Apparatus And Method For Emulating Transactional Infrastructure With A Digital Transaction Processing Unit (dtpu)

WILSON; ROBERT

U.S. patent application number 16/073545 was filed with the patent office on 2019-01-31 for apparatus and method for emulating transactional infrastructure with a digital transaction processing unit (dtpu). The applicant listed for this patent is XARD GROUP PTY LTD. Invention is credited to ROBERT WILSON.

| Application Number | 20190034912 16/073545 |

| Document ID | / |

| Family ID | 59396881 |

| Filed Date | 2019-01-31 |

View All Diagrams

| United States Patent Application | 20190034912 |

| Kind Code | A1 |

| WILSON; ROBERT | January 31, 2019 |

APPARATUS AND METHOD FOR EMULATING TRANSACTIONAL INFRASTRUCTURE WITH A DIGITAL TRANSACTION PROCESSING UNIT (DTPU)

Abstract

Digital transaction apparatus including a Data Assistance Device (DAD), including a user interface that is operable to at least select data, and a DAD transmitter, a Digital Transaction Card (DTC), including a Digital Transaction Processing Unit (DTPU), and a DTC receiver, wherein the DAD and DTC are operable to transfer data from the DAD to the DTC and when subsequently using the DTC to effect a digital transaction, the DTC operates in accordance with data selected and transferred from the DAD to the DTC, wherein the DTPU is configured to enable data communication with a digital transaction device during a digital transaction, the DTPU operable to receive and execute one or more commands that emulate commands received from the digital transaction device.

| Inventors: | WILSON; ROBERT; (Victoria, AU) | ||||||||||

| Applicant: |

|

||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Family ID: | 59396881 | ||||||||||

| Appl. No.: | 16/073545 | ||||||||||

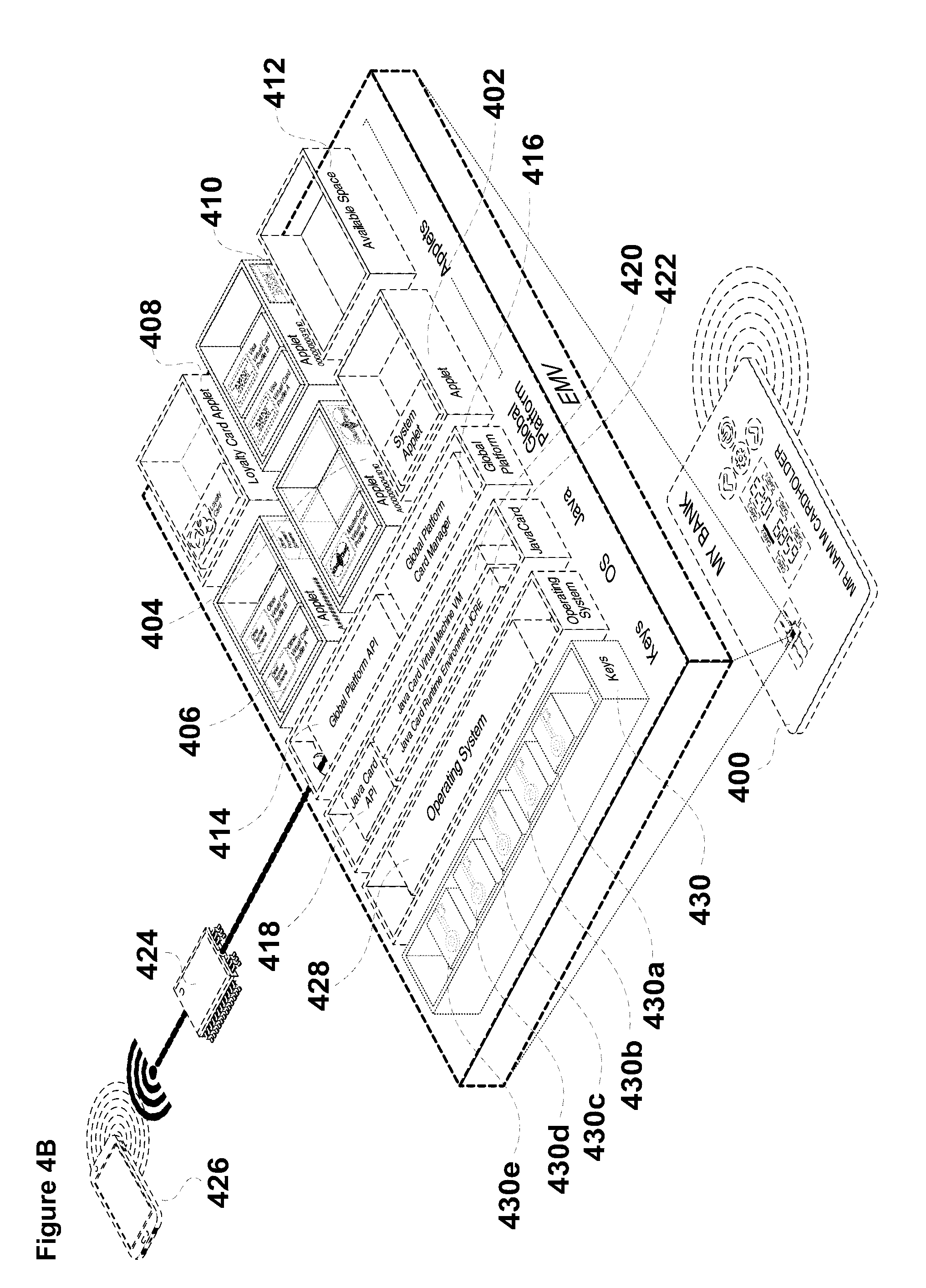

| Filed: | January 28, 2017 | ||||||||||

| PCT Filed: | January 28, 2017 | ||||||||||

| PCT NO: | PCT/AU2017/000026 | ||||||||||

| 371 Date: | July 27, 2018 |

| Current U.S. Class: | 1/1 |

| Current CPC Class: | G06Q 20/3552 20130101; G06Q 20/354 20130101; G06Q 20/3278 20130101; G06Q 20/3558 20130101; G06Q 20/3574 20130101; G06Q 20/352 20130101; G06Q 20/341 20130101; G06Q 20/385 20130101; G06Q 20/227 20130101; G07F 7/0853 20130101 |

| International Class: | G06Q 20/34 20060101 G06Q020/34 |

Foreign Application Data

| Date | Code | Application Number |

|---|---|---|

| Jan 29, 2016 | AU | 2016900277 |

Claims

1. Digital transaction apparatus including: a Data Assistance Device (DAD), including: a user interface that is operable to at least select data, and a DAD transmitter; a Digital Transaction Card (DTC), including: a Digital Transaction Processing Unit (DTPU), and a DTC receiver, wherein the DAD and DTC are operable to transfer data from the DAD to the DTC and when subsequently using the DTC to effect a digital transaction, the DTC operates in accordance with data selected and transferred from the DAD to the DTC, wherein the DTPU is configured to enable data communication with a digital transaction device during a digital transaction, the DTPU operable to receive and execute one or more commands that emulate commands received from the digital transaction device.

2. Digital transaction apparatus according to claim 1, wherein the emulation is of one or more functions that would otherwise be enacted with the DTC in operation with the digital transaction device.

3. Digital transaction apparatus according to claim 1, wherein the transferred data includes data pertaining to one or more selectable personalities.

4. Digital transaction apparatus according to claim 1, wherein the selected and transferred data includes one or more instructions.

5. Digital transaction apparatus according to claim 4, wherein the one or more instructions include instructions to change a current personality of the DTC to a personality selected from a plurality of selectable personalities.

6. Digital transaction apparatus according to claim 3, wherein data pertaining to the plurality of selectable personalities is stored on the DAD, and changing the current personality of the DTC to the selected personality includes: receiving, by the DAD and by operation of the DAD user interface, the instruction to change the current personality of the DTC to the selected personality; transmitting, by the DAD transceiver to the DTC transceiver, data related to the selected personality; and implementing, in the DTC, a change from the current personality to the selected personality in accordance with the data such that when the DTC operates with a digital transaction device to effect the digital transaction, the digital transaction device recognises the selected personality.

7. Digital transaction apparatus according to claim 3, wherein data related to the plurality of selectable personalities is stored on the DTC, and changing the current personality of the DTC to the selected personality includes: receiving, by the DAD, and by operation of the DAD user interface, the instruction to change the current personality of the DTC to the selected personality; transmitting, by the DAD transceiver to the DTC transceiver, the instruction to change the current personality of the DTC to the selected personality; and implementing, in the DTC, a change from the current personality to the selected personality in accordance with the instruction such that when the DTC operates with a digital transaction device to effect the digital transaction, the digital transaction device recognises the selected personality.

8. Digital transaction apparatus according to claim 1, wherein the DTC includes a user interface.

9. Digital transaction apparatus according to claim 3, wherein the selected data transferred from the DAD to the DTC including data pertaining to the plurality of selectable personalities and stored on the DTC are individually selectable by operation of the DTC user interface.

10. Digital transaction apparatus according to claim 9, wherein changing a current personality of the DTC to the selected personality includes: receiving, by operation of the DTC user interface, one or more instructions to change the current personality of the DTC to the selected personality; and implementing, in the DTC, a change from the current personality to the selected personality in accordance with the one or more instructions such that when the DTC operates with a digital transaction device to effect the digital transaction, the digital transaction device recognises the selected personality.

11. Digital transaction apparatus according to claim 8, wherein the DTC scroll keys enable user selection of a personality from the plurality of personalities and the display indicates the selectable personality.

12. Digital transaction apparatus according to claim 1, wherein the DTC external processor is for receiving and storing transferred data.

13. Digital transaction apparatus according to claim 1, wherein the DTC includes a display for displaying information.

14. Digital transaction apparatus according to claim 1, wherein the DTPU is an EMV device operating in accordance with firmware wherein the firmware has been modified to enable the EMV device to receive and execute an expanded set of commands that, when executed, allows the writing of data to a secure memory element of the EMV device.

15. Digital transaction apparatus according to claim 1, wherein the DTPU is an EMV device including a software module having instruction code which, when executed, causes the EMV device to receive and execute commands according to the Global Platform Standard Command set including commands to install an Applet displaying a credit card personality.

16. Digital transaction apparatus according to claim 14, wherein a digital transaction device interfaces with the EMV device by physical connection with contact terminals of the EMV device, or by contactless connection (ISO 14443 Standard), or by interaction between a magnetic stripe reader associated with the digital transaction device and a magnetic stripe of the DTC.

17. Digital transaction apparatus according to claim 16, wherein the DTC is a wearable device including a watch, a wrist band, a ring or an item of jewellery.

18.-22. (canceled)

23. A Digital Transaction Card (DTC) including: a Digital Transaction Processing Unit (DTPU); and a DTC receiver that is operable to receive user-selected data from a transmitter associated with a Data Assistance Device (DAD), wherein the user-selected data that is received causes the DTC to operate in accordance with the user-selected data when the DTC is subsequently used to effect a digital transaction, and wherein the DTPU is configured to enable data communication with a digital transaction device during a digital transaction, the DTPU operable to receive and execute commands that emulate one or more commands received from the digital transaction device.

