Method For Authenticating Financial Instruments And Financial Transaction Requests

Kelly; James John ; et al.

U.S. patent application number 16/875318 was filed with the patent office on 2020-09-03 for method for authenticating financial instruments and financial transaction requests. The applicant listed for this patent is Capital One Services, LLC. Invention is credited to Joseph DeLiberis, James John Kelly, Robert Dean Rowley, III, Todd Adam Sandler, Daniel Lloyd Struble, Rudolph Christian Wolfs.

| Application Number | 20200279275 16/875318 |

| Document ID | / |

| Family ID | 1000004828321 |

| Filed Date | 2020-09-03 |

View All Diagrams

| United States Patent Application | 20200279275 |

| Kind Code | A1 |

| Kelly; James John ; et al. | September 3, 2020 |

METHOD FOR AUTHENTICATING FINANCIAL INSTRUMENTS AND FINANCIAL TRANSACTION REQUESTS

Abstract

A method for authenticating a check of a plurality of checks where the check was previously issued from a first party to a second party, including receiving first information from the first party, storing the first information in a file of a third party and receiving the check. The check has first party identifying information, a unique pseudorandom number of a pseudorandom sequence, and an amount. A status of activating the plurality of checks is determined. At least a portion of the first party identifying information included with the check, the unique pseudorandom number included with the check and the check amount included with the check are authenticated. The received check is authenticated if the first party, the unique pseudorandom number included with the check and the amount included with the check are authenticated and if the plurality of checks have been activated.

| Inventors: | Kelly; James John; (Hockessin, DE) ; Rowley, III; Robert Dean; (West Chester, PA) ; Sandler; Todd Adam; (Gladwyne, PA) ; Struble; Daniel Lloyd; (Newark, DE) ; Wolfs; Rudolph Christian; (Fort Meyers Beach, FL) ; DeLiberis; Joseph; (Gibbstown, NJ) | ||||||||||

| Applicant: |

|

||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Family ID: | 1000004828321 | ||||||||||

| Appl. No.: | 16/875318 | ||||||||||

| Filed: | May 15, 2020 |

Related U.S. Patent Documents

| Application Number | Filing Date | Patent Number | ||

|---|---|---|---|---|

| 15655971 | Jul 21, 2017 | 10672009 | ||

| 16875318 | ||||

| 12971713 | Dec 17, 2010 | 9747601 | ||

| 15655971 | ||||

| 12768876 | Apr 28, 2010 | 8626656 | ||

| 12971713 | ||||

| Current U.S. Class: | 1/1 |

| Current CPC Class: | G06Q 20/04 20130101; G06Q 20/105 20130101; G06Q 20/40 20130101; G06Q 20/042 20130101; G06Q 30/0185 20130101; G06Q 20/354 20130101 |

| International Class: | G06Q 30/00 20060101 G06Q030/00; G06Q 20/04 20060101 G06Q020/04; G06Q 20/10 20060101 G06Q020/10; G06Q 20/34 20060101 G06Q020/34; G06Q 20/40 20060101 G06Q020/40 |

Claims

1. A method for authenticating a checking transaction comprising: receiving, at a financial institution, a first payment amount for a checking transaction of a payor and information for identifying a check for the checking transaction, the check being associated with a set checks; receiving, at the financial institution, a checking request for a received check, the checking request including information for identifying the payor, a unique pseudorandom code of a pseudorandom sequence, wherein the pseudorandom sequence is for each check in the set of checks and generated via a random number processor, and a requested amount; determining, at the financial institution, that the received check is activated based on a stored activation code for the set of checks; determining, at the financial institution, that the information for identifying the payor matches stored information for identifying the payor; determining, at the financial institution, that the unique pseudorandom code matches a stored pseudorandom sequence; determining, at the financial institution, that the requested amount matches the first payment amount for the checking transaction; and authenticating, at the financial institution, the received checking request.

2. The method of claim 1, further comprising: providing an online banking interface to the payor for entering the first payment amount and information for identifying the check; and receiving the first payment amount and information for identifying the check via the online banking interface.

3. The method of claim 2, further comprising: storing information associated with each check of the plurality of checks in a database residing on non-volatile memory of the financial institution and accessible to the online banking interface; updating information associated with each check of the plurality of checks in the online banking interface using information received from the payor to create updated information; storing the updated information in the database; and dynamically displaying the updated information in the online banking interface.

4. The method of claim 2, wherein the online banking interface is provided at a website or a web portal of the financial institution.

5. The method of claim 1, wherein the information for identifying the check further comprises at least one of a name of a payee, an address of the payee, a check date, a time the check was drafted, or a check memo.

6. The method of claim 1, further comprising: associating the stored activation code with each unique pseudorandom code of the pseudorandom sequence; and associating the stored activation code with additional information for identifying the payor.

7. A method for authenticating a checking transaction comprising: receiving, at a financial institution, a first payment amount for a checking transaction of a payor and information for identifying a check for the checking transaction, the check being associated with a set checks; receiving, at the financial institution, a checking request for a received check, the checking request including information for identifying the payor, a unique pseudorandom code of a pseudorandom sequence, wherein the pseudorandom sequence is for each check in the set of checks and generated via a random number processor, and a requested amount; determining, at the financial institution, whether the received check is activated based on a stored activation code for the set of checks; determining, at the financial institution, whether the information for identifying the payor matches stored information for identifying the payor; determining, at the financial institution, whether the unique pseudorandom code matches a stored pseudorandom sequence; determining, at the financial institution, whether the requested amount matches the first payment amount for the checking transaction; and when the received check is activated, the information for identifying the payor matches the stored information for identifying the payor, the unique pseudorandom code matches the stored pseudorandom sequence, and the requested amount matches the first payment amount: authenticating, at the financial institution, the checking request; or when the received check is not activated, the information for identifying the payor does not match the stored information for identifying the payor, the unique pseudorandom code does not match the stored pseudorandom sequence, or the requested amount does not match the first payment amount: declining, at the financial institution, the checking request.

8. The method of claim 7, wherein the checking request is declined, the method further comprising: notifying the payor of the declined checking request.

9. The method of claim 8, further comprising: receiving a request from the payor to cancel the check; canceling the check; and notifying the payor of the cancellation of the check.

10. The method of claim 7, further comprising: associating the stored activation code with each unique pseudorandom code of the pseudorandom sequence; and associating the stored activation code with additional information for identifying the payor.

11. The method of claim 10, further comprising: dynamically displaying stored information associated with the check to the payor, the stored information including the first payment amount and information for identifying the check, the unique pseudorandom code of the check, and the additional information.

