Methods And Systems For Provisioning Payment Credentials

Huxham; Horatio ; et al.

U.S. patent application number 16/230821 was filed with the patent office on 2019-04-25 for methods and systems for provisioning payment credentials. The applicant listed for this patent is Visa International Service Association. Invention is credited to Horatio Huxham, Tara Anne Moss, Alan Joseph O'Regan, John F. Sheets, Hough Arie Van Wyk.

| Application Number | 20190122212 16/230821 |

| Document ID | / |

| Family ID | 51897836 |

| Filed Date | 2019-04-25 |

View All Diagrams

| United States Patent Application | 20190122212 |

| Kind Code | A1 |

| Huxham; Horatio ; et al. | April 25, 2019 |

METHODS AND SYSTEMS FOR PROVISIONING PAYMENT CREDENTIALS

Abstract

A method and system for provisioning payment credentials usable by a mobile device in conducting a payment. The method is conducted at a provisioning system and comprises the steps of: receiving payment credentials from a receiving device, the payment credentials having been obtained from a portable payment device presented by a consumer at the receiving device; receiving, from the receiving device, an identifier entered by the consumer; identifying a mobile device or a secure element corresponding to the identifier; and communicating the payment credentials or a derivation of the payment credentials to the identified mobile device or the secure element to be securely stored in association with the mobile device. The method may include: encrypting the received payment credentials, the encrypted payment credentials having a unique decryption key; and wherein communicating a derivation of the payment credentials communicates the unique decryption key.

| Inventors: | Huxham; Horatio; (Cape Town, ZA) ; O'Regan; Alan Joseph; (Cape Town, ZA) ; Moss; Tara Anne; (Cape Town, ZA) ; Van Wyk; Hough Arie; (Cape Town, ZA) ; Sheets; John F.; (San Francisco, CA) | ||||||||||

| Applicant: |

|

||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Family ID: | 51897836 | ||||||||||

| Appl. No.: | 16/230821 | ||||||||||

| Filed: | December 21, 2018 |

Related U.S. Patent Documents

| Application Number | Filing Date | Patent Number | ||

|---|---|---|---|---|

| 14889714 | Nov 6, 2015 | 10198728 | ||

| PCT/IB2014/061471 | May 15, 2014 | |||

| 16230821 | ||||

| 61823840 | May 15, 2013 | |||

| Current U.S. Class: | 1/1 |

| Current CPC Class: | G07F 19/204 20130101; G06Q 20/3278 20130101; G06Q 20/3226 20130101; G06Q 20/38215 20130101; G06Q 20/18 20130101; G06Q 20/401 20130101; G06Q 20/3229 20130101; G06Q 20/36 20130101; G06Q 20/3829 20130101; G06Q 20/382 20130101; G06Q 20/3227 20130101 |

| International Class: | G06Q 20/38 20060101 G06Q020/38; G06Q 20/32 20060101 G06Q020/32; G06Q 20/40 20060101 G06Q020/40; G07F 19/00 20060101 G07F019/00; G06Q 20/36 20060101 G06Q020/36; G06Q 20/18 20060101 G06Q020/18 |

Foreign Application Data

| Date | Code | Application Number |

|---|---|---|

| May 22, 2013 | ZA | 2013/03719 |

| Aug 20, 2013 | ZA | 2013/06249 |

Claims

1.-30. (canceled)

31. A method comprising the steps of: storing, by a mobile device or a secure element associated with the mobile device, a decryption key; receiving, by the mobile device or the secure element associated with the mobile device from a remote server computer, a request for the decryption key; and providing, by the mobile device to the remote server computer, the decryption key, wherein the remote server computer decrypts encrypted payment credentials stored by the remote server computer to form decrypted payment credentials, and transmits the decrypted payment credentials to a receiving device.

32. The method of claim 31, further comprising: storing the encrypted payment credentials at the remote server computer.

33. The method of claim 31, wherein the remote server computer further communicates additional credentials to the receiving device, wherein the additional credentials are required in use in addition to the decrypted payment credentials or derivation of the decrypted payment credentials to carry out a transaction.

34. The method of claim 31, wherein the secure element is one of the group of: a secure element provided in the mobile device, a secure element embedded in a layer which sits between a communication component of the mobile device and a communication component interface of the mobile device, a secure element provided in a communication component of the mobile device, and a cloud-based secure element associated with the mobile device.

35. The method of claim 31, wherein the decrypted payment credentials comprise a PAN.

36. The method of claim 31, wherein the decrypted payment credentials are transmitted to the receiving device in a single secure transaction message.

37. The method of claim 31, wherein the method further includes: determining whether or not the mobile device or the secure element corresponding to a personal identifier has been registered with the remote server computer.

38. The method of claim 31, wherein the decrypted payment credentials are also on a portable payment device used by a user of the mobile device.

39. A mobile device comprising: a processor; and a computer readable medium, the computer readable medium comprising code, executable by the processor for implementing a method comprising: storing, by the mobile device, a decryption key, receiving, by the mobile device from a remote server computer, a request for the decryption key; and providing, by the mobile device to the remote server computer, the decryption key, wherein the remote server computer decrypts encrypted payment credentials stored by the remote server computer to form decrypted payment credentials, and transmits the decrypted payment credentials to a receiving device.

40. The mobile device of claim 39, wherein the method further comprises: storing the encrypted payment credentials at the remote server computer.

41. The mobile device of claim 39, wherein the remote server computer further communicates additional credentials to the receiving device, wherein the additional credentials are required in use in addition to the decrypted payment credentials or derivation of the decrypted payment credentials to carry out a transaction.

42. The mobile device of claim 39, wherein the mobile device comprises a secure element, the secure element is one of the group of: a secure element provided in the mobile device, a secure element embedded in a layer which sits between a communication component of the mobile device and a communication component interface of the mobile device, a secure element provided in a communication component of the mobile device, and a cloud-based secure element associated with the mobile device.

43. The mobile device of claim 39, wherein the decrypted payment credentials comprise a PAN.

44. The mobile device of claim 39, wherein the decrypted payment credentials are transmitted to the receiving device in a single secure transaction message.

45. The mobile device of claim 39, wherein the method further includes: determining whether or not the mobile device corresponding to a personal identifier has been registered with the remote server computer.

46. The mobile device of claim 39, wherein the decrypted payment credentials are also on a portable payment device used by a user of the mobile device.

47. A secure element associated with a mobile device, the secure element comprising: a computer readable medium, the computer readable medium comprising code, executable by a processor for implementing a method comprising: storing, by the secure element associated with the mobile device, a decryption key, receiving, the secure element associated with the mobile device from a remote server computer, a request for the decryption key; and providing, by the secure element to the remote server computer, the decryption key, wherein the remote server computer decrypts encrypted payment credentials stored by the remote server computer to form decrypted payment credentials, and transmits the decrypted payment credentials to a receiving device.

48. The secure element of claim 47, wherein the method further comprises: storing the encrypted payment credentials at the remote server computer.

49. The secure element of claim 47, wherein the remote server computer further communicates additional credentials to the receiving device, wherein the additional credentials are required in use in addition to the decrypted payment credentials or derivation of the decrypted payment credentials to carry out a transaction.

50. The secure element of claim 47, wherein the secure element is one of the group of: a secure element provided in the mobile device, a secure element embedded in a layer which sits between a communication component of the mobile device and a communication component interface of the mobile device, a secure element provided in a communication component of the mobile device, and a cloud-based secure element associated with the mobile device.

Description

CROSS-REFERENCES TO RELATED APPLICATIONS

[0001] This application claims priority from, and incorporates by reference, U.S. Provisional Patent Application No. 61/823,840 filed on 15 May 2013 entitled "Mobile Device Provisioning Kiosk", South African Provisional Patent Application No. 2013/03719 filed on 22 May 2013 entitled "Provisioning Payment Credentials to a Mobile Device" and South African Provisional Patent Application No. 2013/06249 filed on 20 Aug. 2013 entitled "Provisioning Payment Credentials to a Remotely Accessible Server".

FIELD OF INVENTION

[0002] This application relates to the field of provisioning payment credentials usable by a mobile device.

BACKGROUND

[0003] As more merchants are adopting of point-of-sale terminals that are capable of conducting transactions with mobile devices, consumers are more and more likely to replace their physical wallets with digital wallet applications running on their mobile devices (e.g., mobile phones). Transactions with digital wallet applications running on a mobile device may be contactless, for example, using near field communication (NFC) capabilities of the mobile device.

[0004] Contactless payment transactions provide significant convenience to consumers as they allow consumers to make purchases more quickly and conveniently than in a contact-based environment. In a contactless payment transaction, a consumer brings a contactless enabled consumer portable payment device (CPPD) such as a contactless smart card or a mobile phone in close proximity with an acceptance terminal. Information such as payment credentials is exchanged between the contactless CPPD and the acceptance terminal in a wireless manner to carry out the payment transaction without requiring direct physical contact between the contactless CPPD and the acceptance terminal. In some cases, the contactless CPPD and the acceptance terminal are not collocated, but may rather be in different locations, for example, in different cities or countries. In such a case the information is transmitted between the contactless CPPD and the acceptance terminal via, for example, the Internet.

[0005] It is often required by various standards or compliance authorities that a mobile device being employed as a contactless CPPD contains a secure element. Such a secure element is not unlike a secure integrated circuit used in conventional CPPDs, such as secure integrated circuit credit cards. The secure elements which are in communication with the mobile devices typically provide a secure memory and secure processor which are separate from the mobile device memory and processor and can only be accessed by trusted applications, often only after a specified personal identification number (PIN) has been correctly entered. The mobile devices in which such secure elements are disposed or embedded are often equipped with proximity communications interfaces such as, for example, near field communications (NFC).

[0006] It is in this secure memory that information, such as payment credentials, may be stored. In some cases, the provisioning of such payment credentials to the secure memory of the mobile device may be via over-the-air (OTA) communications methods originating from a trusted service manager (TSM). Such TSMs are typically operated from secure data centers such that the process meets security standards imposed by relevant standards or compliance authorities.