24. (canceled)

25. A digital transaction method including: selecting data, by a user interface of a Data Assistance Device (DAD); transferring the selected data by a DAD transmitter associated with the DAD to a receiver associated with a Digital Transaction Card (DTC) having a Digital Transaction Processing Unit (DTPU); and effecting, by the DTC, a digital transaction wherein the DTC operates in accordance with the data selected and transferred from the DAD to the DTC, wherein the DTPU is configured to enable data communication with a digital transaction device during a digital transaction, the DTPU operable to receive and execute commands that emulate one or more commands received from the digital transaction device.

26.-35. (canceled)

36. A computer-readable medium storing one or more instructions that, when executed by one or more processors associated with a Digital Transaction Card (DTC), cause the one or more processors to: receive user selected data, from a Data Assistance Device (DAD); and subsequently effect a digital transaction wherein the DTC operates in accordance with the user-selected data, wherein the DTC includes a Digital Transaction Processing Unit (DTPU) configured to enable data communication with a digital transaction device during a digital transaction, the DTPU operable to receive and execute commands that emulate commands received from the digital transaction device.

37.-41. (canceled)

Description

FIELD OF THE INVENTION

[0001] The present invention relates generally to apparatus and methods for effecting digital transactions, including both financial and non-financial transactions. The apparatus and method may be particularly useful for transactions involving credit and/or debit cards.

BACKGROUND OF THE INVENTION

[0002] Credit cards, debit cards store cards and gift cards are examples of cards that are used for financial transactions throughout the world. Further, other types of cards such as passes, tags and small booklets (which may be referred to collectively as transaction documents) are used for various financial and non-financial transactions. For example, some jurisdictions require proof of age cards for transactions such as purchasing alcohol or entering into age restricted venues. Other examples of proof of age, or proof of identity, documents include driver licenses which are sometimes used for authentication in respect of transactions. In some countries, passports and/or other similar identification documents are issued in the form of a card, or a small booklet, and can be used for transactions where identification is required including, travel across borders or establishing a bank account.

[0003] Many transaction documents have a magnetic stripe, which can be encoded with information such as a unique identification number, expiry dates or other numerical or alphanumerical information. Other types of transaction documents include contactless stored value smart cards, for example, closed loop transport cards, such as Myki in Melbourne, Australia, and the Octopus Card in Hong Kong.

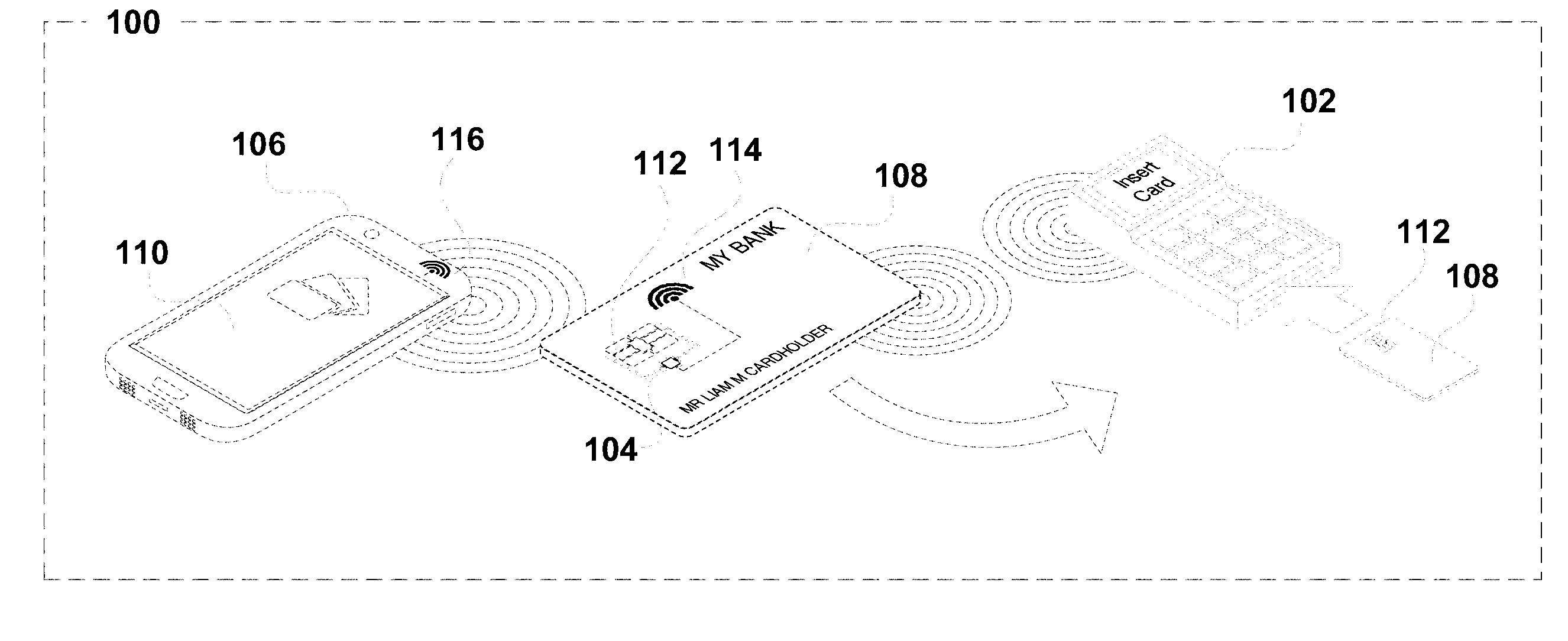

[0004] Transaction documents may include a chip, smart chip, or smart card chip (in this specification, such chips or devices and other similar types of microcircuit will be referred to generally as Digital Transaction Processing Units, or DTPUs). DTPUs typically include one or more of a Central Processing Unit (CPU), Read Only Memory (ROM), Random Access Memory (RAM), Electrically Erasable Programmable Read Only Memory (EEPROM), a crypto-coprocessor and an Input/Output (I/O) system. For example, credit cards often use an EMV device (where EMV is an abbreviation for Europay, MasterCard, and Visa). The EMV device (or other type of DTPU) contains encrypted data relevant to the type of transaction(s) for which the document will be used. The EMV device may be read by a scanner (for example, using contactless, close proximity communications according to ISO/IEC 14443 which is referred to as Near Field Communication (NFC throughout the specification)), by direct contact with chip connected electrodes, or by other means to obtain data from the chip. Such transaction documents enabled for use in digital transactions by means of a chip, a magnetic stripe, a chip and magnetic stripe, or Radio-Frequency IDentification (RFID) are referred to throughout this specification as digital transaction documents.

[0005] Digital transaction documents are configured to work with various components in a digital transaction system including terminals. For example, credit and debit cards work with EFTPOS (Electronic Funds Transfer at Point Of Sale) terminals for Point Of Sale (POS) transactions, and ATM (Automatic Teller Machine) terminals. Other digital transaction documents are configured to work with other types of terminals. Such terminals may be operably connected to financial institutions or other third party organizations to enable digital transactions to occur by authorizing the transaction or performing associated processing to enable the transaction.

[0006] In another example, identification cards, such as a proof of age cards, are implemented with a chip (or DTPU) containing some, or all, of the information of the card owner, along with verification information to confirm the authenticity of the card. Identification cards may be used in a digital transaction, whereby it is inserted into, swiped, or waived near, a terminal to confirm the age of the person holding the card. Other non-financial transactions can be implemented in a similar manner.

[0007] Terminals used for transactions with digital transaction documents are referred to throughout this specification as digital transaction system devices. For "Card-Present" transactions, the digital transaction system devices may include, for example, POS/EFTPOS terminals, ATMs, and network connected or stand-alone readers for reading other types of non-financial transaction documents. The digital transaction devices may also be suitable for "Card-Not-Present" transactions, for example, online transactions, Mail Order/Telephone Order (MOTO) transactions, and may include internet connected personal computers, smartphones, and tablets. Further, digital transaction system devices include telephones used to communicate with an operator who uses, for example, a network connected terminal to enter transaction document data.

[0008] Digital transaction documents have a unique IDentification (unique ID), typically having a number, an alphanumeric ID, or a unique name. The unique ID may be located on, or in, the digital transaction document, for example, printed or embossed on the document. The unique ID is also typically recorded on a database, controlled, for example, by the issuer of the digital transaction document, and accompanied by other information, such as name, address, age, and/or financial information relevant to the user/owner of the digital transaction document. Where a digital transaction document has a chip, an EMV device or other type of DTPU, the unique ID is typically stored on the chip, EMV device or DTPU, respectively.

[0009] Credit cards are typically embossed or printed with a Personal/Primary Account Number (PAN) to uniquely identify the account card holder. A standardized PAN has four fields, namely, a system number, a bank/product number, a user account number, and a check digit. This type of PAN typically has 16 digits, but may have between 13 and 19 digits (for example, an American Express PAN has 17 digits). The first digit is the card issuer type (for example, Visa, MasterCard or American Express), and the next 5 to 7 digits is generally referred to as a Bank Identification Number (BIN) and represents the card network, the bank and the product for this bank. The last digit is reserved for a checksum of the previous digits of the PAN. An expiration date is associated with the PAN and generally includes a month and year code having four digits, but with limited range. The card holder's PAN, name or business, and the card's expiry date typically appear embossed or printed on the face of a card. Previously, some types of credit card had a magnetic stripe encoding some or all of the card information.

[0010] More recently, financial transaction cards have carried a Card Verification Value (CVV) or Card Verification Code (CVC) on the magnetic stripe to make it more difficult to replicate a card for fraudulent purposes. The CVC is usually a unique cryptogram, created based on the card data, for example, including the card PAN and expiry date, and a bank's (or a personalization bureau's) master key, and printed on the card after personalization data is entered on the card. As a consequence, a person seeking to use a card for fraudulent purposes requires possession of the card for a sufficient period of time to make a copy of the magnetic stripe in order to duplicate the card, or to read the card and manually record the card number, expiry date, and other details printed on the card.

[0011] The same principle was subsequently adopted for a second CVC, sometimes called Card Verification Value 2 (CVV2), which is commonly printed in the signature panel on the back of the card. The CVV2 is used primarily to help secure e-Commerce and MOTO transactions. This is a second unique cryptogram created from card data and the bank's master key (although this is a different cryptogram as compared with the magnetic stripe CVC). The CVV2 is not present on the magnetic stripe.

[0012] Some credit cards also have an associated Personal Identification Number (PIN) code, which is primarily used for "Card-Present" transactions. The PIN must generally be kept confidential, and must be entered on secure and certified terminals to make sure that no-one can gain access to the PIN. Further, in modern credit cards, the PIN can be stored on the chip (for example, an EMV device) in an encrypted form within a cryptogram block.

[0013] There are two main classifications of transactions for which credit cards are used including: "Card-Not-Present" transactions, when using the Internet or MOTO; and "Card-Present" transactions, such as used with POS/EFTPOS and ATM terminals. Card-Present transactions involve EMV device readers (including physical contact readers using electrode pins on a card and contactless reading using, for example, Near Field Communications (NFC)) and/or magnetic stripe readers. These transactions generally use the full 13 to 19 digit PAN and the 4-digit expiration date. Card-Not-Present transactions generally require the user to read out to an operator, or enter into a computer, the PAN and expiration date digits. In some instances, the CVC/CVV2 number is also required.