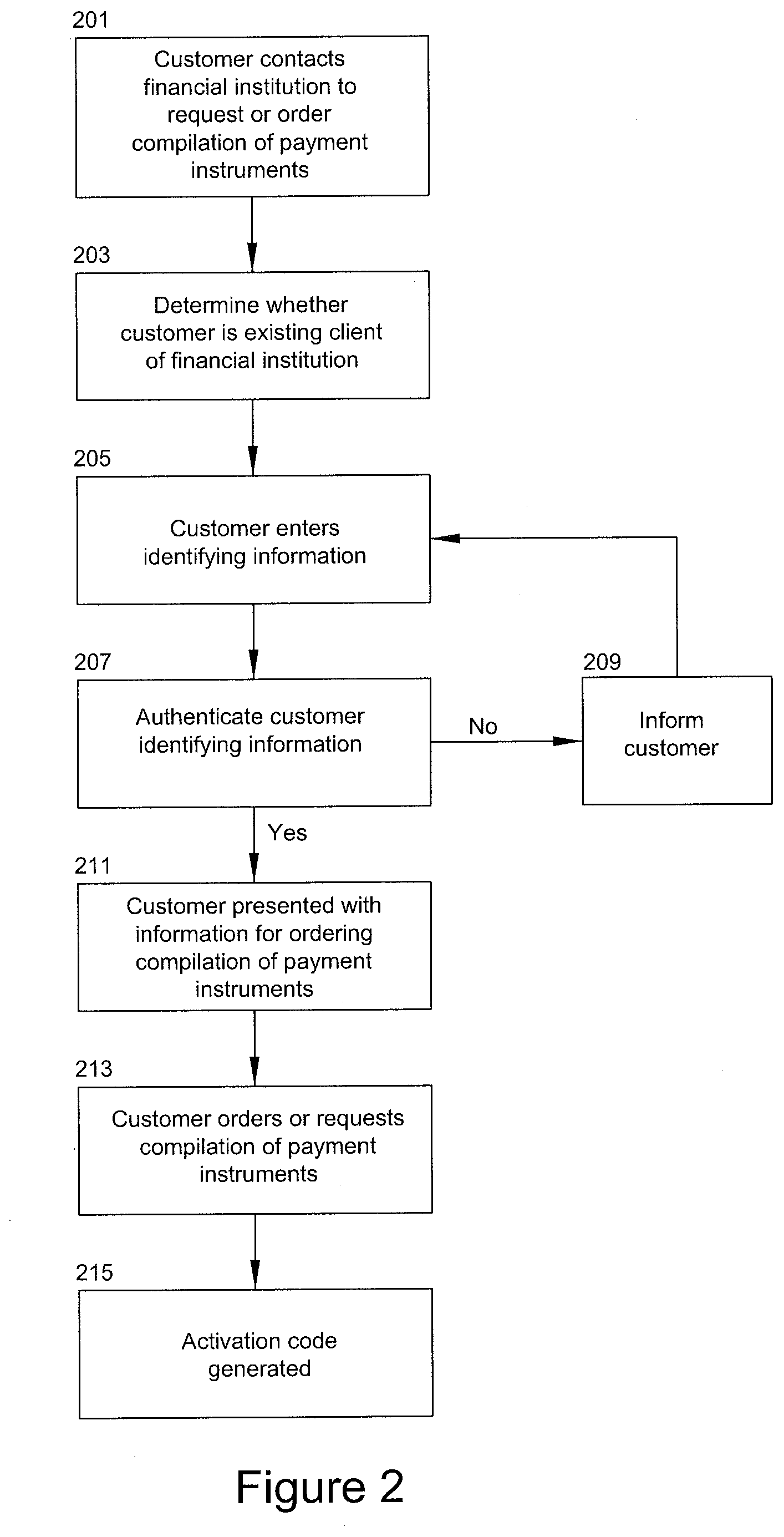

12. The method of claim 7, wherein the requested amount does not match the first payment amount, the method further comprising: sending, from the financial institution, a request to an online banking interface for an updated payment amount from the payor; determining that the updated payment amount matches the first payment amount; and authenticating, at the financial institution, the received checking request.

13. The method of claim 7, wherein the received check is not activated, the method further comprising: sending, from the financial institution, a request to an online banking interface for the payor to activate the received check; receiving, from the online banking interface, an indication that the received check has been activated by the payor; and authenticating, at the financial institution, the received checking request.

14. The method of claim 7, wherein the received check is not activated, the method further comprising: sending, from the financial institution, a request to an online banking interface for the payor to activate the received check; receiving, from the online banking interface, an indication that the received check has not been activated by the payor; and declining, at the financial institution, the received checking request; and notifying the payor of the declined checking request.

15. The method of claim 7, wherein the received check is activated, the information for identifying the payor matches the stored information for identifying the payor, the unique pseudorandom code matches the stored pseudorandom sequence, and the requested amount matches the first payment amount, the method further comprising: sending, from the financial institution, a request to an online banking interface for the payor to authorize the received check; receiving, from the online banking interface, an indication that the received check has been authorized by the payor; and authenticating, at the financial institution, the received checking request.

16. A system for authenticating a checks, the system comprising: one or more processors; one or more transceivers for sending and receiving wired and/or wireless communications; and non-volatile memory storing an electronic check register and instructions that when executed by the one or more processors cause the one or more processors to: receive, at the one or more transceivers, a first signal indicating that a plurality of checks were issued to a payor with an activation code and a unique pseudorandom code of a pseudorandom sequence, wherein the pseudorandom sequence is for each check in a set of checks and generated via a random number processor; automatically update an electronic check register stored in the non-volatile memory to indicate that the plurality of checks were issued to the payor; receive a second signal indicating that the plurality of checks were activated using the activation code; automatically update the electronic check register to indicate that the plurality of checks were activated; receive, at the one or more transceivers, a first unique pseudorandom code and an amount of a check of the plurality of checks from the payor; automatically update the electronic check register to indicate that the check was issued to a payee and the amount; receive, at the processor, a second unique pseudorandom code of a check and an expected amount from the payee; determine whether the received unique pseudorandom code and the amount matches information stored in the electronic check register; determine whether the check has been activated; and when the unique pseudorandom code and the amount matches the information stored in the electronic check register and the check has been activated: authenticate the received checking request; or when the unique pseudorandom code or the amount does not match the information stored in the electronic check register or the check has not been activated: decline the received checking request.

17. The system of claim 16, wherein the information for identifying the check further comprises at least one of a name of a payee, an address of the payee, a check date, a time the check was drafted, or a check memo.

18. The system of claim 16, wherein the checking request is declined, wherein the instructions further cause the one or more processors to: send, with the one or more transceivers, a message notifying the payor of the declined checking request.

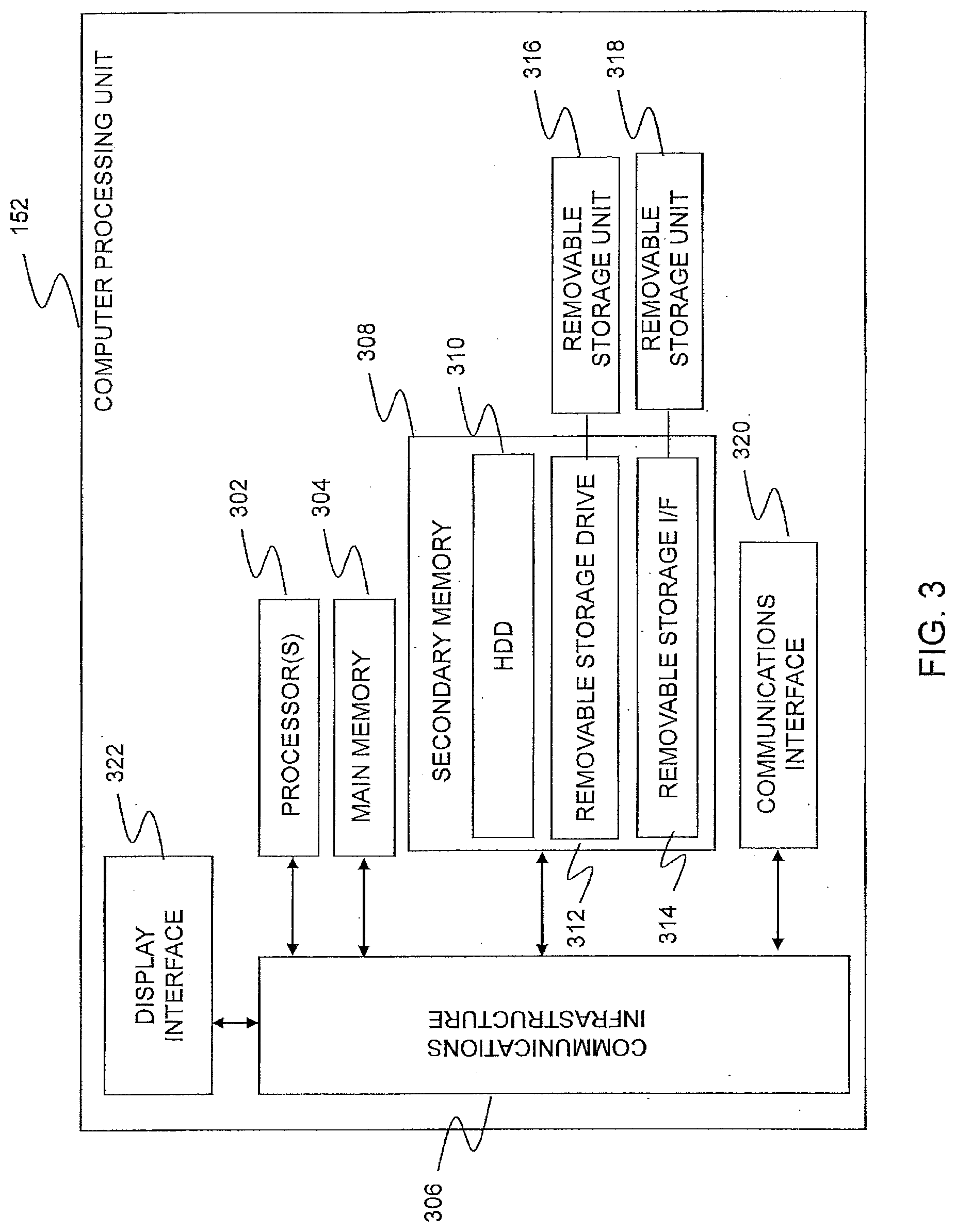

19. The system of claim 16, wherein the instructions further cause the one or more processors to: receive, at the one or more processors, a request from the payor to cancel the check; cancel the check; and notify the payor of the cancellation of the check.

20. The system of claim 16, wherein the instructions further cause the one or more processors to: associate the activation code with each unique pseudorandom code of the pseudorandom sequence; and associate the activation code with additional information for identifying the payor.

Description

CROSS REFERENCE TO RELATED APPLICATIONS

[0001] This application is a continuation of, and claims priority under 35 U.S.C. .sctn. 120 to, U.S. patent application Ser. No. 15/655,971, filed Jul. 21, 2017 of the same title, which is a continuation of U.S. patent application Ser. No. 12/971,713, filed Dec. 17, 2010, now U.S. Pat. No. 9,747,601 of the same title, which is a continuation-in-part of U.S. patent application Ser. No. 12/768,876, filed Apr. 28, 2010, now U.S. Pat. No. 8,626,656, and entitled "SYSTEM AND METHOD FOR SECURING PAYMENT INSTRUMENTS," the entire contents of which are fully incorporated herein by reference.