[0007] Provisioning digital wallet applications on mobile devices can be a cumbersome task. For example, in order to provision a mobile device with the credentials to conduct contactless transactions such as contactless payment transactions, users may be required to access a contactless transaction service provider from their mobile device to carry out an OTA provisioning process. The provisioning process may require the user to manually enter user credentials such as account numbers. As most consumers likely have many credential storage instruments such as credit/debit cards from different banks that the user would like to include in the digital wallet application, entering this information for all credential storage instruments of a user can be a time consuming process. Furthermore, the OTA provisioning process may incur undesirable wireless data usage charges for the user.

[0008] Embodiments of the invention aim to address these and other problems individually and collectively, at least to some extent.

BRIEF SUMMARY

[0009] According to a first aspect of the present invention there is provided a method for provisioning payment credentials usable by a mobile device in conducting a payment, the method being conducted at a provisioning system and comprising the steps of: receiving payment credentials from a receiving device, the payment credentials having been obtained from a portable payment device presented by a consumer at the receiving device; receiving, from the receiving device, an identifier entered by the consumer; identifying a mobile device or a secure element associated with the mobile device corresponding to the identifier; and communicating the payment credentials or a derivation of the payment credentials to the identified mobile device or the secure element to be securely stored in association with the mobile device.

[0010] The method may additionally include: encrypting the received payment credentials, the encrypted payment credentials having a unique decryption key. The payment credentials may be communicated in encrypted form with the unique decryption key being stored at the provisioning system. In one embodiment, communicating a derivation of the payment credentials communicates the unique decryption key and the encrypted payment credentials are stored at the provisioning system. In the case where the unique decryption key is communicated, the unique decryption key may be purged from the provisioning system.

[0011] In embodiments of the method, the provisioning system is a remotely accessible server of an issuing authority, a security gateway, or trusted service manager, and wherein communicating the payment credentials or a derivation of the payment credentials to the identified mobile device or the secure element uses a secure channel of communication.

[0012] In alternative embodiments of the method, the provisioning system is a kiosk having a processor local to the receiving device, and wherein the method includes: establishing a communication channel between the kiosk and the mobile device for communicating the payment credentials or a derivation of the payment credentials. The kiosk may act as an intermediary for a remotely accessible server and the method may includes using the received identifier to identify and/or verify a user or account at a remotely accessible server.

[0013] The method may include: requesting authorization from a trusted service manager to access a secure element; and receiving a security key to access the secure element.

[0014] The method may further include: communicating additional credentials to the identified mobile device or the secure element to be securely stored in association with the mobile device, wherein the additional credentials are required in use in addition to the payment credentials or derivation of the payment credentials to carry out a transaction. In one embodiment, the additional credentials may be card verification values. In another embodiment, the additional credentials may be in the form of a dynamic verification application or algorithm for generating dynamic verification values. The method may include obtaining the additional credentials from a remotely accessible server using the identifier and forwarding the additional credentials to the mobile device.

[0015] The receiving device may be one of the group of: a card reader associated with a kiosk, a point of sales device, an automated teller machine, a merchant point of sales terminal, or a personal PIN entry device (PPED).

[0016] The portable payment device may be one of the group of: a magnetic stripe credit or debit card, a security integrated circuit credit or debit card, a bank card, a contactless bank card, a voucher card, an existing payment credential stored on a mobile device.

[0017] The received payment credentials may include receiving one or more of track 1 data, track 2 data, track 3 data and track 2 equivalent data. The received payment credentials may include one or more of the group of: track data, an account number, account holder name and/or date of birth, a bank identification number (BIN), a primary account number (PAN), a service code, an expiration date, card verification values (CVV1 or CVV2), personal details of an account holder, a PIN block or offset, a bank account number, a branch code, a loyalty account number or identifier, credit and/or debit card number information, account balance information.

[0018] The identifier may be one or more of the group of: a mobile station international subscriber directory number (MSISDN), an email address, a social network identifier, a predefined consumer name, a consumer account number.

[0019] The step of receiving payment credentials and the step of receiving an identifier may include receiving a single secure transaction message containing the payment credentials and the identifier. The secure transaction message may be one of the group of: a payment processing network message, a financial transaction message, a financial transaction message in the form of an ISO8583 message, a financial transaction message containing a server routing code. The server routing code may be used to route the financial transaction message to the remotely accessible server by a payment processing network.

[0020] Identifying a mobile device or a secure element corresponding to the identifier may include: determining whether or not a mobile device or secure element corresponding to the identifier has been registered with a remotely accessible server and, if the mobile device or has been registered, identifying a corresponding communication address of the mobile device and/or secure element.

[0021] Further features provide for the step of identifying a mobile device corresponding to the identifier to include the step of using the identifier to query a database so as to obtain a communication address of the mobile device associated with the identifier. Further features provide for the step of communicating the payment credentials to the mobile device to include communicating the payment credentials to the mobile device using the communication address.

[0022] Communicating the payment credentials or a derivation of the payment credentials to the identified mobile device to be securely stored in association with the mobile device, may include: communicating the payment credentials or a derivation of the payment credentials to the mobile device to be stored in a secure element, wherein the secure element is one of the group of: a secure element provided in the mobile device, a secure element embedded in a layer which sits between a communication component of the mobile device and a communication component interface of the mobile device, a secure element provided in a communication component of the mobile device, a cloud-based secure element associated with the mobile device. In one embodiment, the secure element may be embedded in a label, card or tray and which sits in between a communication component of the mobile device and a communication component interface of the mobile device.

[0023] The method may be repeated for multiple payment credentials to be securely stored in association with a single mobile device.

[0024] The method may be used for transferring payment credentials to a second mobile device from their existing secure storage on a first mobile device, wherein the portable payment device is an existing payment credential securely stored on the first mobile device.

[0025] According to second aspect of the present invention there is provided a method for provisioning payment credentials usable by a mobile device in conducting a payment, the method being conducted at a point of sales device and comprising the steps of: obtaining payment credentials from a portable payment device presented by a consumer at a receiving device; receiving an identifier entered by the consumer into the point of sales device; communicating the payment credentials and identifier to a remotely accessible server for further communication of the payment credentials or a derivation of the payment credentials to a mobile device or a secure element to be securely stored in association with the mobile device.

[0026] According to a third aspect of the present invention there is provided a system for provisioning payment credentials usable by a mobile device in conducting a payment, including a provisioning system comprising: a payment credentials receiver for receiving payment credentials from a receiving device, the payment credentials having been obtained from a portable payment device presented by a consumer at the receiving device; an identifier receiver for receiving, from the receiving device, an identifier entered by the consumer; an identifying component for identifying a mobile device or a secure element associated with the mobile device corresponding to the identifier; and a communication module for communicating the payment credentials or a derivation of the payment credentials to the identified mobile device or the secure element to be securely stored in association with the mobile device.

[0027] The provisioning system may include: an encryption component for encrypting the received payment credentials, the encrypted payment credentials having a unique decryption key; and wherein communicating a derivation of the payment credentials communicates the unique decryption key.

[0028] In embodiments of the system, the provisioning system is a remotely accessible server of an issuing authority, a security gateway, or trusted service manager, and wherein the communication module for communicating the payment credentials or a derivation of the payment credentials to the identified mobile device or the secure element uses a secure channel of communication.

[0029] In alternative embodiments, the provisioning system is a kiosk having a processor local to the receiving device, and wherein the kiosk includes the communication module for establishing a communication channel between the kiosk and the mobile device for communicating the payment credentials or a derivation of the payment credentials. The kiosk may act as an intermediary for a remotely accessible server and the system includes a server communication module for using the received identifier to identify and/or verify a user or account at the remotely accessible server.

[0030] The provisioning system may further includes: an authorization component for requesting authorization from a trusted service manager to access a secure element and receiving a security key to access the secure element.

[0031] The provisioning system may further include: an additional credentials component for communicating additional credentials to the identified mobile device or the secure element to be securely stored in association with the mobile device, wherein the additional credentials are required in use in addition to the payment credentials or derivation of the payment credentials to carry out a transaction. In one embodiment, the additional credentials may be card verification values. In another embodiment, the additional credentials may be in the form of a dynamic verification application or algorithm for generating dynamic verification values. The method may include obtaining the additional credentials from a remotely accessible server using the identifier and forwarding the additional credentials to the mobile device.

[0032] The identifying component for identifying a mobile device corresponding to the identifier may include functionality for determining whether or not a mobile device or a secure element corresponding to the identifier has been registered with a remotely accessible server and, if the mobile device has been registered, identifying a corresponding communication address of the mobile device or secure element.

[0033] The communication module for communicating the payment credentials or a derivation of the payment credentials to the identified mobile device to be securely stored in association with the mobile device, includes functionality for communicating the payment credentials or a derivation of the payment credentials to the mobile device to be stored in a secure element, wherein the secure element is one of the group of: a secure element provided in the mobile device, a secure element embedded in a layer which sits between a communication component of the mobile device and a communication component interface of the mobile device, a secure element provided in a communication component of the mobile device, a cloud-based secure element associated with the mobile device.

[0034] In further embodiments, the system may include: a point of sales device comprising: a payment credentials obtaining component for obtaining payment credentials from a portable payment device presented by a consumer at the receiving device; an identifier receiver for receiving an identifier entered by the consumer into the point of sales device; a communication module for communicating the payment credentials and identifier to a remotely accessible server for further communication of the payment credentials or a derivation of the payment credentials to a mobile device to be securely stored in association with the mobile device.