[0014] Other types of digital transaction documents may use various forms of security, such as PINs, passwords, and the like. However, some other types of digital transaction documents do not use such external security, and rely only upon the authenticity of the document itself, for example, using holograms and other security devices that are difficult to copy. Further, some types of non-credit card digital transaction documents may use chips for security, including chips similar to EMV devices.

[0015] Cards (or other digital transaction documents) may have data stolen, for example, using a Radio Frequency (RF) signal to power the card's EMV internal microprocessor and related transmitter. Generally, the card data, such as the PAN, expiration date and cardholder's name are transferred to a wireless terminal. The terminal can be a portable or stationary wireless terminal, and once near a card, uses the RF signal to energize the card to firstly, extract the card data and copy some to a memory storage device, or to online storage, such as, the cloud, and secondly, use a portable terminal in close proximity to the card to extract monies as a contactless payment (for example, a PayWave and/or tap payment, such transactions being referred to by traders as tap-and-pay or tap-and-go), in accordance with a level of transaction that does not require any authorization. Subsequently, stolen card data can be uploaded to a duplicate "fake card" or used in online transactions to make fraudulent purchases. Yet another method used to steal card data for fraudulent use involves hacking into computer databases that store card data. This data is then used for transactions, and a card owner may only become aware of this when they see a statement detailing the transactions made with their card, or card data.

[0016] Other ways card data is stolen include phishing scams where the card holder is tricked into entering a security code along with other card details via a fraudulent website. Phishing therefore reduces the effectiveness of security codes as an anti-fraud means. However, merchants who do not use security codes are typically subjected to higher card processing costs for transactions, and fraudulent transactions without security codes are more likely to be resolved in favour of the cardholder, which increases costs for merchants. Yet other ways that security of transactions may be compromised is by skimming and man-in-the-middle attacks.

[0017] With the emergence of e-Commerce, an increasing number of transactions are Card-Not-Present type transactions. However, this type of transaction is subject to an increasing number of attacks from fraudsters including attacks that have resulted in increased verification that has caused a "failure positive" result where the card holder is legitimate but the transaction is rejected.

[0018] Several solutions have been developed to address this growing fraud, including use of virtual account numbers, authentication of cardholders separately from the transaction, and use of a hardware token to authenticate the user. Another proposed solution comprises an institution, such as a bank sending a code to the user, typically by SMS to the user's smartphone, which can then be used to authenticate a Card-Not-Present transaction. This arrangement is generally referred to as an Out-Of-Band (OOB) message which unfortunately has been recently hacked. In any event, many of these solutions require expensive infrastructure changes, which merchants prefer to avoid and may only provide protection for a limited time until the arrangement is hacked.

[0019] With the increasing number of Card-Not-Present transactions, a suggested means of conducting such transactions is the electronic wallet (e-wallet), also known as a digital wallet. An e-wallet provides users with a means to pay for purchases from enabled on-line merchants. Upon registration, a user can store their card, billing and shipping information on a site hosted by a suitable document, such as a bank, and can access that information to pay for goods or services. However, e-wallets on an NFC enabled device, such as a smartphone, do not operate in a large percentage of Card-Present transactions, for example, POS/EFTPOS or ATM transactions since these network transaction devices generally do not support contactless payments and amongst the presently available contactless payment arrangements, different back end processes and merchant agreements are involved. As a result, the establishment and use of e-wallets has experienced limited commercial success and whilst they remain available to consumers, only approximately 10% of consumers have elected to install an e-wallet although the take-up rate by consumers is now starting to drop.

[0020] A user may prefer to have, and to carry around with them, many of their available credit cards, debit cards, store cards, government agency cards and loyalty cards since they prefer to physically hold and control the possession of those cards. Further, a user may require an identity card, driver's license, age verification card or passport. Carrying around a large number of individual digital transaction documents can be very inconvenient. Moreover, the person, having so many physical transaction documents, may become confused regarding the location of a particular digital transaction document, for example, a particular credit card, among all the other digital transaction documents.

[0021] An alternative solution to e-wallets that addresses the problem of users carrying a large number of credit or debit cards has been developed, wherein a credit card sized device has a keyboard (or touch pad arranged as a simplified keyboard) and a small limited function Graphical User Interface (GUI), which are used to select one card amongst a number of cards stored on the device, and to enter data for various transactions. However, the keyboards are of limited functionality due to their limited number of keys in the relatively small space available on the card (being the area of an average credit card). The keyboards are also considered difficult to use because of their small size, and as a result a large number of keystrokes may be required to effect any particular function. Further, the keyboard on a credit card is not a solution for other types of digital transaction document such as those documents used for proof of identity or proof of age. Other attempted solutions include products, such as Plastc, Coin, Final, and Wocket. However, the Plastc solution has some operational limitations, and the Wocket solution requires a specific Wocket device. None of these solutions has gained wide commercial acceptance. Moreover, it has been found that cards including a keyboard have an unacceptably high failure rate when given to customers in view of the repeated, perhaps daily, usage. It is suggested that the high failure rate may be, at least in part, due to the complications of having the keyboard on a card, which has limited space for such a complex electronic device.

[0022] Another problem with attempting to accommodate multiple credit cards, debit cards or other digital transaction documents on a single card are the limitations caused by the use of proprietary or standardized chips. Such chips or DTPUs are configured to securely store information for one digital transaction document only. For example, a credit card chip, such as an EMVCo standard chip, securely holds information typically including the credit card PAN, the expiry date, a security code (such as the CCV2 number), and a PIN. Transaction devices, such as POS/EFTPOS terminals, securely communicate with the DTPU to obtain some, or all, of the information from the DTPU for a transaction to be authorized and verified. Many DTPUs are also configured to resist attempts to write to the DTPUs secure record memory (which may also be referred to as a secure element, or part of a secure element), as many such attempts are made by those seeking to use the card fraudulently. It will be understood that a secure element may comprise secure memory and an execution environment, and is a dynamic environment in which application code and application data can be securely stored and administered. Further, it will be understood that, in a secure element, secure execution of the application can occur. A secure element may be located in a highly secure crypto chip (otherwise known as a smart card chip). The security of the DTPU may also prevent legitimately introducing one or more new digital transaction documents (including PANs, tokens expiry dates, PINs and other data attributes of those documents) into the secure record memory (secure element) of the DTPU so that the DTPU cannot take on another document's personality (a term which is used herein to describe a digital transaction document (or logical digital transaction document) and its attributes).

[0023] Accordingly, it has been difficult to instigate use of single physical cards having multiple personalities (multiple credit and/or debit cards expressed or expressible on a single physical card), given the change in infrastructure required, including modified DTPUs (such as the EMVCo device), modified digital transaction devices (for example, modified POS/EFTPOS terminals), along with any other modification required in other parts of the credit/debit card payment infrastructure. Apart from the technical problems, Card Association Scheme providers such as Visa and MasterCard have various additional requirements including the presence of a hologram and logo of the Card Association Scheme on the physical card.

[0024] In this regard, it is desirable to provide a single EMV (or EMV type device), or other type of DTPU, on a Digital Transaction Card (DTC), for example, a credit card sized card, which is able to selectively assume the personality of a number of different digital transaction documents (or logical digital transaction documents). For example, a user may seek to use MasterCard account for one transaction, but to a use Visa account for a different transaction. Alternatively, a user may seek to use the DTC as a credit card, but to subsequently use it as an age identity card.

[0025] However, to-date, there has not been a sufficiently effective, efficient, and/or secure means and/or method for adapting a DTPU (such as an EMVCo specified device) to embody different personalities as compared with the personality of the DTPU that was initially installed.

[0026] Another problem with present digital transaction documents is the ability to obtain data from a credit card or other transaction document. Although devices such as EMV devices have been introduced in an attempt to limit data theft, such arrangements have not proved to be entirely successful in preventing this type of crime. Increasing credit card fraud may incur cost for a bank, a merchant, a user, or all three parties. Further, identity theft is an increasing concern for users since a stolen identity can be used to commit fraudulent financial transactions, and other types of crime.

[0027] For some digital transaction documents, such as credit cards, tokens are sometimes used to enhance security for transactions. For credit cards, tokens are typically numbers that are the same length as the credit card's PAN, and are substituted for the PAN in a transaction. The token should not be feasibly decryptable to obtain the original PAN by a person seeking to use the credit card fraudulently, and so that person is unable to mimic the credit card, and unable to use the credit cards PAN and a card holder's other personal details for on-line transactions. Accordingly, if using a credit card in a high risk, low security environment, tokens are a means of protecting sensitive data. The security of the token is based primarily on the infeasibility of determining the original PAN (or other data) whilst knowing only the surrogate token value. Tokenization may be used instead of, or in conjunction with, other encryption techniques in transactions with digital transaction documents.

[0028] A token (or digital token) may be generated by a third party, such as a credit card issuer, a financial institution, or a security provider for the credit card. Tokens are also used for securing other non-financial transactions, such as those involving drivers' licenses. The token may be generated as a cryptogram using inputs from a selection of, for example, the credit card's PAN (or some other unique ID of a digital transaction document), and/or the card's expiry date. The token for a transaction may be selected from a number of tokens in a pool based on the ID of the merchant or the terminal where the transaction is occurring, the date of the transaction, the time of the transaction, or various other criteria. De-tokenization to retrieve the original PAN typically occurs during the processing of a transaction, and is usually performed by the credit card issuer, financial institution, or security provider who issued the token.

[0029] Usually, tokens are generated during the process of creating and issuing a credit card to its owner/user. Each card may have one or more associated tokens. Where a card has multiple tokens, each token can be selectively used for different transactions or different transaction types.

[0030] Tokens have a number of problems, including not being selectable by the user to allow the user control over security and how tokens are used. For example, a user may seek to be able to select tokens for certain transactions or transaction types. Another problem is that the same token may need to be used for a number of different transactions, thus limiting the security afforded by the token. This is especially the case for a digital transaction document such as a credit card. Even if a digital transaction document has a number of associated tokens, those tokens will need to be reused or reissued after a number of transactions. It is difficult to issue new tokens, for example, to a credit card, since the infrastructure for issuing new tokens has been developed to issue those new tokens at a time of creation and issuance of a new credit card.

[0031] One way to prevent fraudulent use of a stolen or compromised credit card or other types of transaction document is to simply cancel the document, including cancelation of that document's unique identifier (for example, cancelling the account number of a credit card), and issue a new document with a new expiration date. Providers of the document may have a mechanism to invalidate old documents (for example, invalidating old account numbers), and to issue new numbers to existing users. However, it can sometimes take a substantial amount of time to deliver a new document (for example, delivering a credit card through the mail), and the delay greatly inconveniences the user. In the instance of a credit card, the issuance of a new card causes a temporary cessation of the user's ability to maintain payments by auto debit from credit accounts.

[0032] Further, document owners generally prefer instant or near instant ("real time") feedback of information regarding use of their card for financial transactions or other types of transaction, such as use of a card or other such documents for identification, traveling and other purposes. Card owners may also prefer real time feedback regarding account balances and other information related to their card, or other digital transaction documents. Further, owners of cards and other digital transaction documents may prefer the ability to block usage of a document in real time, or with minimal delay. This may be useful if the owner becomes aware of, or suspects, fraudulent transaction(s) with the use of one or more of their digital transaction document(s).

