Short-term Certificate

JANGAMA; Suman Rao ; et al.

U.S. patent application number 16/718039 was filed with the patent office on 2020-06-18 for short-term certificate. This patent application is currently assigned to Comenity LLC. The applicant listed for this patent is Comenity LLC. Invention is credited to Suman Rao JANGAMA, Steinn JONSSON, Jess LAWRENCE, Gabriel ROSTORFER, Bipin SADHWANI, Vinayak SWAMINATHAN, Manoj Ram TAMMINA.

| Application Number | 20200193413 16/718039 |

| Document ID | / |

| Family ID | 71072694 |

| Filed Date | 2020-06-18 |

| United States Patent Application | 20200193413 |

| Kind Code | A1 |

| JANGAMA; Suman Rao ; et al. | June 18, 2020 |

SHORT-TERM CERTIFICATE

Abstract

A short-term certificate is disclosed. The method receives a request for a short-term certificate to be generated from a credit account of a first party and provided to a second party, the request includes an amount allocated to the short-term certificate and an identifier for the second party. A part of the credit account is allocated to cover the value of the short-term certificate. The short-term certificate is generated and provided to the second party. However, no funds are taken from the credit account of the first party until the short-term certificate is redeemed.

| Inventors: | JANGAMA; Suman Rao; (Delaware, OH) ; JONSSON; Steinn; (Columbus, OH) ; LAWRENCE; Jess; (Lewis Center, OH) ; ROSTORFER; Gabriel; (Columbus, OH) ; SADHWANI; Bipin; (Lewis Center, OH) ; SWAMINATHAN; Vinayak; (Dublin, OH) ; TAMMINA; Manoj Ram; (Columbus, OH) | ||||||||||

| Applicant: |

|

||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Assignee: | Comenity LLC Columbus OH |

||||||||||

| Family ID: | 71072694 | ||||||||||

| Appl. No.: | 16/718039 | ||||||||||

| Filed: | December 17, 2019 |

Related U.S. Patent Documents

| Application Number | Filing Date | Patent Number | ||

|---|---|---|---|---|

| 62780867 | Dec 17, 2018 | |||

| Current U.S. Class: | 1/1 |

| Current CPC Class: | G06Q 20/3437 20130101; G06Q 20/3255 20130101; G06Q 20/354 20130101; G06Q 20/348 20130101; G06Q 20/3226 20130101; G06Q 40/02 20130101; G06Q 20/28 20130101; G06Q 20/342 20130101; G06Q 20/322 20130101; G06Q 20/36 20130101; G06Q 20/385 20130101 |

| International Class: | G06Q 20/34 20060101 G06Q020/34; G06Q 20/28 20060101 G06Q020/28; G06Q 20/32 20060101 G06Q020/32 |

Claims

1. A method for providing a short-term certificate from a first party to a second party, the method comprising: receiving, at a credit account management system, a request for a short-term certificate to be provided from a credit account of the first party to the second party, the request comprising: a value of the short-term certificate, and an identifier for the second party; allocating a part of the credit account to cover the value of the short-term certificate; generating the short-term certificate; and providing, from the credit account management system and to the second party, the short-term certificate, wherein no funds are taken from the credit account of the first party until the short-term certificate is redeemed.

2. The method of claim 1, where the identifier of the second party is a physical mail address and the short-term certificate is sent to the physical mail address of the second party.

3. The method of claim 1, where the short-term certificate is provided to the second party in a digital format.

4. The method of claim 3, where the short-term certificate is automatically added to a digital wallet on a mobile device of the second party, when the short-term certificate is received at the mobile device of the second party.

5. The method of claim 3, where the identifier of the second party is an email address and the short-term certificate is sent to the email address of the second party.

6. The method of claim 3, where the identifier of the second party is a mobile phone number and the short-term certificate is sent via an SMS to a mobile device of the second party.

7. The method of claim 1 further comprising: providing an indicator to the first party when the short-term certificate is used to make a purchase, the indicator comprising: an amount of money spent; and a location where the short-term certificate was redeemed.

8. The method of claim 1 further comprising: providing a reminder to the second party, the reminder provided after a pre-defined amount of time, the reminder indicating that the short-term certificate is still active.

9. The method of claim 1 further comprising: providing an expiration date with the short-term certificate; and deactivating the short-term certificate after a passing of the expiration date.

10. The method of claim 9 further comprising: providing an expiration reminder to the second party, the expiration reminder provided a pre-defined amount of time before the expiration date of the short-term certificate; and the expiration reminder indicating that the short-term certificate is still valid.

11. The method of claim 1 further comprising: wherein the short-term certificate is a single use certificate.

12. A non-transitory computer-readable medium for storing instructions, the instructions comprising: one or more instructions which, when executed by one or more processors, cause one or more processors to: receive, at a credit account management system, a request for a short-term certificate to be provided from a credit account of a first party to a second party, the request comprising: a value of the short-term certificate, and an identifier for the second party; allocate a part of the credit account to cover the value of the short-term certificate; generate the short-term certificate; and provide, from the credit account management system and to the second party, the short-term certificate, wherein no funds are taken from the credit account of the first party until the short-term certificate is redeemed.

13. The non-transitory computer-readable medium of claim 12, where the short-term certificate is digital.

14. The non-transitory computer-readable medium of claim 12, where the one or more instructions further cause the one or more processors to: automatically add the short-term certificate to a digital wallet on a mobile device of the second party, when the short-term certificate is received at the mobile device of the second party.

15. The non-transitory computer-readable medium of claim 12, where the one or more instructions further cause the one or more processors to: provide an indicator to the first party when the short-term certificate is used to make a purchase, the indicator comprising: an amount of money spent, and a location where the short-term certificate was redeemed.

16. The non-transitory computer-readable medium of claim 12, where the one or more instructions further cause the one or more processors to: provide an expiration date with the short-term certificate; and deactivate the short-term certificate on the expiration date.

17. The non-transitory computer-readable medium of claim 16, where the one or more instructions further cause the one or more processors to: provide an expiration reminder to the second party, the expiration reminder provided a pre-defined amount of time before the expiration date of the short-term certificate; and the expiration reminder indicating that the short-term certificate is still active.

18. The non-transitory computer-readable medium of claim 12, wherein the short-term certificate is a single use certificate.

19. A system comprising: a memory; a storage; and one or more processors to: receive, at a credit account management system, a request for a single use short-term certificate to be provided from a credit account of a first party to a second party, the request comprising: a value of the single use short-term certificate, and an identifier for the second party; allocate a part of the credit account to cover the value of the single use short-term certificate; generate the single use short-term certificate; provide an expiration date for the single use short-term certificate; provide, from the credit account management system and to the second party, the single use short-term certificate, wherein no funds are taken from the credit account of the first party until the single use short-term certificate is redeemed; and provide an indicator to the first party when the single use short-term certificate is redeemed, the indicator comprising: an amount of money spent, and a location where the single use short-term certificate was redeemed.

20. The system of claim 19 wherein the request for the single use short-term certificate to be generated from the credit account of the first party and provided to the second party is received at an application of the credit account operating on a first party's mobile device; and wherein the single use short-term certificate is provided to another application of the credit account operating on a second party's mobile device.