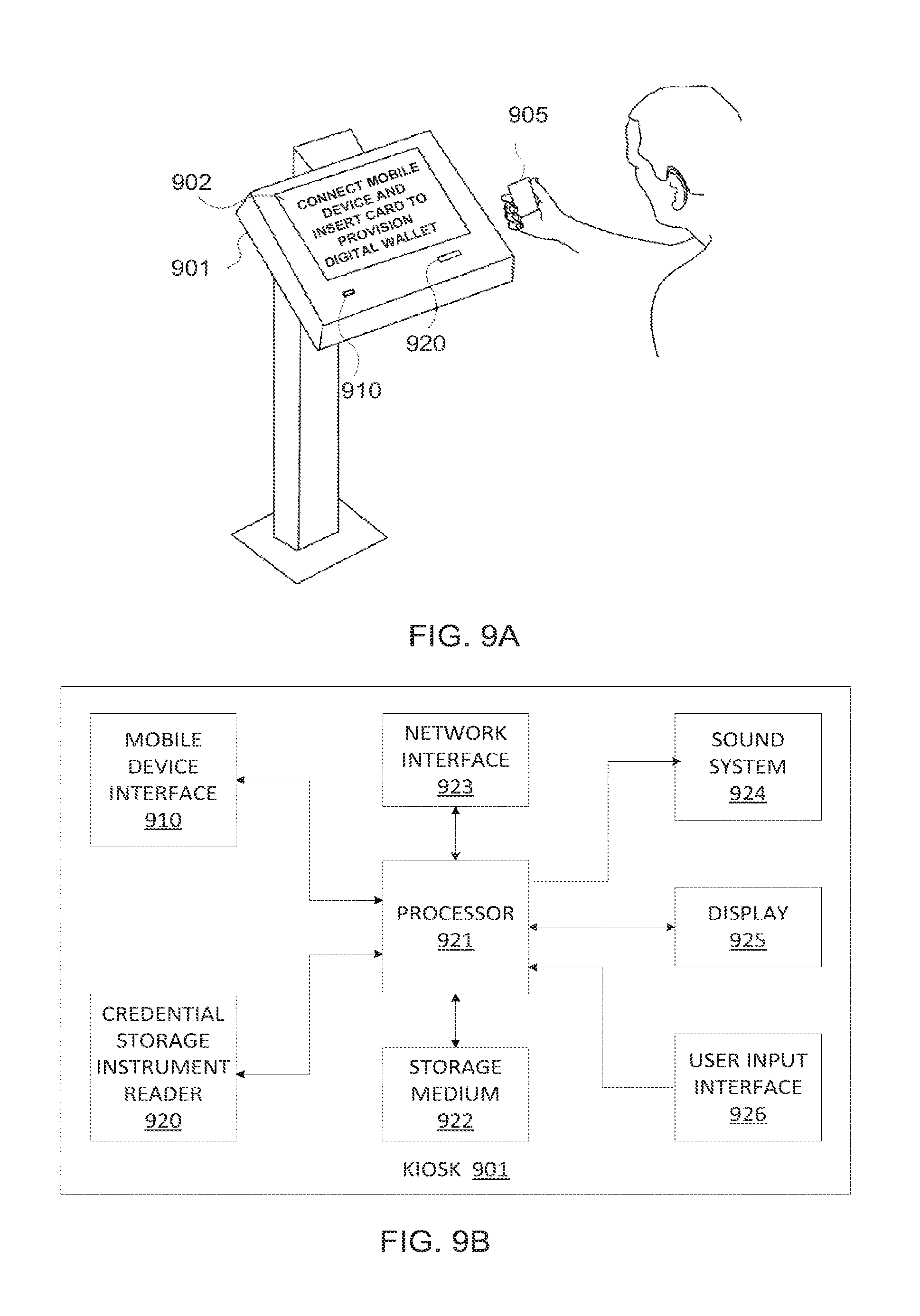

[0035] In a further aspect of the present invention, a kiosk is provided to allow a user to provision a mobile device with credentials from the user's credential storage instruments also referred to as portable payment devices. The kiosk includes a credential storage instrument reader to retrieve credentials from a credential storage instrument. The kiosk also includes a mobile device interface to establish a communication channel with a mobile device, and to load credentials from the credential storage instrument onto the mobile device via the communication channel.

[0036] According to a fourth aspect of the present invention there is provided a computer program product for provisioning payment credentials usable by a mobile device in conducting a payment, the computer program product comprising a computer-readable medium having stored computer-readable program code for performing the steps of the first aspect of the present invention and one or more additionally defined features listed above.

[0037] According to a fifth aspect of the present invention there is provided a computer program product for provisioning payment credentials usable by a mobile device in conducting a payment, the computer program product comprising a computer-readable medium having stored computer-readable program code for performing the steps of the second aspect of the present invention and one or more additionally defined features listed above.

[0038] Further features of the invention provide for the computer-readable medium to be a non-transitory computer-readable medium and for the computer-readable program code to be executable by a processing circuit.

[0039] In order for the invention to be more fully understood, implementations thereof will now be described with reference to the accompanying drawings.

BRIEF DESCRIPTION OF THE DRAWINGS

[0040] FIG. 1 is a schematic diagram of a first embodiment of a system in accordance with the present invention;

[0041] FIG. 2 is a schematic diagram of showing variations to the first embodiment FIG. 1;

[0042] FIG. 3 is a schematic diagram of showing variations to the first embodiment FIG. 1;

[0043] FIG. 4A is a flow diagram of a method carried out at a provisioning system in accordance with the present invention;

[0044] FIG. 4B is a flow diagram of an embodiment of the method of FIG. 4A;

[0045] FIG. 5 is a flow diagram of a method carried out at a point of sale device in accordance with the present invention;

[0046] FIG. 6A is a block diagram of an aspect of a system in accordance with the present invention;

[0047] FIG. 6B is a block diagram of an aspect of a system in accordance with the present invention;

[0048] FIG. 7 is a swim-lane flow diagram of an embodiment of a method in accordance with the present invention;

[0049] FIG. 8 is a swim-lane flow diagram of another embodiment of a method in accordance with the present invention;

[0050] FIG. 9A illustrates a second embodiment of a system in accordance with the present invention;

[0051] FIG. 9B is a block diagram of a kiosk of the embodiment of the system of FIG. 9A;

[0052] FIG. 9C is a schematic diagram of a system of the embodiment of FIG. 9A;

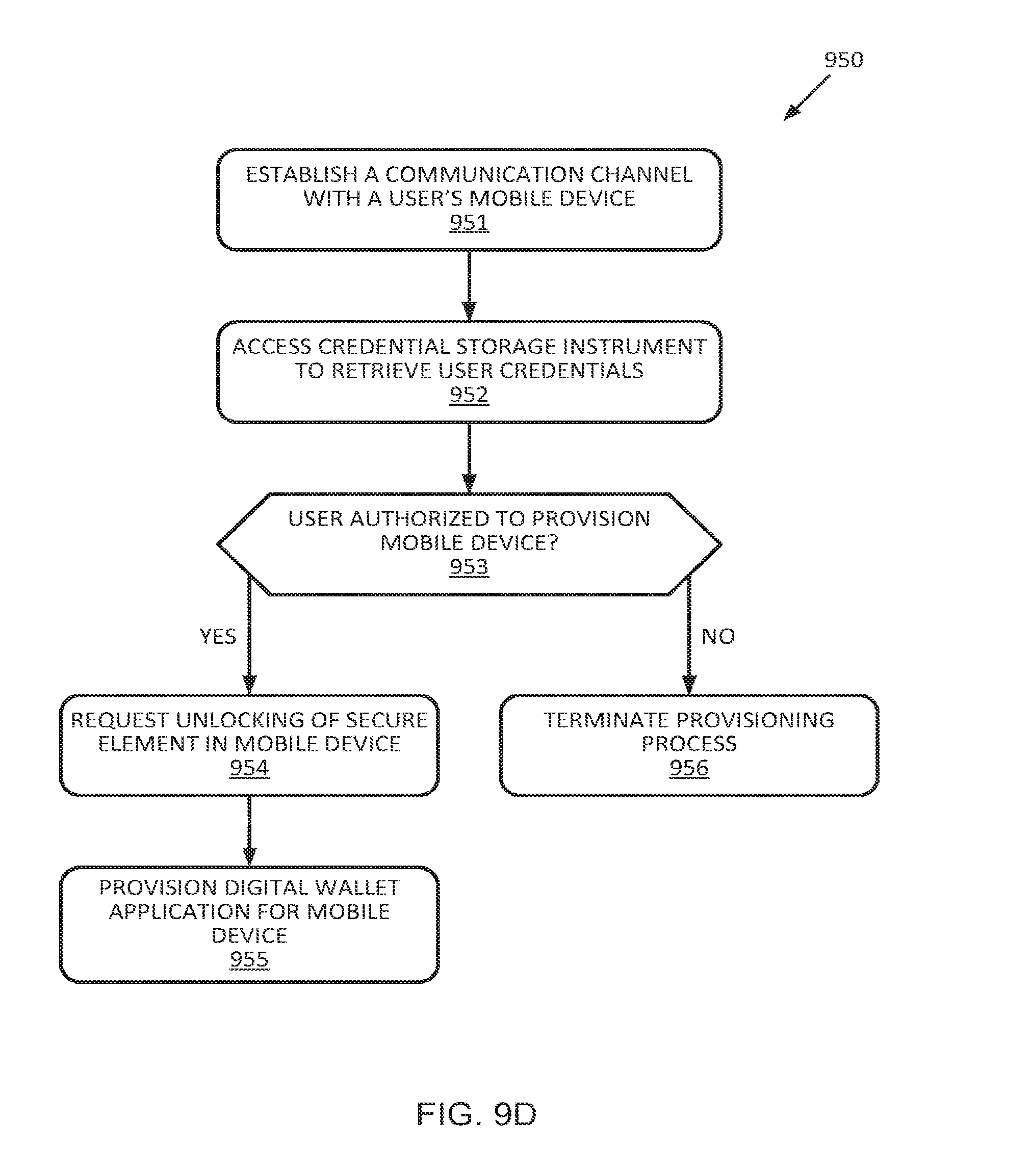

[0053] FIG. 9D is a flow diagram of a method of the embodiment of FIG. 9A;