[0033] It is an object of the present invention to overcome, or at least ameliorate, at least one of the above-mentioned problems in the prior art, and/or provide at least a useful alternative to prior art devices, systems and/or methods.

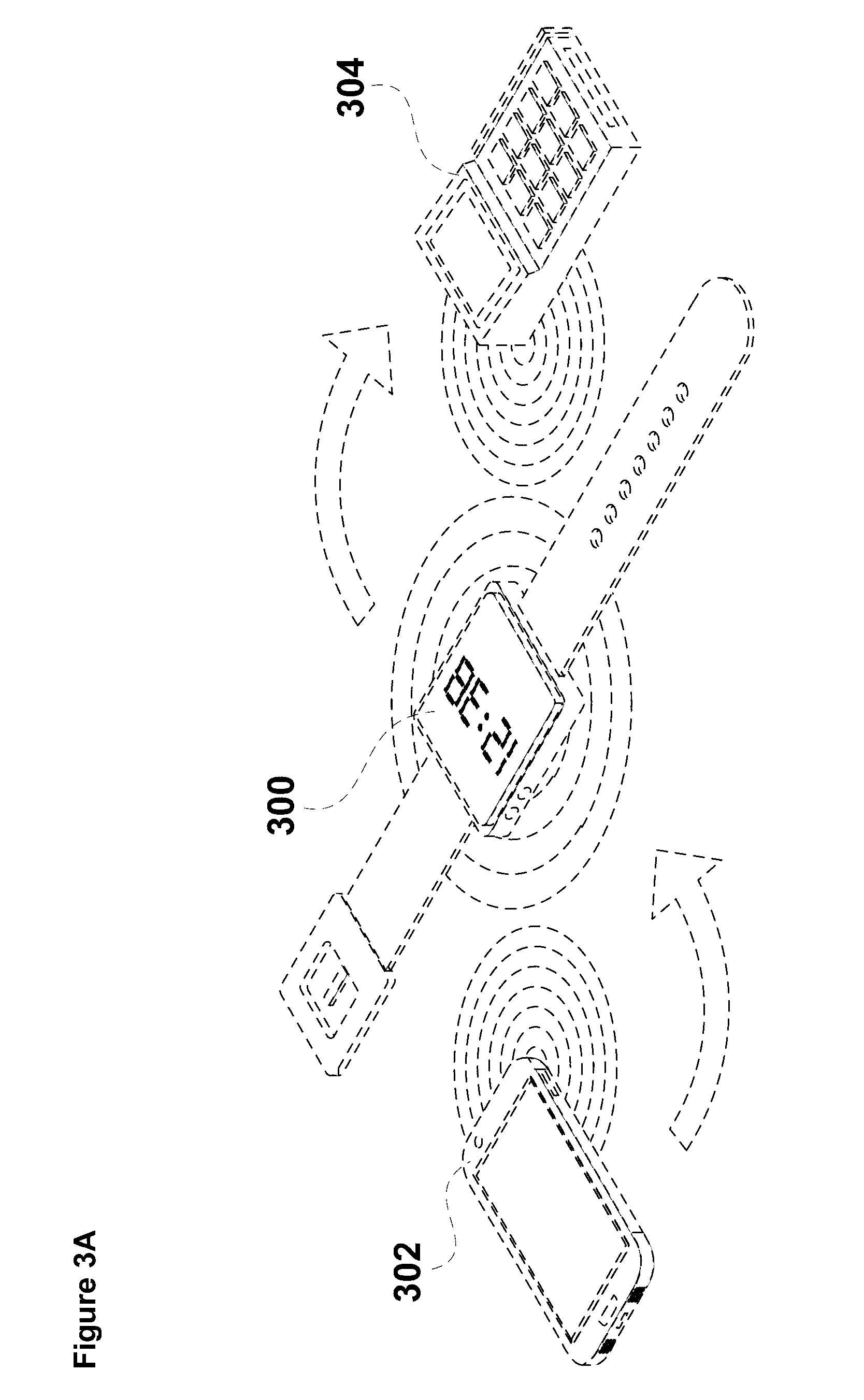

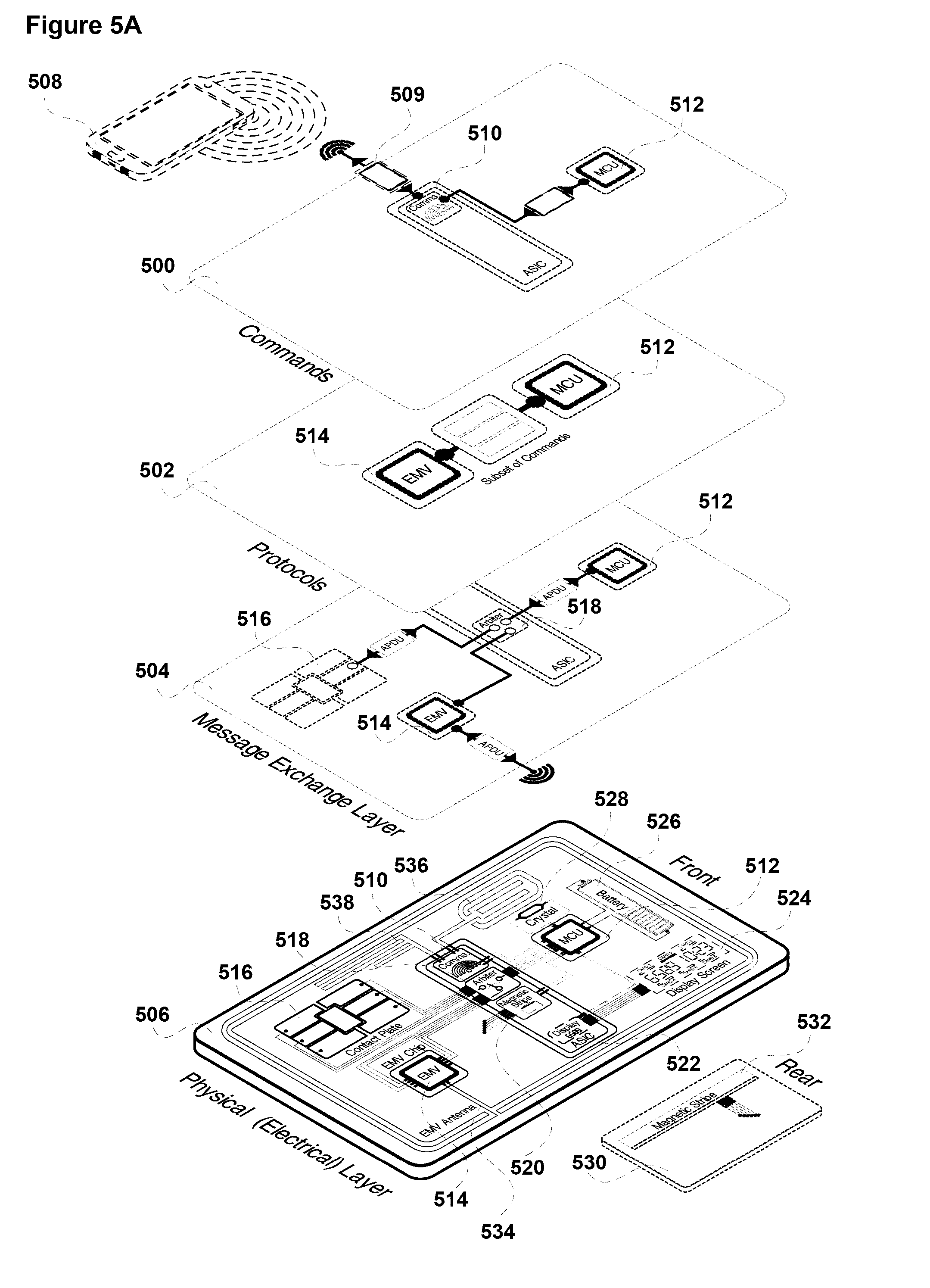

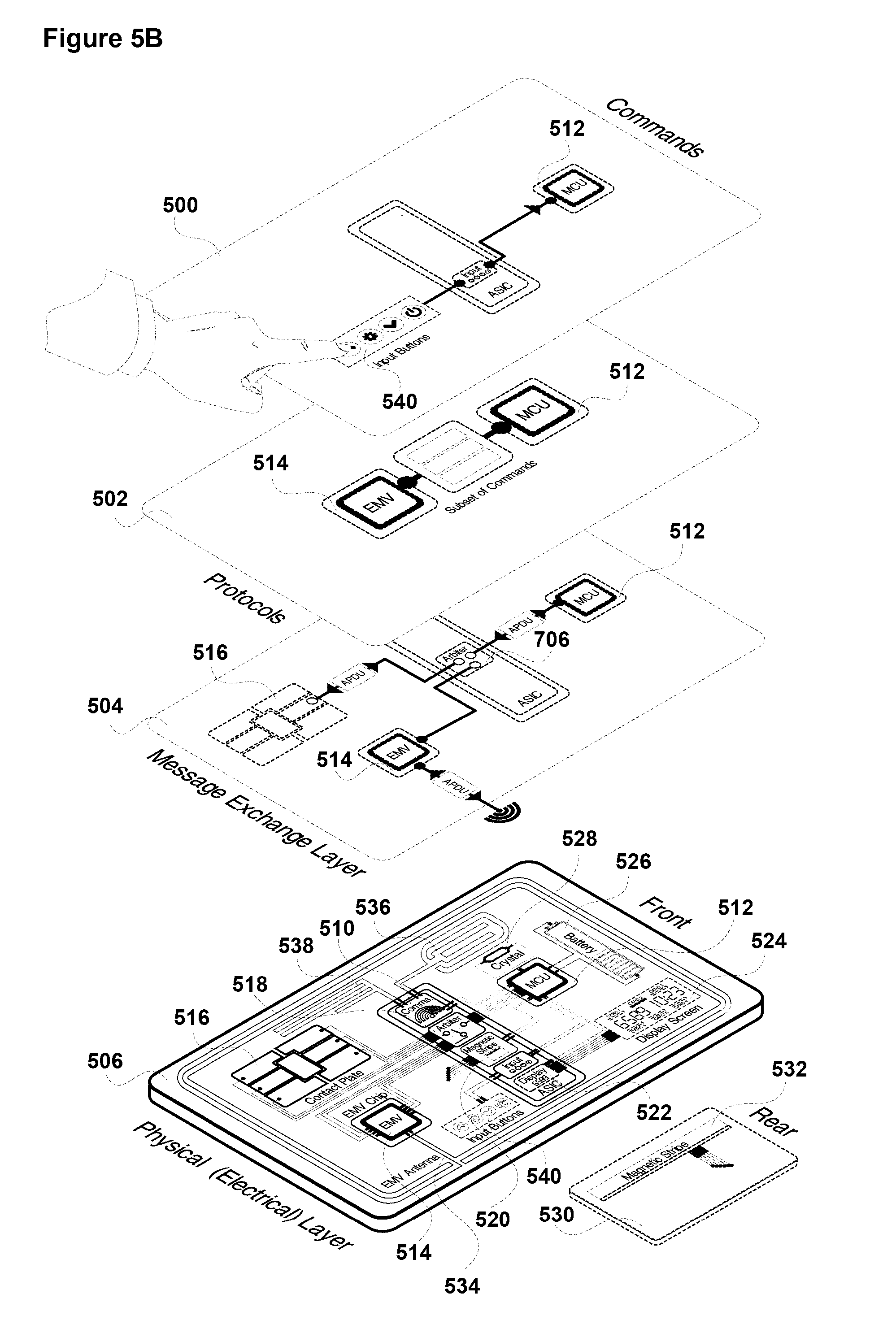

[0034] Presently, Digital Transaction Cards (DTCs) such as credit/debit cards have been capable of communications with financial institutions (e.g. banks) via a predefined keypad typically located at a financial institution-approved ATM or card reader or reader/writer. The infrastructure currently in operation restricts any interaction between a financial institution-approved reader-writer and an EMV device outside of the approved external keypad.

