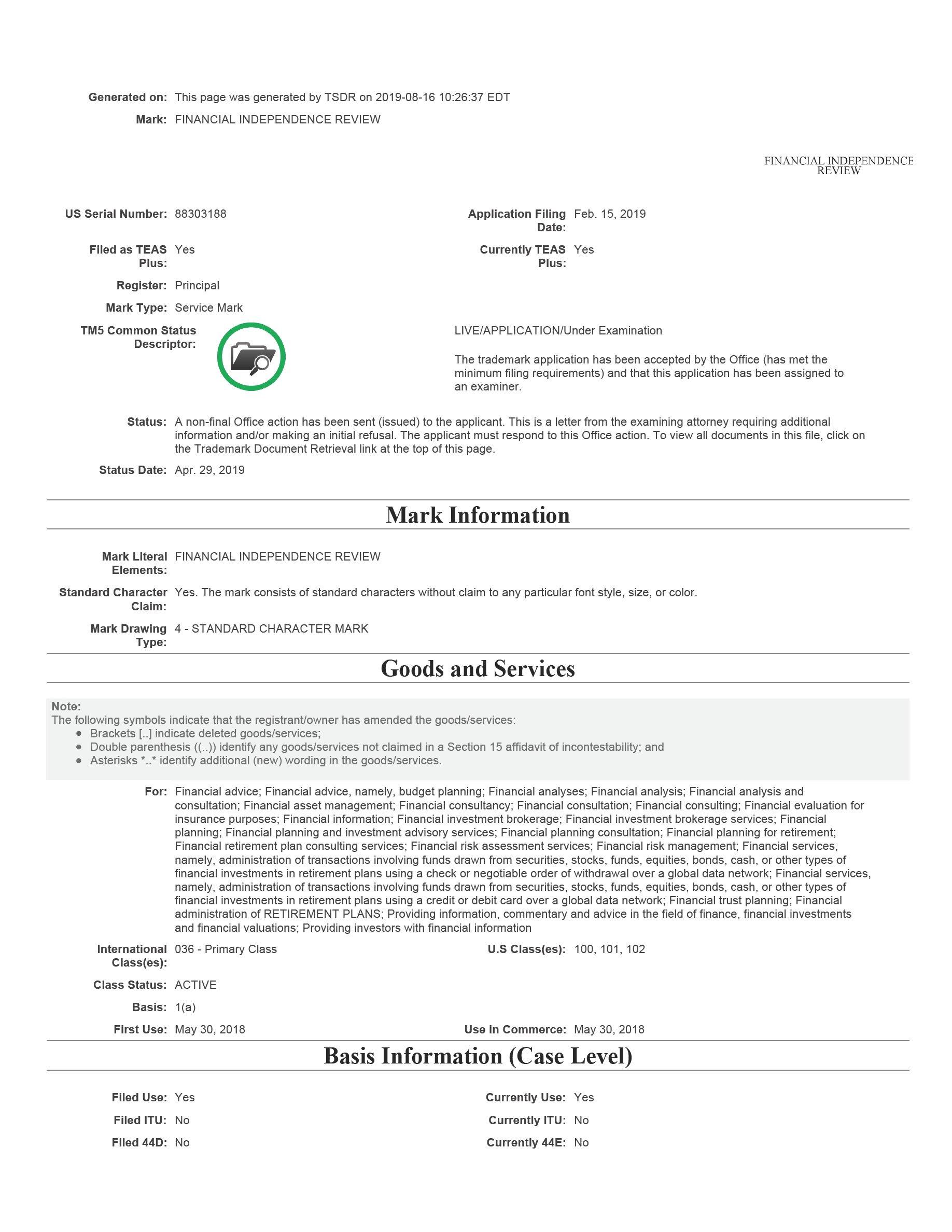

| Under the Paperwork Reduction Act of 1995 no persons are required to respond to a collection of information unless it displays a valid OMB control number. PTO Form 1957 (Rev 10/2011) |