Description

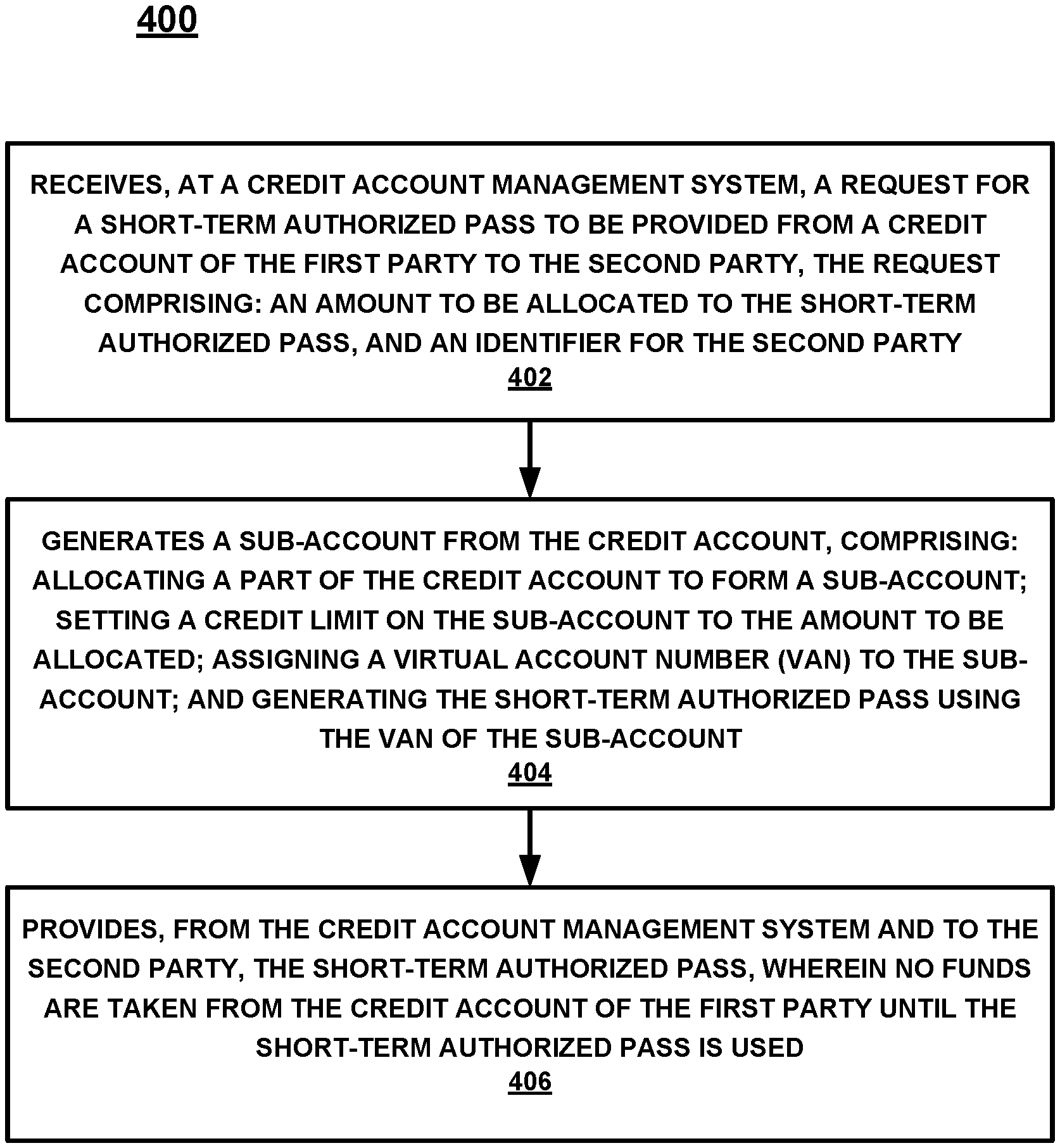

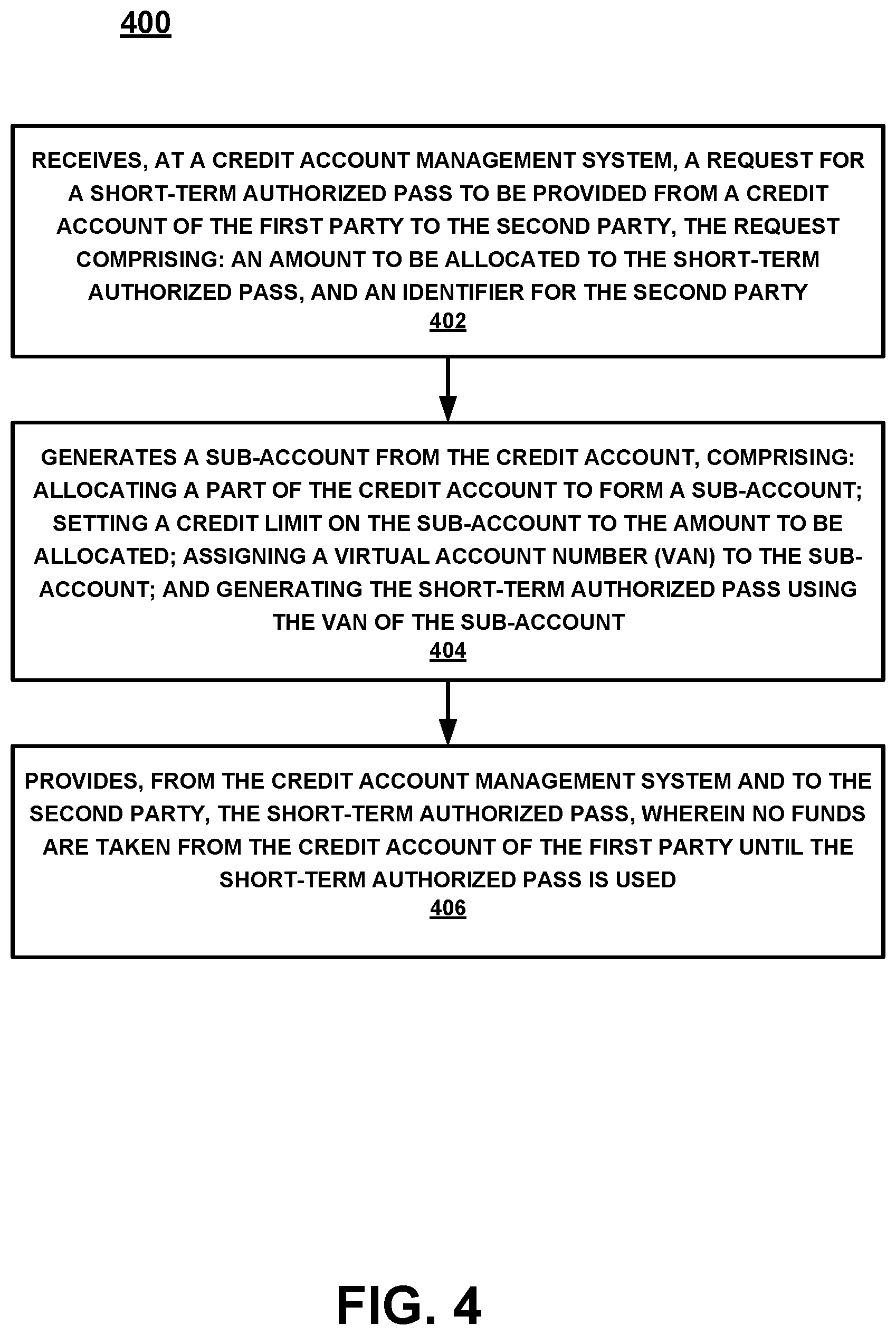

CROSS-REFERENCE TO RELATED APPLICATIONS (PROVISIONAL)

[0001] This application claims priority to and benefit of co-pending U.S. Provisional Patent Application No. 62/780,867 filed on Dec. 17, 2018, entitled "A SHORT-TERM AUTHORIZED PASS" by Lawrence et al., and assigned to the assignee of the present application, the disclosure of which is hereby incorporated by reference in its entirety.

BACKGROUND

[0002] Company specific, brand specific and even store specific gift card programs make nice gift ideas. By issuing gift cards, the provider is able to direct customer spending. Similarly, the giver of the gift card can provide the gift card to a recipient thereby showing the recipient that a thoughtful attempt was made by the giver, instead of the giver merely putting cash in a card. However, once a gift card is purchased, the money is spent by the giver, regardless of whether or not the gift card is redeemed. Moreover, unredeemed money from lost, or not completely used gift cards will deleteriously remain as outstanding liability on the gift card company's books.

BRIEF DESCRIPTION OF THE DRAWINGS

[0003] The accompanying drawings, which are incorporated in and form a part of this specification, illustrate various embodiments and, together with the Description of Embodiments, serve to explain principles discussed below. The drawings referred to in this brief description should not be understood as being drawn to scale unless specifically noted.

[0004] FIG. 1 is a block diagram of a mobile device, in accordance with an embodiment.

[0005] FIG. 2 is a block diagram of a credit account management system to generate a short-term authorized pass, in accordance with an embodiment.

[0006] FIG. 3 is a block diagram of a short-term authorized pass as presented on a display screen of a mobile device, in accordance with an embodiment.

[0007] FIG. 4 is a flowchart of a method for obtaining a short-term authorized pass, in accordance with an embodiment.

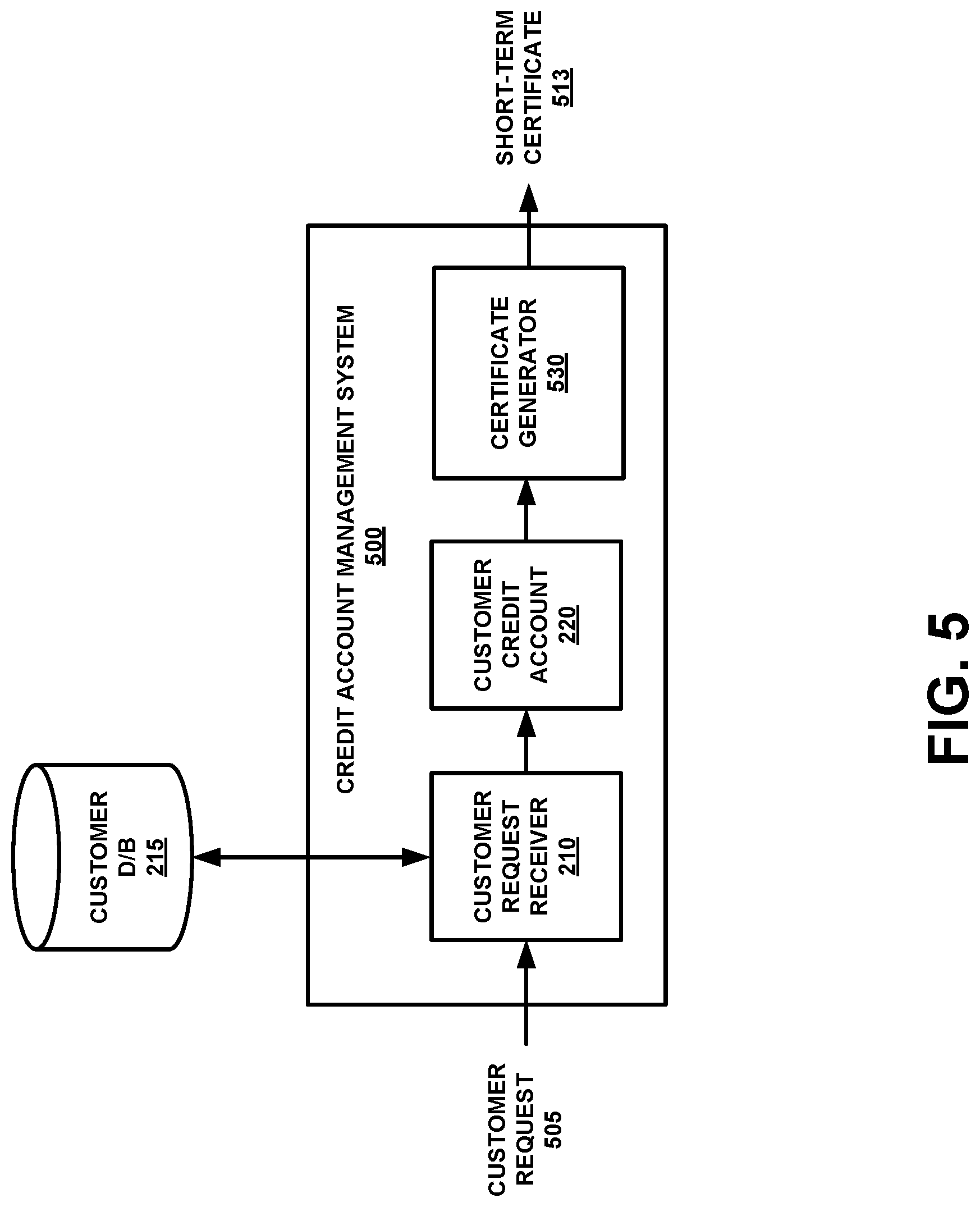

[0008] FIG. 5 is a block diagram of a credit account management system to generate a short-term certificate, in accordance with an embodiment.