[0035] Existing digital transaction terminals are not able to be operated using a device such as a smartphone. For example, Electronic Funds Transfer at Point Of Sale (EFTPOS) or Point of Sale (POS) terminals are only able to operate with suitably configured Digital Transaction Cards (DTCs) such as credit or debit cards. Such credit or debit cards will each have a single "personality", or express only a single document. For example, a given DTC can only have the personality of a MasterCard or a Visa card, but cannot selectively and serially take on the personality of both a MasterCard and a Visa card, at different times.

[0036] In addition, devices such as smartphones cannot communicate with known DTCs. For example, a smartphone cannot use existing communication protocols to communicate with a credit or debit card. Accordingly, it has not been possible to reprogram, rewrite or reconfigure a DTC to provide it with a different personality.

[0037] Furthermore, known DTCs such as credit or debit cards cannot be updated to express a desired personality (for example, changing a physical card from expressing a MasterCard to expressing a Visa card). Consequently, the DTC cannot be used with a POS/EFTPOS terminal using the desired personality for the transaction.

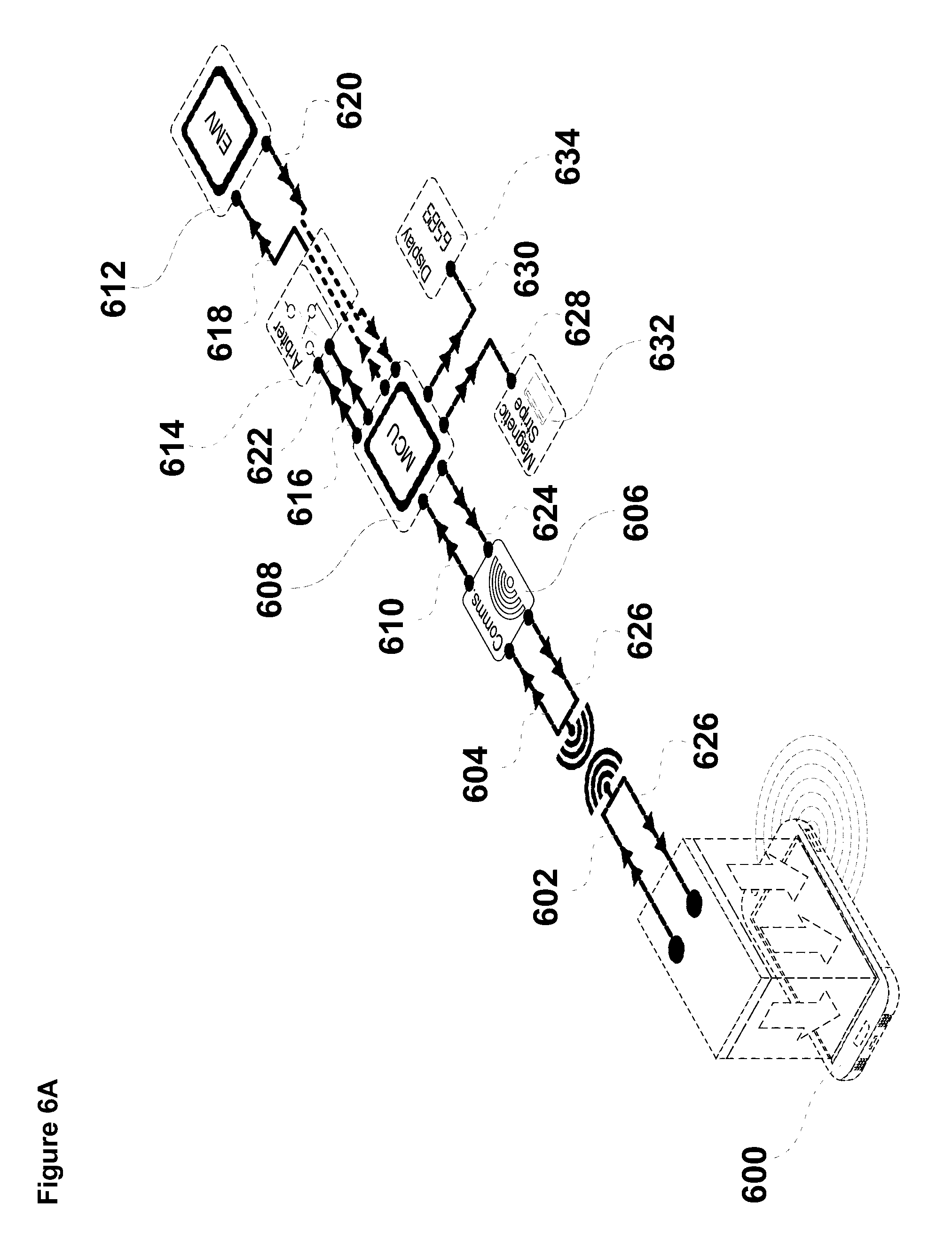

[0038] Digital Transaction Processing Units (DTPUs) embedded into a standard credit or debit card typically include contact electrodes presented on the surface of the card configured to make contact with corresponding contact electrodes in, for example, a POS/EFTPOS terminal. This physical contact allows the DTPU to communicate with the POS/EFTPOS terminal, and to connect with a payment infrastructure to complete a digital transaction. The DTPU is typically an EMV chip or a chip complying with one or more of EMV Co specifications.

[0039] Such current DTPUs or EMV chips may include an Integrated Circuit (IC), being part of the EMV chip typically formed from substances such as silicon. The EMV chip may further include Read Only Memory (ROM), Random Access Memory (RAM), and/or Electrically Erasable Programmable Read Only Memory (EEPROM). The DTPU may contain other kinds of memory. Further, the DTPU may include a Central Processing Unit (CPU) for controlling operations of the DTPU. The CPU may work in cooperation with a crypto-coprocessor, which handles the tasks of encrypting and decrypting data, thus freeing the CPU to perform other processing tasks. Communications between the DTPU and the electrodes are made via a system Input/Output (system I/O).

[0040] The IC of the EMV chip has an active side usually in some form of encapsulation, and is adhered to a substrate using adhesive. The contact electrodes, typically made of metal, are exposed for contact with external terminal devices and are connected to the IC with bond wires. The substrate is placed in a pit, which is made in the card body. The substrate, carrying the IC, the metal contact electrodes, the encapsulation, and the bond wires is fixed into the pit of the card body using hot melt, applied at the edges of the substrate.

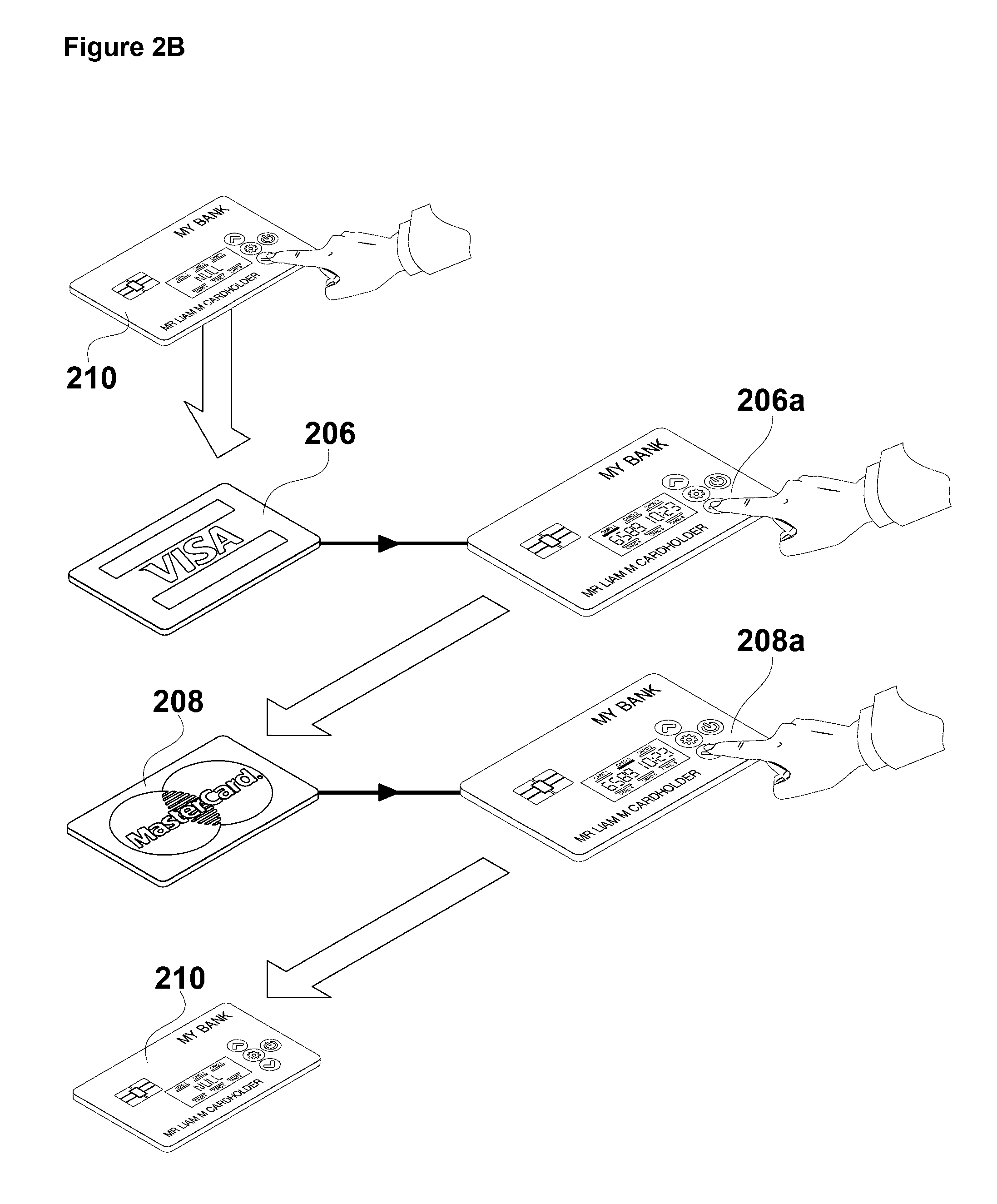

[0041] Some known DTCs include a numeric keypad which is used for controlling operations of the EMV chip embedded in the card. Such cards may also include a numeric display and one or more buttons or keys to switch the card on and off. The card may use a specially built EMV chip which allows the keypad and any other elements of the card to operate the EMV chip for limited control of the chip and for operating the display. However, this type of card is difficult to operate, as the functionality afforded by the keypad is very limited. Additionally, the display can only show a very limited amount of data. Such cards have proved to be cumbersome and difficult to operate, resulting in a very low acceptance with customers.