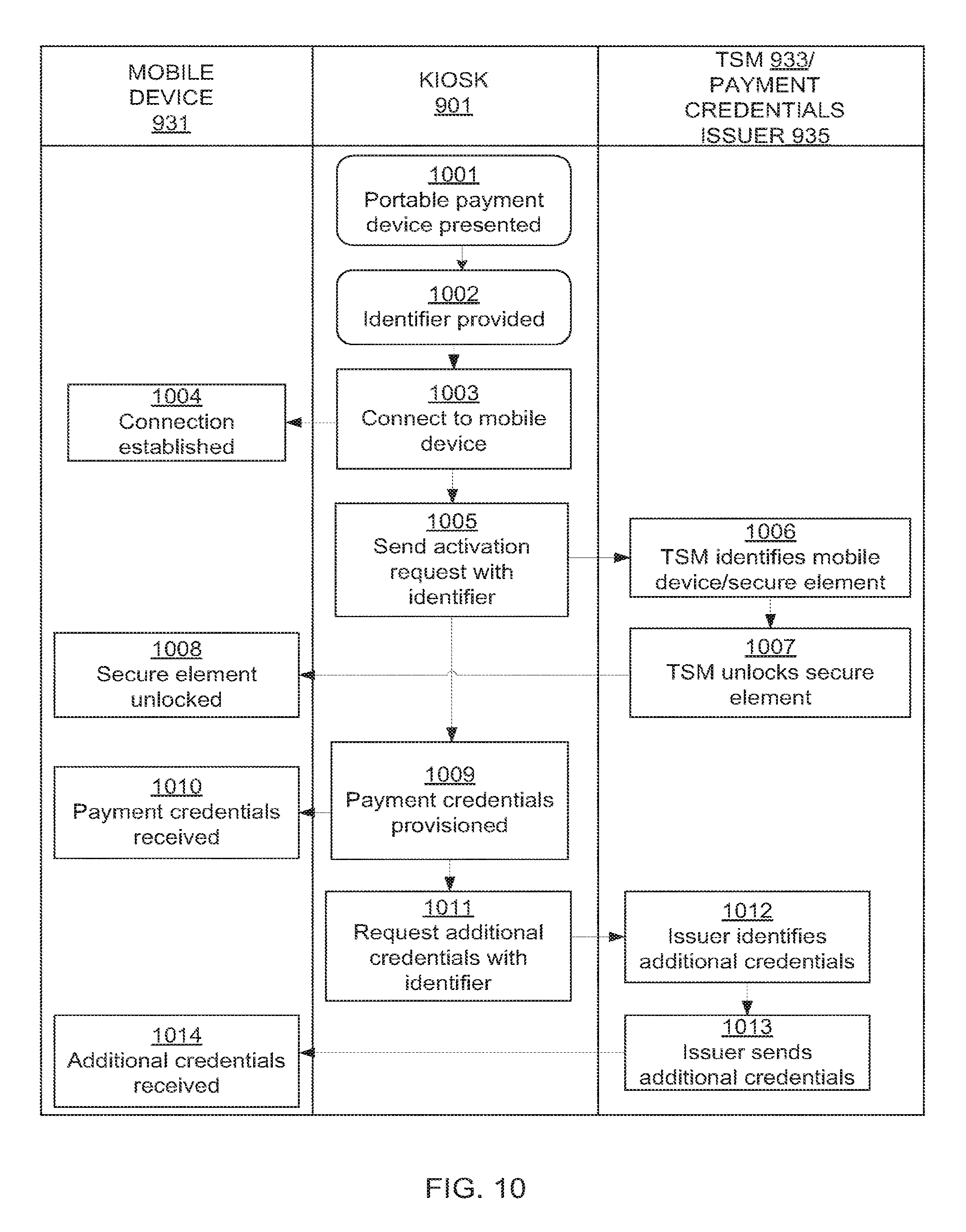

[0054] FIG. 10 is a swim-lane flow diagram of the embodiment of FIG. 9A;

[0055] FIG. 11 illustrates a block diagram of a computing device in which various aspects of the invention may be implemented; and

[0056] FIG. 12 illustrates a block diagram of a communication device that can be used in various embodiments of the invention.

DETAILED DESCRIPTION

[0057] In the following detailed description, numerous specific details are set forth in order to provide a thorough understanding of the invention. However, it will be understood by those skilled in the art that the present invention may be practiced without these specific details. In other instances, well-known methods, procedures, and components have not been described in detail so as not to obscure the present invention.

[0058] Methods and systems for provisioning payment credentials or derivations of payment credentials usable by a mobile device in conducting a contactless payment are described.

[0059] Embodiments of the invention include a method carried out at a remotely accessible server for provisioning payment credentials or derivations thereof to a mobile device via a receiving device at which a portable payment device or credential storage instrument such as a payment card may be input. The receiving device may be, for example, a point-of-sale device, an automated teller machine, or other intermediary device.

[0060] The payment credentials may be provisioned securely to the mobile device from the remotely accessible server via channels to a secure element associated with the mobile device.

[0061] The payment credentials may be provisioned to the mobile device or, alternatively, the payment credentials may be stored at the remotely accessible server in an encrypted form and a unique decryption key may be provisioned to the mobile device.

[0062] Other embodiments of the invention provide a kiosk to allow a user to provision a mobile device with credentials from the user's credential storage instruments. By providing a kiosk as an interface between the user's mobile device and the user's credential storage instruments, manual input of the credentials can be avoided because such credentials can be read directly from the user's credential storage instruments. Furthermore, the kiosk can act as a communication intermediary between the mobile device and entities involved in the provisioning process such as an issuer or a trusted service manager to avoid wireless data usage on the mobile device during the provisioning process. Thus, embodiments of the present invention provide a convenient and cost-effective way to enable mobile devices with digital wallet applications for use in contactless transactions.

[0063] These and additional embodiments are now described in detail.

[0064] FIG. 1 illustrates a block diagram of an exemplary system (100) according to embodiments of the invention. The system includes a mobile device (112) and a portable payment device (114) of a consumer (102). The system further includes a receiving device for the portable payment device (114) and, in this embodiment, the receiving device is in the form of a point of sales device (120). The system further includes a remotely accessible server (140) which, in the exemplary system (100), is in communication with the point of sales device (120) via a payment processing network (130). While the figure only shows one consumer (102), one mobile device (112), one portable payment device (114) and one point of sales device (120), it will be appreciated that this is purely for illustrative purposes and that the invention anticipates one or more of each.

[0065] The mobile device (112) may be any suitable mobile device having a secure element (113). The secure element (113) may be embedded in the mobile device, disposed within a micro secure digital (SD) or similar card form factor which is placed in a micro SD card slot of the mobile device (112).

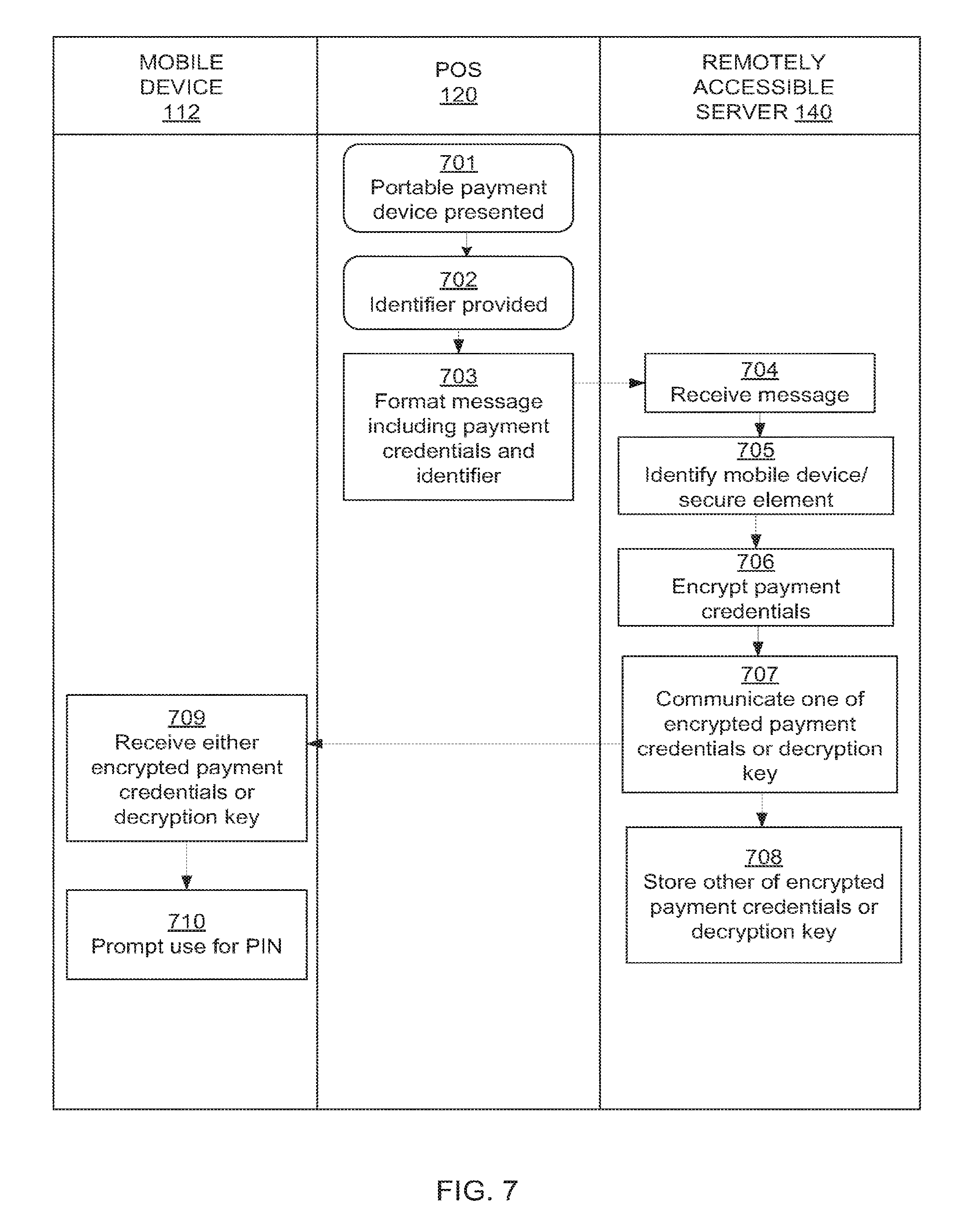

[0066] Alternatively, the secure element (113) may be disposed within a communication component of the mobile device, such as a universal integrated circuit card (UICC). It is also anticipated that in some embodiments the secure element (113) may be disposed in an expansion device which may be connected to a mobile device or alternatively disposed within, for example a label, tray or card which is then placed in between a UICC and a UICC interface of the mobile device such that the secure element can intercept and appropriately process any communication sent between the UICC and the mobile device and consequently, between the mobile device and a mobile communication network.

