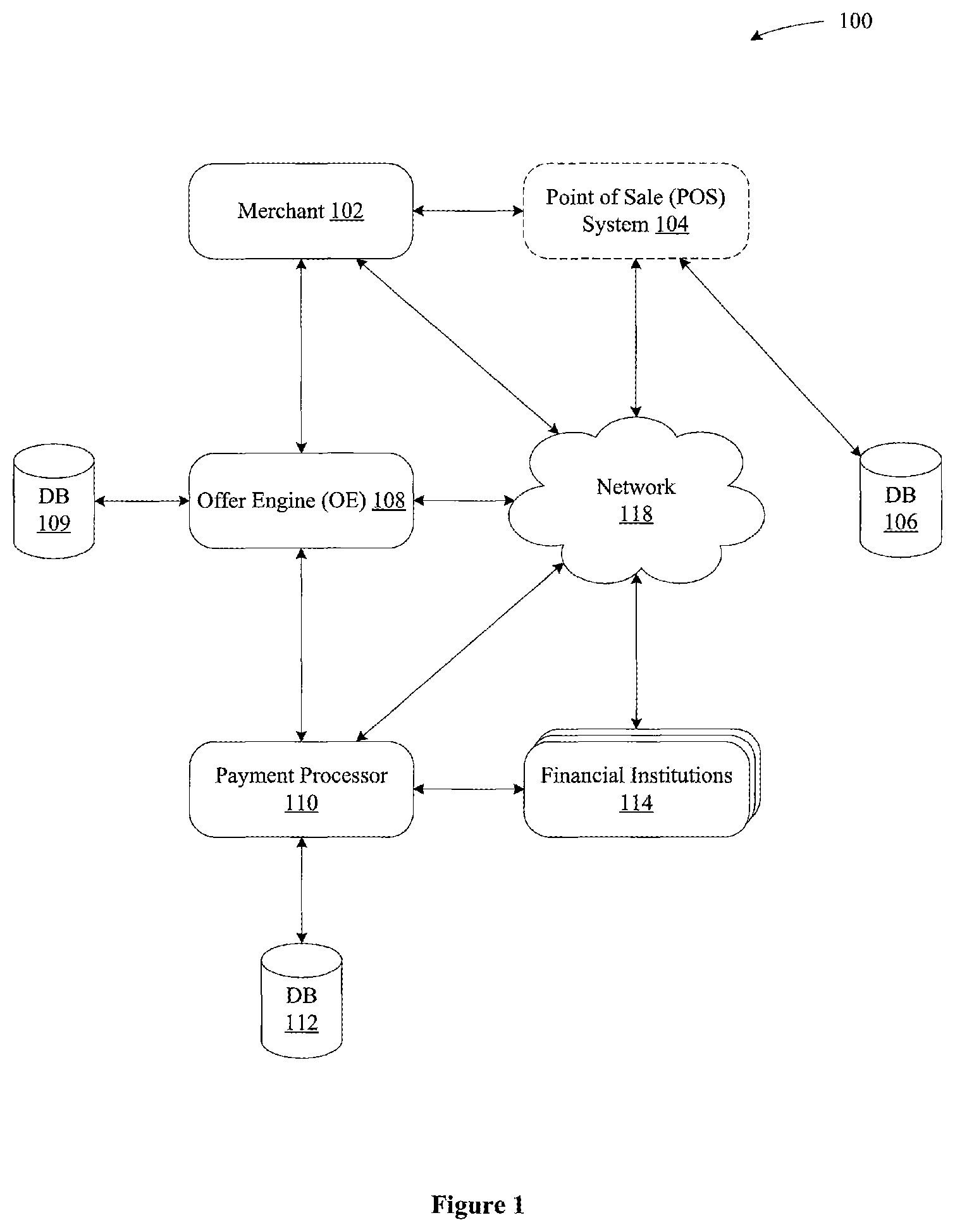

| Filed: | July 9, 2020 |

Related U.S. Patent Documents

| Application Number | Filing Date | Patent Number | ||

|---|---|---|---|---|

| 13211253 | Aug 16, 2011 | |||

| 16924795 | ||||

| 61442943 | Feb 15, 2011 | |||

| 61442691 | Feb 14, 2011 | |||

| Current U.S. Class: | 1/1 |

| Current CPC Class: | G06Q 30/0246 20130101; G06Q 30/02 20130101; G06Q 30/0273 20130101 |

| International Class: | G06Q 30/02 20060101 G06Q030/02 |

Claims

1. In a system (100) comprising a point of sale (POS) system (104) associated with a merchant (102), and a payment processor (110) communicatively coupled to the POS system via a network (118): an offer engine (108) to measure conversion of an online advertising campaign for the merchant by determining transactions completed, using the PUS system, between respective customers and the merchant in response to the respective customers receiving and accepting an online offer from the merchant via an online advertisement (202, 204) rendered on customer devices coupled to the network and used by the respective customers to view the online offer, wherein the online offer specifies at least one criterion for the respective customers to satisfy the online offer and complete the transactions with the merchant, the offer engine comprising: a processor; and a memory storing computer-readable instructions that when executed by the processor cause the offer engine to: A) provide, via the network, a merchant registration interface; B) receive, via the network and in response to A), merchant account registration information including a merchant identification (ID) issued to the merchant by one of a merchant bank and the payment processor, wherein the merchant ID uniquely identifies transactions initiated at the merchant via the POS system; C) generate a merchant account based on the merchant account registration information received in B); D) receive, via the network, from the merchant having the merchant account generated in C), a request to create the online offer and offer information associated with the online offer, wherein the offer information includes the at least one criterion for the respective customers to satisfy the online offer; E) determine that a first customer of the respective customers viewing the online advertisement including the online offer via a first customer device clicked on the online advertisement including the online offer; F) provide, via the network and in response to E), an interface (200) for display on the first customer device of the first customer to register a first customer account to accept the online offer; G) receive, via the network and in response to F), a first payment account number of a first payment account for the first customer, wherein the first payment account includes at least one of a customer credit card, a customer debit card, and a customer prepaid card; H) transmit, via the network to the payment processor, the merchant ID received in B) and not the offer information received in D), such that the payment processor has no offer information associated with the online offer; I) receive, via the network from the payment processor, in response to H), at least one transaction initiated using the POS system associated with the merchant; and J) determine, based on the at least one transaction received in I) and the offer information received in D), whether the first customer has completed a first transaction corresponding to the online offer.

2. The offer engine of claim 1, wherein D); the at least criterion for the respective customers to satisfy the online offer includes at least one of: buying a first amount of a product; spending a second amount of money; completing the transaction at a particular time; or making a number of purchases within a particular amount of time.

3. The offer engine of claim 1, wherein after D), and when executed by the processor, the computer-readable instructions further cause the offer engine to: cause the online offer to be published, via the network, as at least one of a contextual advertisement on a search engine results page, a banner advertisement, a rich media advertisement, a social network advertisement, and interstitial advertisement, an online classified advertisement, a short-message-service (SMS) message, or an email.

4. The offer engine of claim 1, wherein in E), the offer engine determines, via at least one of a browser cookie and Internet Protocol (IP) address tracking, that the first customer clicked on the online advertisement including the online offer.

5. The offer engine of claim 1, wherein in F), the interface provided by the offer engine comprises: at least one first interface widget to allow the first customer to register the first customer account; at least one second interface widget to allow the first customer to accept the online offer; and at least one third interface widget to allow the first customer to be electronically notified when the online offer is satisfied.

6. The offer engine of claim 5, wherein the at least one first interface widget comprises: a first field to enter the first payment account number of the first payment account of the first customer; a second field to enter an expiration date of the first payment account; and a third field to enter a security code for the first payment account.

7. The offer engine of claim I, wherein in response to G), the offer engine: G1) generates and stores the first customer account in the memory; G2) generates and stores in the first customer account at least one data object based on the first payment account number received in G); and G3) associates the online offer with the first customer account.

8. The offer engine of claim 7, wherein in G2), the offer engine applies a hash function to the first payment account number to generate a corresponding hash value as the at least one data object.

9. The offer engine of claim 1, wherein in I), each transaction of the at least one transaction received by the offer engine from the payment processor includes a unique transaction ID, the merchant ID, a transaction payment account number, a total amount charged, and a timestamp.

10. The offer engine of claim 1, wherein in J), the offer engine: J1) determines if the at least one criterion specified by the online offer is satisfied in the at least one transaction received from the payment processor; and J2) for each transaction of the at least one transaction in which the at least one criterion specified by the online offer is satisfied, determines if one transaction of the at least one transaction is the first transaction completed by the first customer, based at least in part on the first payment account number of the first payment account for the first customer received in G).

11. The offer engine of claim 10, wherein J1), the at least criterion includes at least one of: buying a first amount of a product; spending a second amount of money; completing the transaction at a particular time; or making a number of purchases within a particular amount of time.

12. The offer engine of claim 11, wherein in I), each transaction of the at least one transaction received by the offer engine from the payment processor includes a unique transaction ID, the merchant ID, a hashed transaction payment account number, a total amount charged, and a timestamp.