[0009] FIG. 6 is a block diagram of a short-term certificate, in accordance with an embodiment.

[0010] FIG. 7 is a flowchart of a method for obtaining a short-term certificate, in accordance with an embodiment.

[0011] FIG. 8 is a block diagram of an example computer system with which or upon which various embodiments of the present invention may be implemented.

DESCRIPTION OF EMBODIMENTS

[0012] Reference will now be made in detail to various embodiments, examples of which are illustrated in the accompanying drawings. While the subject matter will be described in conjunction with these embodiments, it will be understood that they are not intended to limit the subject matter to these embodiments. On the contrary, the subject matter described herein is intended to cover alternatives, modifications and equivalents, which may be included within the spirit and scope as defined by the appended claims. In some embodiments, all or portions of the electronic computing devices, units, and components described herein are implemented in hardware, a combination of hardware and firmware, a combination of hardware and computer-executable instructions, or the like. In one embodiment, the computer-executable instructions are stored in a non-transitory computer-readable storage medium. Furthermore, in the following description, numerous specific details are set forth in order to provide a thorough understanding of the subject matter. However, some embodiments may be practiced without these specific details. In other instances, well-known methods, procedures, objects, and circuits have not been described in detail as not to unnecessarily obscure aspects of the subject matter.

Notation and Nomenclature

[0013] Unless specifically stated otherwise as apparent from the following discussions, it is appreciated that throughout the present Description of Embodiments, discussions utilizing terms such as "selecting", "outputting", "allowing," "limiting," "issuing," "preventing," "inputting", "providing", "receiving", "utilizing", "obtaining", "performing", "accessing", "authorizing" or the like, often refer to the actions and processes of an electronic computing device/system, such as a desktop computer, notebook computer, tablet, mobile phone, and electronic personal display, among others. The electronic computing device/system manipulates and transforms data represented as physical (electronic) quantities within the circuits, electronic registers, memories, logic, and/or components and the like of the electronic computing device/system into other data similarly represented as physical quantities within the electronic computing device/system or other electronic computing devices/systems.

[0014] It should be appreciated that the obtaining, accessing, or utilizing of information conforms to applicable privacy laws (e.g., federal privacy laws, state privacy laws, etc.).

[0015] A brand specific credit account refers to a credit account that is available for use only at locations related to the brand. E.g., Mike's store has a brand specific credit account that allows Marsha, a Mike's store customer, to purchase with credit at Mike's store using Mike's brand specific credit account. However, Marsha cannot use the Mike's brand specific credit account to make purchases at her local gas station. A brand specific credit account may also be referred to as a private label card, e.g., a card that can be used for purchases only at the store on the label.

[0016] A co-branded card refers to a card that has a store on the label as well as an underlying credit card network with an accompanying logo (e.g., Visa.TM., Mastercard.TM., etc.). As such, a co-branded card may be used for purchases at the store on the label as well as at other stores that accept that credit card network's credit cards.

[0017] It is well known that gift card redemption rates hover around 60%. This redemption level is a shortcoming to the giver of the gift card, the recipient of the gift card, and the company backing the gift card. For example, with respect to the giver, once the gift card is given there is no way for the giver to track (or follow) or otherwise ensure that the gift card was used, that it was not lost, forgotten, etc. Basically, after giving a gift card the giver has paid the gift card amount e.g., $50 and is left in the dark as to whether or not the gift card is ever used.

[0018] With respect to the recipient, if the recipient loses the gift card they are likely looking at a complete loss. In the recipient redeems only a portion of the gift card, they are left with a gift card having a remaining small amount of money they did not spend. Depending, upon the consumer, they could throw away the gift card with the minimal amount left on it, put the gift card to the side in a drawer for later use, lose the card, etc.

[0019] With respect to the company backing the gift card, if the gift card is not redeemed in full then, as stated above, the outstanding liability remains the company's books. Depending upon the guiding laws, this liability will need to be tracked, and accounted for, by the bookkeeper until it is deemed expired, or until the end of time if no expiration is allowed. Moreover, while some gift cards will promote the underlying company, by causing additional monies to be spent at the company, it is just as likely that the loss of a gift card combined with the company's inability to replace the lost gift card will cause animosity between the purchaser, the recipient, and the company.

[0020] For example, if the gift card recipient loses a $100 gift card for "Sporting goods by Bob" (Bob) when the customer contacts "Bob" and tells "Bob" about the loss, "Bob" will have a very limited solution. That is, since the gift card is likely active and still redeemable, "Bob" is put in a position of rejecting the customer, providing a reduced amount to the customer, or providing a replacement gift card with could result in a $100 loss for "Bob". Each of these solutions, can easily cause ill will. For example, if the gift card recipient indicates to the gift card giver that "Bob" is not doing anything about the lost gift card, the giver (e.g., the gift card purchaser) will also feel cheated because they spent the have already spent the money to purchase the gift card and now their money is lost. Moreover, it may even be spent by someone other than the intended recipient.

[0021] In such a case, hurt feelings and bad publicity are likely to occur. In addition, because of Internet reviews, such as company reviews, customer reviews, and the like. These types of gift card problems could cause a bad review that could include deleterious comments about the brand, a lowering of the brand's ranking, a reduction in the number of stars for the brand, and the like. Thus, while gift cards can be a valuable source of focused customer spending, they can also be significantly detrimental to a company's customer appreciation outlook, etc.

[0022] Embodiments described herein provide a solution that overcomes a number of the gift card issue previously discussed. Importantly, instead the customer purchasing a "blind" gift card, after the purchase of which the customer no longer has any connection thereto the embodiments described herein, provide a solution which differs significantly from the conventional processes. In conventional approaches, after a gift-card is purchased, the customer that made the purchase is "blind", that is, after the purchase and giving of the gift card, the customer no longer has any connection thereto. The giver is never sure of whether or not the card was used, forgotten, or if it was used, what was purchased.

[0023] In contrast, the present embodiments, as will be described herein, provide a previously unknown procedure for allowing a customer to create, from their own credit account, a short-term authorized pass with a fixed amount of credit thereon, and assign the short-term authorized pass to the desired gift recipient. By providing the short-term authorized pass, from their own already existing account, the gift giver can realize a number of important solutions, modification, and actions that are not available in the present "blind" gift card scenario. For example, the gift giver can see if the short-term authorized pass has been used, they can track the amount spent with the short-term authorized pass, they can provide a prompt to the gift receiver if the short-term authorized pass has not been used, they can cancel the short-term authorized pass if it is lost, they can receive rewards (points, etc.) at the underlying account when the short-term authorized pass is used, etc. The gift giver can further withdraw or cancel the short-term authorized pass. For example, if the receiver gets in trouble, bad grades, or the like, the short-term authorized pass could be canceled by the giver.

[0024] As will be described in detail, the various embodiments of the present invention do not merely implement conventional non-integrated credit account processes on a computer. Instead, the various embodiments of the present invention, in part, provide a previously unknown procedure for procedure for generating, providing, tracking, and paying for a gift card.

[0025] Moreover, the embodiments do not recite a mathematical algorithm; nor do they recite a fundamental economic or longstanding commercial practice. Instead, they address a known problem in gift card presentation and utilization. Thus, the embodiments do not "merely recite the performance of some business practice known from the pre-Internet world along with the requirement to perform it on the Internet". Instead, the embodiments are necessarily rooted in computer-based credit account technology in order to overcome a problem specifically arising in the realm of gift card management.