[0067] It is further anticipated that the secure element (113) may be a cloud-based secure element using host card emulation (HCE) which enables network-accessible storage external to the mobile device (112) with an application on the mobile device (112) configured to emulate the card functions.

[0068] Exemplary mobile devices include smart phones, feature phones, tablet computers, personal digital assistants, or the like. The mobile device (112) is in data communication with the remotely accessible server over, for example a mobile data or mobile communication network, and is at least configured to securely receive, store, release and transmit payment credentials or derivations of payment credentials. For instance, the mobile device (112) may be any such device which meets any appropriate financial or payment scheme standards, such as, for example, the Global Platform Card Specification. Embodiments of the invention provide for an appropriate mobile software application to be resident on the mobile device (112) which allows a user thereof to interface with the secure element (113) coupled thereto, or associated with it in a cloud-based architecture, and which may also facilitate communications between the mobile device (112) and the secure element (113).

[0069] The software application may provide: a user interface to facilitate the entry of a passcode into the mobile device (112) to be compared to an offset stored in the secure element (113); a list from which users can select payment credentials to be used; notifications of receipt or use or payment credentials or the like. The user interface may include a menu from which at least some of these communications can be initiated. Embodiments of the invention further provide for such an interface to be provided by a SIM Application Toolkit protocol (commonly referred to as the STK protocol) implementation or the like.

[0070] The portable payment device (114) in the illustrated embodiment is a security integrated circuit bank card. Such cards are also known as `chip and pin` cards or `EMV smart cards`. The portable payment device (114) has payment credentials, which may be track 2 and/or track 2 equivalent information (such as EMV tag 57 data), stored therein. Track 2 and track 2 equivalent information may include a bank identification number (BIN), a primary account number (PAN), an expiration date, a service code, discretionary data such as card verification values (CVV) as well as any relevant spacing and redundancy checks. In addition to this, embodiments of the invention provide for the portable payment device (114) to contain payment credentials which may include any one or more of a customer name and/or date of birth, a BIN, a PAN, a service code, an expiration date, CVV1 or CVV2 numbers, a PIN block or offset, a bank account number, a branch code, a loyalty account number or identifier, credit and/or debit card number information, account balance information and/or other consumer information. In other embodiments of the invention, the payment credentials may include track 1 and/or track 3 information.

[0071] The point of sales device (120) may be any suitable device configured to obtain payment credentials from appropriate portable payment devices and to communicate these payment credentials to a payment processing network or financial institution network. The point of sales device (120) may be configured to obtain payment credentials from portable payment devices via any appropriate contact or contactless communications interface which may, for example be ISO/IEC 7813, ISO/IEC 7816 or ISO/IEC 14443 standards where applicable.

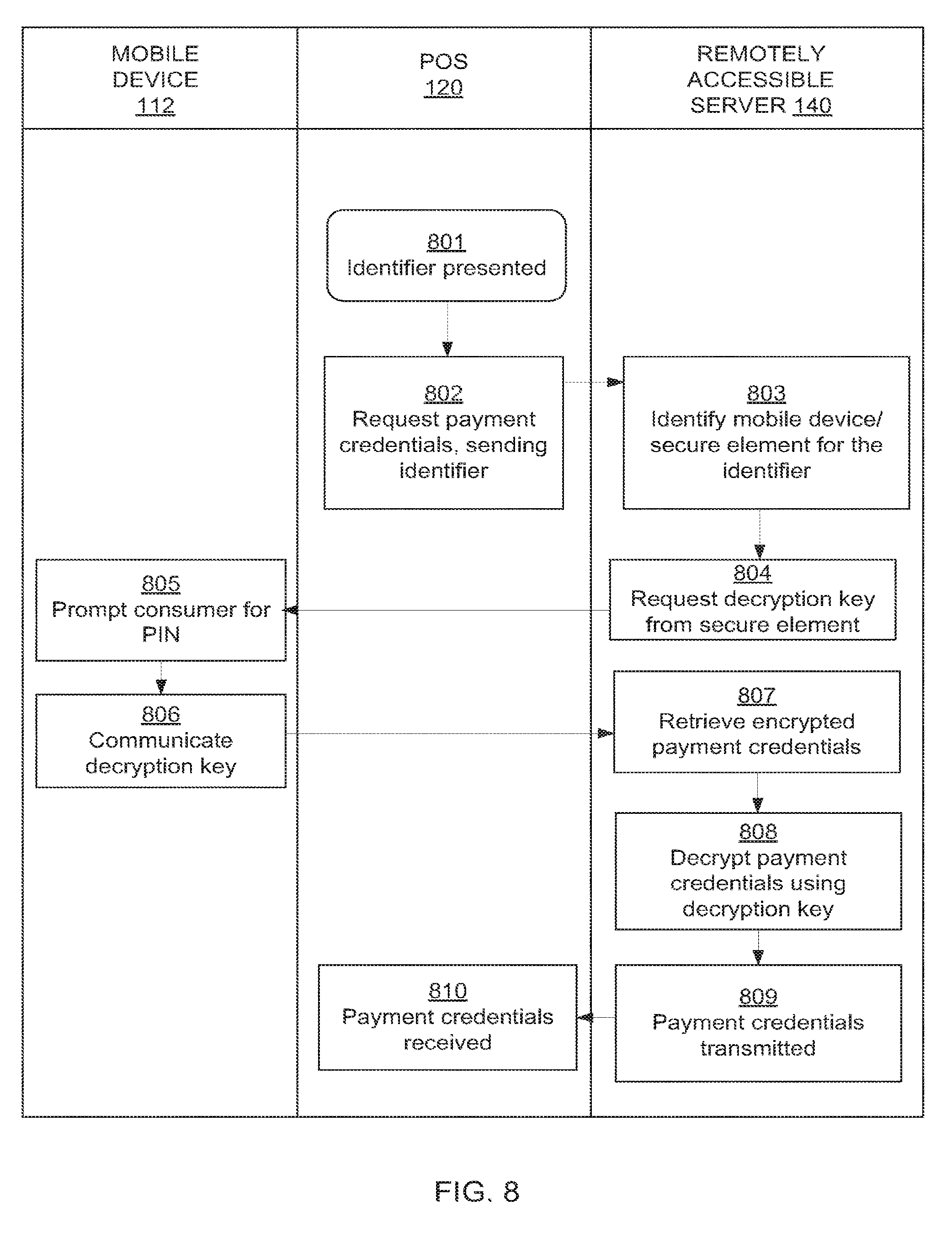

[0072] The point of sales device (120) may include one or more of various means for retrieving information from a portable payment device including the user placing the portable payment device (114) in physical contact with the point of sales device (120), for example, by swiping or inserting a magnetic stripe card into a magnetic stripe reader, or by inserting a chip-card into a chip-card reader slot, or the user placing the portable payment device (114) in close proximity with the point of sales device (120), for example, by placing a contactless card in close proximity to a contactless card reader, or by placing a printed medium, for example, with a bar code or quick response (QR) code in front of an infrared scanner.

[0073] In the illustrated exemplary system (100), the point of sales device (120) is a handheld point of sales device. In addition to this, the point of sales device (120) is configured to receive an identifier entered by a consumer via, for example, a keypad of the point of sales device (120).

[0074] The point of sales device (120) is further configured to format the payment credentials as well as the identifier into a financial transaction message and to communicate this message to the payment processing network (130). The financial transaction message may, for example, be an ISO 8583 message. Furthermore, the point of sales device (120) is configured to insert a server routing code into the financial transaction message such that the financial transaction message is routed to the remotely accessible server (140) by the payment processing network (130) using the server routing code. The server routing code may be placed in the `BIN` field of the financial transaction message.

[0075] The payment processing network (130) is a network of financial institutions and payment processing institutions and is configured to route financial transaction messages between, for example, merchants, acquirers, and issuers, amongst others. An example of such a payment processing network is VisaNet.TM. having a plurality of acquiring and issuing financial institutions being a part of the network.

[0076] The remotely accessible server (140) may be any appropriate sever computer or distributed server computer system and has a database (142) stored in a digital memory therein and also has a secure memory which, in a preferred embodiment is within a hardware security module (144) of the remotely accessible server. The remotely accessible server (140) is configured to receive payment credentials from a point of sales device (e.g. 120), where the payment credentials have been obtained from a portable payment device (e.g. 114) presented by a consumer (e.g. 102) at the point of sales device (120).

[0077] The remotely accessible server may be configured to encrypt the payment credentials, the encrypted payment credentials having a unique decryption key. The encryption may be performed in the hardware security module (144). In one embodiment, the key to decrypt the payment credentials is kept by the remotely accessible server (140) and the encrypted payment credentials are sent to the mobile device (112) for storage in the secure element (114) associated with the mobile device (112). In another embodiment, the encrypted payment credentials are stored in the hardware security module (144) of the remotely accessible server (140) and the decryption key is sent to the mobile device (112) for storage in the secure element (113) associated with the mobile device (112).

[0078] In addition to this, the remotely accessible server (140) is configured to receive an identifier from the point of sales device (120) which is entered by the consumer (102) into the point of sales device (120). The remotely accessible server (140) is configured to then identify a mobile device (e.g. 112), or a secure element (113) associated with a mobile device (112), corresponding to the identifier and to communicate the payment credentials to the mobile device (112) to be stored in a secure element (113) associated with the mobile device (112).