[0042] Accordingly, devices such as smartphones and credit and debit cards have not been able to interoperate. Such cards may be designed to interact physically with an EMV access terminal in a POS/EFTPOS terminal, and such POS/EFTPOS terminals may include a terminal module for processing transactions and communicating via an EMV interface with a payment processing infrastructure including with institutions such as an EMV issuer back office.

[0043] Devices such as smartphones may also communicate wirelessly with a wireless access node in the POS/EFTPOS terminal. However, wireless communication between smartphones and the POS/EFTPOS terminals has had very low penetration into merchants, as replacing existing infrastructure to allow for this type of operation is expensive. Furthermore, direct communication between a smartphone and a POS/EFTPOS terminal may introduce a number of security issues for such transactions.

SUMMARY OF THE INVENTION

[0044] In one aspect, the present invention provides digital transaction apparatus including a Data Assistance Device (DAD) including a user interface that is operable to at least select data and a DAD transmitter, and a Digital Transaction Card (DTC), including a Digital Transaction Processing Unit (DTPU) and a DTC receiver, wherein the DAD and DTC are operable to transfer data from the DAD to the DTC and when subsequently using the DTC to effect a digital transaction, the DTC operates in accordance with data selected and transferred from the DAD to the DTC, wherein the DTPU is configured to enable data communication with a digital transaction device during a digital transaction, the DTPU operable to receive and execute commands that emulate commands received from the digital transaction device.

[0045] In another aspect, the present invention provides a Data Assistance Device (DAD) including a user interface that is operable to at least select data and a DAD transmitter that is operable to transfer data from the DAD to a receiver associated with a Digital Transaction Card (DTC) having a Digital Transaction Processing Unit (DTPU), wherein the data that is selected and transferred to the DTC causes the DTC to operate in accordance with the selected data when the DTC is subsequently used to effect a digital transaction, and wherein the DTPU is configured to enable data communication with a digital transaction device during a digital transaction, the DTPU operable to receive and execute commands that emulate commands received from the digital transaction device.

[0046] In another aspect, the present invention provides a Digital Transaction Card (DTC) including a Digital Transaction Processing Unit (DTPU) and a DTC receiver that is operable to receive user-selected data from a transmitter associated with a Data Assistance Device (DAD), wherein the user-selected data that is received causes the DTC to operate in accordance with the user-selected data when the DTC is subsequently used to effect a digital transaction, and wherein the DTPU is configured to enable data communication with a digital transaction device during a digital transaction, the DTPU operable to receive and execute commands that emulate commands received from the digital transaction device.

[0047] In another aspect, the present invention provides a digital transaction method including selecting data, by a user interface of a Data Assistance Device (DAD), transferring the selected data by a DAD transmitter associated with the DAD to a receiver associated with a Digital Transaction Card (DTC) having a Digital Transaction Processing Unit (DTPU), and effecting, by the DTC, a digital transaction wherein the DTC operates in accordance with the data selected and transferred from the DAD to the DTC, wherein the DTPU is configured to enable data communication with a digital transaction device during a digital transaction, the DTPU operable to receive and execute commands that emulate commands received from the digital transaction device.

[0048] In yet another aspect, the present invention provides a method of operating a Data Assistance Device (DAD), including selecting data, by a user interface of the DAD, and transferring the selected data, by a DAD transmitter associated with the DAD to a receiver associated with a Digital Transaction Card (DTC) having a Digital Processing Unit (DTPU), wherein the DTPU is configured to enable data communication with a digital transaction device during a digital transaction, the DTPU operable to receive and execute commands that emulate commands received from the digital transaction device, and wherein the DTC operates in accordance with the selected and transferred data when the DTC is subsequently used to effect a digital transaction.

[0049] In a further aspect, the present invention provides a method of operating a Digital Transaction Card (DTC) having a Digital Transaction Processing Unit (DTPU), including receiving, from a Data Assistance Device (DAD), data including user-selected data, effecting, by the DTC, a digital transaction, wherein the DTC operates in accordance with the user-selected data, wherein the DTPU is configured to enable data communication with a digital transaction device during a digital transaction, the DTPU operable to receive and execute commands that emulate commands received from the digital transaction device.

[0050] In a further aspect, the present invention provides a computer-readable medium storing one or more instructions that, when executed by one or more processors associated with a Data Assistance Device (DAD), cause the one or more processors to select data, by a user interface of the DAD, and transfer the selected data, by a DAD transmitter to a receiver associated with a Digital Transaction Card (DTC) having a Digital Transaction Processing Unit (DTPU), wherein the DTPU is configured to enable data communication with a digital transaction device during a digital transaction, and the DTPU is operable to receive and execute commands that emulate commands received from the digital transaction device, the DTC operating in accordance with the selected and transferred data when the DTC is subsequently used to effect a digital transaction.

[0051] In a further aspect, the present invention provides a computer-readable medium storing one or more instructions that, when executed by one or more processors associated with a Digital Transaction Card (DTC), cause the one or more processors to receive user selected data, from a Data Assistance Device (DAD), and subsequently effect a digital transaction wherein the DTC operates in accordance with the user-selected data, wherein the DTC includes a Digital Transaction Processing Unit (DTPU) configured to enable data communication with a digital transaction device during a digital transaction, the DTPU operable to receive and execute commands that emulate commands received from the digital transaction device.

[0052] In a further aspect, the present invention provides a method including receiving, from an issuing authority, a DTC configured to operate in accordance with any one or more of the statements above.

[0053] In a further aspect, the present invention provides a method including issuing, by an issuing authority, a DTC configured to operate in accordance with any one or more of the statements above.

[0054] In a further aspect, the present invention provides a method including receiving, from an issuing authority, a DTC configured to operate in accordance with the method of any one or more of the statements above.

[0055] In a further aspect, the present invention provides a method including issuing, by an issuing authority, a DTC configured to operate in accordance with the method of any one or more of the statements above.

[0056] In a further aspect, the present invention provides a method including issuing, by an issuing authority, operating code, including software and/or firmware, to a Data Assistance Device (DAD) and/or a Digital Transaction Card (DTC) to enable the DAD and/or DTC to operate in accordance with any one or more of the statements above.

[0057] In a further aspect, the present invention provides a method including issuing, by an issuing authority, operating code, including software and/or firmware, to a Data Assistance Device (DAD) and/or a Digital Transaction Card (DTC) to enable the DAD and/or DTC to operate in accordance with the method of any one or more of the statements above.

SUMMARY OF EMBODIMENT(S) OF THE INVENTION

[0058] In embodiments, the emulation may be of one or more functions that would otherwise be enacted with the DTC, or other types of transaction cards such as credit and/or debit cards, in operation with a digital transaction device such as an Point Of Sale/Electronic Funds Transfer at Point Of Sale (POS/EFTPOS) terminal when the digital transaction device is connected to a third party entity or organization, such as a financial institution or credit card provider. In this regard, it may be expressed that, in some embodiments, the apparatus and method emulate the actions of a financial institution with the DTC, or emulate actions of a digital transaction device during a digital transaction with such a device. In other embodiments, the emulation may occur outside of a digital transaction with a digital transaction device, so that the DAD and the DTC are operable for emulation.

[0059] It will be appreciated that the DTPU in many credit and debit cards (for example, an EMV chip, or a chip complying with one or more of the EMVCo specifications), is connected to electrodes which present on the surface of the credit or debit cards. These electrodes contact corresponding electrodes in a digital transaction device, such as an POS/EFTPOS terminal, or an Automatic Teller Machine (ATM). When respective electrodes are in contact, data communication is enabled between the card and the third party entity or organization controlling the digital transaction device. The third party entity or organization may perform or control one or more functions during a transaction, such as reading a credit card number (Personal/Primary Account Number (PAN)), expiry date and other information, which is located in the DTPU of the card, or sending the read data from the transaction device back to the third party (and/or some other third party) for processing. The processing may lead to an authorization being given for the transaction, and this is communicated back to the transaction device, so that the transaction can proceed. In the present invention, emulation is for mimicking one or more of the functions that are typically performed with, for example, a credit card or debit card. However, the functions provided by the emulation may extend beyond those provided on many digital transaction devices.

[0060] In some embodiments, the emulation includes functions that are not normally provided by many or any digital transaction devices. These functions may include providing a DTC with a new personality, such that the DTC can be used as, for example, a credit card, then, after change in personality, can be used as an identification card. Other possible emulation functions include, for example, setting spend limits on a DTC, enacting authorization requirements for a DTC, changing a Personal Identification Number (PIN) (for example changing digits 0000 to 1111, or changing the number of digits 0000 to 101010), changing a public key (which is used to create a cryptogram (transaction wrapper) when used in, for example, a POS/EFTPOS terminal), and assigning different personalities for different locations or times. The types of functions that can be used during an emulation process are not limited to those mentioned in the present specification, and the present invention is intended to include within its scope all such functions.

[0061] In some embodiments, the DTC processor (which may itself be a Central Processing Unit (CPU)), is connected to the DTPU or may be directly connected with the CPU of the DTPU via electrodes. The DTPU may be an EMV chip or a chip complying with one or more EMVCo specifications. Such EMV/EMVCo chips may be connected to the external (surface) electrodes of the DTC via wires which connect into a bottom part of the chip, the wires extending to the surface electrodes on a top surface of the DTC. Similarly, the DTC CPU may be connected via wires to a bottom part of the chip. It will be understood that chips have a number of input/output channels, and that the DTC CPU and the DTPU CPU may have corresponding input/output channels. In some embodiments, the surface electrodes of the DTC are connected to a selection of input/output channels of the DTPU CPU, and the corresponding input/output channels of the DTC CPU are also connected to the same selection of input/output channels of the DTPU CPU, thus allowing the emulation to be operated from the DAD via the DTC CPU. In other embodiments, a different selection of input/output channels may be used for connection between the DTC CPU and the DTPU CPU from the channels that are connected between the DTPU CPU and the surface electrodes of the DTC.

[0062] In some embodiments, the apparatus is operable to copy a selected one LDTDP from LDTDP storage memory to the DTPU thereby enabling the DTC to be operable as the digital transaction document associated with the selected one LDTDP. The selection may be performed using the interface of the DAD during an emulation, and in cooperation with the at least one program operating on the DTC and operated from the interface of the DAD.