13. The offer engine of claim 12, wherein in J2), the offer engine: extracts the hashed transaction payment account number included in the one transaction; compares the extracted hashed transaction payment account number against a first hashed account number corresponding to the first payment account number of the first payment account for the first customer received in G); and determines that the first customer has completed the first transaction corresponding to the online offer if the extracted hashed transaction payment account number matches the first hashed account number corresponding to the first payment account number of the first payment account for the first customer.

14. The offer engine of claim 10, wherein: in I), each transaction of the at least one transaction received by the offer engine from the payment processor includes a unique transaction ID; and in J1), the offer engine: J1a) obtains from the PUS system, via the network, POS transaction data for the at least one transaction; and J1b) determines if the at least one criterion specified by the online offer is satisfied in the at least one transaction received from the payment processor, based on at least some of the PUS transaction data obtained from the PUS system and the unique transaction ID for the at least one transaction.

15. The offer engine of claim 14, wherein for each transaction of the at least one transaction: the POS system sends a request, via the network, to the payment processor to process the transaction; the payment processor returns to the POS system, via the network, the unique transaction ID of the transaction; the POS system creates and stores a POS transaction object for the transaction, the PUS transaction object comprising the unique transaction ID of the transaction and at least one of: a unique PUS transaction ID; at least one universal product code (UPC) for at least one item purchased in the transaction; a description for the at least one item purchased in the transaction; a subtotal amount for the transaction; a tax amount for the transaction; or a total amount for the transaction; and in J1a), the POS transaction data obtained by the offer engine is based on the POS transaction data object.

16. In a system (100) comprising a point of sale (POS) system (104) associated with a merchant (102), and a payment processor (110) communicatively coupled to the POS system via a network (118): an offer engine (108) to measure conversion of an online advertising campaign for the merchant by determining transactions completed, using the POS system, between respective customers and the merchant in response to the respective customers receiving and accepting an online offer from the merchant via an online advertisement (202, 204) rendered on customer devices coupled to the network and used by the respective customers to view the online offer, wherein the online offer specifies at least one criterion for the respective customers to satisfy the online offer and complete the transactions with the merchant, the offer engine comprising: a processor; and a memory storing computer-readable instructions that when executed by the processor cause the offer engine to: A) determine that a first customer of the respective customers viewing the online advertisement including the online offer via a first customer device clicked on the online advertisement including the online offer; B) provide. via the network and in response to A). an interface (200) for display on the first customer device of the first customer to register a first customer account to accept the online offer; C) receive, via the network and in response to B), a first payment account number of a first payment account for the first customer, wherein the first payment account includes at least one of a customer credit card, a customer debit card, and a customer prepaid card; D) transmit, via the network to the payment processor, a merchant identification (ID) for the merchant and no offer information regarding the online offer, such that the payment processor has no offer information associated with the online offer; E) receive, via the network from the payment processor, in response to D), at least one transaction initiated using the POS system associated with the merchant; and F) determine, based on the at least one transaction received in E) whether the first customer has completed a first transaction corresponding to the online offer.

17. The offer engine of claim 16, wherein in B), the offer engine determines, via at least one of a browser cookie and Internet Protocol (IP) address tracking, that the first customer clicked on the online advertisement including the online offer.

18. The offer engine of claim 16, wherein in B), the interface provided by the offer engine comprises: at least one first interface widget to allow the first customer to register the first customer account; at least one second interface widget to allow the first customer to accept the online offer; and at least one third interface widget to allow the first customer to be electronically notified when the online offer is satisfied.

19. The offer engine of claim 18, wherein the at least one first interface widget comprises: a first field to enter the first payment account number of the first payment account of the first customer; a second field to enter an expiration date of the first payment account; and a third field to enter a security code for the first payment account.

20. The offer engine of claim 16, wherein in response to C), the offer engine: C1) generates and stores the first customer account in the memory; C2) generates and stores in the first customer account at least one data object based on the first payment account number received in C); and C3) associates the online offer with the first customer account.

21. The offer engine of claim 20, wherein in C2), the offer engine applies a hash function to the first payment account number to generate a corresponding hash value as the at least one data object.

22. The offer engine of claim 16, wherein in E), each transaction of the at least one transaction received by the offer engine from the payment processor includes a unique transaction ID, the merchant ID, a transaction payment account number, a total amount charged, and a timestamp.

23. The offer engine of claim 22, wherein: the memory of the offer engine further stores offer information associated with the online offer, wherein the offer information includes the at least one criterion for the respective customers to satisfy the online offer; and in F), the offer engine: F1) determines, based on the offer information stored in the memory, if the at least one criterion specified by the online offer is satisfied in the at least one transaction received from the payment processor; and F2) for each transaction of the at least one transaction in which the at least one criterion specified by the online offer is satisfied, determines if one transaction of the at least one transaction is the first transaction completed by the first customer, based at least in part on the first payment account number of the first payment account for the first customer received in C).

24. The offer engine of claim 23, wherein in F1), the at least criterion includes at least one of: buying a first amount of a product; spending a second amount of money: completing the transaction at a particular time; or making a number of purchases within a particular amount of time.

25. The offer engine of claim 24, wherein in E), each transaction of the at least one transaction received by the offer engine from the payment processor includes a unique transaction ID, the merchant ID, a hashed transaction payment account number, a total amount charged, and a timestamp.

26. The offer engine of claim 25, wherein in F2), the offer engine: extracts the hashed transaction payment account number included in the one transaction; compares the extracted hashed transaction payment account number against a first hashed account number corresponding to the first payment account number of the first payment account for the first customer received in C); and determines that the first customer has completed the first transaction corresponding to the online offer if the extracted hashed transaction payment account number matches the first hashed account number corresponding to the first payment account number of the first payment account for the first customer.

27. The offer engine of claim 26, wherein: in E), each transaction of the at least one transaction received by the offer engine from the payment processor includes a unique transaction ID; and in F1), the offer engine: F1a) obtains from the POS system, via the network, POS transaction data for the at least one transaction; and F1b) determines if the at least one criterion specified by the online offer is satisfied in the at least one transaction received from the payment processor, based on at least some of the POS transaction data obtained from the POS system and the unique transaction ID for the at least one transaction.

28. The offer engine of claim 27, wherein for each transaction of the at least one transaction: the POS system sends a request, via the network, to the payment processor to process the transaction; the payment processor returns to the PUS system, via the network, the unique transaction ID of the transaction; the PUS system creates and stores a PUS transaction object for the transaction, the POS transaction object comprising the unique transaction ID of the transaction and at least one of: a unique POS transaction ID; at least one universal product code (UPC) for at least one item purchased in the transaction; a description for the at least one item purchased in the transaction; a subtotal amount for the transaction; a tax amount for the transaction; or a total amount for the transaction; and in F1a). the POS transaction data obtained by the offer engine is based on the POS transaction data object.

29. The offer engine of claim 26, wherein prior to A), and when executed by the processor, the computer-readable instructions further cause the offer engine to: A-4) provide, via the network, a merchant registration interface; A-3) receive, via the network and in response to A-4), merchant account registration information including the merchant ID, wherein the merchant ID is issued to the merchant by one of a merchant bank and the payment processor, and wherein the merchant ID uniquely identifies transactions initiated at the merchant via the PUS system; A-2) generate a merchant account based on the merchant account registration information received in A-3); and A-1) receive, via the network, from the merchant having the merchant account, generated in A-2), a request to create the online offer and the offer information associated with the online offer.

30. A method for measuring conversion of an online advertising campaign for a merchant by determining transactions completed between respective customers and the merchant in response to the respective customers receiving and accepting an online offer from the merchant via an online advertisement rendered on customer devices coupled to a network and used by the respective customers to view the online offer, wherein the online offer specifies at least one criterion for the respective customers to satisfy the online offer and complete the transactions with the merchant, the method comprising: A) determining that a first customer of the respective customers viewing the online advertisement including the online offer via a first customer device clicked on the online advertisement including the online offer; B) providing, via the network and in response to A), an interface for display on the first customer device of the first customer to register a first customer account to accept the online offer; C) receiving, via the network and in response to B), a first payment account number of a first payment account for the first customer, wherein the first payment account includes at least one of a customer credit card, a customer debit card, and a customer prepaid card; D) transmitting, via the network to a payment processor communicatively coupled to a point of sale (POS) system associated with the merchant, a merchant identification (ID) for the merchant and no offer information regarding the online offer, such that the payment processor has no offer information associated with the online offer; E) receiving, via the network from the payment processor, in response to D), at least one transaction initiated using the POS system associated with the merchant; and F) determining, based on the at least one transaction received in E) whether the first customer has completed a first transaction corresponding to the online offer.

31. The method of claim 30, wherein B) comprises determining, via at least one of a browser cookie and Internet Protocol (IP) address tracking, that the first customer clicked on the online advertisement including the online offer.

2. The method of claim 30, wherein in B), the interface comprises: at least one first interface widget to allow the first customer to register the first customer account; at least one second interface widget to allow the first customer to accept the online offer; and at least one third interface widget to allow the first customer to be electronically notified when the online offer is satisfied.