[0079] This may be performed by using the identifier to query the database (142) so as to obtain a communication address of the mobile device (112) associated with the identifier. The payment credentials can then be sent to the mobile device (112) using the communication address. The identifier received by the remotely accessible server may be, for example, any one or more of a mobile station international subscriber directory number (MSISDN), an email address, a social network identifier, a predefined consumer name, a consumer account number or the like. The communication address of the mobile device may similarly be, for example, any one or more of an MSISDN, an email address, a social network identifier, a predefined consumer name, a consumer account number or the like. The identifier and communication address may be the same.

[0080] Embodiments of the invention provide for the remotely accessible server to be configured to associate one or more of the group of: the identifier; decryption key; encrypted payment credentials; and communication address with a user profile in the database.

[0081] In some embodiments of the invention the role played by the remotely accessible server (140) may be similar to that of a trusted service manager (TSM) and accordingly may meet any security or data integrity requirements imposed by relevant financial or payment scheme standards, such as, for example, the Global Platform Card Specification.

[0082] In use, a consumer (102) may wish to provision his or her payment credentials or a derivation thereof to a secure element (113) on his or her mobile device (112) such that the mobile device (112) may be used to conduct contactless payments at either brick-and-mortar merchants or online merchants.

[0083] To do this, the consumer, having already registered his or her mobile device (112) with the remotely accessible server (140) and associated it with an identifier and communication address, visits, for example, a brick-and-mortar merchant and presents the merchant with his or her portable payment device (114). The portable payment device (114) is interfaced with a point of sales device (120) of the merchant and a `credential transfer` menu option, for example is selected on the point of sales device (120). The consumer (102) may be prompted to enter a PIN which he or she enters into the point of sales device (120), following which, the consumer (102) may be prompted to enter his or her identifier. The consumer (102) enters their predetermined identifier, which has been registered with the remotely accessible server (140), into the point of sales device (120).

[0084] Having received the consumer's PIN, the point of sales device (120) is able to extract payment credentials from the portable payment device (114). The point of sales device (120) formats the payment credentials into a financial transaction message. The point of sales device (120) may also include the identifier in the financial transaction message as well as a server routing code. The server routing code may be similar to a BIN and ensures that the financial transaction message is routed to the remotely accessible server (140) by the payment processing network (130)

[0085] The financial transaction message is received at the remotely accessible server (140). The remotely accessible server uses the identifier contained in the financial transaction message to identify a communication address of an associated mobile device (112). The remotely accessible server (140) uses the communication address to communicate the payment credentials or a derivation of the payment credentials to the mobile device (112) for storage in the secure element (113) associated therewith.

[0086] The payment credentials are then received by the mobile device (112) and stored securely in the secure element (113) of the mobile device (112). The user may be prompted for a PIN before the payment credentials are stored in the secure element. In some embodiments the payment credentials are provisioned to the mobile device (112) from the remotely accessible server (140) and stored in the secure element (113) via over-the-air (OTA) provisioning. This accordingly may enable the user to make contactless payments using his or her mobile device (112) as a contactless portable payment device, where the credentials provided by the mobile device (112) to the merchant's appropriately configured point of sales device are those of the user's portable payment device (114).

[0087] In some embodiments, the remotely accessible server (140) may encrypt the payment credentials and a unique decryption key may be associated with the payment credentials. One of either the encrypted payment credentials or the decryption key may then be stored in secure memory, such as a hardware security module (144) of the remotely accessible server. The other of the encrypted payment credentials or the decryption key may be sent to the secure element (113) associated with the mobile device (112). The payment credentials may be encrypted using any appropriate encryption algorithm such that, once encrypted, the payment credentials may only be decrypted using the unique decryption key. If the decryption key is sent to the mobile device (112) for storage in the secure element (113), this decryption key is not stored at the remotely accessible server nor in its hardware security module.

[0088] The encrypted payment credentials or decryption key received by the mobile device (112) are stored securely in the secure element (113) of the mobile device (112). The user may be prompted for a PIN before the encrypted payment credentials or decryption keys are stored in the secure element. In some embodiments decryption keys are provisioned to the mobile device (112) from the remotely accessible server (140) and stored in the secure element (113) via over-the-air (OTA) provisioning.

[0089] In the scenario of the derivation of the payment credentials in the form of a decryption key is stored at the secure element (113) associated with the mobile device (112), a user may present the identifier to a merchant as a payment method in conducting a transaction. The merchant can request payment credentials from the remotely accessible server (140) and, in conjunction, communicate the identifier to the remotely accessible server (140). The remotely accessible server (140) can use the received identifier to identify a mobile device (112) and request a decryption key from the identified mobile device (112). The mobile device (112), upon receiving this request, may then prompt the user for a PIN, passcode or password before communicating a relevant decryption key to the remotely accessible server (140) so that corresponding encrypted payment credentials can be decrypted and communicated to the merchant and/or the merchant's acquirer, and/or the payment processing network so that the transaction may be completed.

[0090] FIG. 2 illustrates an exemplary system (200) according to a second embodiment of the invention. The system is similar to that which is illustrated in FIG. 1 and like reference numerals refer to like systems, entities or devices. The system (200) of FIG. 2 differs from that of FIG. 1 in that the point of sales device in this embodiment is an automatic teller machine (ATM) (222). The ATM (222) may be any suitable ATM and is configured to obtain payment credentials from a portable payment device (214) of a consumer (202) and to communicate these payment credentials to a payment processing network (230) or financial institution network. The ATM (222) may be configured to obtain payment credentials from the portable payment device (214) via any appropriate contact or contactless communications interface, for example a card reader or near field communication (NFC) interface.

[0091] The ATM (222) in the illustrated embodiment is configured to receive an identifier entered by a consumer (202) via, for example, a keypad of the ATM (222). The ATM (222) is further configured to format the payment credentials as well as the identifier into a financial transaction message and to communicate this message to the payment processing network (230). The financial transaction message may, for example, be an ISO 8583 message. Furthermore, the ATM (222) is configured to insert a server routing code into the financial transaction message such that the financial transaction message is routed to the remotely accessible server (240) by the payment processing network (230) using the server routing code. The server routing code may be placed in the `BIN` field of the financial transaction message.

[0092] Once the payment credentials are received at the remotely accessible server, they may communicated or a derivation of the payment credentials may be communicated to the mobile device for storage in a secure element thereof as has been described in the foregoing description.

[0093] The system (200) may be put to use by a user (202) in a similar manner to that system of FIG. 1. The user (202) presents his or her portable payment device (214) to a portable payment device interface of the ATM (222). The user may be prompted for a PIN, responsive to a correct entry of which, the user (202) user selects a `credential transfer` option from a menu displayed on a screen of the ATM (222). The user (202) will also be prompted for an identifier, which he or she enters into the ATM (222) via keypad of the ATM (222). The ATM (222) obtains payment credentials from the portable payment device (214) and formats the payment credentials, identifier, as well as the server routing code into a financial transaction message which is then sent to the payment processing network (230) and routed from there to the remotely accessible server (240). Similar to the in-use scenario of FIG. 1, the payment credentials are then communicated to the user's mobile device (926) to be stored in a secure element thereof.