[0063] It will be understood by skilled readers that in embodiments of the invention, a digital transaction apparatus including, and requiring both, a Data Assistance Device (DAD) and a Digital Transaction Card (DTC) for a digital transaction provides a multi-factor factor verification (including authorization, authentication, and both authorization and authentication) for the digital transaction, the factors being that the user (for example, someone seeking to pay for goods and/or services using a financial digital transaction) requires two items, namely, the DAD and the DTC and also knowledge regarding how to effect a transaction with the two items. Accordingly, if a person has both a DAD and a DTC when seeking to conduct a digital transaction, the likelihood that the person has obtained both items by fraud, theft, or deception is significantly reduced. For example, if the DAD is a smartphone, then it is unlikely that a person seeking to conduct a fraudulent transaction would be able to steal a legitimate DTC and the owner's smartphone when compared with solely the theft of a legitimate credit card as presently used to conduct digital transactions. Further, if a person seeking to conduct a fraudulent transaction managed to steal a legitimate DTC, it would be very difficult for that person to emulate, or spoof, the DTC owner's smartphone, including any necessary additional hardware and software to operate with the DTC to conduct a digital transaction.

[0064] In embodiments, the DAD and DTC are operable to transfer data therebetween which may further assist to reduce the incidence of fraudulent digital transactions. For example, the DAD could be used to transmit a One Time PIN (OTP) to the DTC prior to each and every transaction, the OTP being requested by a digital transaction system device during a digital transaction and requiring entry of the PIN by the user to complete the transaction. In any event, it is expected that transferring data between the DAD and DTC will assist users to manage and monitor their digital transactions.

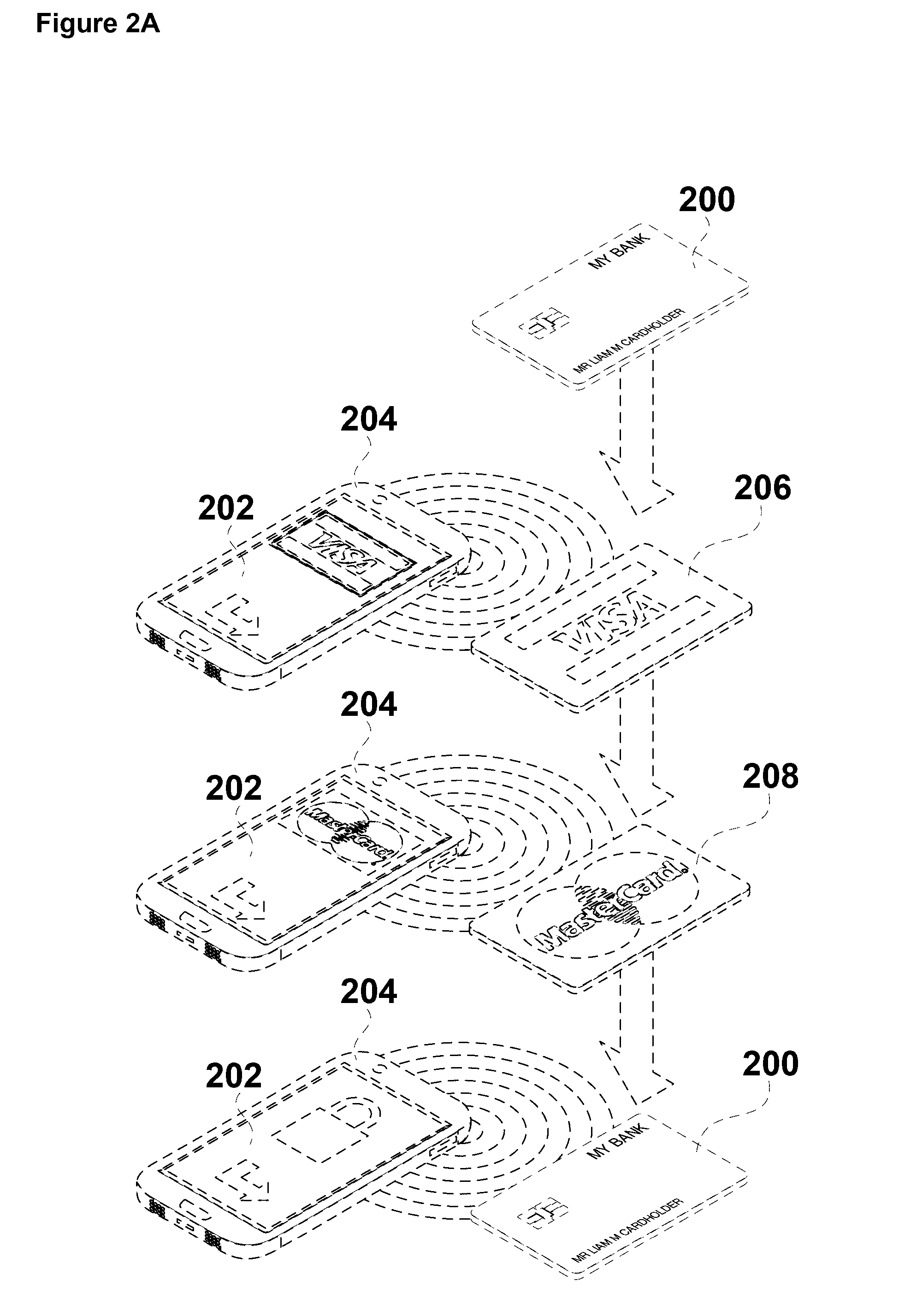

[0065] In embodiments, the present invention provides a method of conducting digital transactions using a digital transaction apparatus including a plurality of Logical Digital Transaction Document Packets (LDTDPs), each LDTDP representing a digital transaction document and including one or more of a unique Identification (unique ID) or a token associated with the unique ID for performing a digital transaction with at least one digital transaction device, the digital transaction apparatus further including, an LDTDP storage memory, a staging memory, a DAD, and a DTC, including a Digital Transaction Processing Unit (DTPU) and a secure record memory, the method including, operating the DAD to select one of the at least one LDTDPs stored in the LDTDP storage memory, copying the selected one LDTDP from LDTDP storage memory to staging memory, and copying the selected one LDTDP from staging memory to the secure record memory thus enabling the DTC to be operable as the digital transaction document associated with the selected one LDTDP. In other embodiments, a method of conducting digital transactions using a digital transaction apparatus that recognises a plurality of LDTDPs is provided, each LDTDP representing a digital transaction document and including one or more of a unique ID or a token associated with the unique ID for performing a digital transaction with at least one digital transaction device, the digital transaction apparatus further including, an LDTDP storage memory, a staging memory, a DAD, and a DTC, the DTC including a DTPU having a secure record memory, the method including, operating the DAD to select one of the at least one LDTDPs stored in the LDTDP storage memory, copying a selected one LDTDP from LDTDP storage memory to staging memory, copying the selected one LDTDP from staging memory to the secure record memory thus enabling the DTC to be operable as the digital transaction document associated with the selected one LDTDP. In these embodiments, the known operation of the existing DTPU, such as an EMV device, is exploited to place data pertaining to a particular personality in the memory location that will be accessed by the EMV device to establish the personality of the DTC.

[0066] In various embodiments, the digital transaction document may be a credit card, debit card, bank account, store card, passport, identity card, age verification card, loyalty card, government agency card, driver's license, and/or various other kinds and types of digital transaction document, which would be typically implemented as cards, documents or booklets, or implemented electronically. It will be understood that in this specification the term "logical" refers to a set of characteristics for each of the digital transaction documents, and those characteristics may be in part, or all, contained in an LDTDP representing the document or logical document. The characteristics may include data such as a unique ID for the digital transaction document, ownership information and expiry dates. The unique ID information may be a unique ID number. A change in the DTC parameters adopted by the DTPU from expressing one digital transaction document to expressing another digital transaction document may also be referred to as a change in the DTC "personality". In addition to changing parameters in a DTC such that it adopts a personality for the purpose of future transactions, in one particular embodiment, the DAD is operable to receive data pertaining to new personalities by accessing a website and is further operable to transmit relevant commands to the DTC to adopt the personality of the newly acquired personality obtained by the DAD.

[0067] In embodiments, an LDTDP may include the unique ID and a token associated with the unique ID, the unique ID and token both associated with the digital transaction document represented by the LDTDP. In other embodiments, the LDTDP may include only the unique ID associated with the digital transaction document. In yet other embodiments, the LDTDP may include only the token associated with a particular unique ID, the unique ID (and, therefore, the token) associated with the digital transaction document.

[0068] In some embodiments, each of a number of digital transaction documents may be associated with a single unique ID and a single token associated with the unique ID, each of some other digital transaction documents may be associated with a single unique ID and a number of different tokens associated with the unique ID, and each of yet other digital transaction documents may not be associated with any token (in which case such a digital transaction document will be associated only with a unique ID). In these embodiments, the unique ID and/or token for a digital transaction document (or logical digital transaction document) will be contained in an LDTDP. Where a document has a number of associated tokens, each token or token/unique ID pair, may be in a separate LDTDP. In embodiments, the unique ID for the digital transaction document contained in the LDTDP may be a Personal/Primary Account Number (PAN) if the document is a credit/debit type card, or similar kinds of unique IDs, such as unique alphanumeric ID's or unique names.

[0069] In some embodiments, the at least one of the plurality of LDTDPs is stored on the DAD, wherein the LDTDP storage memory is located on the DAD. In other embodiments, the at least one of the plurality of LDTDPs is stored in LDTDP storage memory located on the DTC, wherein selection of a LDTDP through the DAD is effected by an icon, name or other indicator associated with the LDTDP, although the LDTDP is not itself stored on the DAD. In this example, the selection of the LDTDP is communicated to the DTC by data indicating which LDTDP has been selected, and the DTC implements the selected LDTDP from its LDTDP storage memory based on the indicative data.

[0070] In yet other embodiments, a part of each of the at least one of the plurality of LDTDPs is stored on the DAD. Another part of each corresponding at least one LDTDP is stored on the DTC, wherein the selection is based on the part stored on the DAD. The part of the LDTDP selected is transmitted to the DTC, and the determination of which part of the LDTDP matches the selected part is made on the DTC. In this way, the two parts of the LDTDP can be combined to form the whole LDTDP, which can then be implemented by the DTC. In such an embodiment, the LDTDP storage memory is split between the DAD and the DTC.

[0071] In an embodiment, the DAD is enabled to store and provide for selection of an LDTDP, which is implemented as a digital transaction document on the DTC. The selection of the document associated with an LDTDP (or selection of the LDTDP) may occur before selection of a token associated with the LDTDP. Where a document has only one associated token, the selection of the document may be selection of the associated token, since a further selection process is not required. In some embodiments, selection of a token automatically indicates which LDTDP is to be selected, since the token is associated only with one document (or one LDTDP).

[0072] In another embodiment, the user may select an LDTDP and a predetermined token is selected based on context determined by the DAD. For example, if the DAD determines different locations, then a token can be automatically selected based on the determined location.

[0073] In various embodiments, some digital transaction documents contained in an LDTDP will have only one associated token and other digital transaction documents will have multiple associated tokens. It will be understood that embodiments described in this specification include both options, unless otherwise stated or unless the inclusion of both options results in an embodiment that is not possible to implement.

[0074] In various embodiments, some identifying information in respect of a digital transaction document contained in an LDTDP will not need to be stored in the apparatus LDTDP storage memory (either in the device memory or the card memory) since the token(s) stored in the apparatus will be sufficient to identify its (their) associated digital transaction document(s).