33. The method of claim 32, wherein the at least one first interface widget comprises: a first field to enter the first payment account number of the first payment account of the first customer; a second field to enter an expiration date of the first payment account; and a third field to enter a security code for the first payment account.

34. The method of claim 30, wherein C) further comprises: C1) generating and storing the first customer account; C2) generating and storing in the first customer account at least one data object based on the first payment account number received in C); and C3) associating the online offer with the first customer account.

35. The method of claim 34, wherein C2) comprises applying a hash function to the first payment account number to generate a corresponding hash value as the at least one data object.

36. The method of claim 30, wherein in E), each transaction of the at least one transaction received from the payment processor includes a unique transaction ID, the merchant ID, a transaction payment account number, a total amount charged, and a timestamp.

37. The method of claim 36, further comprising storing offer information associated with the online offer, wherein the offer information includes the at least one criterion for the respective customers to satisfy the online offer, wherein F) comprises: F1) determining, based on the offer information, if the at least one criterion specified by the online offer is satisfied in the at least one transaction received from the payment processor; and F2) for each transaction of the at least one transaction in which the at least one criterion specified by the online offer is satisfied, determining if one transaction of the at least one transaction is the first transaction completed by the first customer, based at least in part on the first payment account number of the first payment account for the first customer received in C).

38. The method of claim 37, wherein in F1), the at least criterion includes at least one of: buying a first amount of a product; spending a second amount of money; completing the transaction at a particular time; or making a number of purchases within a particular amount of time.

39. The method of claim 38, wherein in E), each transaction of the at least one transaction received by the offer engine from the payment processor includes a unique transaction ID, the merchant ID, a hashed transaction payment account number, a total amount charged, and a timestamp.

40. The method of claim 39, wherein F2) comprises: extracting the hashed transaction payment account number included in the one transaction; comparing the extracted hashed transaction payment account number against a first hashed account number corresponding to the first :payment account number of the first payment account for the first customer received in C); and determining that the first customer has completed the first transaction corresponding to the online offer if the extracted hashed transaction payment account number matches the first hashed account number corresponding to the first payment account number of the first payment account for the first customer.

41. The method of claim 40, wherein: in E), each transaction of the at least one transaction received from the payment processor includes a unique transaction ID; and F1) comprises: F1a) obtaining from the POS system, via the network, POS transaction data for the at least one transaction; and F1b) determining if the at least one criterion specified by the online offer is satisfied in the at least one transaction received from the payment processor, based on at least some of the POS transaction data obtained from the POS system and the unique transaction ID for the at least one transaction.

42. The method of claim 41, wherein for each transaction of the at least one transaction: the POS system sends a request, via the network, to the payment processor to process the transaction; the payment processor returns to the POS system, via the network, the unique transaction ID of the transaction; the POS system creates and stores a POS transaction object for the transaction, the POS transaction object comprising the unique transaction ID of the transaction and at least one of: a unique POS transaction ID; at least one universal product code (UPC) for at least one item purchased in the transaction; a description for the at least one item purchased in the transaction; a subtotal amount for the transaction; a tax amount for the transaction; or a total amount for the transaction; and in F1a), the POS transaction data is based on the POS transaction data object.

43. The method of claim 41, wherein prior to A), the method further comprises: A-4) providing, via the network, a merchant registration interface; A-3) receiving, via the network and in response to A-4), merchant account registration information including the merchant ID, wherein the merchant ID is issued to the merchant by one of a merchant bank and the payment processor, and wherein the merchant ID uniquely identifies transactions initiated at the merchant via the POS system A-2) generating a merchant account based on the merchant account registration information received in A-3); and A-1) receiving, via the network, from the merchant having the merchant account generated in A-2), a request to create the online offer and the offer information associated with the online offer.

Description

CROSS-REFERENCE TO RELATED APPLICATIONS

[0001] This application claims priority benefit to United States provisional patent application titled, "SYSTEM AND METHOD IMPLEMENTING REFERRAL PROGRAMS," filed on Feb. 15, 2011, having application Ser. No. 61/442,943 (Attorney Docket Number CARD/0002USL) and also claims priority benefit to United States provisional patent application titled, "SYSTEM AND METHOD FOR IMPLEMENTING PAYMENT NETWORK COOKIES," filed on Feb. 14, 2011, having application Ser. No. 61/442,691 (Attorney Docket Number CARD/0003USL), both of which are incorporated by reference herein.

BACKGROUND

Field of the Invention

[0002] The present invention relates to the field of computer software and, in particular, to a system and method for monitoring for transactions.

Description of the Related Art

[0003] Online advertising is a form of promotion that uses the internet to deliver marketing messages to potential customers. Examples of online advertising include contextual advertisements on search engine results pages, banner advertisements, rich media (e.g., video) advertisements, social network advertisements, interstitial advertisements, online classified advertisements, e-mail marketing, and many others.

[0004] One important aspect of an online advertisement is the online "conversion" of the online advertisement, which refers generally to a customer completing an online transaction with an online merchant in response to viewing the online advertisement. Typically, when a customer views an online advertisement, the customer's activity across one or more web pages is tracked to determine whether a particular online transaction is actually completed by the customer. One example of a tracking technique is referred to as pixel-based tracking, where a 1.times.1 pixel image--often referred to as a "web beacon"--is linked to an online advertisement and included in each web page of, for example, an online shopping cart. The 1.times.1 pixel image reports information back to a manager of the online advertisement such that the manager is able to determine whether the customer has reached an order confirmation page, indicating that the online advertisement was successful by resulting in a conversion.

[0005] Although many merchants provide their customers the ability to shop online, there exists a large number of merchants that have one or more brick-and-mortar locations, referred to herein as "offline" merchants. Though offline merchants typically do not provide an online shopping cart to their customers, the offline merchants may nonetheless be interested in online advertising that causes customers to visit their brick-and-mortar locations in an attempt to increase sales. Unfortunately, as with offline advertising (e.g., advertising in magazines, TV, radio, etc.), it is difficult for offline merchants to measure the performance of their online advertising campaigns.

[0006] One attempt to measure performance of an advertising campaign involves polling customers and asking them to share the motivation for the purchase they are making. For example, if a customer shops at a merchant location during a sale, then the merchant may ask the customer, "Where did you hear about our sale?" Unfortunately, some customers are lazy and do not wish to share such information with the merchant or may provide inaccurate information. Determining the effectiveness of an online portion of ad campaign is further complicated when the same advertisements are presented to potential customers through other channels that are not online.

[0007] As the foregoing illustrates, there is a need in the art for an improved technique that overcomes the deficiencies of prior approaches.

SUMMARY

[0008] One embodiment of the invention provides a method for tracking conversion of an online offer. The method includes identifying an online offer accepted by a customer; receiving a set of transactions executed at a merchant; parsing the set of transactions to determine that a set of criteria associated with the online offer has been satisfied by the customer via one or more transactions at the merchant; and notifying the merchant that the online offer has been satisfied by the customer.

[0009] Another embodiment of the invention provides a method for identifying an identification code corresponding to a merchant. The method includes providing the merchant access to an account; instructing the merchant to execute a transaction using the account; parsing one or more transactions made using the account to identify the transaction; and extracting from the transaction the identification code of the merchant.

[0010] Further embodiments of the present invention provide a computer-readable storage medium that includes instructions for causing a computer system to carry out one or more of the methods set forth above.

BRIEF DESCRIPTION OF THE DRAWINGS

[0011] So that the manner in which the above recited features of the invention can be understood in detail, a more particular description of the invention, briefly summarized above, may be had by reference to embodiments, some of which are illustrated in the appended drawings. It is to be noted, however, that the appended drawings illustrate only typical embodiments of this invention and are therefore not to be considered limiting of its scope, for the invention may admit to other equally effective embodiments.

[0012] FIG. 1 is a block diagram illustrating components of a system in which embodiments of the invention may be implemented.

[0013] FIG. 2 is a screenshot of an interface configured to gather customer data from a customer that accepts an offer, according to one embodiment of the invention.

[0014] FIG. 3 is a flow diagram of method steps for generating a merchant account, according to one embodiment of the invention.

[0015] FIG. 4 is a flow diagram of method steps for associating a customer with an offer, according to one embodiment of the invention.

[0016] FIG. 5 is a flow diagram of method steps for determining whether a set of offers has been satisfied, according to one embodiment of the invention.

[0017] FIG. 6 is a flow diagram of method steps for processing a group offer, according to one embodiment of the invention.

[0018] FIG. 7 is a flow diagram of method steps for processing a referral offer, according to one embodiment of the invention.

[0019] FIG. 8 is a flow diagram of method steps for processing an offer involving specific criteria, according to one embodiment of the invention.

[0020] FIG. 9 is a flow diagram of method steps for extracting an identification (ID) of a merchant, according to one embodiment of the invention.

DETAILED DESCRIPTION

[0021] In the following description, several specific details are presented to provide a thorough understanding of embodiments of the invention. One skilled in the relevant art will recognize, however, that the concepts and techniques disclosed herein can be practiced without one or more of the specific details, or in combination with other components, etc. In other instances, well-known implementations or operations are not shown or described in detail to avoid obscuring aspects of various examples disclosed herein.