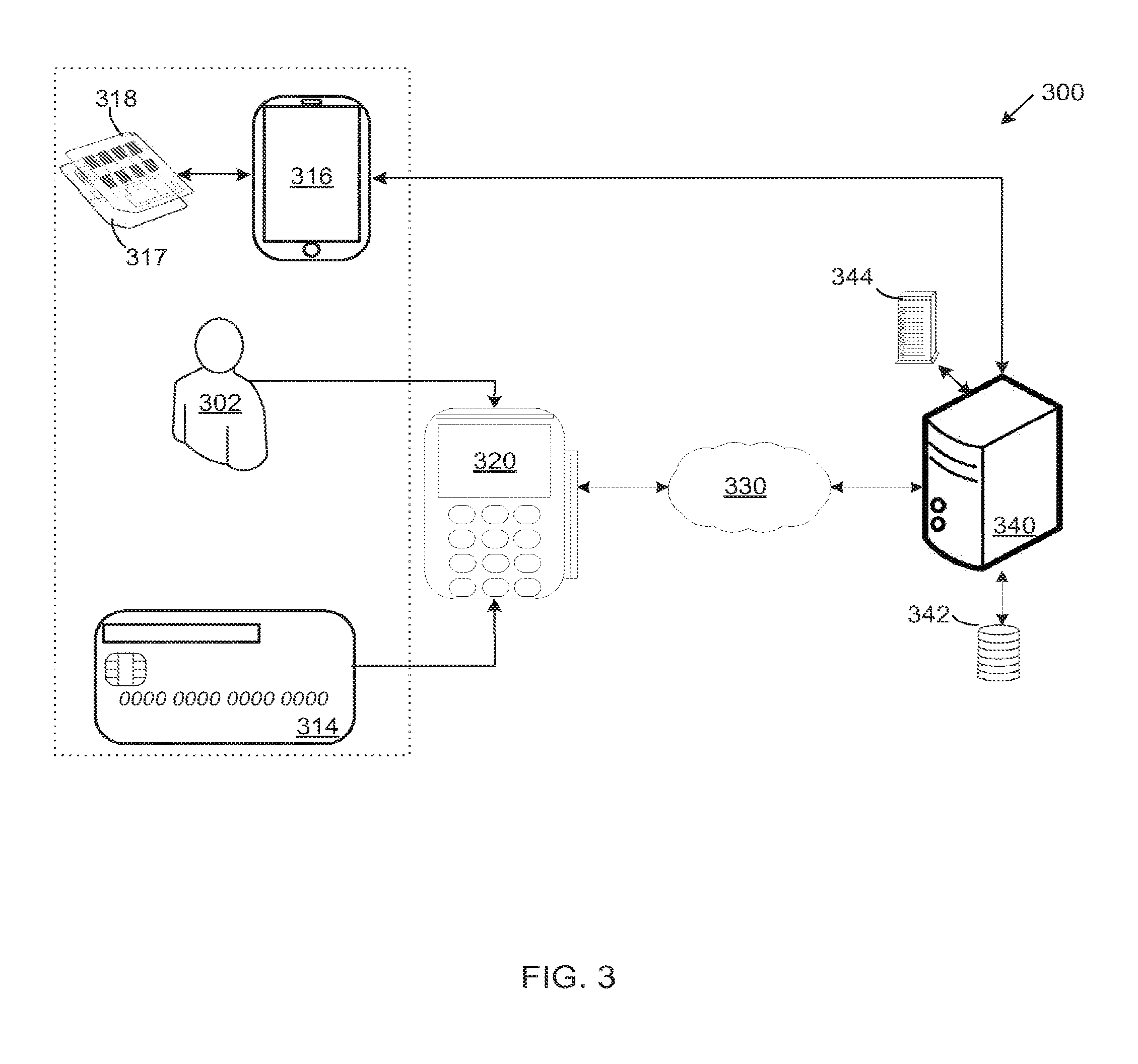

[0094] FIG. 3 illustrates yet another exemplary system (300) according to a third embodiment of the invention. The system (300) is similar to that which is illustrated in FIGS. 1 and 2, and like reference numerals refer to like systems, entities or devices. The system (300) of FIG. 3 differs from that of FIGS. 1 and 2 in that the mobile device (316) does not have an embedded secure element. Rather, the mobile device (316) has a cryptographic expansion label (318) in which a secure element is disposed. The cryptographic expansion label (318) has electrical contacts disposed on a top side and a bottom side thereof which interface to a communication component (317) and a communication component interface of the mobile device (316) respectively. The cryptographic expansion label (318) may then be attached to the communication component (317) which is inserted into a communication bay of the mobile device (316) such that the secure element can intercept and appropriately process any communication sent between the communication component (317) and the mobile device (316) and consequently, between the mobile device (316) and a mobile communication network. In the illustrated embodiment, the communication component is a universal integrated circuit card (UICC).

[0095] FIG. 4A illustrates a flow diagram of a method according to one embodiment of an aspect of the invention. The method is conducted at a provisioning system which may be a remotely accessible server, similar to those described in the foregoing description with reference to FIGS. 1 to 3, or a dedicated kiosk as described further below in relation to FIGS. 9A to 9D.

[0096] The method includes a series of steps, a first (402) of which is the step of receiving payment credentials from a receiving device which may be a point of sales device, incorporated into or used in association with a point of sales device, as described with reference to FIGS. 1 to 3, or a credential storage instrument reader of a kiosk with reference to FIGS. 9A to 9D, or another form of receiving device for receiving payment credentials. The point of sales device may, for example, be an automatic teller machine, a merchant point of sales terminal or a personal PIN entry device (PPED).

[0097] The payment credentials received from the point of sales device are obtained from a portable payment device (also referred to below in relation to the embodiment of FIGS. 9A to 9D as a credential storage instrument) which is presented by a consumer at the receiving device. The portable payment device may be a credit or debit card which may be any one of a magnetic stripe bank card, a security integrated circuit bank card or a contactless bank card. The payment credentials may be track 1 data, track 2 data, track 3 data or track 2 equivalent data (such as EMV tag 57 data). Furthermore, the payment credentials may include an account holder name and/or date of birth, a bank identification number (BIN), a primary account number (PAN), a service code, an expiration date, card verification values (CVV1 or CVV2), a PIN block or offset, a bank account number, a branch code, a loyalty account number or identifier, credit and/or debit card number information, account balance information, and/or consumer information such as name, date of birth. The payment credentials may be received by the remotely accessible server via a payment processing network.

[0098] The method includes a step (404) of receiving an identifier from the receiving device, for example, the point of sales device, or kiosk user input interface. The identifier may be any one or more of a mobile station international subscriber directory number (MSISDN), an email address, a social network identifier, a predefined consumer name or a consumer account number. In a preferred embodiment of the invention, the payment credentials and identifier are received at the remotely accessible server in a financial transaction message, which may, for example, be an ISO8583 message. Furthermore, the financial transaction message may be communicated from the point of sales device to the remotely accessible server via a payment processing network. The financial transaction message may accordingly include a server routing code such that the payment processing network is able to route the financial transaction message to the remotely accessible server.

[0099] The method includes a next step (406) of identifying a mobile device and/or a secure element of a mobile device corresponding to the identifier. This step may include the step of determining whether or not a mobile device and/or secure element corresponding to the identifier has been registered with the remotely accessible server and, if a mobile device and/or secure element has been registered, identifying a corresponding communication address of the mobile device and/or secure element. This may be performed by using the identifier to query a database of the remotely accessible server so as to obtain the communication address of the mobile device and/or secure element associated with the identifier.

[0100] As an optional additional step (408), a registration or activation request may be sent to a trusted management service (TSM) which manages security keys or tokens that are used to access a secure element. The request may include the identifier. The TSM may authorize the unlocking of a secure element associated with the mobile device. The TSM may be provided at the remotely accessible server or by a remote service provided on a separate remotely accessible server.

[0101] The method includes a step (410) of communicating the payment credentials to the mobile device to be stored in a secure element associated with the mobile device. This may include communicating the payment credentials to the mobile device using the communication address. This may also include communicating the payment credentials to the secure element associated with the mobile device using an identification code of a secure element in order to set up a secure channel of communication with the secure element which may be via the mobile device. In some embodiments as described further in relation to FIG. 4B, a derivation of the payment credentials is communicated to the mobile device or secure element, for example, the derivation of the payment credentials may be a decryption key corresponding to remotely stored encrypted payment credentials.

[0102] As a further optional additional step (412), additional credentials may be requested by or supplied by the remotely accessible server. The additional credentials may be credentials which cannot be automatically read from a portable payment device such as a printed card verification value (for example the CVV2 number) which is human-readable from the portable payment device. In this case, the additional credentials may be requested by the remotely accessible server and obtained from the consumer via the point of sales device.

[0103] The additional credentials may also include dynamic card verification value (dCVV) software that is used to generate a dCVV for individual transactions. Such additional credentials may be identified using the identifier and supplied by the remotely accessible server or by a separate remotely accessible server during the provisioning process. The additional credentials may be communicated to the secure element associated with the mobile device. These may be communicated separately to the payment credentials or derivation of the payment credentials.

[0104] The secure element of the mobile device may, according to some embodiments of the invention, be embedded in a label, card or tray as described previously in the forgoing description. Before communicating the payment credentials to the mobile device, the remotely accessible server may encrypt the payment credentials using any one of a number of encryption algorithms. Exemplary encryption algorithms include Advance Encryption Standard (AES), Data Encryption Standard (DES), Triple Data Encryption Standard/Algorithm (TDES/TDEA), Secure Socket Layer (SSL), Blowfish, Serpent, Twofish, International Data Encryption Algorithm (IDEA), Rivest, Shamir, & Adleman (RSA), Digital Signature Algorithm (DSA), Tiny Encryption Algorithm (TEA), extended TEA (XTEA), and/or other encryption algorithms or protocols. In some embodiments, the decryption key, also referred to as the private key, is stored in a secure memory of the remotely accessible server in association with the identifier, such that only the remotely accessible server, or a hardware security module thereof, may decrypt the payment credentials before presentment to, for example, a merchant. In this embodiment, the payment credentials are stored in their encrypted form in the secure element of the mobile device.

[0105] FIG. 4B illustrates a flow diagram of a method according to another embodiment of an aspect of the invention. The method is conducted at remotely accessible server, such as that of FIGS. 1 to 3. The method includes a series of steps, a first (422) of which is receiving payment credentials from a receiving device such as point of sales device similar to that of step (402) of FIG. 4A.

[0106] The method includes a next step (424) of receiving an identifier from the receiving device such as a point of sales device similar to that of step (404) of FIG. 4A.

[0107] The method includes a following step (426) of encrypting the payment credentials. The payment credentials may be encrypted with any appropriate algorithm and once encrypted, have a unique decryption key. Exemplary encryption algorithms include, but are not limited to, Advance Encryption Standard (AES), Data Encryption Standard (DES), Triple Data Encryption Standard/Algorithm (TDES/TDEA), Secure Socket Layer (SSL), Blowfish, Serpent, Twofish, International Data Encryption Algorithm (IDEA), Rivest, Shamir, & Adleman (RSA), Digital Signature Algorithm (DSA), Tiny Encryption Algorithm (TEA), extended TEA (XTEA), and/or other encryption algorithms or protocols.

[0108] As the decryption key is unique to those payment credentials, only that decryption key may be used to decrypt those payment credentials. The unique decryption key, which in some embodiments may be a private key, is not stored in the same location as the encrypted payment credentials.

[0109] The method includes a next step (428) of storing one of either the encrypted payment credentials or the decryption key in a secure memory of the remotely accessible server, which in a preferred embodiment, is a hardware security module. The encrypted payment credentials or the unique decryption key, communication address, and identifier may be associated with a user profile stored in a database of the remotely accessible server. Upon receiving, for example, a unique decryption key, the corresponding payment credentials, stored in the hardware security module, may be identified.

[0110] The method includes a following step (430) of identifying a mobile device and/or a secure element corresponding to the identifier. This step is similar to step (406) of FIG. 4A.

[0111] The method includes a final step (432) of communicating the other of the encrypted payment credentials and the unique decryption key to the mobile device to be stored in a secure element associated with the mobile device. This may include communicating to the mobile device using the communication address. The secure element of the mobile device may, according to some embodiments of the invention, be embedded in a label, card or tray as described previously in the forgoing description.

[0112] As only one of the encrypted payment credentials and the decryption key is only stored in the secure element of the mobile device, the encrypted payment credentials cannot be decrypted, and consequently cannot be used.

[0113] In the scenario where the encrypted payment credentials are stored at the remotely accessible server and the unique decryption key is transmitted to the secure element of the mobile device, the unique decryption key is purged and not stored at the hardware security module of the remotely accessible server.