FIELD

[0002] The present disclosure is directed generally to methods for protecting sensitive financial information from theft and fraud. In particular, the present disclosure relates to methods for authenticating the initiation of a financial transaction.

BACKGROUND

[0003] Safeguarding customer financial information against criminal fraudsters, forgers and cybercriminals represents an ongoing battle for consumers, businesses and financial institutions. Financial fraud can assume many forms including swindling, payment instrument fraud, debit or credit card fraud, real estate fraud, identity theft, deceptive telemarketing, or even money laundering. Personal computers continue to be a favorite target for fraudsters as they are typically poorly protected. Common attacks against consumers include the use of mirror or phishing sites, pharming sites, carding or skimming techniques, and crimeware such as Trojans. Although advancements in computer technology have offered more robust security features to consumers, businesses and financial institutions, they have also offered an easier operating environment for fraudsters to manipulate financial instruments, such as payment instruments, in such a way as to deceive innocent victims expecting value in exchange for their money.

[0004] In particular, payment instrument fraud is one of the largest challenges facing businesses, consumers and financial institutions today. Annual losses due to payment instrument fraud are estimated to be in the billions of dollars. This problem affects consumers who face financial losses and anxiety from the instant theft and also from possible future repercussions with credit bureaus. The Uniform Commercial Code has placed increasing emphasis on the role of businesses and financial institutions in ensuring that their issued payment instruments are secure.

[0005] Victims of payment instrument fraud include financial institutions, businesses who accept and issue payment instruments, and the consumer. These crimes may begin with the theft of a financial document, for example, the theft of a blank check from a consumer's home or vehicle during a burglary, searching for a canceled or old check in the garbage, or removing a consumer's check from a mailbox. As financial institutions also continue to expand "automated clearing house" (or ACH) activities, the foregoing fraud risks only increase. ACH refers to an electronic clearing and settlement system for exchanging electronic credit and debit transactions among participating depository institutions. These electronic transactions are substitutes for paper checks and are typically used to make recurring payments such as payroll or loan payments. ACH transactions are often available as a way to reload prepaid debit cards issued by many companies.

[0006] Common types of payment instrument fraud include forgery where an individual, such as a disgruntled employee of a financial institution or business, issues a check without proper authorization, counterfeiting where a payment instrument may be fabricated as a whole or duplicated, alteration where chemicals are used to remove or modify information on the payment instrument, paperhanging where consumers purposefully write checks on closed accounts, or kiting where a fraudster opens accounts at two or more financial institutions and uses "the float time" of available funds to create fraudulent balances. In particular, payment instrument compilations, such as paper checkbooks, are particularly prone to fraud due to check number guessing and limited controls placed on the physical paper checks within the checkbook.

[0007] Conventional systems and methods have utilized transaction specific information, such as a transaction amount or a particular type of transaction, to permit independent verification of a transaction and a payment instrument. For example, U.S. Pat. No. 4,630,201 to White discloses a paper check security feature in which the checks include unique transaction numbers. When a check is cleared, the bank compares the unique transaction number to a stored number to determine if the check number is being duplicated. White further discloses that a password protected portable device generates the transaction numbers. Additionally, U.S. Patent Publication Ser. No. 2005/0149439 to Suisa discloses a paper check security feature in which the checks include unique transaction numbers generated for a particular type of transaction. When a check is cleared, the bank compares the unique transaction number to a stored number to determine if the check number is being duplicated. Further by way of example, U.S. Pat. No. 5,754,653 to Canfield discloses a paper check security feature that uses a security code that is unique for each check and for each transaction involving a check. The security code is generated from the check sequence number preprinted on the check or the total transaction amount and a customer selected base code. Still further, U.S. Pat. No. 4,958,066 to Hedgcoth discloses a checkbook in which each check has a randomly assigned number. The number is used to verify the authenticity of the check by comparing it to digits on the payor's ATM card or separate dedicated, disposable card, but is not compared to a stored bank number during check clearing.

[0008] In U.S. Pat. No. 6,754,640, to Bozeman, a system is disclosed for a customer to enter current check register information via an interface such as a PC or PDA, and that a financial institution, intermediary, clearing house can match and compare the information from a check to the information in the check register. If the check has been altered in any way, then the transaction is stopped. The system notifies each of the parties when a check has been rejected or when a deposit has occurred. Electronic check processing and electronic check registering is disclosed that allows checks to be deposited and cleared in a wide variety of ways, including ACH.

[0009] In U.S. Patent Pub. No. 20100078471 to Lin et al., discloses peer-to-peer financial transactions using one or more electronic devices such as a mobile device. The device includes one or more input interfaces, including a camera, image processing software, and communication interfaces to retrieve transaction information from a payment instrument, such as a check, transmit payment information to a financial server and/or another electronic device or conduct a transaction. Lin et al., also disclose using a partial image of the check. A notification message is provided on the screen of the mobile device including information regarding the transaction, such as the depositing of a requested payment amount.

[0010] U.S. Pat. No. 7,774,283, issued to Das et al., discloses a system for a mobile device, including a camera, to capture an image of a bar code on a "printed medium", decodes the transaction information and identification information for a business entity contained in the bar code and communicates the transaction information to the business entity that is identified in the bar code to conduct the transaction.

[0011] U.S. Pat. No. 7,389,913, issued to Starrs, discloses a system for a customer to provide online and/or electronically, such as via a graphical user interface, check information for a transaction. Starrs suggests that the check information is used by a financial institution to create an electronic image of an authorized demand check to provide funds to a third party (bank, retailer, etc. . . . ) via wire or a paper check.

[0012] U.S. Patent Pub. No. 20020120846 to Stewart, et al., discloses an electronic check payment system designed to facilitate network transactions, e.g., via the Internet. In the system, a consumer enters identifying information and check information, including MICR information, into a payment portal. The financial institution or merchant's server receives the electronic check information via the Internet and transfers this check information to an authorization server. The authorization server verifies the identity of the consumer, does a risk analysis, sends an acceptance or declination message back to the merchant server and sends the check information to an ACH. The deposit is then processed as an ACH transfer.

[0013] U.S. Pat. No. 6,064,990, issued to Goldsmith, discloses a system for notifying a user of account activity, such as a withdrawal from a savings or checking account. The system maintains information on financial accounts and customer contact information for a financial account of the customer. Information on a transaction with respect to the customer's financial account is received and processed. The system processes the information on the transaction and generates a message, e.g., bye-mail, page, or phone call, providing information on the transaction, retrieves the user contact information for the financial account involved in the transaction and transmits the notification message to the location identified by the user contact information for the financial account. Goldsmith discloses the notification may include transaction-related information.

[0014] U.S. Patent Pub. No. 20020013711 to Ahuja et al., discloses a customer being provided with access to a notification or alert system, that an "event" which is selected by the customer is received and stored in a database following its selection, that "trigger" data from a separate database, including a database containing customer financial information, is received which triggers the selected event, and that the customer is notified of the triggering of the event via a "notification message" (i.e. alert). Possible triggers include specific credit charges (e.g., single amount charges, location charges), direct deposits, check clearing alert and ATM withdrawals. The customer is asked to select a "method of notification" and the customer's selected notification method is stored in a database. The "notification message" is sent to the customer via the customer's selected notification method.

[0015] U.S. Pat. No. 5,878,337, issued to Joao discloses a system that receives information regarding a financial transaction and transmits a notification to a "communication device" of the customer (such as a cell phone or PDA of the customer) such that the notification serves as an alert to notify the customer of the financial transaction. The information and/or data transmitted to the communication device may include information and/or data identifying the transaction, such as the amount, time, location of the transaction, contact information for the customer to respond in order to authorize or cancel the transaction, the type of goods and/or services involved in the transaction. Joao discloses that this information may be displayed to the customer on the communication device. Joao also discloses that the system may wait for the customer to respond to the transmission, and/or may permit the customer to approve, or authorize, the transaction or to disapprove, or void the transaction.

[0016] Conventional technologies instituted by financial institutions to minimize fraud and secure financial information have also included implementing procedures to actively monitor for customer check sequence numbers that are used out of sequence. Additionally, some financial institutions have established policies to only process check sequence numbers that they know have been sent to a consumer. However, there remains a need in the art to overcome conventional limitations and provide a novel system and method for securing payment instruments, such as checks, with improved security and fraud protection capability.