Operation

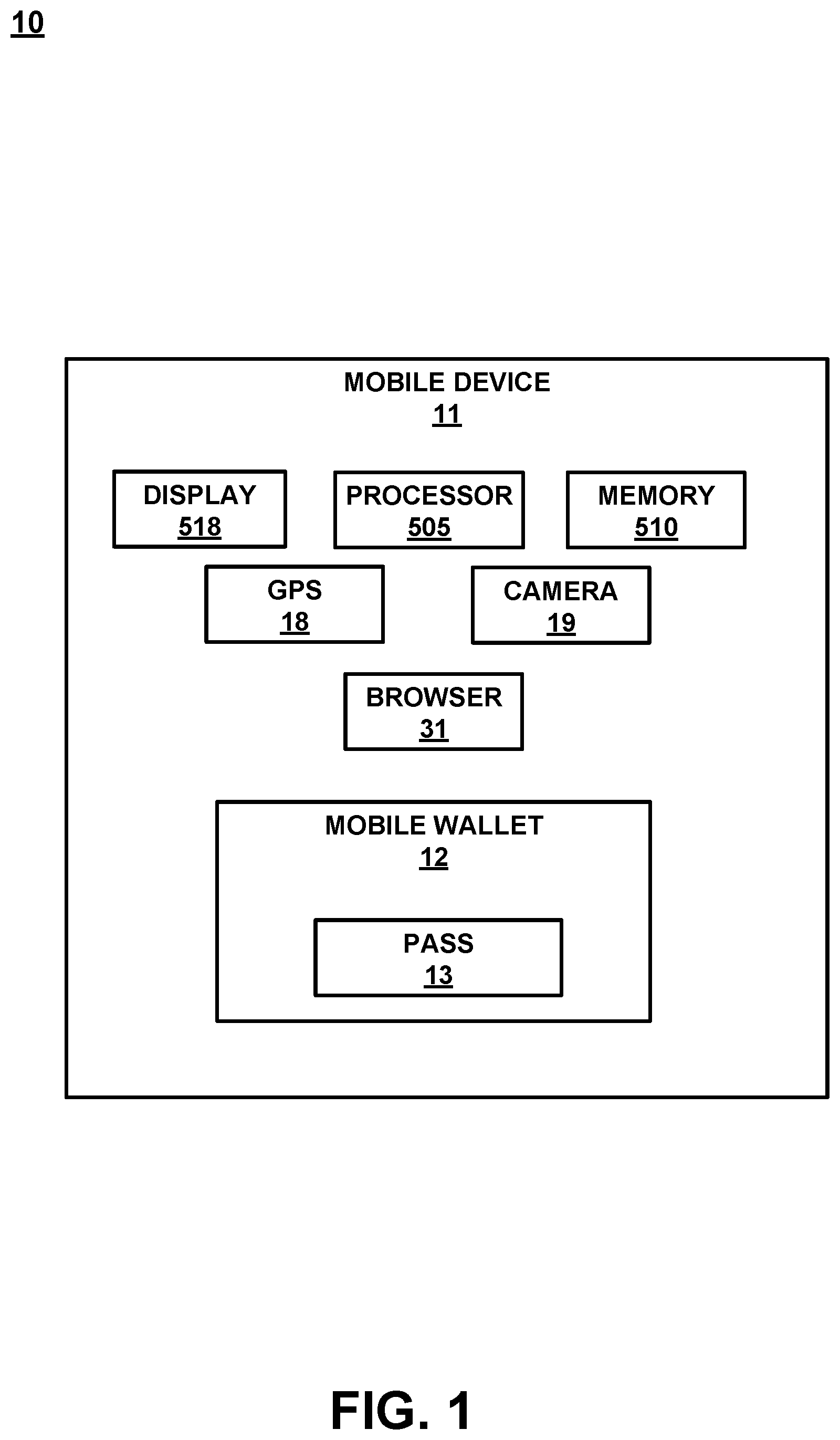

[0026] Referring now to FIG. 1, a block diagram 10 of a mobile device 11 is shown. Although a number of components are shown as part of mobile device 11, it should be appreciated that other, different, more, or fewer components may be found on mobile device 11.

[0027] In general, mobile device 11 is an example of a customer's mobile device, a store's mobile device, an associate's mobile device, or the like. Mobile device 11 could be a mobile phone, a smart phone, a tablet, a smart watch, a piece of smart jewelry, smart glasses, or other user portable devices having wireless connectivity. For example, mobile device 11 would be capable of broadcasting and receiving via at least one network, such as, but not limited to, WiFi, Cellular, Bluetooth, NFC, and the like. In one embodiment, mobile device 11 includes a display 818, a processor 805, a memory 810, a GPS 18, a camera 19, a browser 31, an app 32, and the like. In one embodiment, instead of providing GPS information, the location of mobile device 11 may be determined within a given radius, such as the broadcast range of an identified beacon, a WiFi hotspot, overlapped area covered by a plurality of mobile telephone signal providers, or the like. In general, browser 31 could be any web or Internet browsing capability. App 32 could be a brand app, a credit provider's app, or any other type of app that operates on mobile device 11.

[0028] Mobile device 11 also includes a digital or mobile wallet 12 which is an electronic application that operates on mobile device 11. Mobile wallet 12 includes short-term authorized pass 13. Although short-term authorized pass 13 is shown as part of mobile wallet 12, it should be appreciated that short-term authorized pass 13 could be located in a different application operating on mobile device 11, as part of an email, text, or the like. Further, mobile wallet 12 could refer to the application that is operating on mobile device 11 and maintaining the short-term authorized pass 13.

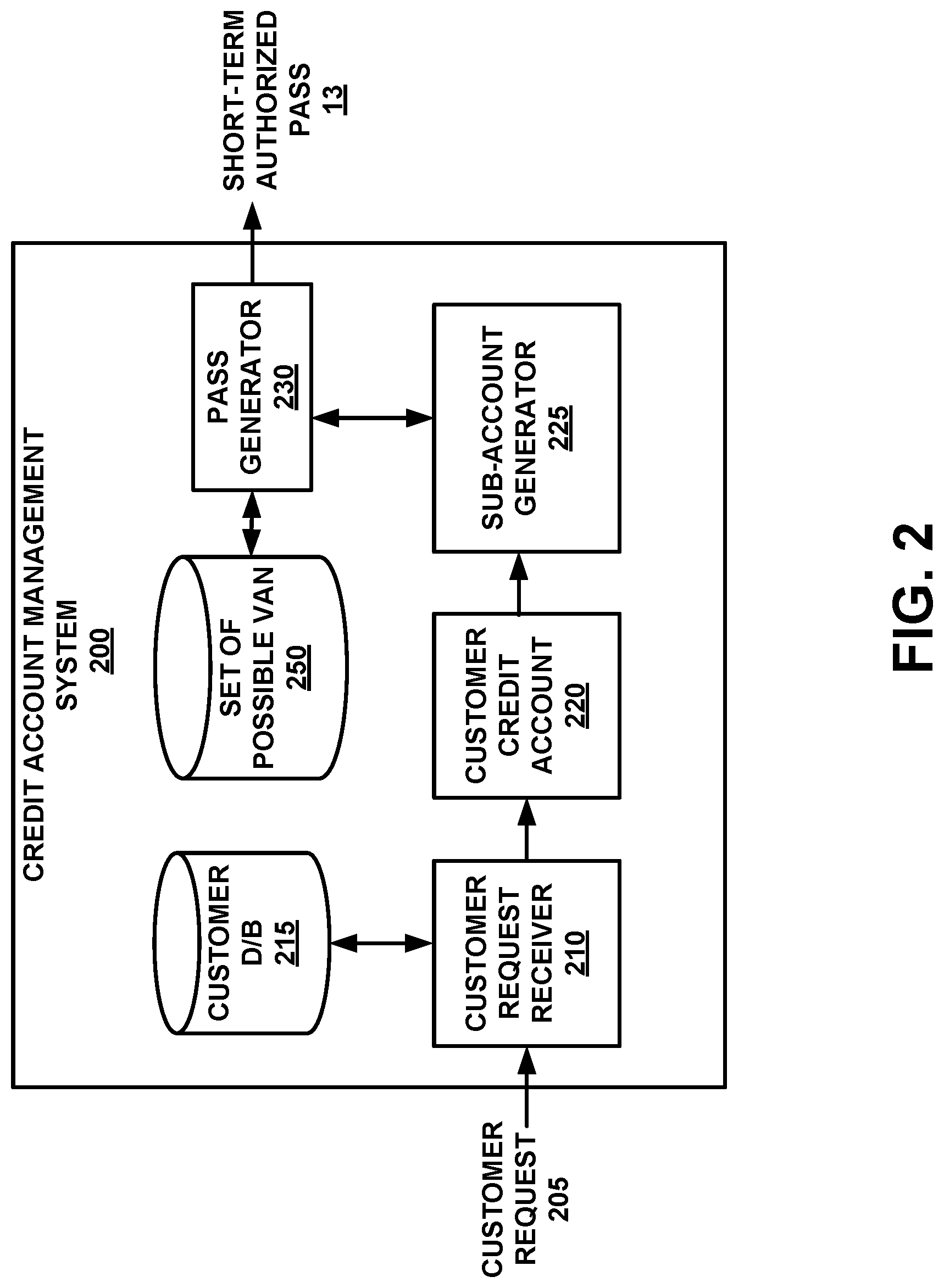

[0029] FIG. 2 is a block diagram of credit account management system 200 to generate a short-term authorized pass, in accordance with an embodiment. Credit account management system 200 of FIG. 2 includes a customer request receiver 210, a customer database 215, a customer credit account 220, a sub-account generator 225, a pass generator 230, a database of possible VAN 250. In one embodiment, credit account management system 200 receives a customer request 205 for the generation of a short-term authorized pass and provides a short-term authorized pass 13.

[0030] In one embodiment, the credit-based payment processor has a set of possible VAN 250 from which each short-term authorized pass is pulled. The set of possible VAN 250 is a set of numbers that conform to credit-based transaction rules and standards such that they can be used in the same manner as a normal credit account would be used.

[0031] In one embodiment, a customer request 205 is received at the customer request receiver 210 which performs a look up at via a customer database 215 to identify the customer and obtain the customer credit account 220 associated with the customer that provided the customer request 205. Once the customer credit account 220 is identified, the sub-account generator 225 generates a sub-account and associates the sub-account with the customer credit account 220. The sub-account generator 225 provides a credit limit to the sub-account, which in one embodiment, is the amount requested by the customer in the customer request 205.

[0032] A pass generator 230 pulls a valid credit card number, valid expiration date and a valid security code from the set of possible VAN 250, links the VAN information for the sub-account to the customer credit account 220, and generates a customer short-term authorized pass 13. In one embodiment, the valid credit card number, valid expiration date and a valid security code of the customer short-term authorized pass 13 are not tied directly to the customer's Primary Account Number. In one embodiment, the VAN conforms to a payment card industry (PCI) standard. In one embodiment, pass generator 230 provides an expiration date on the short-term authorized pass 13.

[0033] With reference now to FIG. 3, a block diagram 300 of a short-term authorized pass 13 as presented on a display screen 818 of a mobile device 11 is shown in accordance with an embodiment. Although a number of different features are shown in conjunction with the description of short-term authorized pass 13, it should be appreciated that some embodiments may include additional features or may skip some of the features altogether.

[0034] In one embodiment, the short-term authorized pass 13 is received at mobile device 11 from pass generator 230 (of FIG. 2) via a delivery method such as, but not limited to: a text, an email, a mobile push to a mobile wallet 12, via a network such as near field communication (NFC), Bluetooth, WiFi, or the like.

[0035] For example, the pass generator 230 will send a message to mobile device 11 which will include the short-term authorized pass 13 information such that the opening of the text message will result in the insertion of the short-term authorized pass 13 into mobile wallet 12. As such, the user can access the mobile wallet 12 and open the short-term authorized pass 13.