[0114] This scenario, which may be considered an inverse of one where the payment credentials are stored in the secure element of the mobile device, is advantageous in that if the secure element of the mobile device is compromised, only the decryption keys of encrypted payment credentials can be obtained. Furthermore, in the event that the secure element is compromised, the decryption keys stored therein can simply be revoked, without payment credentials having to be re-issued.

[0115] FIG. 5 illustrates a flow diagram of a method according to another aspect of the invention. The method is conducted at a suitably modified point of sales device, such as any of those described in the foregoing description with reference to FIGS. 1 to 3.

[0116] The method includes a first step (502) of obtaining payment credentials from a portable payment device presented by a consumer at the point of sales device. This may be performed in a manner similar to conventional payment credential access operations, such as for example via an ISO 7816, or ISO/IEC 14443 communication protocol or the like. The payment credentials obtained might be considered as `card present` payment credentials in that they provide sufficient information for a subsequent transaction using the payment credentials to be considered a card present transaction. The payment credentials may then, for instance, be track 1 data, track 2 data, track 3 data or track 2 equivalent data (such as EMV tag 57 data). Furthermore, the payment credentials may include an account holder name and/or date of birth, a bank identification number (BIN), a primary account number (PAN), a service code, an expiration date, card verification values (CVV1 or CVV2), a PIN block or offset, a bank account number, a branch code, a loyalty account number or identifier, credit and/or debit card number information, account balance information, or consumer information such as name, date of birth.

[0117] The method includes a next step (504) of receiving an identifier entered by the consumer into the point of sales device. The identifier may be any one or more of a one or more of a mobile station international subscriber directory number (MSISDN), an email address, a social network identifier, a predefined consumer name or a consumer account number.

[0118] The method further includes a next step (506) of communicating the payment credentials and identifier to a remotely accessible server for further communication to a secure element associated with a mobile device of the consumer. This step may include formatting the payment credentials and identifier into a financial transaction message. The financial transaction message may, for example, be an ISO8583 financial transaction message. The point of sales device may further be configured to insert a server routing code into the financial transaction message such that the financial transaction message is routed to the remotely accessible server by a payment processing network and not, for example an issuing bank as indicated by the BIN originally included in the payment credentials.

[0119] If requested, additional credentials may be input by the consumer at the point of sales device and communicated to the remotely accessible server, for example, non-machine readable card verification values (for example, CVV2 data).

[0120] A remotely accessible server for provisioning of payment credentials, such as that of FIGS. 1, 2 and 3, is illustrated in FIG. 6A. The remotely accessible server (140) has a payment credentials receiver (602) for receiving payment credentials. The payment credentials may be received from a point of sales device whereat the payment credentials may have been obtained from a portable payment device presented by a consumer. The remotely accessible server (140) has an identifier receiver (604) for receiving, from the point of sales device, an identifier entered by the consumer. In some embodiments the payment credentials receiver (602) and the identifier receiver (604) may be provided in a single receiver which may be configured to receive payment credentials and an identifier in a financial transaction message. In some embodiments, the financial transaction message may be an ISO 8583 message.

[0121] The remotely accessible server (140) may include an encryption component (606) for encrypting the received payment credentials, the encrypted payment credentials having a unique decryption key. The remotely accessible server (140) may have a secure memory (608) incorporated therein or associated with the remotely accessible server (140) for storing one of the encrypted payment credentials or the unique decryption key. In the illustrated embodiment, the secure memory (608) and the encryption component (606) are within a hardware security module (644) of the remotely accessible server (140).

[0122] The remotely accessible server (140) may include an identifying component (610) for identifying a mobile device and/or secure element corresponding to the identifier. In the illustrated embodiment, the identifying component (610) forms part of a database (642) of the remotely accessible server (140) in which one or more of the group of: an identifier; decryption key; encrypted payment credentials; and communication address may be associated with a user profile.

[0123] The remotely accessible server (140) further includes a communication module (612) for communicating to the identified mobile device or the secure element associated with the mobile device. The communication module may communicate with the mobile device via any appropriate mobile communication or mobile data network. The communication module (612) may set up a secure communication channel with the secure element via the mobile device for communication of one of the encrypted payment credentials or the unique decryption key.

[0124] The remotely accessible server (140) may optionally include an authorization component (646) for sending a registration or activation request to a trusted management service (TSM) which manages security keys or tokens that are used to access a secure element.

[0125] The remotely accessible server (140) may optionally include an additional credentials component (648) for requesting or supplying additional credentials for communicating to the mobile device or the secure element. The additional credentials component (648) may request additional credentials from a consumer via a point of sale device, for example, human-readable card verification values, which are forwarded for storage on the secure element associated with the mobile device. Alternatively or additionally, the additional credential component (648) may supply additional credentials stored at the remotely accessible server or a related remote server, for example, in the form of dynamic card verification value (dCVV) software used to generate a dCVV for individual transactions. The supplied additional credentials may be forwarded for storage on the secure element associated with the mobile device.

[0126] A point of sales device for provisioning of payment credentials, such as that of FIGS. 1, 2 and 3, is illustrated in FIG. 6B.

[0127] The point of sales device (120) may include a payment credentials obtaining component (652) which may be in the form of a card reader or scanner as previously described. The point of sales device (120) may also include an identifier receiver (654) for receiving an identifier as input by a consumer.

[0128] The point of sales device (120) may include a communication module (656) for communication with a remotely accessible server. The communication module (656) may communicate with the remotely accessible server securely using financial transaction messages.

[0129] In some embodiments, the point of sales device (120) may include an authorization component (658) for sending a registration or activation request to a trusted management service (TSM) which manages security keys or tokens that are used to access a secure element.

[0130] In further embodiments, the point of sales device (120) may include an additional credentials receiver (659) for receiving additional credentials from a consumer, for example, in the form of a printed card verification value which is not obtainable by the payment credentials obtaining component (652).

[0131] FIG. 7 shows a swim-lane flow diagram illustrating the flow between a mobile device (112), a point of sales device (120), and a remotely accessible server (140) according to embodiments. The remotely accessible server (140) may be provided by a financial institution or service provider. In one embodiment, the remotely accessible server (140) is part of a payment processing network.

[0132] A consumer may present (701) his portable payment device (for example, a payment card) at the point of sales device which may extract payment credentials from the portable payment device. The consumer may also provide (702) an identifier. For example, the consumer may present a merchant with his payment card which may be inserted into a point of sales device and a "credential transfer" transaction may be requested. The consumer may be prompted for his payment card PIN which may be entered into the point of sales device via a keypad. The point of sales device may also prompt the consumer for an "alias" which is used as an identifier for the consumer and his mobile device.

[0133] The point of sales device may format (703) the extracted payment credentials and the identifier into a transaction message, for example, an ISO8583 message. This message is similar to a normal point of sale transaction message with the addition of the provided identifier. The BIN field may be populated with a payment processing network BIN so that the message is routed to a payment processing gateway instead of an issuer. The consumer's BIN remains provided in the message.

[0134] The remotely accessible server receives (704) the transaction message and extracts the payment credentials and the identifier. The identifier is used to identify (705) one or more of: a consumer having a registered mobile device and/or secure element; an account having a registered mobile device and/or secure element; or the mobile device and/or secure element itself.

[0135] The remotely accessible server may encrypt (706) the payment credentials and a unique decryption key may be generated specific to the payment credentials. One of the encrypted payment credentials and the unique decryption key may be securely communicated (707) to the secure element associated with the mobile device, whilst the other of the encrypted payment credentials and the unique decryption key may be stored (708) at the remotely accessible server.

[0136] The secure element associated with the mobile device may receive (709) either the encrypted payment credentials or the unique decryption key and may prompt the user for a PIN (710), the offset of which is stored in association with the payment credentials or the decryption key such that the payment credentials will only be released by the secure element in the event that the correct PIN is entered.

[0137] FIG. 8 is a swim-lane flow diagram illustrating the flow between a mobile device (112), a point of sales device (120), and a remotely accessible server (140) according to an embodiment of the described method in which the decryption key for the payment credentials is provisioned to the secure element associated with the mobile device.

[0138] A consumer may present (801) an identifier to a merchant as a payment method in conducting a transaction. The merchant may request (802) payment credentials from the remotely accessible server sending the identifier with the request.

[0139] The remotely accessible server may use the received identifier to identify (803) a mobile device associated with a secure element at which a decryption key is stored. The remotely accessible server may request (804) the decryption key via a secure communication with the secure element which may be via the mobile device.

[0140] The mobile device upon receiving the request may prompt (805) the consumer for a PIN before communicating (806) the decryption key to the remotely accessible server.

[0141] The remotely accessible server may retrieve (807) the encrypted payment credentials from its storage and decrypt (808) the payment credentials using the decryption key. The payment credentials may then be transmitted (809) and received (810) at a point of sales device or another intermediary using a secure channel in order to complete the transaction.

[0142] An advantage of storing payment credentials, encrypted, at a remotely accessible server instead of in a secure element of a mobile device, according to embodiments of the present invention, is that if the secure element of the mobile device is compromised by a malicious third party and information stored therein is obtained by that third party, the information obtained by the third party will not include payment credentials. This is in contrast to scenarios in which payment credentials are stored in the secure element and where the third party may obtain and fraudulently make use of these payment credentials.

[0143] In addition to this, in the event that the secure element is compromised or lost, the decryption keys stored therein can simply be revoked, without payment credentials having to be re-issued.

[0144] A further advantage of storing the payment credentials, encrypted, at the remotely accessible server instead of in a secure element of a mobile device is that the mobile device need not meet security standards imposed by relevant standards or compliance authorities. For example, the secure element need not be EMV compliant or may not have to meet PCI DSS requirements.

[0145] Similarly as the unique decryption key is stored only in the secure element of the consumer's mobile device, the corresponding encrypted payment credentials cannot be decrypted, and consequently cannot be used, without the decryption key being released from the secure element in which it is securely stored. Thus the consumer has ultimate control over when his or her payment credentials may be used. Furthermore, if the remotely accessible server is compromised by a malicious third party, encrypted payment credentials stored therein will be of no use to that third party without a corresponding unique decryption key.