SUMMARY

[0017] One embodiment of the present invention provides a method for authenticating a check where the check is one of a plurality of checks and where the check was previously issued from a first party to a second party, including receiving first information from the first party. The first information includes an amount of the check and information for identifying the check. The first information is stored in a file of a third party. The check having information for identifying the first party, a unique pseudorandom number of a pseudorandom sequence, and an amount, included with the check is received. A status of activating the plurality of checks is determined using at least a portion of the information for identifying the first party included with the check, a stored activation code, and stored information for identifying the first party. The stored information for identifying the first party is stored with the pseudorandom sequence. The at least a portion of the information for identifying the first party included with the check is authenticated with the stored information for identifying the first party. The unique pseudorandom number included with the check is authenticated using at least a portion of the information for identifying the first party included with the check, the stored information for identifying the first party and the stored sequence. The amount included with the check is authenticated using the stored first information. The received check is authenticated if (i) the first party, (ii) the unique pseudorandom number included with the check and (iii) the amount included with the check are authenticated and (iv) if the plurality of checks have been activated.

[0018] Another embodiment of the present invention provides a method for authenticating a financial transaction request where the financial transaction request is representative of a check and where the check was previously issued from a first party to a second party, including providing a first computer processor at a third party. The first computer processor has a computer readable storage medium. The computer readable storage medium includes instructions stored therein for executing on the processor. The instructions when read and executed are for receiving first information from the first party. The first information includes a check amount and information for identifying the check. The first information is stored in a file of the third party. Second information including information for identifying the first party, a unique pseudorandom number of the check, and the check amount is received. The unique pseudorandom number of the check includes a pseudorandom number of a pseudorandom number sequence associated with a plurality of checks. A status of activating the plurality of checks is determined using at least a portion of the information for identifying the first party included with the second information, a stored activation code, and stored information for identifying the first party. The stored information for identifying the first party is stored with the pseudorandom sequence. The at least a portion of the information for identifying the first party included with the second information is authenticated with stored information for identifying the first party. The unique pseudorandom number included with the second information is authenticated using at least a portion of the information for identifying the first party included with the second information, the stored information for identifying the first party and the stored sequence. The amount included with the second information is authenticated using the stored first information. The second information is authenticated if (i) the at least a portion of the information for identifying the first party included with the second information, (ii) the unique pseudorandom number included with the second information and (iii) the amount included with the second information are authenticated and (iv) if the plurality of checks have been activated.

[0019] These embodiments and many other objects and advantages thereof will be readily apparent to one skilled in the art to which the invention pertains from a perusal of the claims, the appended drawings, and the following detailed description of the embodiments.

BRIEF DESCRIPTION OF THE DRAWINGS

[0020] Various aspects of the present disclosure will be or become apparent to one with skill in the art by reference to the following detailed description when considered in connection with the accompanying exemplary non-limiting embodiments. In the Figures like elements have been given like numerical designations to facilitate an understanding of the present invention.

[0021] FIG. 1 is a diagram of an online banking access system connected to a plurality of interconnected computer system networks and devices according to an embodiment of the present disclosure.

[0022] FIG. 2 is a flow chart of for a method for securing financial information according to an embodiment of the disclosure.

[0023] FIG. 3 is a diagram of an illustrative example of an architecture of a computer processing unit with the present invention.

[0024] FIG. 4 is a flow chart illustrating a method for securing payment instruments according to an embodiment of the present invention.

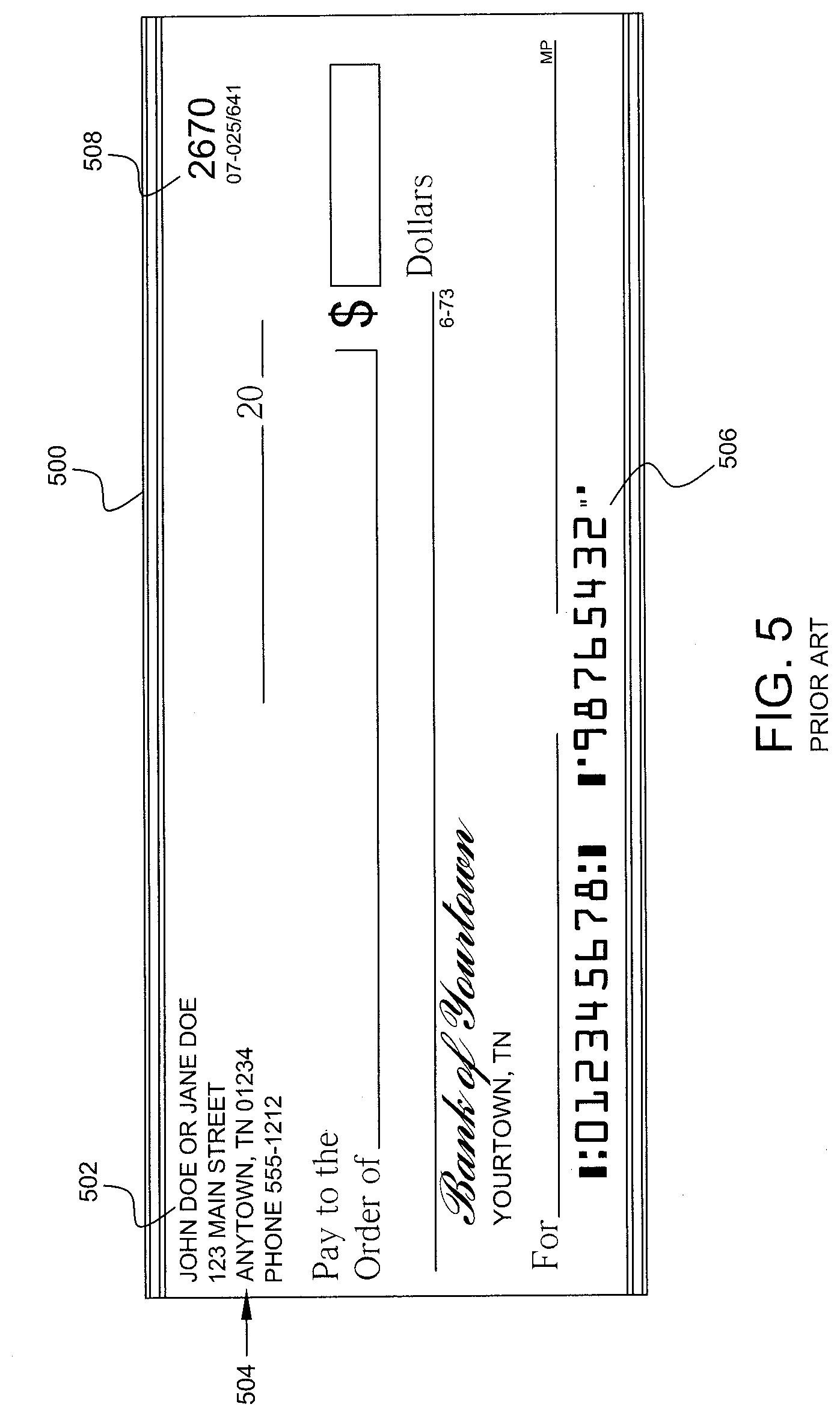

[0025] FIG. 5 is a diagram of a conventional paper check.

[0026] FIG. 6 is a flow chart illustrating a method for securing payment instruments according to an embodiment of the present invention.