[0022] FIG. 1 is a block diagram illustrating components of a system 100 in which embodiments of the invention may be implemented. As shown, system 100 includes a merchant 102, a point of sale (POS) system 104 with an associated database 106, an offer engine (OE) 108 with an associated database 109, a payment processor 110 with an associated database 112, one or more financial institutions 114, and a network 118. As shown, merchant 102, OE 108, payment processor 110 and financial institutions 114 communicate with one another via network 108, such as the internet.

[0023] Though not illustrated in FIG. 1, each of OE 108, payment processor 110 and POS system 104 include conventional components of a computing device, e.g., a processor, system memory, a hard disk drive, input devices such as a mouse and a keyboard, and output devices such as a monitor.

[0024] In one embodiment, DB 106, DB 109 and/or DB 112 can be any type of storage system, e.g., a relational database hosted on a network file system (NFS) device, a storage system hosted by a cloud service provider, and the like. Alternatively, DB 106, DB 109 and/or DB 112 may be integrated in POS system 104, OE 108 and payment processor 110, respectively, such as a database hosted on a local disk and managed by an operating system.

[0025] Merchant 102 may be a brick-and-mortal physical merchant, an online merchant, a mail-order/telephone-order (MOTO) merchant, and the like. Merchant 102 is capable of processing accounts of customers when they pay for goods or services offered by merchant 102. Such accounts include credit cards, debit cards, prepaid cards, and the like. In some embodiments, merchant 102 is equipped with POS system 104. As shown, POS system 104 is coupled to database 106, which enables POS system 104 to store detailed information associated with transactions between merchant 102 and customers of merchant 102.

[0026] A transaction may be initiated at merchant 102 according to a variety of techniques. For example, a cashier at merchant 102 may swipe a credit card through a card reader included in POS system 104. Alternatively, an account may be delivered virtually on a customer's mobile device, which enables a customer at merchant 102 to wave his/her mobile device in front of a contactless card reader included in POS system 104. Further, the customer may show his/her mobile device to a cashier at merchant 102 who manually enters an account number of the account being used by the customer. Alternatively, the mobile device may include a contactless chip or tag that is wireless-readable by POS system 104 using, e.g., near-field-communication (NFC) technology.

[0027] Payment processor 110, in conjunction with financial institutions 114, facilitates payment transactions between merchant 102 and customers thereof, and stores the transactions in DB 112. More specifically, when a customer attempts to pay for goods and/or services offered by merchant 102 using his or her account, a POS terminal submits the transaction through a merchant account to an acquiring bank of the merchant (i.e., one of the financial institutions 114). The acquiring bank then transmits a request for funds through the payment processor 110. The payment processor 110 routes the request for funds to the card holder's issuing bank (i.e., the appropriate financial institution 114) for authorization based on a type of the account. The issuing bank verifies the card number, the transaction type, and the amount. In some examples, the issuing bank then reserves that amount of the cardholder's credit limit for the merchant.

[0028] For example, if payment processor 110 detects that the account is a debit card associated with a checking account of the customer, then payment processor 110 routes the transaction request to the bank that issued the debit card, whereupon the issuing bank indicates to payment processor 110 whether the checking account possesses sufficient funds to satisfy the transaction request. In turn, payment processor 110 indicates to the merchant acquiring bank whether the request is for funds has been approved. If the transaction is successfully processed, then funds are transferred from the card holder's account at the issuing bank to the merchant account at the inquiring bank.

[0029] An Offer Engine (POE) 108 is configured to determine the effectiveness of advertising campaigns requested and managed by merchant 102. As shown in FIG. 1, OE 108 is in communication with both merchant 102 and payment processor 110. OE 108 manages "offers" that are advertised to, possibly accepted by, and possibly satisfied by customers of merchant 102. The offer can be coupled to a reward that is given to the customer when he or she has satisfied the offer, e.g., cash-back rewards, credit card rewards, store credit, virtual currency, and the like.

[0030] An offer may be any offer that involves a customer completing a transaction according to specific criteria, such as buying a certain amount of a product, spending a certain amount in one purchase, making a purchase at a particular time, making a number of purchases within a particular amount of time, and the like. Offers may also involve a group of customers completing a transaction according to specific criteria. As is described in greater detail herein, OE 108 is configured to monitor for transactions to determine whether the criteria for a particular offer have been satisfied. As is also described herein, OE 108 can monitor both online and offline transactions to determine whether the criteria for a particular offer have been satisfied.

[0031] Offer data is stored in database 109 accessed by OE 108. The offer data is advertised to customers via webpage advertisements, email marketing campaigns, short-message-service (SMS) messages, telemarketing campaigns, and the like, as described herein. As described below in conjunction with FIG. 2, OE 108 provides an interface that enables customers (e.g., individuals) to register an account with OE 108, including their account information, and subsequently accept and complete offers. OE 108 subsequently monitors transactions initiated at merchant 102 (i.e., online and/or offline) to determine whether offers are satisfied by the customers whom accepted them.

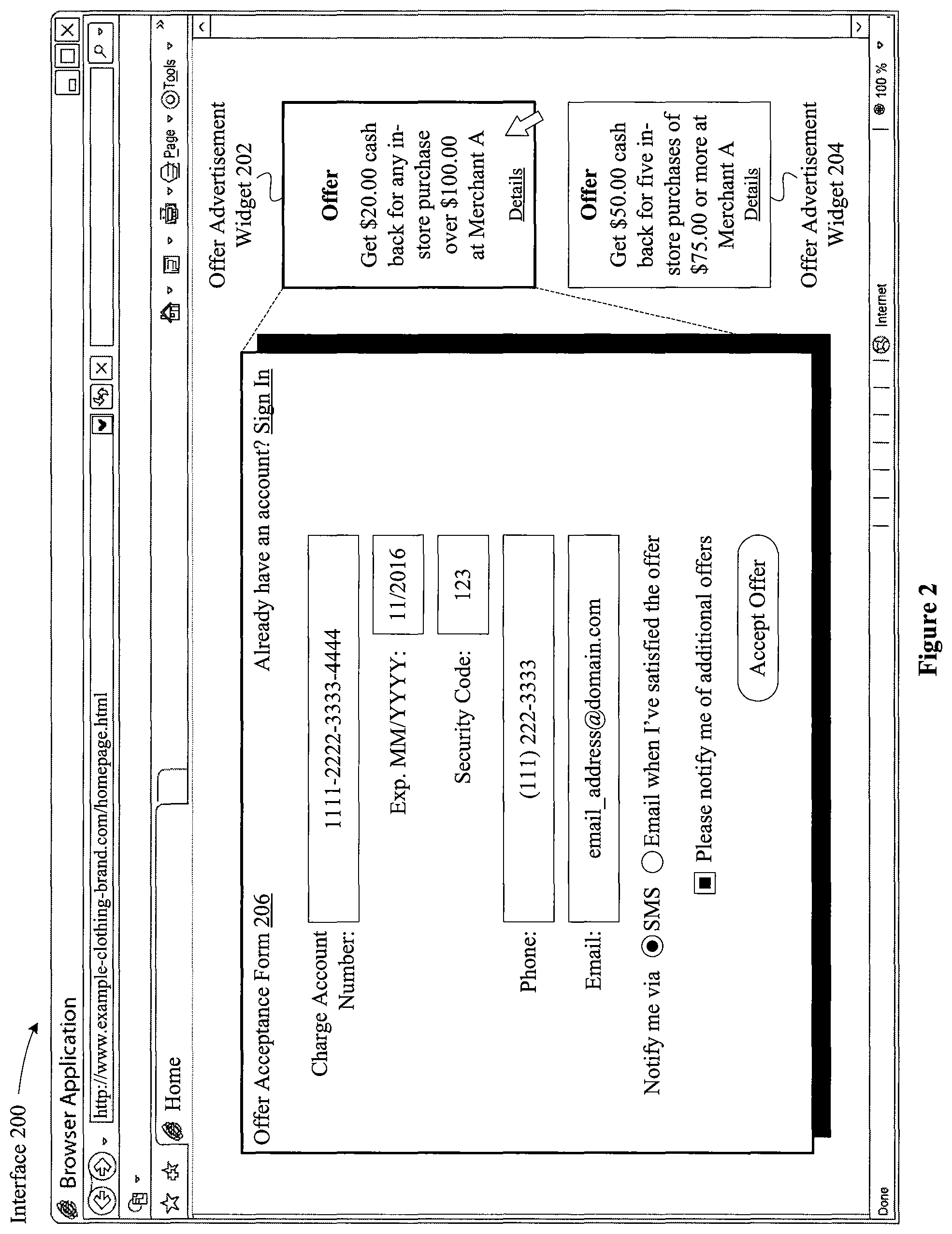

[0032] FIG. 2 is a screenshot of an interface 200 configured to gather customer data from a customer that accepts an offer, according to one embodiment of the invention. As shown, interface 200 is accessible via a web browser application and includes offer advertisement widget 202, offer advertisement widget 204, and offer acceptance form 206. Offer advertisement widgets 202, 204, when selected by a customer (e.g., by clicking on them) enable a customer to accept offers provided by merchant 102 (e.g., "Merchant A"). For example, the customer may accept the offer advertised in offer advertisement widget 202 to receive a $20.00 cash back reward for any in-store purchase over $100.00 at Merchant A. Similarly, the customer may also accept the offer advertised in offer advertisement widget 204 to receive a $50.00 cash back reward after performing five in-store purchases, each being $75.00 or more, at a physical location of merchant A.