[0036] In a mobile push scenario, the pass generator 230 will push the short-term authorized pass 13 information to mobile device 11. In one embodiment, the result of the push will be the receipt of short-term authorized pass 13 at mobile device 11, such as in the mobile wallet 12, an application operating on mobile device 11, or the like. In another embodiment, the result of the push, text message, beacon data reception, etc. will be the receipt of a link to short-term authorized pass 13. After the link is received, the user will have to follow the link on mobile device 11 to obtain the short-term authorized pass 13 at mobile device 11.

[0037] Information 310 refers to the identification information such as where the short-term authorized pass 13 can be used. For example, if the short-term authorized pass 13 is brand specific to "Dresses and More", then it would include the name "Dresses and More" to indicate to the recipient where it can be used.

[0038] Identifier 315 is a message that can optionally be provided on short-term authorized pass 13, to identify the giver, the reason for the gift, etc.

[0039] Credit amount 321 is the value or amount of credit available on the short-term authorized pass 13. In one embodiment, credit amount 321 is fixed.

[0040] In another embodiment, credit amount 321 will reflect the remaining balance of short-term authorized pass 13. For example, short-term authorized pass 13 could initially have a credit amount of $50.00. After short-term authorized pass 13 is used to make a purchase (e.g., $35.00) in one embodiment, the credit amount 321 would automatically update to reflect the remaining amount (e.g., $15.00).

[0041] VAN 323 is the credit account number that is assigned to short-term authorized pass 13 and is linked to the underlying customer credit account 220, but it is not the underlying customer credit account number.

[0042] Expiration date 324 is generally not related to the underlying customer credit account 220 but is instead an expiration for the short-term authorized pass 13. In one embodiment, expiration date 324 is provided not as an expiration but to provide the ability for the short-term authorized pass 13 to be used. For example, the expiration date 324 is provided to enable short-term authorized pass 13 to make a purchase. In one embodiment, the expiration date 324 is an actual expiration date of short-term authorized pass 13. It could be a year, two-years, 6-months or the like, and could be selected by the customer or automatically provided by credit account management system 200.

[0043] Security code 325 is also not related to the underlying account specifically, but is instead provided as it may be necessary when making a purchase utilizing the short-term authorized pass 13.

[0044] In one embodiment, short-term authorized pass 13 includes a scanable code 330, such as a barcode, QR code, 1D code, 2D code, or the like. A QR code is shown as code 330 in FIG. 3 for purposes of clarity. In one embodiment, code 330 is scanned by the retailer/clerk at the register or during the time of checkout to provide the short-term authorized pass 13 details to the POS.

[0045] In one embodiment, short-term authorized pass 13 includes an animated digital watermark 360 that is displayed on display 818. The term "animated digital watermark", as used herein, is any visually perceptible image that is dynamically moving or animated that facilitates in ensuring that mobile payment card is authentic (or not fraudulent).

[0046] Animated digital watermark 360, by being animated, provides visual evidence that short-term authorized pass 13 is not a fraudulent copy. More specifically, animated digital watermark 360 provides visual evidence that the displayed short-term authorized pass 13 is not a fraudulent captured static image of the authentic short-term authorized pass 13.

[0047] For example, a merchant visually examining short-term authorized pass 13 displayed on device 11 will notice the dynamic moving properties of animated digital watermark 360 and determine that short-term authorized pass 13 is authentic and not fraudulent.

[0048] Animated digital watermark 360 can be any image with dynamic (or visually moving/changing) properties. For example, animated digital watermark 360 is a rotating logo of the bank that issued short-term authorized pass 13. In another example, animated digital watermark 360 is an image that constantly or variably changes shape, color, and/or position.

[0049] In various embodiments, animated digital watermark 360 varies based on the day, time, session, etc.

[0050] In one embodiment, animated digital watermark 360 is a user-interactive animated digital watermark. For example, a message is displayed in response to a user selecting animated digital watermark 360 on the touch screen display. The displayed message, in response to the touch by the user, provides visual evidence that the displayed short-term authorized pass 13 is not a fraudulently captured video of the authentic mobile payment card because a captured video of short-term authorized pass 13 (including animated digital watermark) would not be able to display a message in response to a user touching the animated digital watermark in the fraudulent video.

[0051] In one embodiment, short-term authorized pass 13 also displays a show government issued ID 330 to promote the user to show identification to the retailer. Short-term authorized pass 13 optionally includes an add to wallet 370 feature which will add the short-term authorized pass 13 to the user's mobile wallet 12. In one embodiment, the add to wallet 370 feature is available if the short-term authorized pass 13 was not automatically added to the user's mobile wallet 12.

[0052] Referring now to FIG. 4, a flowchart 400 of a method for generating a short-term authorized pass for display on a display screen of a mobile device is shown in accordance with an embodiment. In one embodiment, the credit account is a brand credit account and the associated short-term authorized pass is only useable for the brand. For example, if the customer's branded credit account is a Michelle's boating supply branded card, then the gift recipient would receive a short-term authorized pass for use at Michelle's boating supply. In addition, the gift recipient would be provided with the amount of money available on the short-term authorized pass (e.g., $25). In another embodiment, the credit account is a co-branded credit account and the short-term authorized pass is useable in many, or all, locations where a credit card can be used.

[0053] With reference now to 402 of FIG. 4, one embodiment receives, at a credit account management system, a request for a short-term authorized pass to be provided from a credit account of the first party to the second party, the request comprising: an amount to be allocated to the short-term authorized pass, and an identifier for the second party.

[0054] In one embodiment, the creation of the short-term authorized pass is initiated by the giver. For example, the giver could access: a kiosk in a store, a website, an application (app) on a device, a web app, making a telephone call, requesting the assignment at a point-of-sale (POS), from a store associate, or the like. In one embodiment, the initiation of the process occurs via a computing device such as, but not limited to, a mobile device, a work computer, a home computer, a smart TV, etc.

[0055] In general, the creation of the short-term authorized pass does not require the giver to provide any monies, spend any money, or the like. Instead, during the creation of the short-term authorized pass, a hold is placed on the requested amount of the underlying credit account. For example, if the short-term authorized pass is for 75 dollars, then a hold on 75 dollars' worth of credit would be provided on the credit account's credit limit. For example, if the credit account's credit limit is 3,500 dollars, then the new credit limit would be 3,425 dollars. In so doing, the short-term authorized pass would remain funded and the giver would not be able to surpass their credit limit for the credit account. Once the amount on the short-term authorized pass was spent or the short-term authorized pass was otherwise deactivated, the hold would be removed, and the credit limit on the original credit account would return to 3,500 dollars.

[0056] In one embodiment, the identifier of the second party is a snail mail address and the short-term authorized pass 13 is a physical card and is sent to the snail mail address of the second party.

[0057] In one embodiment, the short-term authorized pass 13 is digital. In addition, the identifier of the second party is an email address and the short-term authorized pass 13 is sent to the email address of the second party. In another embodiment, the identifier of the second party is a mobile phone number and the short-term authorized pass 13 is sent via an SMS to mobile device 11 of the second party.

[0058] In one embodiment, the short-term authorized pass 13 is automatically added to a digital or mobile wallet 12 on a mobile device 11 of the second party when the short-term authorized pass 13 is received at the mobile device 11.

[0059] Referring now to 404 of FIG. 4, one embodiment generates a sub-account from the credit account, comprising: allocating a part of the credit account to form a sub-account; setting a credit limit on the sub-account to the amount to be allocated; assigning a virtual account number (VAN) to the sub-account; and generating the short-term authorized pass using the VAN of the sub-account.

[0060] With reference now to 406 of FIG. 4, one embodiment provides, from the credit account management system and to the second party, the short-term authorized pass, wherein no funds are taken from the credit account of the first party until the short-term authorized pass is used. In one embodiment, the short-term authorized pass is received at the second party's mobile device and displayed thereon. As discussed herein, in one embodiment, the short-term authorized pass is received from a text, email, beacon, SMS, or the like. In one embodiment, the short-term authorized pass is received at an application operating on the second party's mobile device. For example, the short-term authorized pass could be received in a brand specific application, in a credit provider's application, or the like. In one embodiment, the initial information provided to the second party could be a notice to download a specific application in order to obtain the short-term authorized pass. In one embodiment, the use of the specific application for managing the short-term authorized pass would operate similar to (or in place of) the mobile wallet 12 discussed herein.

[0061] When the short-term authorized pass is used, the underlying credit account is billed. Thus, the purchase is shown on the giver's credit account statement. In one embodiment, there is no fee charged for giving a short-term authorized pass. In other words, unlike a store-bought gift-card that includes an activation fee, the short-term authorized pass would be free to the credit account holder. In another embodiment, there is a fee charged for creating/giving a short-term authorized pass, or for the 5th or greater short-term authorized pass created per year, etc.

[0062] Further, by being able to quickly and easily authorize and deliver a short-term authorized pass to a recipient (e.g., via a digital delivery to a recipient's mobile device, digital wallet, etc.), the giver is able to use this capability to provide a person (that is not of age or otherwise without a credit account) to have a credit purchasing capability with the short-term authorized pass versus the person using the giver's credit card, debit card, etc. For example, a 17-year-old needs to get gas at a gas station, buy a winter coat, or the like. Instead of the parent providing cash or a credit card to the 17-year-old (and thus having limited control on any of the purchases actually made on the card, such as food, drinks, clothes, etc.), the parent could provide the short-term authorized pass for a limited amount of money (e.g., 50 dollars for gas, 200 dollars for a jacket, etc.). In so doing, not only would the parent's actual cash, credit, or debit account be safe from any additional costs, the parents would also receive a report of the spending that occurred.

[0063] In one embodiment, since the giver is notified about the amount spent, the giver can cancel the short-term authorized pass after one or more purchases are made even when the actual amount spent is less than the amount authorized. For example, if the short-term authorized pass was for 50 dollars for gas, and the recipient only spent 30 dollars on gas. The short-term authorized pass could be canceled after only 30 dollars had been spent by the giver.