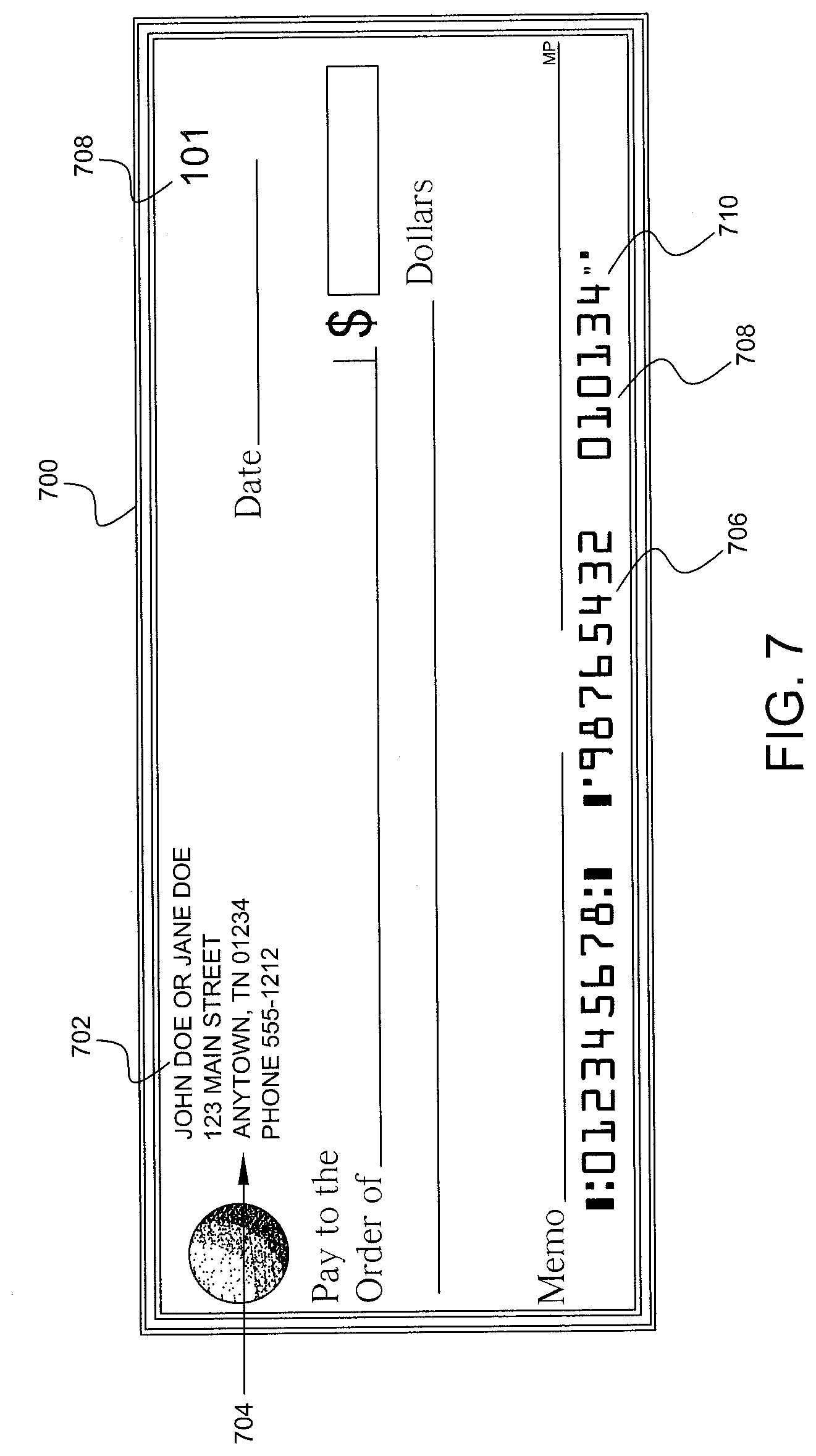

[0027] FIG. 7 is an illustrative example of a paper check according to an embodiment of the present disclosure.

[0028] FIG. 8 is a flow chart showing a method for activating a compilation of payment instruments according to an embodiment of the present disclosure.

[0029] FIG. 9 is an illustrative website screenshot according to an embodiment of the present invention.

[0030] FIG. 10 is a flow chart for authenticating a received payment instrument according to an embodiment of the present disclosure.

[0031] FIG. 11 is an illustrative example of a paper check according to an embodiment of the present disclosure.

[0032] FIG. 12 is an illustrative website screenshot according to an embodiment of the present disclosure.

[0033] FIG. 13 is an illustrative website screenshot according to an embodiment of the present disclosure.

[0034] FIG. 14 is a flow chart for clearing a payment instrument according to an embodiment of the present disclosure.

[0035] FIG. 15 is a flow chart for clearing a payment instrument according to another embodiment of the present disclosure.

[0036] FIG. 16 is a flow chart for clearing a payment instrument according to an embodiment of the present disclosure.

[0037] FIG. 17 is an illustrative website screenshot according to an embodiment of the present disclosure.

[0038] FIG. 18 is an illustrative website screenshot according to an embodiment of the present disclosure.

DETAILED DESCRIPTION

[0039] The present disclosure may be utilized to secure financial information in payment instruments provided to customers of financial institutions. A financial institution may be, but is not limited to, a bank or other similar entity. The present disclosure may utilize a computer-based system and method that provides financial institution customers access to numerous online banking services offered by online banking service providers based on customer information profiles that may be developed over time. "Online" may mean connecting to or accessing account information from a location remote from the financial institution or a branch of the financial institution. Alternatively, "online" may refer to connecting or accessing an electronic network (wired or wireless) via a computer as described below. In exemplary embodiments, the methods are often web-based.

[0040] The Internet is a worldwide system of computer networks--a network of networks in which a user at one computer or other device connected to the network can obtain information from any other computer and communicate with users of other computers or devices. The most widely used part of the Internet is the World Wide Web (often-abbreviated "WWW" or called "the Web").

[0041] One of the most outstanding features of the Web is its use of hypertext, which is a method for cross-referencing. In most Web sites, certain words or phrases appear in text of a different color than the surrounding text. This text is often also underlined. Sometimes, there are hot spots, such as buttons, images, or portions of images that are "clickable." Clicking on hypertext or a hot spot causes the downloading of another web page via a protocol such as hypertext transport protocol (HTTP). Using the Web provides access to millions of pages of information. Web "surfing" is done with a Web browser, the most popular of which presently are Apple Safari and Microsoft Internet Explorer. The appearance of a particular website may vary slightly depending on the particular browser used. Versions of browsers have "plug-ins," which provide animation, virtual reality, sound, and music. Interpreted programs (e.g., applets) may be run within the browser.

[0042] FIG. 1 shows an online banking access system 150 connected to a plurality of interconnected computer system networks 102 and devices 110. Each computer system network 102 may include a corresponding local computer processor unit 104, which is coupled to a corresponding local data storage unit 106 and to local network user terminals 108. A computer system network 102 may be a local area network (LAN) or part of a wide area network (WAN), for example. The online banking access system 150 and local computer processor units 104 are selectively coupled to a plurality of user devices 110 through Internet 114. Each of the plurality of user devices 110 and local user terminals 108 (collectively, user terminals) may have various devices connected to their local computer systems, such as scanners, barcode readers, printers, fingerprint scanners, mouse devices, keyboards, and other interface devices 112.

[0043] Online banking access system 150 includes a processing unit 152 coupled to one or more data storage units 154, 156. The processing unit 152 provides front-end graphical user interfaces (GUI), e.g., customer GUI 158 and online banking service provider GUI 160, as well as back-end GUIs 162 to a user's terminal 108, 110 or to local computer 164. The GUIs can take the form of, for example, a webpage that is displayed using a browser program local to the user terminal 108, 110, or to local computer 164. It is understood that the online banking access system 150 may be implemented on one or more computers 164, servers 166, or like devices. Front-end and back-end GUIs 158, 160, 162 are preferably portal pages that include various content retrieved from the one or more data storage devices 154, 156. As used herein, "portal" is not limited to general-purpose Internet portals, such as YAHOO! or GOOGLE but also includes GUIs that are of interest to specific, limited audiences and that provide the user access to a plurality of different kinds of related or unrelated information, links and tools as described below. "Webpage" and "website" may be used interchangeably herein.

[0044] A user may gain access to online banking access system 150 by using a user device 108, 110, 164, programmed with a Web browser or other software, to locate and select (such as by clicking with a mouse) a particular webpage. The content of the webpage is located on the one or more data storage devices 154, 156. The user devices 108, 110 may be microprocessor-based computer terminals, pagers that can communicate through the Internet using the Internet Protocol (IP), Kiosks with Internet access, connected personal digital assistants or PDAs (e.g., a PALM device manufactured by Palm, Inc., IPAQ device available from Compaq, iPhone from Apple or Blackberry from RIM), or other devices capable of interactive network communications, such as an electronic personal planner. User devices 108, 110 may also be wireless devices, such as a hand-held unit (e.g., a cellular telephone or a portable music player such as an iPod) that connect to, and communicate through, the Internet using a wireless access protocol (WAP).

[0045] The methods of the present invention may be implemented by utilizing at least a part of the system 150. The functionality of the method may be programmed and executed by at least one computer processor unit 152, with necessary data and graphical interface pages as described below stored in and retrieved from a data storage unit 154, 156. A user can access this functionality using a user device 108, 110. Online banking access system 150 may provide separate features and functionality for front-end users, including customers and online banking service provider users, as well as back-end users that manage the online banking access system 150. As used herein, a "customer" is an individual or organization that signs up for or otherwise takes advantage of an online banking service, and an "online banking service provider" is an individual or organization, such as a financial institution, that provides one or more online banking services to customers. Accordingly, the customers are actual customers of the online banking service providers.

[0046] Referring to FIG. 2, and flow diagram 200, at block 201 a customer may contact a financial institution to request or order a compilation of payment instruments, such as a checkbook, from the financial institution. For example, the checkbook may be a paper checkbook or an electronic checkbook. As can readily be appreciated, the present disclosure is applicable to a number of payment instruments and compilations of payment instruments, and that a check and compilation of a plurality of checks commonly referred to as a checkbook are only an exemplary form of a payment instrument or a compilation of payment instruments that are contemplated by the present invention.

[0047] The customer may order a checkbook by contacting the financial institution through a wide variety of methods including, but not limited to, telephone, mobile telephone, SMS, electronic mail, physical mail or by entering the financial institution's electronic system for online check ordering. The financial institution's electronic system for online check ordering may be a website provided by the financial institution's online banking access system 150 that the customer may access via a public or private network. The customer may enter the website a number of ways (i.e., the customer's entrance into the financial institution's website may be "path sensitive") such as via a public network, via a link from another account the customer may have with the financial institution, via a notice or alert sent to the customer by the financial institution, via an e-mail advertisement sent to the customer by the financial institution, in response to a receipt of a promotional advertisement, etc.