[0033] When an offer advertisement widget, such as offer advertisement widget 202 or 204, is selected by a customer, an offer acceptance form 206 is caused to be displayed within interface 200. The customer then enters a variety of information that is subsequently used by OE 108 to determine whether the customer eventually satisfies the offer, as described in further detail below. The customer enters the details of one or more accounts, including account number, expiration date, security code, billing address, etc.

[0034] In some embodiments, the customer may optionally submit his or her phone number and/or email address to receive additional offer notifications from OE 108. When the customer provides a phone number and subsequently satisfies an offer, OE 108 may send an SMS message to the phone number with a message indicating that the offer has been satisfied. OE 108 may, in some embodiments, provide another offer to the customer for acceptance by the customer via SMS.

[0035] Additionally, the customer may submit his or her information by providing to OE 108 credentials that link to an existing online account hosted by an alternative online service, e.g., a Facebook account or an Oauth account. In particular, OE 108 accesses the online account using the credentials and retrieves the required information, thereby reducing the amount of input required by the customer.

[0036] Additionally, the customer may opt to create a customer account with OE 108 when accepting, for example, an offer for the first time. In one example, the customer opts to create a customer account by clicking on a checkbox titled "Create Account" (not shown) and included in offer acceptance form 206, which causes a password input field to appear. Subsequently, and upon providing valid inputs to OE 108 when accepting the offer, OE 108 generates a customer account for the customer and stores the customer account in DB 109. In one example, the customer's email address is assigned as a login ID and is tied to the password that is input by the customer. In this way, when the customer accepts additional offers, he or she is only required to input his or her email address and password by, for example, clicking the "Sign In" link included in offer acceptance form 206. In this way, the customer is able to recall his or her account information and is not required to redundantly provide his or her account information each time he or she accepts an offer.

[0037] Though not illustrated in FIG. 2, the customer may associate one or more of his or her account numbers with his or her account. Thus, the OE 108 can track transactions made using any one of the one or more accounts.

[0038] FIG. 3 is a flow diagram of method steps 300 for generating a merchant account, according to one embodiment of the invention. Persons skilled in the art will understand that, even though method 300 is described in conjunction with FIG. 1, any system configured to perform the method steps, in any order, is within the scope of embodiments of the invention. A merchant account enables merchants to manage offers through interfaces provided by OE 108. As shown, method 300 begins at step 302, where OE 108 receives, e.g., from an administrator of merchant 102, a request to generate a merchant account. For example, the administrator may click a "Sign Up" link found on an interface provided by OE 108 that causes a registration interface to be displayed.

[0039] At step 304, OE 108 receives merchant account registration information. Merchant account registration includes, for example, a merchant identification (ID) issued to merchant 102 by the merchant's acquiring bank and/or payment processor 110, where the merchant ID may be used to uniquely identify transactions initiated at merchant 102. POE 110 can filter transaction data processed by payment processor 110 such that POE 110 is able to determine whether accepted offers have been satisfied. As described in further detail below, embodiments of the invention provide a technique for determining a merchant ID of a merchant, since the merchant is sometimes not aware of their own merchant ID, and thus cannot provide this information to the OE 108 at step 304.

[0040] At step 306, and in response to receiving the merchant account registration information at step 304, OE 108 generates a merchant account based on the registration information. The merchant account and associated information is stored in database 109.

[0041] At step 308, OE 108 receives one or more requests to create offers. Such requests may be generated by merchant 102 via interfaces provided by OE 108 that enable merchant 102 to submit information associated with the offers. For example, the merchant 102 may request an offer that provides a reward of $30.00 cash-back to customers who accept the offer and perform a purchase of $150.00 or more with the merchant in a single transaction any time during the month of July in a given year.

[0042] At step 310, OE 108 causes the offers to be published so that they can be accepted by and/or satisfied by one or more customers. In some embodiments, a third-party, other than the OE 108 may publish the offers according to the techniques described above, e.g., web marketing campaigns, email marketing campaigns, etc. For example, merchant 102 may submit, for a particular offer, a list of customer email addresses to which an email that describes the offer should be sent. The offer email received by the customers may include a hyperlink that, when opened by a customer, displays to the customer an offer acceptance form associated with the offer, e.g., offer acceptance form 206.

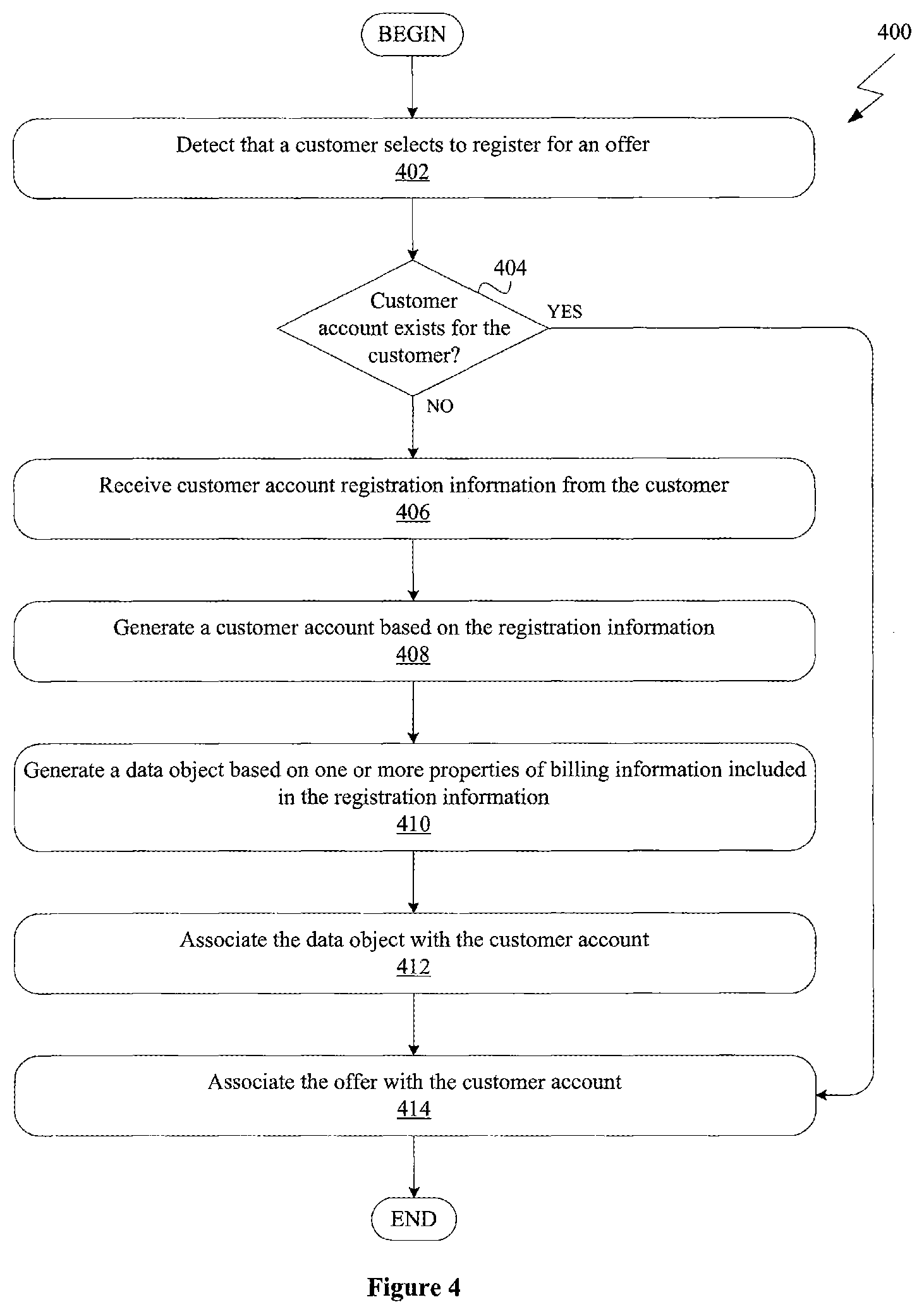

[0043] FIG. 4 is a flow diagram of method steps 400 for associating a customer with an offer, according to one embodiment of the invention. Persons skilled in the art will understand that, even though method 400 is described in conjunction with FIG. 1, any system configured to perform the method steps, in any order, is within the scope of embodiments of the invention. As shown, method 400 begins at step 402, where OE 108 detects that a customer selects to register for an offer, e.g., via clicking on offer advertisement widget 202.