[0075] For example, where the digital transaction document is a credit card, the card number (the PAN) is not contained in the LDTDP and instead, the tokens associated with the credit card are sufficient to identify the particular credit card. In such an example, the credit card PAN may include the typical 4 leading digits which identifies the card as being of a certain type or brand (MasterCard, Visa, etc.). A token for the particular credit card may have the same four leading digits, but with different remaining digits, so that the token identifies the card with which it is associated. It will be understood by skilled readers that not having a PAN, for example, contained in the respective LDTDP and stored in the apparatus LDTDP storage memory (either in the DAD memory or the DTC memory) should increase security for the associated digital transaction document. In such examples, only the digital token containing LDTDPs are selected by the DAD, with the associated digital transaction document being automatically identified and selected.

[0076] In one embodiment, the DTPU CPU operates to copy data from the staging memory (staging area) to the EEPROM, or a part of the EEPROM, which has been set aside for secure record memory (secure element). In other embodiments, the DTPU CPU operates to copy part of the data from the staging memory to a part of the EEPROM, which has been set aside for secure record memory, and another part of the data to part of the EEPROM which has not been set aside for secure record memory. When, for example, an LDTDP is copied into secure record memory (secure element), the DTPU uses the digital transaction document information from the LDTDP (unique ID, token, commencement date/time, expiry date/time, etc.) to attain a personality, such that the DTC operates as the associated digital transaction document with the document's associated characteristics, such as commencement date/time, expiry date/time, etc.

[0077] It will be understood by skilled readers that a particular digital transaction document may be represented by one or more LDTDPs. For example, a digital transaction document associated only with a unique ID will be represented by a single LDTDP including that unique ID. In this example, the LDTDP being copied to secure record memory (which may be referred to as a secure element, or a secure element area) causes the DTC to operate as the digital transaction document associated with the unique ID.

[0078] In another example, a digital transaction document associated with a unique ID and a single token may be represented by a single LDTDP including the unique ID and the token. In this example, the LDTDP being copied to secure record memory (secure element) causes the DTC to operate as the digital transaction document associated with the tokenized unique ID. Alternatively, a digital transaction document associated with a unique ID and a single token may be represented by two LDTDPs, one of which includes the unique ID, the other including the token. In this alternative example, the LDTDP including the unique ID being copied to secure record memory (secure element) causes the DTC to operate as the digital transaction document associated with the unique ID (untokenized), whereas the LDTDP including the token associated with the unique ID being copied to secure record memory (secure element) causes the DTC to operate as the digital transaction document associated with the tokenized unique ID.

[0079] In yet another example, a digital transaction document associated with a unique ID and multiple tokens may be represented by various LDTDPs including both the unique ID and one of the multiple tokens, or could be represented by one LDTDP containing the unique ID, and a number of other LDTDPs, each containing one of the multiple tokens associated with the unique ID associated with the digital transaction document represented by all the LDTDPs, wherein the one of the LDTDPs being copied to secure record memory causes the DTC to operate as either the digital transaction document associated with the tokenized unique ID, or the digital transaction document associated with the untokenized unique ID.

[0080] Other arrangements for the LDTDPs may be contemplated, depending on the nature of the digital transaction document represented by the LDTDP (or LDTDPs).

[0081] In some embodiments, an LDTDP may also contain further data associated with a digital transaction document, such as an expiry date for the document. It may also be desirable in some circumstances to have multiple expiry dates in an LDTDP, for example, one expiry date for the unique ID (or for the associated digital transaction document) and another expiry date for a token associated with the unique ID. It will be understood that, where a digital transaction document has a number of associated tokens, each token may have a different expiry date, which will be contained in the respective LDTDP.

[0082] Further, the LDTDP for some digital transaction documents may include a commencement date, so that the period between commencement of validity and expiry of validity of the document (and/or one or more tokens associated therewith) can be controlled. For example, it may be desirable to have the digital transaction document valid for only one day if the document is a door pass, or some other card or pass, with a short validity requirement. Moreover, the commencement and expiry in the LDTDP could include times as well as dates for finer control of the validity period of the digital transaction document (and/or one or more tokens associated therewith).

[0083] In other embodiments, the further data contained in an LDTDP may include a security code associated with the unique ID of the document, and may also include a number of other different security codes associated with one or more tokens also contained in the LDTDP. For example, where the digital transaction document is a credit card, the security codes may be Card Verification Value 2 (CVV2) security codes, or similar. In this example, the unique ID is a PAN, which has an associated CVV2 security code, and the PAN has, perhaps, five associated tokens, each token also having an associated CVV2.

[0084] In yet other embodiments, the LDTDP may contain a Personal Identification Number (PIN) for the digital transaction document. There may be one PIN associated with the unique ID of the document, and other (different) PINs, each associated with a token. In some embodiments, the PINs could be One-Time PINs (OTPs), which expire after being used for a single transaction. In other embodiments, the PINs may have a limited period of validity, for example, expiring one week after first use.

[0085] In other embodiments, the LDTDP may contain other data, such as name, date-of-birth, physical characteristics, and other personal data of a person who owns the digital transaction document. For example, if the digital transaction document is a passport, for certain transactions an LDTDP containing the passport unique ID and eye color of the owner may be desired for authentication and/or verification in such transactions.

[0086] The LDTDP may be described as including, containing, wrapping or embodying a unique ID, token and/or other data. Further, the LDTDP may be encrypted (or otherwise secured) to protect the data contained in the LDTDP. In yet other embodiments, the LDTDP may be secured by using a public/private key infrastructure. The public and private keys may be issued by, for example, the DTC's primary issuer. Alternatively, the public and private keys may be issued by a primary issuer of an LDTDP, for example, a credit card provider.

[0087] In some embodiments, the DTPU may include a System Input/Output (System I/O) for inputting and outputting data and/or encrypted data to and from the DTPU. The System I/O is a means by which the LDTDP can be copied into secure record memory (secure element), allowing the DTPU to operate with the personality of the logical digital transaction document contained in the LDTDP. The secure element could be located on one or more devices. It could also be located in a single device with a virtual partition, or a folder.

[0088] The DTPU may also include a processor, or Central Processing Unit (CPU), which operates to control the DPTU. Further, the DTPU may include a crypto-coprocessor for encrypting and decrypting data efficiently, thus allowing the DTPU CPU to operate more efficiently without having the burden of encryption and decryption tasks. In some embodiments, the DTPU CPU and crypto-processor co-operate to decrypt (unwrap, unpack, or otherwise deal with) a selected LDTDP, before or while being stored in secure record memory, such that the DTPU can operate with data from the LDTDP.

[0089] The DTPU may also include various different types of memory, such as Read Only Memory (ROM), Random Access Memory (RAM), and Electrically Erasable Programmable Read Only Memory (EEPROM). In some embodiments, one of the types of memory can be used for the secure record memory (also known as a secure element), with one of the other types of memory used for the staging memory (which may also be referred to as a staging area). Any one of the abovementioned types of memory could be used as LDTDP storage memory.

[0090] In some embodiments, the DTPU is an EMV device, or a device that conforms with one or more EMVCo specifications. In other embodiments, the DTPU is an EMV device (otherwise conforming to one or more EMVCo specifications), which is constructed to read a secure storage area (staging memory/staging area) for the purpose of establishing the personality of the card in which the DTPU is installed. The secure storage area, or staging memory, may be within the constructed EMV device, within the constructed EMV device storage area (memory), or within some other secure memory.

[0091] In embodiments, the CPU of the DTPU and/or a CPU that is external to the DTPU but resident within the DTC (referred to as an external DTC processor) is activated only after the CPU or the external CPU securely identifies itself to a linked DAD, such as a smartphone. In some embodiments, linking between the DAD (for example, a smartphone) and the DTC uses strong encryption for the ID and transfer of data. Links may be unique to each set (smartphone and DTC).

[0092] In embodiments, the linking between the DAD and the DTC is wireless, and may be formed using respective transceivers of the DAD and DTC. In yet other embodiments, the DTC is linkable" (i.e. operable to establish communications) with the DAD using a physical connection, such as a data cable. In such embodiments, the data cable may be adapted at one end to plug in to a communications port, such as a USB port, on the DAD, with the other end adapted to clamp or clip on to a part of the DTC. The DTC may have electrodes, or metal plates at or towards an edge thereof to connect with the cable when clamping or clipping the other end of the data cable to the DTC. In some embodiments, the respective transceivers for the DAD and the DTC may be suitable for Bluetooth.TM., Low Energy Bluetooth.TM., Wi-Fi, NFC, ANT+, or other types of contactless, or wireless communication transceivers. In embodiments, the DTC may include a button, or a similar device, to activate linking with the DAD.

[0093] In various embodiments, the DAD is operable to transfer data to the DTC without the formation of a direct link between the DAD and DTC. In such embodiments, the DAD is used to transfer data, for example, via the internet to a (cloud) connected third party device. A link between the DAD and the third party device for the data transfer can be temporary, and that link can be terminated once the data has been completely transferred. The third party device is connected, for example, to a network (perhaps via another third party, such as a payment processor), which enables the third party device to form a link and communicate with a digital transaction system device, such as a Point Of Sale/Electronic Funds Transfer at Point Of Sale (POS/EFTPOS) terminal or Automatic Teller Machine (ATM), subsequent to forming a link with the network and thence to the digital transaction system device. The third party device is enabled to transfer the data previously received from the DAD to the digital transaction system device. A holder of a DTC (which may be a person different from the owner and/or operator of the DAD) can take the DTC to the digital transaction device, and by insertion, or placing the DTC proximal to the device, the DTC holder can obtain data from the digital transaction system device. In this way, data from the DAD can be transferred indirectly and asynchronously to the DTC. This indirect data communication between the DAD and the DTC can also be reversed such that the DTC indirectly and asynchronously transfers data to the DAD, perhaps using the same infrastructure of the digital transaction system device, the network including the payment processor, the third party device and the internet. It will be recognised that the indirect and asynchronous data transfer may be useful where a first person has a DAD and wants to send data to a DTC in the control of a second person who is geographically remote from the first person. For example, a mother operating her DAD may prefer to increase spending limits of a DTC operated by her son who is travelling in a foreign country.

[0094] In embodiments, the external DTC CPU controls the reading and re-reading of the DTPU (for example, an EMV device), and updating the memory contents of the DTPU.

[0095] In embodiments, a DTC includes a wearable payment device such as a watch but also includes payment devices that are incorporated into pieces of jewellery such as finger rings, bangles and pendants. The DTC could also comprise an implantable payment device, which includes chip and transceiver arrangements which may be suitably configured for subcutaneous implantation.

[0096] In other embodiments, the DAD may be a smartphone, or another suitable device such as a fob, or key fob, or a portable processing device with an internal/external wireless communications capability such as an NFC reader/writer which is configured to operate as a DAD. In some embodiments, the DAD may be, or may include a wearable device, such as a watch or other piece of jewellery. In this regard, some smartphones presently operate with wearable wrist (or watch-like) devices. It is envisaged that future smartphones may be wholly incorporated into a wearable device, and that the DAD can be such a device. In the circumstance that the DAD includes a smartphone operating with a wearable wrist (or watch-like) device, the wearable component may have its own unique ID, which can be used for securing linking and data transfer between the DAD and the DTC in cooperation with unique IDs, respectively, for a smart phone and the DTC.