[0064] Similarly, the short-term authorized pass could be initially authorized with a credit limit that is more than the amount needed to cover the expected purchase expense, and then after the actual purchase is made, the short-term authorized pass could be terminated. For example, a daughter wants to purchase a winter coat that she believe costs 100 dollars, but she is not certain. Since the parents are not sure of the cost, they set up the short-term authorized pass with an initial limit that is certain to be able to cover the cost of the coat (e.g., 130 dollars). If the daughter buys the coat for 111 dollars, then the parent's credit account is only charged for the amount of money actually spent with the short-term authorized pass (e.g., 111 dollars) and not the initial amount of money designated to the short-term authorized pass (e.g., 130 dollars). Then, when the short-term authorized pass expires (or is canceled) the 19 dollars would remain unspent.

[0065] In another embodiment, the daughter wants to purchase a winter coat with a short-term authorized pass having a 100-dollar credit limit. If the daughter buys a coat for 125 dollars, then the gift giver's credit account is only charged for the amount of money actually spent with the short-term authorized pass (e.g., 100 dollars) and the remaining 25 dollars would have to be paid by the daughter using another revenue source.

[0066] In yet another embodiment, the daughter wants to purchase a winter coat and the parents provide her with a short-term authorized pass having a 100-dollar credit limit. If the daughter finds a coat for 125 dollars, she could contact her parents and request an increase in the short-term authorized pass credit limit to 125 dollars to cover the additional costs. The parents can either agree and increase the credit limit of the short-term authorized pass to 125 dollars or else disagree and maintain the initial amount (e.g., 100 dollars), such that the remaining 25 dollars would have to be paid by the daughter from a different source.

[0067] In one embodiment, the short-term authorized pass can help build clientele via at least one previously unattainable acquisition channels. For example, by providing the daughter (in the above example) with the short-term authorized pass (such as to a given clothing establishment), the daughter would be able to have a shopping "experience" at the clothing establishment. This shopping "experience" would be an opportunity for the given clothing establishment to provide rewards, coupons, discounts, services, support, and guidance that could blossom into a long-lasting relationship that would include brand loyalty, obtaining of a branded credit account by the daughter, social media feedback that would provide brand recognition, etc.

[0068] In another example of how the short-term authorized pass will build clientele, a parent (or grandparent) could give the short-term authorized pass to a recipient that is too young to have their own credit account. When the recipient becomes of age to apply for a credit account, the branded account could realize that the recipient had received a number of short-term authorized passes for a given clothing store, gas station, etc. The clothing store could then provide a credit opportunity for the recipient (or to the parent or grandparent that had been previously providing the short-term authorized pass to the recipient) to apply for their own branded credit account with the store. In one embodiment, if the credit opportunity was provided to the parent or the grandparent, the opportunity could include a reward in conjunction with the opportunity.

[0069] Similarly, a parent (or grandparent) could give a number of short-term authorized passes to a given recipient every year. Based on the knowledge about the number of short-term authorized passes received, the one or more stores where the recipient used the short-term authorized passes, and the like, it is possible to utilize the data from the short-term authorized pass to provide offers, rewards, credit accounts opportunities, and the like to one or both of the giver and the recipient of the short-term authorized passes. This data would provide another means for building clientele.

[0070] In one embodiment, the system is proactive, e.g., send a reminder to a customer that it is almost someone's birthday and that a short-term authorized pass could be delivered to the that person before or on their birthday, etc. Similarly, the system could be set up to automatically create and deliver a short-term authorized pass from the customer to the recipient on a given day every year (e.g., such as an anniversary, birthday, holiday, etc.). Further, the amount on the short-term authorized pass could be automatically adjusted each years (e.g., increase 3% per year), unmodified without a customer's specific adjustment (e.g., 20 dollars to Suzy each year on her birthday), or the like. In one embodiment, there can be any number of short-term authorized passes created for a given credit account, as long as the total of the short-term authorized passes did not extend beyond the credit accounts' credit limit.

[0071] In one embodiment, an indicator is provided to the first party (e.g., the customer of customer credit account 220) when the short-term authorized pass 13 is used to make a purchase. In one embodiment, the indicator indicates an amount of money spent and a location where the short-term authorized pass 13 was used.

[0072] In one embodiment, a reminder is provided to the second party. The reminder provided after a pre-defined amount of time and indicating that the short-term authorized pass 13 is still active.

[0073] In one embodiment, an expiration date 324 is provided with the short-term authorized pass and the short-term authorized pass 13 is expired after a passing of the expiration date 324. In addition, an expiration reminder can be provided to the second party. The expiration reminder providing the recipient with a pre-defined amount of time before the expiration date of the short-term authorized pass 13 while also acting as a reminder indicating that the short-term authorized pass 13 is still active.

[0074] In one embodiment, the short-term authorized pass 13 is non-rechargeable. That is, once the short-term authorized pass 13 is used, it is terminated. Any desire by the customer to provide a recharge to the terminated short-term authorized pass 13, would be resolved by the generation of a new short-term authorized pass 13 with a new VAN, etc.

[0075] However, in one embodiment the first party (e.g., the customer with the credit account) can make a request for an increase in the amount to be allocated to the short-term authorized pass 13. As long as short-term authorized pass 13 is not terminated or expired, the credit limit on the sub-account can be increased to the new amount requested by the first party.

Short-Term Certificate

[0076] FIG. 5 is a block diagram of credit account management system 500 to generate a short-term certificate 513, in accordance with an embodiment. In general, by providing a short-term certificate 513, a giver can give a recipient a gift that is similar in form and function to the short-term authorized pass 13 described herein. However, since it is a short-term certificate 513 that is being given, there is no need for the retailer to have any sort of credit card rails, capabilities, or the like. Instead, the redemption of the short-term certificate 513 would work in the same way as any certificate, rewards, coupons, or the like, and could be performed with existing/legacy systems.

[0077] Moreover, since the short-term certificate 513 would not need to utilize any credit card rails to be redeemed, the retailer would not have to pay any of the fees normally incurred with a credit card purchase. Instead, the redemption would operate on the same system as coupons, certificates, discounts, rewards, or the like. e.g., via a reward validation/verification system. In one embodiment, there is no gift card fee charged to the customer giving the short-term certificate 513.

[0078] In one embodiment, the short-term certificate 513 can be tracked, revoked, recipient reminded of the short-term certificate 513 or its pending expiration, giving customer informed of the use (or lack thereof) of the short-term certificate 513, and rewards provided to the giving customer in a similar manner as the short-term authorized pass 13 described herein. Further, in one embodiment, since the short-term certificate 513 is brand specific, the relationship building between the short-term certificate 513 recipient and the brand can be built, monitored, and maintained in a similar manner as the short-term authorized pass 13 described herein.

[0079] In one embodiment, similar to the short-term authorized pass 13 disclosed herein, by using the short-term certificate 513, the customer would not have to spend any money until the short-term certificate 513 is redeemed. Instead, the credit account management system 500 could put a hold on the customer's credit account, the value could be floated, the customer's credit limit could be reduced, or the like, based on the value of the short-term certificate 513. Further, in one embodiment, after the short-term certificate 513 is redeemed, only the money that was spent would actually be charged to the customer's credit account.

[0080] In one embodiment, the customer could select to initially pay for the value of the short-term certificate 513, and then any monies that was not used during redemption (or expiration) of short-term certificate 513 would be credited back to the customer's credit account.

[0081] In one embodiment, such as when the short-term certificate 513 is a single use certificate. The short-term certificate 513 could act as a basket builder for one or both of the retailer and the redeemer. For example, if the redeemer of the short-term certificate 513 is informed (by an associate) or knows that the short-term certificate 513 is single use, the retailer could suggest the redeemer add a product or two to obtain the full redemption value of the short-term certificate 513. Similarly, the redeemer may pick up an extra item or two to make sure they meet the value of the short-term certificate 513.

[0082] Credit account management system 500 of FIG. 5 includes a customer request receiver 210, a customer database 215, a customer credit account 220, and a certificate generator 530. In one embodiment, credit account management system 500 receives a customer request 505 for the generation of a short-term certificate and provides a short-term certificate 513. In general, the customer request 505 for the generation of a short-term certificate is a way for the customer to give an amount of money to another party. For example, grandma could provide a customer request 505 for a short-term certificate in the amount of 50 dollars to be sent to her granddaughter as a birthday gift.

[0083] In one embodiment, customer request 505 is received at the customer request receiver 210 which performs a look up at the customer database 215 to identify the customer and obtain the customer credit account 220 associated with the customer that provided the customer request 505. Once the customer credit account 220 is identified, the certificate generator 530 generates a certificate. In one embodiment, the certificate generator 530 generates a short-term certificate 513 that includes information such as, but not limited to, one or more of: an assignment, a monetary value, an expiration date, a number of uses, and the like.

[0084] In one embodiment, the assignment is the receiving party (e.g., the granddaughter). In one embodiment, the monetary value is the value of the certificate and is the amount requested by the customer in the customer request 505 (e.g., 50 dollars). An expiration date is the date at which the short-term certificate 513 will no longer be valid. For example, the short-term certificate 513 may be valid for 3 months (or any range that could be customer defined, credit account management system 500 defined, or the like.) After the 3-month period tolls, the short-term certificate 513 would be invalid. If it was a digital certificate, it could be automatically removed from the recipient's mobile wallet, from an app on the recipient's mobile device, or the like.

[0085] The number of uses refers to the amount of times the receiving party can use the short-term certificate 513. In one embodiment, the short-term certificate 513 may be a single use certificate. That is, when it is redeemed the first time, any remaining value of the short-term certificate 513 would expire. For example, if the granddaughter only purchased 35 dollars' worth of goods, then only 35 dollars of the short-term certificate 513 would have been spent and the certificate would be redeemed at the lower 35 dollar value.

[0086] In one embodiment, the short-term certificate 513 may be a multi-use short-term certificate 513. That is, when it is redeemed the first time, any remaining value of the certificate would remain available for the recipient to use on another occasion. For example, if the granddaughter only purchased 35 dollars' worth of goods, then only 35 dollars of the short-term certificate 513 would have been spent and she would now have a short-term certificate 513 with a 15 dollar value.