[0044] At step 404, OE 108 determines whether a customer account exists for the customer. This may be determined according to a variety of techniques, including analysis of browser cookies, internet protocol (IP) addresses, login information, etc., that is accessible to OE 108 and/or provided by the customer. For example, the customer may select a "Sign In" hyperlink included in interface 200 and submit his or her login credentials, whereupon OE 108 references database 109 with the login credentials to determine whether a customer account exists for the customer. If the customer holds an account with OE 108, then OE 108 may display to the customer a list of one or more account numbers registered with the customer's account and previously provided by the customer, and method 400 proceeds to step 414, described below. If the customer does not hold an account with OE 108, then OE 108 displays to the customer input fields that enable him or her to input customer account registration information and accept the offer, and method 400 proceeds to step 406. At step 406, OE 108 receives customer account registration information from the customer, e.g., the customer account registration information described above in conjunction with FIG. 2.

[0045] At step 408, OE 108 generates a customer account based on the registration information. The customer account is then stored by OE 108 in database 109. At step 410, OE 108 generates a data object based on one or more properties of billing information included in the registration information. For example, OE 108 may apply a hash function to each account number to generate a corresponding hash value for each account. The hash function is configured to match a hash function executed by payment processor 110 that receives and hashes the account number of the customer when merchant 102 attempts to charge the customer for goods or services. In this way, OE 108 is capable of identifying transactions when reviewing transaction data provided by payment processor 110 and associated with merchant 102 without storing the actual account number, which advantageously decreases overall liability of OE 108 and increases security to the customer. At step 412, OE 108 associates the data object with the customer account.

[0046] At step 414, OE 108 associates the offer with the customer account. Thus, OE 108 may subsequently compare offers accepted by the customer with transaction data of merchants associated with the offers to determine whether the offers are satisfied, as described in further detail below in conjunction with FIG. 5.

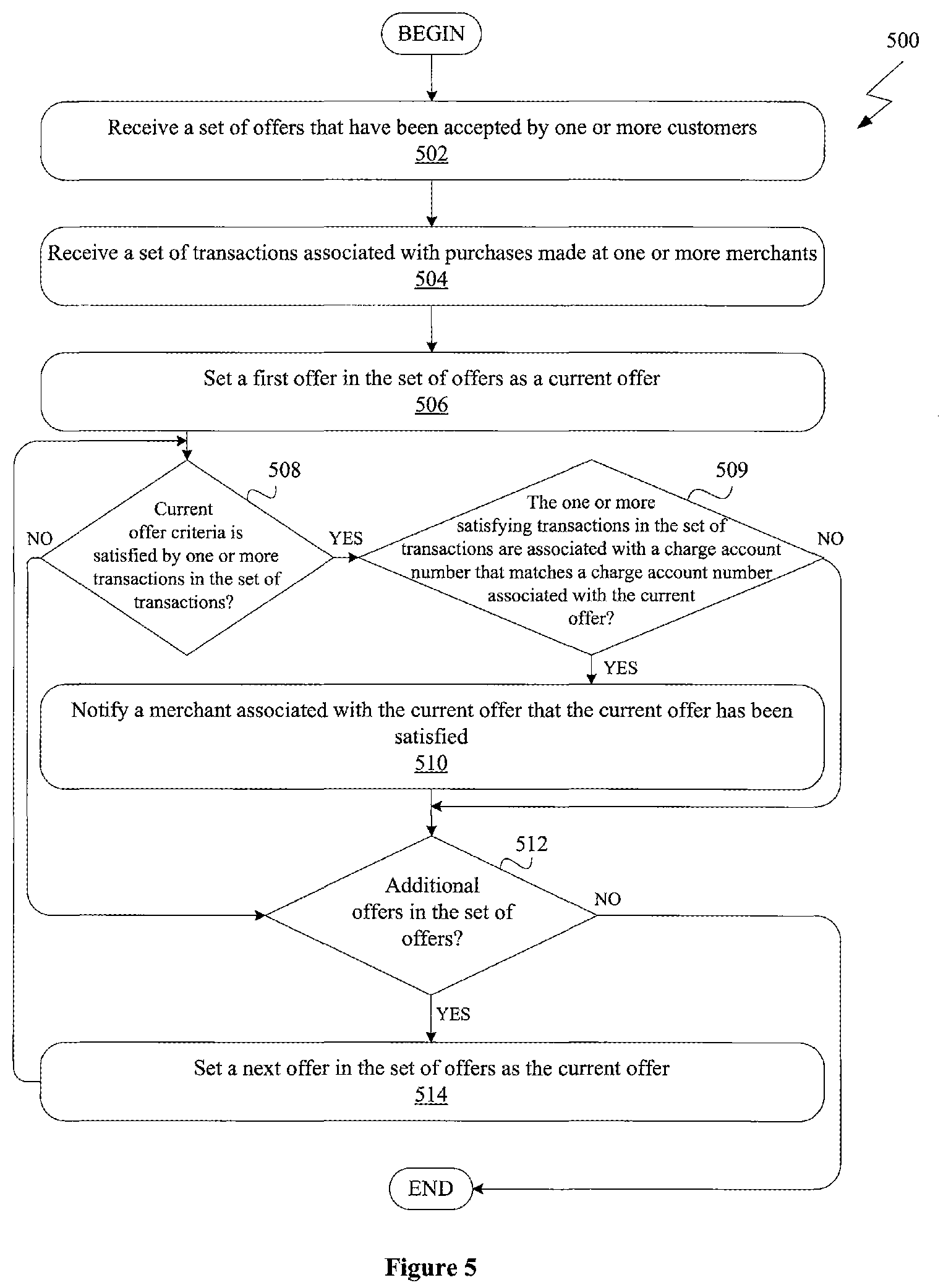

[0047] FIG. 5 is a flow diagram of method steps 500 for determining whether a set of offers has been satisfied, according to one embodiment of the invention. Persons skilled in the art will understand that, even though method 500 is described in conjunction with FIG. 1, any system configured to perform the method steps, in any order, is within the scope of embodiments of the invention. As shown, method 500 begins at step 502, where OE 108 receives a set of offers that have been accepted by one or more customers. For example, OE 108 may query database 109 to return a set of offers that have not been marked as expired or satisfied such that only outstanding and/or valid offers are processed.

[0048] At step 504, OE 108 receives a set of transactions associated with purchases made at one or more merchants. In one embodiment, OE 108 receives the set of transactions by querying payment processor 110 for particular transactions from one or more merchants. In one example, OE 108 may transmit to payment processor 110 both an ID of a merchant and a set of hashed account numbers associated with customers who have accepted at least one offer with the merchant. In response, payment processor 110 returns transactions that match the hashed account numbers. In another embodiment, a merchant can give the payment processor 110 permission to deliver all transactions from the merchant to a third party, such as OE 108. For example, the transactions can be delivered to the OE 108 periodically (e.g., daily) or in real-time.

[0049] At step 506, OE 108 sets a first offer in the set of offers as a current offer. At step 508, OE 108 determines whether criteria of the current offer are satisfied by one or more transactions in the set of transactions. In one embodiment, each offer is associated with executable code that, when executed by OE 108, enables OE 108 to determine whether the current offer has been satisfied by one or more transactions in the set of transactions. For example, if a customer accepts an offer that requires him or her to make an in-store purchase at merchant 102 between the hours of 5:00PM-6:00PM, and OE 108 determines from a transaction in the set of transactions that a customer performs a purchase at merchant 102, then OE 108 analyzes timestamp data included the transaction to determine whether the transaction was performed between the required hours.

[0050] If, at step 508, OE 108 determines that criteria of the current offer are not satisfied by one or more transactions in the set of transactions, then method 500 proceeds to step 512. Otherwise, at step 509, OE 108 determines whether the one or more transactions identified at step 508 are associated with an account number that matches an account number associated with the current offer. In one embodiment, OE 108 extracts a hashed account number from each transaction and compares the hashed account number against the hashed account number associated with the current offer. If, at step 509, OE 108 determines that the one or more transactions identified at step 508 are associated with an account number that matches an account number associated with the current offer, then method 500 proceeds to step 512. Otherwise, method 500 proceeds to step 510.

[0051] At step 510, OE 108 notifies a merchant associated with the current offer that the current offer has been satisfied. In one embodiment, OE 108 is configured to lookup via database 109 notification preferences of the merchant that is associated with the current offer. For example, OE 108 may determine that the merchant associated with the current offer prefers to receive a daily batch file emailed at the end of each day, where the batch file includes line-by-line detail of each customer who satisfied an offer and the reward that is to be given to them. In addition to notifying the merchant, OE 108 may also be configured to notify the customer associated with the current offer that he or she has satisfied the current offer, as described above in conjunction with FIG. 2.

[0052] At step 512, OE 108 determines whether additional offers are in the set of offers. If, at step 512, OE 108 determines that additional offers are in the set of offers, then at step 514, OE 108 sets a next offer in the set of offers as the current offer. In this way, each of the offers in the set of offers are compared against the set of transaction data.

[0053] FIG. 6 is a flow diagram of method steps 600 for processing a group offer, according to one embodiment of the invention. Persons skilled in the art will understand that, even though method 600 is described in conjunction with FIG. 1, any system configured to perform the method steps, in any order, is within the scope of embodiments of the invention. As shown, method 600 begins at step 602, where OE 108 determines that a group offer accepted by a first customer requires that one or more additional customers both accept and satisfy the group offer.