[0048] At block 203, a determination may be made as to whether the customer is an existing client of the financial institution. In one embodiment, a determination may be made as to whether the customer is an existing online client of the financial institution. This determination may be based on information from block 201 or other information provided by the customer or from another source, including records or files possessed by, or stored at, the financial institution, including, but not limited to, at data storage units 154, 156. The determination at block 203 may be made as to whether the customer is an existing offline client of the financial institution or both an online and offline client of the financial institution. An offline client may include the situation where the customer currently does business with the financial institution but not through the financial institution's online system.

[0049] If the customer is an existing online client of the financial institution, then at block 205, the customer enters information (which may sometimes be referred to herein as information for identifying a party or information for identifying a customer) such as, for example, a username and password. This information may typically be entered and transmitted to the financial institution using a computer such as, for example, through customer's terminal 108, 110 or local computer 164. Alternatively, other information may be entered or used in place of a username and password. For example, the information for identifying a customer may include the customer's name, the customer's mailing address, the customer's electronic mailing address, the customer's account number, the customer's social security number, the customer's bank's name, the customer's bank's identification number, the customer's bank's routing transit number, the website login information assigned to the customer by the financial institution or selected by the customer when creating an online account with the financial institution, a digital signature, information stored in a security token such as a soft token, hard token, key fob, or the like, a personal identification number (PIN), source IP address, a session identification, a session start time, a knowledge based authentication (KBA) status or any combination thereof. In one embodiment, since the customer is an existing online client of the financial institution only a limited amount or portion of information need be entered by the customer. In an exemplary embodiment, the information sent between the customer and the financial institution is encrypted using a network security protocol known in the art such as, for example, Secure Socket Layer (SSL) or Transport Layer Security (TLS). If the customer is an existing offline client of the institution, the customer provides identifying information, at block 205, such as, for example, the customer's name, customer's mailing address, the customer's electronic mailing address, the customer's account number, the customer's social security number, the customer's bank's name, the customer's bank identification number, the customer's bank's routing transit number, telephone call-in information assigned to the customer by the financial institution or selected by the customer during account set-up, a call-in password, a call-in PIN, or any combination thereof. In another embodiment, when the customer is an existing offline client of the financial institution, only a limited amount or portion of information need be entered by the customer.

[0050] At block 207, the information provided by the customer at block 205 may be authenticated by any appropriate method known in the art. For example, the information provided by the customer at block 205 may be compared to information stored for the customer in records or files possessed by, or stored at, the financial institution, including, but not limited to, at data storage units 154, 156. If the information provided by the customer at block 205 is not authenticated, the financial institution may inform the customer that the information provided at block 205 is incorrect by any appropriate method known in the art including, for example, by displaying an error message on the customer's computer screen at block 209 and looping the process back to block 205. If the information provided by the customer at block 205 is authenticated, then the financial institution may, at block 211, present to the customer (e.g. by displaying information on a webpage presented to the customer) at, for example, the customer's terminal 108, 110 or local computer 164, information for ordering a compilation of payment instruments. In one embodiment, the financial institution may provide to the customer, at block 211, information for ordering a checkbook by telephone, electronic mail, mobile telephone, SMS, physical mail, or any other correspondence mechanism.

[0051] The information for ordering a checkbook presented to the customer at block 211 may be dynamically presented based at least partially on the information provided by the customer at block 201 or 205 or from another source, including records or files possessed by, or stored at, the financial institution, including, but not limited to, at data storage units 154, 156. For example, the information for ordering the checkbook may include a type of account held by the customer at the financial institution including, but not limited to, a savings account, checking account, money market account, etc. In one embodiment, the information for ordering the checkbook may include the name of the primary account holder, the name of a joint account holder, an account number of a checking, savings, money market or other account, a physical or electronic mailing address of the customer, terms and conditions for ordering the checkbook, etc. The terms and conditions, as is known in the art, typically includes information appropriate for a product to be selected or ordered by a customer, in this case at block 211, and may include information, such as, but not limited to, minimum balance requirements, payment rules, interest rates charged, overdraft charges, late fee applicability, etc. In an embodiment, the information for ordering the checks may include an option for renewal of a previous order or request made by the customer. In another embodiment, the customer may be asked to verify the accuracy of the information presented at block 211 and/or accept terms and conditions presented at block 211 prior to ordering or requesting the checkbook. In a further embodiment, the customer may perform edits to the information presented at block 211 to ensure accuracy. In another embodiment, the information for ordering the checkbook may include a link to a third party provider site, including but not limited to, a check provider or check printing service provider. At block 213, the customer makes a selection from the information for ordering the checkbook provided or presented at block 211 and orders or requests the checkbook.

[0052] Upon receipt of the request or order from the customer, at block 215, an activation code is generated by the financial institution. As used herein, an activation code is a random or pseudorandom code generated by any appropriate method known in the art, including at least one or more of a number, letter or symbol, or combination thereof, and that is unique to the checkbook ordered or requested by the customer at block 213. In one embodiment of the invention, computer processing unit 152 may be programmed to execute an activation code generating algorithm that returns a sequence of apparently non-related numbers, letters, symbols or combinations thereof each time the program is called. For example, an activation code for a requested checkbook may be generated as "e429ab." In an alternate embodiment, the activation code may be generated by a third party check provider or check printing service provider.

[0053] Referring to FIG. 3, computer processing unit 152 may be configured to implement the algorithms associated with the present disclosure by including one or more processors 302. The processor 302 is connected to a communication infrastructure 306 (e.g., a communications bus, cross-over bar, or network). Computer processing unit 152 may include a display interface 422 that forwards graphics, text, and other data from the communication infrastructure 406 (or from a frame buffer not shown) for display on the front- and back-end GUIs 158, 160, 162 and as retrieved from the one or more data storage devices 154, 156.

[0054] Computer processing unit 152 may also include a main memory 304, such as a random access memory (RAM), and a secondary memory 308. The secondary memory 308 may include, for example, a hard disk drive (HDD) 310 and/or removable storage drive 312, which may represent a floppy disk drive, a magnetic tape drive, an optical disk drive, or the like. The removable storage drive 312 reads from and/or writes to a removable storage unit 316. Removable storage unit 316 may be a floppy disk, magnetic tape, optical disk, or the like. In some instances, the removable storage unit 316 may include a computer readable storage medium having stored therein computer software and/or data. In alternative embodiments, secondary memory 308 may include other similar devices for allowing computer programs or other instructions to be loaded into computer processing unit 152. Secondary memory 308 may include a removable storage unit 318 and a corresponding interface 314. Examples of such removable storage units include, but are not limited to, USB or flash drives, which allow software and data to be transferred from the removable storage unit 318 to computer processing unit 152.

[0055] Computer processing unit 152 may also include a communications interface 320. Communications interface 320 allows software and data to be transferred between computer processing unit 152 and external devices. Examples of communications interface 320 may include a modem, Ethernet card, wireless network card, a Personal Computer Memory Card International Association (PCMCIA) slot and card, or the like. Software and data transferred via communications interface 320 may be in the form of signals, which may be electronic, electromagnetic, optical, or the like that are capable of being received by communications interface 320. These signals may be provided to communications interface 320 via a communications path (e.g., channel), which may be implemented using wire, cable, fiber optics, a telephone line, a cellular link, a radio frequency (RF) link and other communication channels.

[0056] In connection with many of the methods of the present invention, the terms "computer program medium" and "computer readable storage medium" refer to media such as removable storage drive 312, or a hard disk installed in hard disk drive 310. These computer program products may provide software to computer processing unit 152. Computer programs (also referred to as computer control logic) are stored in main memory 304, secondary memory 308 and/or data storage devices 154, 156. Computer programs may also be received via communications interface 320. Such computer programs, when executed by a processor, enable the computer processing unit 152 to perform features of the methods discussed herein. For example, main memory 304, secondary memory 308, data storage devices 154, 156 or removable storage units 316 or 318 may be encoded with computer program code for performing the activation code algorithm.

[0057] In an embodiment implemented using software, the software may be stored in a computer program product and loaded into computer processing unit 152 using removable storage drive 312, hard drive 310, or communications interface 320. The software, when executed by a processor 302, causes the processor 302 to perform the functions of the activation code algorithm described herein. In another embodiment, the activation code algorithm may be implemented primarily in hardware using, for example, hardware components such as a digital signal processor comprising application specific integrated circuits (ASICs). In yet another embodiment, the activation code algorithm is implemented using a combination of both hardware and software.