[0087] In one embodiment, if the multi-use short-term certificate 513 is a paper (or a physical object) certificate, the original short-term certificate 513 with a face value of 50 dollars would be redeemed and a new short-term certificate 513 with a face value of 15 dollars would be provided at the time of purchase.

[0088] In one embodiment, if the multi-use short-term certificate 513 is a digital (or a virtual object) certificate, the original short-term certificate 513 with a face value of 50 dollars would be replaced with a short-term certificate 513 with a face value of 15 dollars.

[0089] In one embodiment, the certificate generator 530 can also provide one or more optional pieces of information on the short-term certificate 513, information such as, but not limited to, an indication of who the certificate is from (e.g., grandma), why it was sent (e.g., happy birthday), where it can be used (e.g., at the jean emporium), and the like. Although a number of pieces of information are described, it should be appreciated that there may be more, fewer, or different pieces of information (or optional information) provided on the short-term certificate 513 in plain format and/or in an encrypted format. The pieces of information discussed herein are provided for purposes of clarity, and for some embodiments. However, other embodiments could have more, fewer, or different pieces of information (or optional information) on the short-term certificate 513.

[0090] With reference now to FIG. 6, a block diagram of the short-term certificate 513 is shown in accordance with an embodiment. In one embodiment, short-term certificate 513 is printed on a physical media. In another embodiment, the short-term certificate 513 is a digital product (e.g., a virtual certificate). Although a number of different features are shown in conjunction with the description of short-term certificate 513, it should be appreciated that some embodiments may include additional features or may skip some of the features altogether.

[0091] In one embodiment, the physical version of short-term certificate 513 is received via a physical delivery method such as, but not limited to: via a letter, inside a card, or the like. In one embodiment, the physical version of the short-term certificate 513 could be sent to the customer that requested the certificate such that the customer could give the certificate to the recipient. In another embodiment, the physical version of the short-term certificate 513 could be sent to the recipient as identified in the customer request 505. For example, the customer request 505 could include the recipient's address and request the short-term certificate 513 be sent directly to the recipient. In one embodiment, the customer request 505 could also include a request such as: deliver the short-term certificate 513 in a card (e.g., a birthday card, a holiday card, a graduation card, another notable event, or the like).

[0092] In one embodiment, the virtual version of short-term certificate 513 is received at mobile device 11 from certificate generator 530 (of FIG. 5) via a delivery method such as, but not limited to: a text, an email, a link to be followed by browser 31, a mobile push to app 32, a mobile push to a mobile wallet 12, or the like. In general, short-term certificate 513 could be digitally delivered via a network such as near field communication (NFC), Bluetooth, WiFi, cellular, or the like.

[0093] For example, in one embodiment, the certificate generator 530 will send a message to mobile device 11 which will include the short-term certificate 513 information such that the opening of the text message will result in the insertion of the short-term certificate 513 into mobile wallet 12. As such, the user can access the mobile wallet 12 and open the short-term certificate 513.

[0094] In a mobile push scenario, the certificate generator 530 will push the short-term certificate 513 information to mobile device 11. In one embodiment, the result of the push will be the receipt of short-term certificate 513 at mobile device 11, such as in the mobile wallet 12, app 32, or the like. In another embodiment, the result of the push, text message, beacon data reception, etc. will be the receipt of a link to short-term certificate 513. After the link is received, the user will have to follow the link on mobile device 11 to obtain the short-term certificate 513 at mobile device 11.

[0095] Referring still to short-term certificate 513 of FIG. 6, in general, the short-term certificate 513 functions similar to a reward. In one embodiment, the short-term certificate 513 will include a number of pieces of information such as, but not limited to, one or more of: an assignment 602, a location 603, a value 604, an expiration date 605, a number of uses 606, and the like.

[0096] The assignment 602 would be the party to which short-term certificate 513 was issued. For example, granddaughter, friend, co-worker, etc.

[0097] The location 603 would be the store or brand where the short-term certificate 513 could be redeemed. For example, the short-term certificate 513 may be specifically for the brand "Apple Picking Supplies Inc."

[0098] The value 604 could be a monetary value, a percentage value, or the like. For example, in one embodiment, the value 604 could be a set amount such as $50 dollars (or any other monetary amount).

[0099] In another example, the value 604 could be a percentage. For example, the value 604 will cover half of a purchase (e.g., 50%), such that the value is not defined until after the short-term certificate 513 is redeemed.

[0100] In one embodiment, the certificate value percentage could be directed toward a specific item. For example, the value 604 could be for 25% of the cost of a new refrigerator, a dinnerware set, etc. Thus, the short-term certificate 513 could have a value 604 for a portion of a specific purchase, that is not defined until it is redeemed. At that time, the customer credit account 220 would provide the retailer with the value 604. For example, if the short-term certificate 513 was for 25% of a recliner and the recliner was 400 dollars, then after the short-term certificate 513 is redeemed, the customer credit account 220 would make a 100 dollar payment to the retailer from the customer credit account (or otherwise provide the payment from the customer's credit account to the retailer).

[0101] Expiration date 605 is the date at which the short-term certificate 513 will no longer be valid. Expiration date 605 is not related to the underlying customer credit account 220 but is instead an expiration for the short-term certificate 513. In one embodiment, expiration date 323 is an actual expiration date of short-term certificate 513. It could be a 2-weeks, 1-month, 6-months, a year, or the like, and could be selected by the customer in the customer request 505 or automatically provided by credit account management system 500.

[0102] After the expiration date 605, the short-term certificate 513 would be invalid. If it was a digital certificate, it could be automatically removed from the recipient's mobile wallet, from an app on the recipient's mobile device, or the like.

[0103] The number of uses 606 refers to the amount of times the receiving party can use the short-term certificate 513. In one embodiment, the short-term certificate 513 may be a single use certificate. That is, when it is redeemed the first time, any remaining value of the certificate would expire. For example, if the granddaughter only purchased 35 dollars' worth of goods, then only 35 dollars of the short-term certificate 513 would have been spent and the certificate would be redeemed at the lower 35 dollar value. As such, the remaining 15 dollars would be returned to the customer's credit account 220, only 35 dollars would be charged to an amount on hold in the customer's credit account, only 35 dollars would be charged to the customer's credit account, or the like.

[0104] In one embodiment, the short-term certificate 513 may be a multi-use short-term certificate 513. That is, when it is redeemed the first time, any remaining value of the certificate would remain available for the recipient to use on another occasion before the expiration date 605. For example, if the granddaughter only purchased 35 dollars' worth of goods, then only 35 dollars of the short-term certificate 513 would have been spent and she would now have a short-term certificate 513 with a 15 dollar value 604.

[0105] Referring still to short-term certificate 513 of FIG. 6, in one embodiment, the short-term certificate 513 may also include one or more optional pieces of information such as, but not limited to, an indication of who the certificate is from 613 (e.g., grandma), why it was sent 612 (e.g., happy birthday), and the like. Although a number of pieces of information are described, it should be appreciated that there may be more, fewer, or different pieces of information (or optional information) provided on the short-term certificate 513 in plain format and/or in an encrypted format. The pieces of information discussed herein are provided for purposes of clarity, and for some embodiments. However, other embodiments could have more, fewer, or different pieces of information (or optional information) on the short-term certificate 513.

[0106] In one embodiment, short-term certificate 513 includes an identifier 630. In general, identifier 630 could be, a written statement, a string of numeric or alpha-numeric characters, a bar code, a QR code, an image code, a 2D code, a 3D code, or the like. In one embodiment, the identifier 630 will allow a redeemer to obtain information about the short-term certificate 513. The information could include one or more of the assignment 602, the value 604, the expiration date 605, a provider of the certificate, the number of uses 606, a one-time use requirement, a unique identifier, an encryption or token, some, none or all of the other information discussed herein, and the like. In one embodiment, identifier 630 also includes information about the customer that requested the short-term certificate 513 and a link to the underlying customer credit account 220. In one embodiment, it does not include the underlying customer credit account number.

[0107] A QR code is shown as identifier 630 in FIG. 6 for purposes of clarity. In one embodiment, identifier 630 is scanned by the retailer/clerk at the register or during the time of checkout to provide the short-term certificate 513 details to the POS.

[0108] In one embodiment, short-term certificate 513 includes an animated digital watermark 360 that is displayed on display 818. The term "animated digital watermark", as used herein, is any visually perceptible image that is dynamically moving or animated that facilitates in ensuring that mobile payment card is authentic (or not fraudulent).

[0109] Animated digital watermark 360, by being animated, provides visual evidence that short-term certificate 513 is not a fraudulent copy. More specifically, animated digital watermark 360 provides visual evidence that the displayed short-term certificate 513 is not a fraudulent captured static image of the authentic short-term certificate 513.

[0110] For example, a merchant visually examining short-term certificate 513 displayed on device 11 will notice the dynamic moving properties of animated digital watermark 360 and determine that short-term certificate 513 is authentic and not fraudulent.

[0111] Animated digital watermark 360 can be any image with dynamic (or visually moving/changing) properties. For example, animated digital watermark 360 is a rotating logo of the bank that issued short-term certificate 513. In another example, animated digital watermark 360 is an image that constantly or variably changes shape, color, and/or position. In various embodiments, animated digital watermark 360 may vary based on the day, time, session, etc.

[0112] In one embodiment, animated digital watermark 360 is a user-interactive animated digital watermark. For example, a message is displayed in response to a user selecting animated digital watermark 360 on the touch screen display. The displayed message, in response to the touch by the user, provides visual evidence that the displayed short-term certificate 513 is not a fraudulently captured video of the authentic mobile payment card because a captured video of short-term certificate 513 (including animated digital watermark) would not be able to display a message in response to a user touching the animated digital watermark in the fraudulent video.

[0113] In one embodiment, short-term certificate 513 also displays a show government issued ID 335 to promote the user to show identification to the retailer. Short-term certificate 513 optionally includes an add to wallet 370 feature which will add the short-term certificate 513 to the user's mobile wallet 12 (or app 32). In one embodiment, add to wallet 370 feature is available if the short-term certificate 513 was not automatically added to the user's mobile wallet 12.