[0054] At step 604, OE 108 determines whether the one or more additional customers have accepted the group offer. In one example, the first customer accepts a group offer that requires a total of ten or more customers to spend $25.00 or more with merchant 102. In this case, OE 108 parses accepted group offers included in database 109 to determine whether nine or more different customers, in addition to the first customer, have also accepted the group offer.

[0055] If, at step 604, OE 108 determines that the one or more additional customers have not accepted the group offer, then the group offer has not been satisfied, and method 600 ends. Otherwise, method 600 proceeds to step 606, where OE 108 receives a set of transactions associated with purchases made by the first customer and the one or more additional customers according to the techniques described above in conjunction with FIG. 2. Alternatively, OE 108 may receive from payment processor 110 a set of all transactions associated with merchant 102 and filter out transactions that are not relevant to the group offer.

[0056] At step 608, OE 108 determines whether the first customer and the one or more additional customers have all satisfied the group offer. If, at step 608, OE 108 determines that the first customer and the one or more additional customers have all satisfied the group offer, then method 600 proceeds to step 610, where OE 108 notifies a merchant associated with the group offer that the group offer has been satisfied.

[0057] FIG. 7 is a flow diagram of method steps 700 for processing a referral offer, according to one embodiment of the invention. Persons skilled in the art will understand that, even though method 700 is described in conjunction with FIG. 1, any system configured to perform the method steps, in any order, is within the scope of embodiments of the invention. As shown, method 700 begins at step 702, where OE 108 determines that a referral offer accepted by a first customer requires that one or more additional customers recommended by the first customer both accept and satisfy an offer associated with the referral offer.

[0058] In one example, the first customer is exposed to an offer advertisement widget for a referral offer that requires him or her to get additional customers to both accept and satisfy an offer, where the offer requires them to make a purchase of $25.00 or more at merchant 102. Typically, the offer provides incentive to the five or more friends to both accept and satisfy the referral offer, such as $5.00 cash back for making the $25.00 purchase. In turn, the first customer is rewarded $50.00 by merchant 102 when each of the five or more friends both accept and satisfy the offer. The first customer may notify the five friends according to a variety of techniques, such as submitting their email addresses into an interface provided by OE 108, which then delivers a notification of the offer to each email address.

[0059] At step 704, OE 108 determines whether the one or more additional customers have accepted the offer. If, at step 704, OE 108 determines that the one or more additional customers have accepted the offer, then method 700 proceeds to step 706, where OE 108 receives a set of transactions associated with purchases made by the additional customers. Otherwise, the referral offer remains outstanding, and method 700 ends.

[0060] At step 708, OE 108 determines whether the one or more additional customers have all satisfied the offer. Continuing with the example described above at step 702, OE 108 determines whether each of the five customers have made a purchase of $25.00 or more with merchant 102. If, at step 708, OE 108 determines that the one or more additional customers have all satisfied the offer, then method 700 proceeds to step 710, where notifies a merchant associated with the referral offer that the referral offer has been satisfied.

[0061] As described above, OE 108 is configured to manage various types of offers using typical transaction data provided by payment processor 110. Typical transaction data includes properties such as a unique transaction ID, a merchant ID, the customer's card information, a total amount charged, and a timestamp. Though the total amount charged to the customer is included in the transaction data, important data pertaining to the breakdown of the total amount charged--among other more detailed information--is absent from the transaction data, which may be advantageously used by OE 108 to provide offers that are targeted toward, e.g., purchasing specific items from merchant 102.

[0062] Such detailed information is often stored in POS system 104 used by merchant 102 to process transactions. In one example, merchant 102 charges a customer $108.00 in total for five $20.00 items purchased, and an 8% sales tax on the total price. As described above in conjunction with FIG. 1, POS system 104 requests payment processor 110 to process the transaction, and payment processor 110 returns to POS system 104 the transaction ID of the transaction if the transaction is successfully processed. In turn, POS system 104 creates in database 109 a new POS transaction object that includes, e.g., a unique POS transaction ID, universal product codes (UPC) codes of each of the five items, product details of each of the five items, a subtotal amount, a tax amount, a total amount, and the transaction ID returned by payment processor 110. Moreover, many POS systems provide application programming interfaces (APIs) that enable administrators to extract transaction data to, e.g., process returns, calculate performance, and the like.

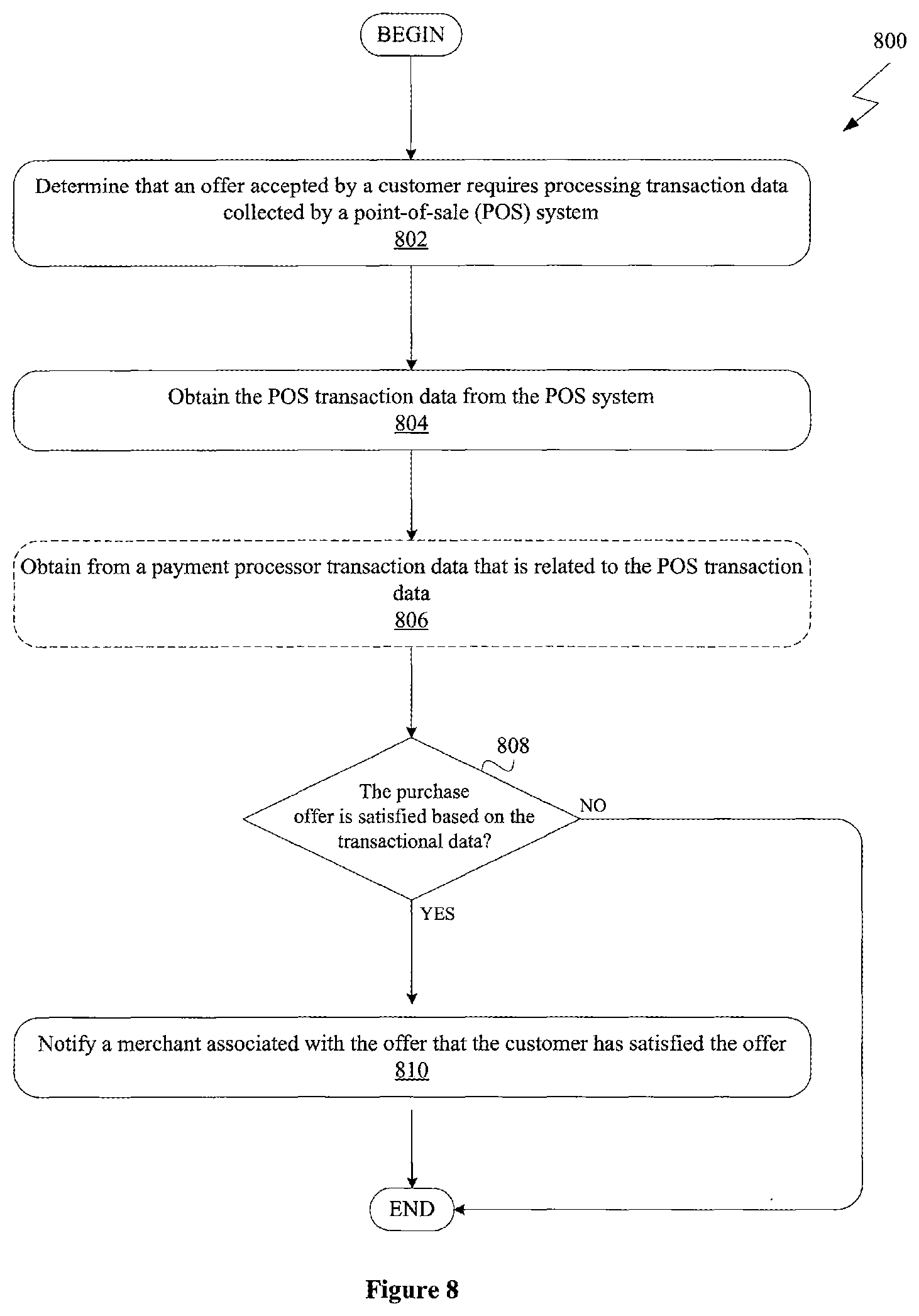

[0063] FIG. 8 is a flow diagram of method steps 800 for processing an offer involving specific criteria, according to one embodiment of the invention. Persons skilled in the art will understand that, even though method 800 is described in conjunction with FIG. 1, any system configured to perform the method steps, in any order, is within the scope of embodiments of the invention. As shown, method 800 begins at step 802, where OE 108 determines that an offer accepted by a customer requires processing transactional data collected by a point-of-sale (POS) system, e.g., POS system 104.

[0064] At step 804, OE 108 obtains the POS transaction data from POS system 104. In one embodiment, POS system 104 is configured to upload POS transaction data to OE 108 at regular intervals. In another embodiment, POS system 104 is configured to query POS system 104 via an API that provides access to POS system 104 to retrieve the POS transaction data.