[0058] As discussed above, at block 215, the financial institution may generate an activation code by any appropriate method known or used in the art. For example, it is well-known in the art to program and execute a standard C RAND or RANDS function, or the PHP hypertext preprocessor functions microtime or mt rand, or the Unix function /dev/random, or the Java function SecureRandom, to return a pseudorandom number or alphanumeric sequence within a specified range. It is understood that a pseudorandom number or alphanumeric sequence generator should produce a pseudorandom sequence with a period that is long enough so that a finite sequence of reasonable length is not periodic. It is also well known that all pseudorandom number or alphanumeric sequence generators have an internal memory or state and that the size of the state is the value that determines the strength of the pseudorandom number or alphanumeric sequence generator, where an n-bit state can produce at most 2n different values. The strength, or ability of the pseudorandom sequence generator to resist a brute force attack by a cryptanalyst, of the output of the pseudorandom number or alphanumeric sequence generator is also commonly associated with the information entropy of the process that produced the pseudorandom sequence. This information entropy (H) is conventionally measured in bits and is commonly calculated as: H=L log.sub.2 N where L is the number of letters, numbers or symbols in the sequence and N is the number of possible letters, numbers or symbols. See, e.g. National Institute of Standards and Technology Special Publication 800-63, Electronic Authentication Guideline, Appendix A; Bruce Schneier, Applied Cryptography, John Wiley & Sons, 1996, Chapter 11, Mathematical Background, p. 233-237. For example, in a pseudorandom alphanumeric sequence, where each alphanumeric character in the sequence is produced independently, and where the number of possible letters, numbers or symbols includes all letters in the Latin alphabet from a-z (26), A-Z (26) and all Arabic numerals from 0-9 (10), the entropy per symbol would be calculated as H=log.sub.2 N or log.sub.2 (52) or 5.70 bits per symbol. It is well known in the art to select L and N based on a desired information entropy, thus, one skilled in the art would understand to select those values for the activation code based on a desired information entropy.

[0059] It is also understood that to be cryptographically secure, a pseudorandom sequence must be unpredictable where a secret key, or seed, is used to set the initial state of the pseudorandom sequence generator. Key management of the secret key or seed may be implemented by the financial institution in any method known in the art and should be at least in compliance with the financial industry standards set forth by the Accredited Standards Committee X9. In addition to employing a secret key, there are a wide variety of known methods to generate the seed for pseudorandom sequence generation. For example, the standard C function RAND may be seeded using the time function, although time of day is often not used as a seed due to its susceptibility to cryptographic attacks. Additionally, by way of example, Open SSL may use the function RAND_screen( ) to hash the contents of the screen to generate a seed. Further by way of example, the Linux random number generator may collect data from a variety of sources, including mouse, keyboard and other interrupts to seed a random number generator. Furthermore, it is well known in the art to combine the seed and a counter output and hash the output with a one-way hashing functions such as MD5 or SHA-1 to generate a cryptographically secure pseudorandom sequence.

[0060] In an embodiment, at block 215, a third party check provider or check printing service provider may generate an activation code for the customer requested checkbook at block 213. It is understood that the financial institution and third party check provider or check printing service provider should use identical activation code algorithms, identical pseudorandom sequence generators in synchronism and an identical initiating seed previously supplied in advance of the activation code generation. In one embodiment, the activation codes generated by the financial institution and third party check provider or check printing service provider may be verified by any secure communication method known in the art including secure communication methods employing asymmetric or symmetric encryption techniques, message authentication codes, secure hashing algorithms, and/or, as discussed above, a combination thereof using, for example, a network security protocol known in the art such as SSL or TLS where the information sent between the financial institution and third party check provider or check printing service provider is encrypted. In an alternate embodiment, a third party check provider or check printing service provider may generate the activation code for the customer requested checkbook at block 213.

[0061] FIG. 4 illustrates a flow chart illustrating a method for securing payment instruments according to an embodiment of the present invention. In the present embodiment and as discussed above, the customer may order or request a checkbook at block 213. Upon receipt of the request or order from the customer, at block 215, an activation code is generated by the financial institution using any appropriate method known or used in the art. As discussed above, in an alternate embodiment, the activation code, or an identical activation code, may be generated by a third party check provider or check printing service provider. At block 417, in embodiments including a compilation of paper payment instruments, such as a paper checkbook, each of the plurality of paper checks in the checkbook is printed, assembled and united into a booklet form by the financial institution, third party check provider or third party check printing service provider as requested by the customer at block 213. In embodiments including a compilation of electronic financial instruments, such as an electronic checkbook, each of the plurality of electronic checks is created, electronically assembled and electronically united into an electronic checkbook file by the financial institution or third party check provider at block 417, as requested by the customer at block 213.

[0062] In an embodiment, at block 419, the activation code is issued to an address of the customer stored or possessed by the financial institution at, for example, records or files at data storage units 154, 156. The address of the customer may include, but is not limited to, a physical mailing address or electronic mailing address. In one embodiment, the customer may be requested to verify the physical mailing address or electronic mailing address that is stored or possessed by the financial institution prior to requesting or ordering a checkbook at block 213. In an exemplary embodiment using a paper checkbook, at block 419, the activation code may be mailed, with the printed checkbook that was ordered by the customer at block 213, to an address of the customer stored by the financial institution, a third party check provider, or a third party check printing service provider. The activation code may be printed on a card or a sticker with instructions to the customer such as, for example, "Use the below code to activate your checkbook". The card or sticker may also include instructions for contacting the financial institution to activate the checkbook including, but not limited to, a website address, secure electronic mailing address, or telephone number, and may also include instructions for activating the checkbook once contact has been established with the financial institution.

[0063] At block 421, the activation code generated for the customer's checkbook at block 215 is associated with at least a portion of the standard indicia, for example, the traditional check sequence number, for each of the plurality of checks in the checkbook ordered by the customer at block 213. With reference to FIG. 5, standard indicia on a conventional paper check 500 include a customer name 502, a customer address 504, a customer account number 506 printed on the check in traditional Magnetic Ink Character Recognition (MICR) format, and a check sequence number 508. As discussed above, the generated activation code is unique to the plurality of checks in the checkbook ordered by the customer at block 213. In one embodiment, at block 421, the activation code is associated with the traditional check sequence number for each of the plurality of checks in the customer's checkbook ordered by the customer at block 213. At block 421, the activation code generated for the customer's checkbook at block 215 may be associated with identifying information for the customer. The identifying information for the customer may be stored in records or files possessed by, or stored at, the financial institution, including, but not limited to, at data storage units 154, 156. In another embodiment, the customer's identifying information may be stored in records or files possessed by, or stored at, a third party check provider or third party check printing service provider.

[0064] The stored customer identifying information may be based upon whether the customer is an existing offline customer or existing online customer of the financial institution. Customer identifying information may include, but is not limited to, a username, a password, the customer's name, the customer's mailing address, the customer's electronic mailing address, the customer's account number, the customer's social security number, the customer's bank's name, the customer's bank's identification number, the customer's bank's routing transit number, the website login information assigned to the customer by the financial institution or selected by the customer when creating an online account with the financial institution, a digital signature, information stored in a security token such as a soft token, hard token, key fob, or the like, a personal identification number (PIN), source IP address, a session identification, a session start time, a knowledge based authentication (KBA) status, telephone call-in information assigned to the customer by the financial institution or selected by the customer during account set-up, a call-in password, a call-in PIN, or any combination thereof.

[0065] At block 423, the generated activation code may be stored in the appropriate customer's records or files possessed by, or stored at, the financial institution, including, but not limited to, at data storage units 154, 156 with at least a portion of the customer identifying information and at least a portion of the standard indicia, for example, the traditional check sequence number, for each of the plurality of checks in the checkbook ordered by the customer at block 213. In another embodiment, at block 423, the activation code, at least a portion of the customer identifying information and at least a portion of the standard indicia, for example, the traditional check sequence number, for each of the plurality of checks in the checkbook ordered by the customer at block 213, may be stored in the appropriate customer's records or files possessed by, or stored at, a third party check provider or third party check printing service provider.

[0066] With reference to FIG. 6, the customer may order or request a checkbook at block 213. Upon receipt of the request or order from the customer, at block 215, an activation code may be generated by the financial institution using any appropriate method known or used in the art. As discussed above, in an alternate embodiment, the activation code, or an identical activation code, may be generated by a third party check provider or check printing service provider. In the present embodiment, at block 617, and upon receipt of the request or order from the customer at block 215, a pseudorandom check code sequence is generated by the financial institution. Each check code in the pseudorandom check code sequence includes at least one or more of a number, letter or symbol, or combination thereof, that is unique to each check of the plurality of checks in the checkbook ordered by the customer at block 213. The pseudorandom check code sequence may be generated by any appropriate method known in the art. For example, a pseudorandom check code of the pseudorandom check code sequence for a requested checkbook may be generated as "34", "3216", "183", "9", "6543", "74a5", or "37ps2". In a preferred embodiment, the pseudorandom check code sequence is generated by a pseudorandom number generator (PRNG) and includes a sequence of pseudorandom codes of variable length numeric values. In an embodiment, at least a portion of a pseudorandom check code of the generated pseudorandom check code sequence may include the activation code. In another embodiment, computer processing unit 152 may also be programmed to execute a pseudorandom check code sequence generating algorithm that returns a sequence of pseudorandom line check codes each time the program is called. In a preferred embodiment, the computer processing unit 152 may also be programmed to execute a pseudorandom check code sequence generating algorithm that returns a sequence of pseudorandom check codes each time the program is called. In an alternate embodiment, the pseudorandom check code sequence may be generated by a third party check provider or check printing service provider.