[0114] Referring now to FIG. 7, a flowchart 700 of a method for generating the short-term certificate 513 is shown in accordance with an embodiment. In one embodiment, the credit account is a brand credit account and the associated short-term certificate 513 is only useable at the brand. For example, if the customer's branded credit account is a Michelle's boating supply branded card, then the gift recipient would receive a short-term certificate 513 for use at Michelle's boating supply. In addition, the gift recipient would be provided with the value 604 of the short-term certificate 513. In another embodiment, the credit account is a co-branded credit account and the short-term certificate 513 is useable in many, or all, locations where that associated credit card can be used.

[0115] With reference now to 702 of FIG. 7, one embodiment receives, at credit account management system 500, a request for a short-term certificate 513 to be provided from a credit account of the first party to the second party, the request including at least: an amount to be allocated to the short-term certificate 513, and an identifier for the second party.

[0116] In one embodiment, the creation of the short-term certificate 513 is initiated by the giver. For example, the giver could access: a kiosk in a store, a website, an application (app) on a computing device, a web app, make a telephone call, request the short-term certificate 513 at a point-of-sale (POS), from a store associate, or the like. In one embodiment, the initiation of the process occurs via a computing device such as, but not limited to, a mobile device, a work computer, a home computer, a smart TV, etc.

[0117] In one embodiment, the identifier of the second party is an actual mail address and the short-term certificate 513 is a physical card sent to the actual mail address of the second party.

[0118] In one embodiment, the short-term certificate 513 is digital. In addition, the identifier of the second party is an email address and the short-term certificate 513 is sent to the email address of the second party. In another embodiment, the identifier of the second party is a mobile phone number and the short-term certificate 513 is sent via an SMS to mobile device 11 of the second party.

[0119] In one embodiment, the short-term certificate 513 is automatically added to a digital or mobile wallet 12, or an app 32, on mobile device 11 of the second party when the short-term certificate 513 is received at the mobile device 11.

[0120] Referring now to 704 of FIG. 7, one embodiment allocates a part of the credit account to cover the value of the short-term certificate 513. That is, in one embodiment, the creation of the short-term certificate 513 does not require the giver to provide any upfront money, spend any money, or the like. Instead, in one embodiment, during the creation of the short-term certificate 513, a hold is placed on the requested amount of the underlying credit account. For example, if the short-term certificate 513 has a face value of 75 dollars, then a hold on 75 dollars' worth of credit would be placed on the customer's credit account. For example, if the customer's credit account credit limit is 3,500 dollars, then the new credit limit would be 3,425 dollars.

[0121] In so doing, the short-term certificate 513 would remain funded and the giver would not be able to surpass their credit limit for the credit account. Once the short-term certificate 513 is redeemed or the short-term certificate 513 expires or is otherwise deactivated, the hold would be removed, and the credit limit on the original credit account would return to 3,500 dollars.

[0122] With reference now to 706 of FIG. 7, one embodiment generates the short-term certificate 513. In one embodiment, the certificate generator 530 generates the short-term certificate 513 to include information such as, but not limited to, one or more of: an assignment, a monetary value, an expiration date, a number of uses, and the like.

[0123] In one embodiment, the certificate generator 530 can also provide one or more optional pieces of information on the short-term certificate 513, information such as, but not limited to, an indication of who the certificate is from (e.g., pup-up), why it was sent (e.g., college graduation), where it can be used (e.g., Maddy's haberdashery), and the like. Although a number of pieces of information are described, it should be appreciated that there may be more, fewer, or different pieces of information (or optional information) provided on the short-term certificate 513 in plain format and/or in an encrypted format.

[0124] With reference now to 708 of FIG. 7, one embodiment provides, from the credit account management system 500 and to the second party, the short-term certificate 513, wherein no funds are taken from the credit account of the first party until the short-term certificate 513 is redeemed.

[0125] In one embodiment, the short-term certificate 513 is received at the second party's mobile device and displayed thereon. As discussed herein, in one embodiment, the short-term certificate 513 is received from a text, email, beacon, SMS, or the like. In one embodiment, the short-term certificate 513 is received at an application 32 operating on the second party's mobile device 11. For example, the short-term certificate 513 could be received in a brand specific application, in a credit provider's application, or the like. In one embodiment, the initial information provided to the second party could be a notice to download a specific application in order to obtain the short-term certificate 513. In one embodiment, the use of the specific application 32 for managing the short-term certificate 513 would operate similar to (or in place of) the mobile wallet 12 discussed herein.

Example Computer System

[0126] With reference now to FIG. 8, portions of the technology for providing a communication composed of computer-readable and computer-executable instructions that reside, for example, in non-transitory computer-readable medium (or storage media, etc.) of a computer system. That is, FIG. 8 illustrates one example of a type of computer that can be used to implement embodiments of the present technology. FIG. 8 represents a system or components that may be used in conjunction with aspects of the present technology. In one embodiment, some or all of the components described herein may be combined with some or all of the components of FIG. 8 to practice the present technology.

[0127] FIG. 8 illustrates an example computer system 800 used in accordance with embodiments of the present technology. It is appreciated that computer system 800 of FIG. 8 is an example only and that the present technology can operate on or within a number of different computer systems including general purpose networked computer systems, embedded computer systems, routers, switches, server devices, user devices, various intermediate devices/artifacts, stand-alone computer systems, mobile phones, personal data assistants, televisions and the like. As shown in FIG. 8, computer system 800 of FIG. 8 is well adapted to having peripheral computer readable media 802 such as, for example, a disk, a compact disc, a flash drive, and the like coupled thereto.

[0128] Computer system 800 of FIG. 8 includes an address/data/control bus 804 for communicating information, and a processor 805A coupled to bus 804 for processing information and instructions. As depicted in FIG. 8, computer system 800 is also well suited to a multi-processor environment in which a plurality of processors 805A, 805B, and 805C are present. Conversely, computer system 800 is also well suited to having a single processor such as, for example, processor 805A. Processors 805A, 805B, and 805C may be any of various types of microprocessors. Computer system 800 also includes data storage features such as a computer usable volatile memory 808, e.g., random access memory (RAM), coupled to bus 804 for storing information and instructions for processors 805A, 805B, and 805C.

[0129] Computer system 800 also includes computer usable non-volatile memory 810, e.g., read only memory (ROM), coupled to bus 804 for storing static information and instructions for processors 805A, 805B, and 805C. Also present in computer system 800 is a data storage unit 812 (e.g., a magnetic disk drive, optical disk drive, solid state drive (SSD), and the like) coupled to bus 804 for storing information and instructions. Computer system 800 also can optionally include an alpha-numeric input device 814 including alphanumeric and function keys coupled to bus 804 for communicating information and command selections to processor 805A or processors 805A, 805B, and 805C. Computer system 800 also can optionally include a cursor control device 815 coupled to bus 804 for communicating user input information and command selections to processor 805A or processors 805A, 805B, and 805C. Cursor control device may be a touch sensor, gesture recognition device, and the like. Computer system 800 of the present embodiment can optionally include a display device 818 coupled to bus 804 for displaying information.

[0130] Referring still to FIG. 8, display device 818 of FIG. 8 may be a liquid crystal device, cathode ray tube, OLED, plasma display device or other display device suitable for creating graphic images and alpha-numeric characters recognizable to a user. Cursor control device 815 allows the computer user to dynamically signal the movement of a visible symbol (cursor) on a display screen of display device 818. Many implementations of cursor control device 815 are known in the art including a trackball, mouse, touch pad, joystick, non-contact input, gesture recognition, voice commands, bio recognition, and the like. In addition, special keys on alpha-numeric input device 814 capable of signaling movement of a given direction or manner of displacement. Alternatively, it will be appreciated that a cursor can be directed and/or activated via input from alpha-numeric input device 814 using special keys and key sequence commands.

[0131] Computer system 800 is also well suited to having a cursor directed by other means such as, for example, voice commands. Computer system 800 also includes an I/O device 820 for coupling computer system 800 with external entities. For example, in one embodiment, I/O device 820 is a modem for enabling wired or wireless communications between computer system 800 and an external network such as, but not limited to, the Internet or intranet. A more detailed discussion of the present technology is found below.

[0132] Referring still to FIG. 8, various other components are depicted for computer system 800. Specifically, when present, an operating system 822, applications 824, modules 825, and data 828 are shown as typically residing in one or some combination of computer usable volatile memory 808, e.g. random-access memory (RAM), and data storage unit 812. However, it is appreciated that in some embodiments, operating system 822 may be stored in other locations such as on a network or on a flash drive; and that further, operating system 822 may be accessed from a remote location via, for example, a coupling to the internet. In one embodiment, the present technology, for example, is stored as an application 824 or module 825 in memory locations within RAM 808 and memory areas within data storage unit 812. The present technology may be applied to one or more elements of described computer system 800.

[0133] Computer system 800 also includes one or more signal generating and receiving device(s) 830 coupled with bus 804 for enabling computer system 800 to interface with other electronic devices and computer systems. Signal generating and receiving device(s) 830 of the present embodiment may include wired serial adaptors, modems, and network adaptors, wireless modems, and wireless network adaptors, and other such communication technology. The signal generating and receiving device(s) 830 may work in conjunction with one (or more) communication interface 832 for coupling information to and/or from computer system 800. Communication interface 832 may include a serial port, parallel port, Universal Serial Bus (USB), Ethernet port, Bluetooth, thunderbolt, near field communications port, WiFi, Cellular modem, or other input/output interface. Communication interface 832 may physically, electrically, optically, or wirelessly (e.g., via radio frequency) couple computer system 800 with another device, such as a mobile phone, radio, or computer system.

[0134] Computer system 800 is only one example of a suitable computing environment and is not intended to suggest any limitation as to the scope of use or functionality of the present technology. Neither should the computing environment be interpreted as having any dependency or requirement relating to any one or combination of components illustrated in the example computer system 800.