[0065] Next, the optional step 806 enables OE 108 to verify that the purchase did in fact take place and that no corruption of POS system 104 has occurred. More specifically, at step 806, OE 108 optionally obtains from a payment processor, e.g., payment processor 110, transaction data that is related to the POS transaction data. In one example, OE 108 extracts the transaction ID from the POS transaction data which, as described above, is returned by payment processor 110 for each transaction that is successfully processed. OE 108 then queries payment processor 110 for a transaction that matches the transaction ID. If payment processor 110 returns a transaction based on the transaction ID, then OE 108 verifies that the POS transaction data obtained from POS system 104 is not corrupt. Otherwise, OE 108 may notify merchant 102 of the discrepancy.

[0066] At step 806, OE 108 determines whether the offer is satisfied based on the transactional data. In one example, the offer requires that the customer purchases a medium-sized black T-Shirt to receive a $2.00 reward. OE 108 then, according to the techniques described above in conjunction with FIG. 5, processes the POS transaction data to determine whether the offer has in fact been satisfied. For example, the POS transaction data may include a "Description" field with a value "Size: M; Color: Blk" that OE 108 is able to parse and identify as a purchase that satisfies the offer. In another example, merchant 102 may provide a UPC code associated with medium-sized black T-Shirts to OE 108 when creating the offer such that OE 108 need only verify that UPC code included in the POS transaction data is valid.

[0067] At step 808, OE 108 notifies merchant 102 associated with the offer that the customer has satisfied the offer according to the

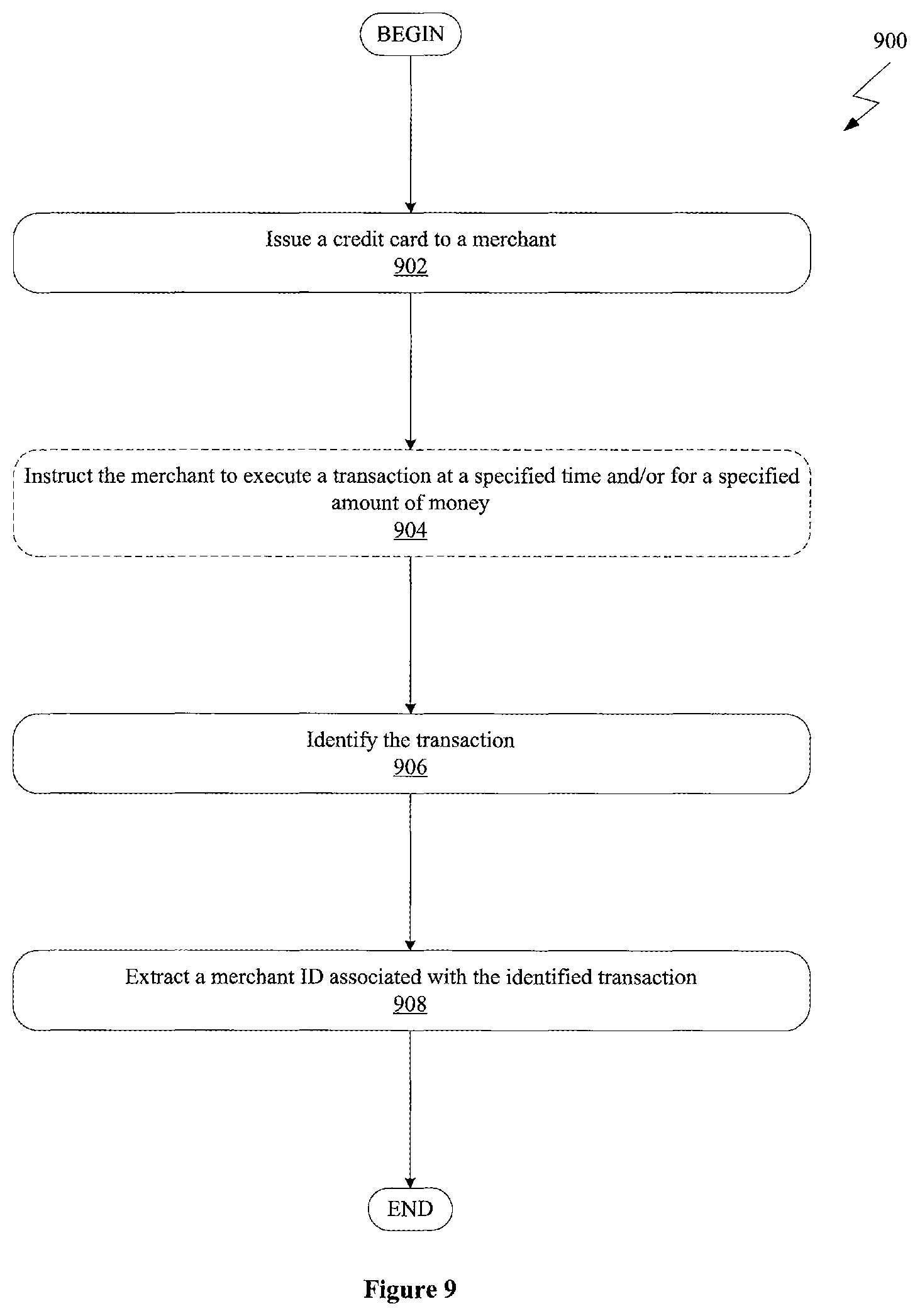

[0068] FIG. 9 is a flow diagram of method steps 900 for extracting an identification (ID) of a merchant, according to one embodiment of the invention. Persons skilled in the art will understand that, even though method 900 is described in conjunction with FIG. 1, any system configured to perform the method steps, in any order, is within the scope of embodiments of the invention. In the method 900, OE 108 is configured to act as an issuing bank. More specifically, OE 108 is configured to issue one or more pre-paid credit cards that are distributed to merchants who are unaware of their merchant ID, which is a typical problem. When charges are attempted on such cards, OE 108 receives a transaction request because the OE 108 is the issuer of the card. The transaction received by the OE 108 includes at least a merchant ID of the merchant that is attempting to charge the card. The transaction may also include a date/time that the transaction was generated and amount associated therewith.

[0069] As shown, method 900 begins at step 902, where OE 108 issues a credit card to a merchant. OE 108 also maintains a hash of the numbers included on the credit card according to the hashing techniques described above in conjunction with FIG. 4 such that comparisons can be made in a secure manner.

[0070] At step 904, OE 108 instructs merchant 102 to execute a transaction at a specified time and/or for a specified amount of money. In one example, merchant 102 is instructed by OE 108 to attempt a charge for $11,302.34 on Jan. 23, 2011 between the hours of 3:00PM and 4:00PM.

[0071] At step 906, OE 108 identifies the transaction. In one embodiment, OE 108 is configured to automatically identify the transaction when a request for the transaction is received. In another embodiment, OE 108 is configured to parse a set of transactions, e.g., at the end of each day, to identify the transaction. At step 908, OE 108 extracts a merchant ID associated with the identified transaction. In turn, the merchant ID may be used to register a merchant account, as described above in conjunction with FIG. 3. In some embodiments, the OE 108 may then decline the transaction so that no funds are actually transferred between financial institutions.

[0072] Advantageously, embodiments of the invention provide an improved technique for monitoring for offline transactions. A customer accepts an offer provided by a merchant and submits his or her account information so that he or she may receive a reward for satisfying criteria associated with the offer. Transactions of the merchant are then monitored to determine whether the customer satisfies the purchase criteria. As a result, the merchant is able to determine the overall effectiveness of advertising campaigns by analyzing the number of offers that are both accepted and satisfied.

[0073] While the foregoing is directed to embodiments of the present invention, other and further embodiments of the invention may be devised without departing from the basic scope thereof. For example, aspects of the present invention may be implemented in hardware or software or in a combination of hardware and software. One embodiment of the invention may be implemented as a program product for use with a computer system. The program(s) of the program product define functions of the embodiments (including the methods described herein) and can be contained on a variety of computer-readable storage media. Illustrative computer-readable storage media include, but are not limited to: (i) non-writable storage media (e.g., read-only memory devices within a computer such as CD-ROM disks readable by a CD-ROM drive, flash memory, ROM chips or any type of solid-state non-volatile semiconductor memory) on which information is permanently stored; and (ii) writable storage media (e.g., floppy disks within a diskette drive or hard-disk drive or any type of solid-state random-access semiconductor memory) on which alterable information is stored. Such computer-readable storage media, when carrying computer-readable instructions that direct the functions of the present invention, are embodiments of the present invention.

[0074] In view of the foregoing, the scope of the present invention is determined by the claims that follow.

* * * * *

D00000

D00001

D00002

D00003

D00004

D00005

D00006

D00007

D00008

D00009

XML

uspto.report is an independent third-party trademark research tool that is not affiliated, endorsed, or sponsored by the United States Patent and Trademark Office (USPTO) or any other governmental organization. The information provided by uspto.report is based on publicly available data at the time of writing and is intended for informational purposes only.

While we strive to provide accurate and up-to-date information, we do not guarantee the accuracy, completeness, reliability, or suitability of the information displayed on this site. The use of this site is at your own risk. Any reliance you place on such information is therefore strictly at your own risk.

All official trademark data, including owner information, should be verified by visiting the official USPTO website at www.uspto.gov. This site is not intended to replace professional legal advice and should not be used as a substitute for consulting with a legal professional who is knowledgeable about trademark law.