[0067] In embodiments implemented using software, the software may be stored in a computer program product and loaded into computer processing unit 152 using removable storage drive 312, hard drive 310, or communications interface 320. The software, when executed by a processor 302, causes the processor 302 to perform the functions of the pseudorandom check code sequence algorithm. In another embodiment, the pseudorandom check code sequence algorithm may be implemented primarily in hardware using, for example, hardware components such as a digital signal processor comprising application specific integrated circuits (ASICs). In yet another embodiment, the pseudorandom check code sequence algorithm is implemented using a combination of both hardware and software.

[0068] At block 617, the financial institution may generate a pseudorandom check code sequence by any appropriate method known or used in the art. It is understood that a pseudorandom check code sequence algorithm should produce a pseudorandom check code sequence with a period that is long enough so that a finite sequence of reasonable length is not periodic, and where each unique pseudorandom check code is not repeated within the same checkbook so that customers can easily reconcile their checks with the financial institution. In a preferred embodiment, the generated pseudorandom check code sequence is cryptographically secure. In an embodiment, at block 617, a third party check provider or check printing service provider may generate an identical pseudorandom check code sequence for the customer requested checkbook at block 213. It is understood that the financial institution and third party check provider or check printing service provider should use identical pseudorandom check code sequence generating algorithms, identical pseudorandom sequence generators in synchronism and an identical seed previously supplied in advance of the pseudorandom check code sequence generation. In an embodiment, the pseudorandom check code sequences generated by the financial institution and third party check provider or check printing service provider may be verified by any secure communication method known in the art including secure communication methods employing asymmetric or symmetric encryption techniques, message authentication codes, secure hashing algorithms, and/or, as discussed above, a combination thereof using, for example, a network security protocol known in the art such as SSL or TLS where the information sent between the financial institution and third party check provider or check printing service provider is encrypted.

[0069] At block 619, a unique pseudorandom check code of the generated pseudorandom check code sequence is associated with each of the checks of the plurality of checks in the checkbook by the financial institution, third party check provider or third party check printing service provider. At block 621, in embodiments including a compilation of paper financial instruments, such as a paper checkbook, each of the plurality of paper checks, including the associated unique pseudorandom check code of the generated pseudorandom check code sequence, in the checkbook is printed, assembled and united into a booklet form by the financial institution, third party check provider or third party check printing service provider as requested by the customer at block 213. In embodiments including a compilation of electronic financial instruments, such as an electronic checkbook, each of the plurality of electronic checks, including the associated unique pseudorandom check code of the generated pseudorandom check code sequence, in the checkbook, is created, electronically assembled and electronically united into an electronic checkbook file by the financial institution, third party check provider or third party check printing service provider at block 621, as requested by the customer at block 213.

[0070] With reference to FIG. 7, a check including a unique pseudorandom check code 708 also includes a customer name 702, a customer address 704, a customer account number 706 printed on the check in traditional Magnetic Ink Character Recognition (MICR) format, and a check sequence number 708. The check sequence number 708 may be included on the check for the convenience of the customer such as for use in balancing the customer's checkbook. Unique pseudorandom check code 710 is illustrated as a MICR line check number printed adjacent to customer account number 706. However, one skilled in the art would understand that unique pseudorandom check code 710, as illustrated, represents only an exemplary form of a unique pseudorandom check code that is contemplated by the present disclosure.

[0071] Returning to FIG. 6, at block 623, the activation code generated at block 215 is issued to an address of the customer stored or possessed by the financial institution at, for example, records or files at data storage units 154, 156. The address of the customer may include, but is not limited to, a physical mailing address or electronic mailing address. In an embodiment, the customer may be requested to verify the physical mailing address or electronic mailing address that is stored or possessed by the financial institution prior to requesting or ordering a checkbook at block 213. In an exemplary embodiment using a paper checkbook, the activation code may be mailed to an address of the customer stored by the financial institution, third party check provider or third party check printing service provider with the printed checkbook that was ordered by the customer at block 213 and assembled by the financial institution, third party check provider or third party check printing service provider at block 621. The activation code may be printed on a card or a sticker with instructions to the customer such as, for example, "Use the below code to activate your checkbook". The card or sticker may also include instructions for contacting the financial institution to activate the checkbook including, but not limited to, a website address, secure electronic mailing address, or telephone number, and instructions for activating the checkbook once contact has been established with the financial institution.

[0072] At block 625, the activation code generated for the customer's checkbook at block 215 is associated with each of the unique pseudorandom check codes of the generated pseudorandom sequence associated with each of the plurality of checks in the checkbook at block 619. The generated activation code is unique to the plurality of checks in the checkbook ordered by the customer at block 213. At block 625, the activation code generated for the customer's checkbook at block 215 may be associated with identifying information for the customer. The identifying information for the customer may be stored in records or files possessed by, or stored at, the financial institution, including, but not limited to, at data storage units 154, 156. In another embodiment, the customer's identifying information may be stored in records or files possessed by, or stored at, a third party check provider or third party check printing service provider. At block 627, the generated activation code may be stored in the appropriate customer's records or files possessed by, or stored at, the financial institution. with at least a portion of the customer identifying information and each of the unique pseudorandom check codes of the generated pseudorandom sequence associated with each of the plurality of checks in the checkbook at block 619. In another embodiment, at block 423, the activation code, customer identifying information, and each of the unique pseudorandom check codes of the generated pseudorandom sequence associated with each of the plurality of checks in the checkbook at block 619 may be stored in the appropriate customer's records or files possessed by, or stored at, a third party check provider.

[0073] Referring to FIG. 8, in order to activate a compilation of payment instruments according to an embodiment of the present invention, at block 801 a customer may contact a financial institution to activate a compilation of payment instruments, such as a checkbook, that may have been issued to the customer by the financial institution, third party check provider or third party check printing service provider. In an embodiment, an activation code unique to a checkbook is issued by a financial institution, third party check provider or third party check printing service provider and received by the customer with the corresponding checkbook. In an alternate embodiment, a customer may contact a financial institution to activate a checkbook after receiving an activation code unique to an electronic checkbook. One skilled in the art will recognize that the customer may activate a checkbook by contacting the financial institution through a wide variety of methods including, but not limited to, telephone, electronic mail, mobile telephone, SMS, physical mail or by entering the financial institution's electronic system for online checkbook activation. The financial institution's electronic system for online checkbook activation may be a website provided by the financial institution's online banking access system 150 that the customer may access via a public or private network. The customer may enter the website a number of ways (i.e., the customer's entrance into the financial institution's website may be "path sensitive," which may have implications) such as via a public network, via a link from another account the customer may have with the financial institution, via a notice or alert sent to the customer by the financial institution, via an email advertisement sent to the customer by the financial institution, in response to a receipt of a promotional advertisement, etc.

[0074] At block 803, a determination may be made as to whether the customer is an existing client of the financial institution. In an embodiment, a determination may be made as to whether the customer is an existing online client of the financial institution. This determination may be based on information from block 801 or other information provided by the customer or from another source, including records or files possessed by, or stored at, the financial institution, including, but not limited to, at data storage units 154, 156. In an embodiment, the determination at block 803 may be made as to whether the customer is an existing offline client of the financial institution or both an online and offline client of the financial institution. If the customer is an existing online client of the financial institution, then at block 805, the customer enters and transmits information for identifying the customer, such as, for example, a username and password. This information may typically be entered and transmitted to the financial institution using a computer such as, for example, through customer's terminal 108, 110 or local computer 164. Alternatively, other information for identifying the customer may be entered or used in place of a username and password. In one embodiment, since the customer is an existing online client of the financial institution, only a limited amount or portion of information need be entered by the customer. In an exemplary embodiment, the information sent between the customer and the financial institution is encrypted using a network security protocol known in the art such as, for example, Secure Socket Layer (SSL) or Transport Layer Security (TLS). If the customer is an existing offline client of the institution, the customer provides or transmits information for identifying the customer, at block 805, such as, for example, the customer's name, customer's mailing address, the customer's electronic mailing address, the customer's account number, the customer's social security number, the customer's bank's name, the customer's bank identification number, the customer's bank's routing transit number, telephone call-in information assigned to the customer by the financial institution or selected by the customer during account set-up, a call-in password, a call-in PIN, or any combination thereof. In an embodiment, since the customer is an existing offline client of the financial institution, only a limited amount or portion of information need be transmitted by the customer to the financial institution.