| OMB No. 0651-0050 (Exp 09/20/2020) |

| Input Field |

Entered |

|---|---|

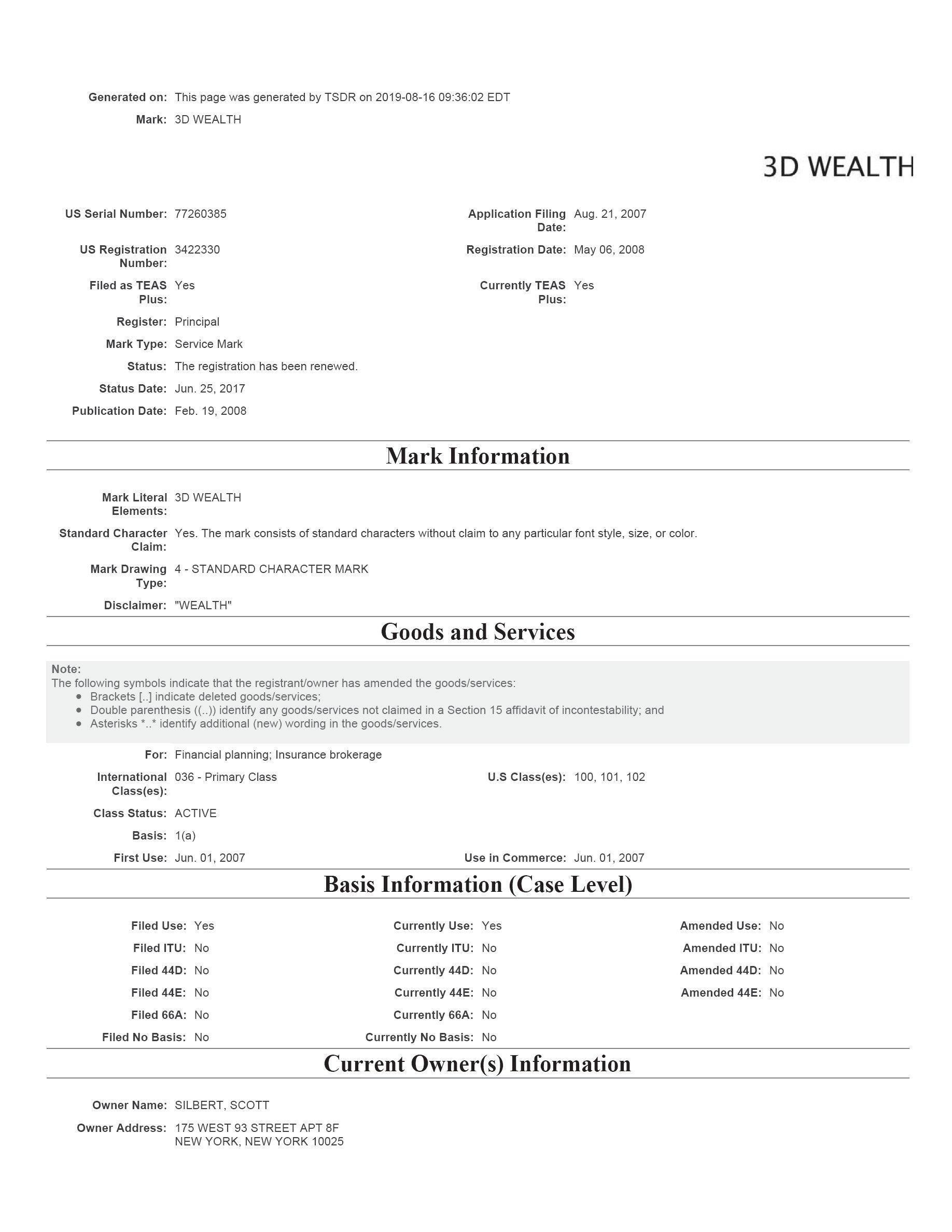

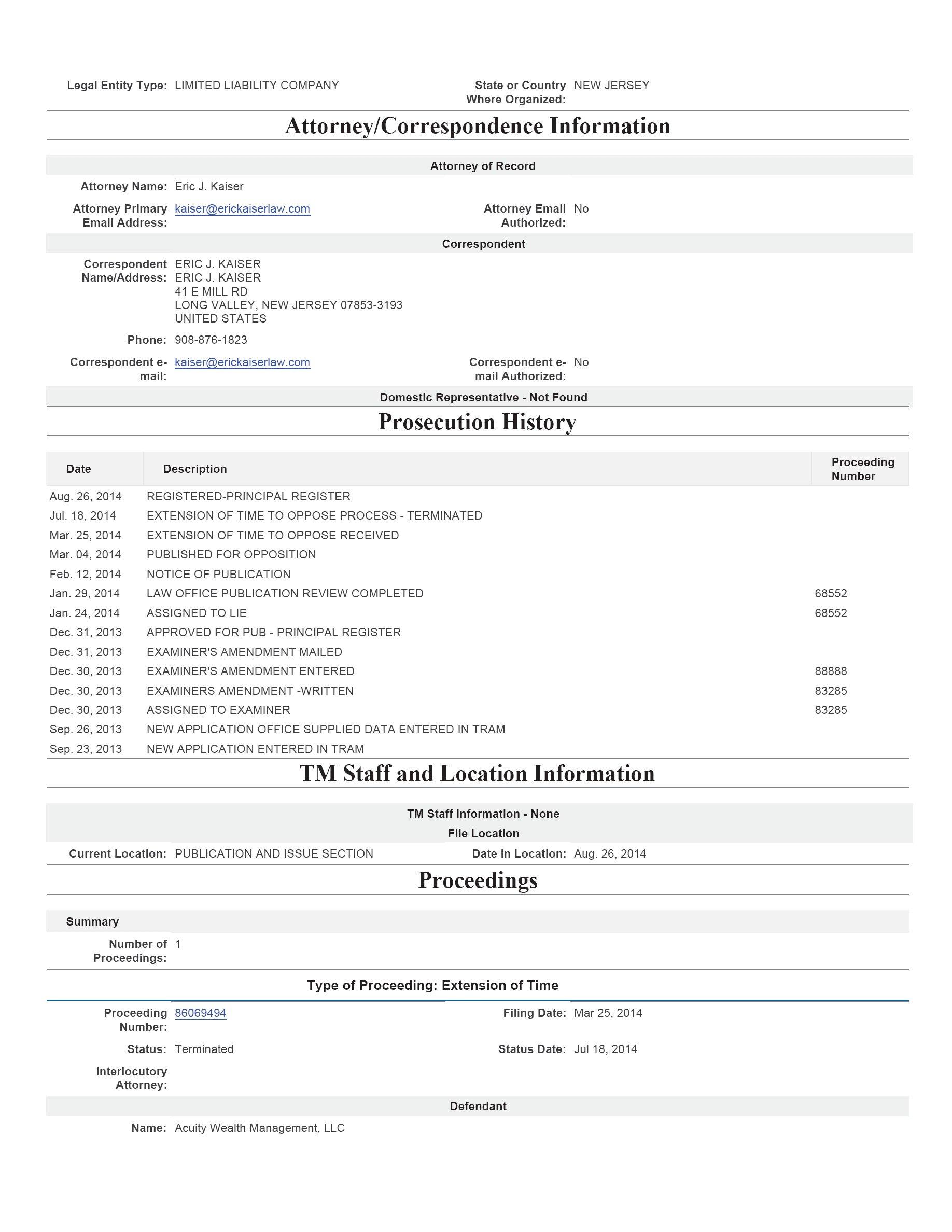

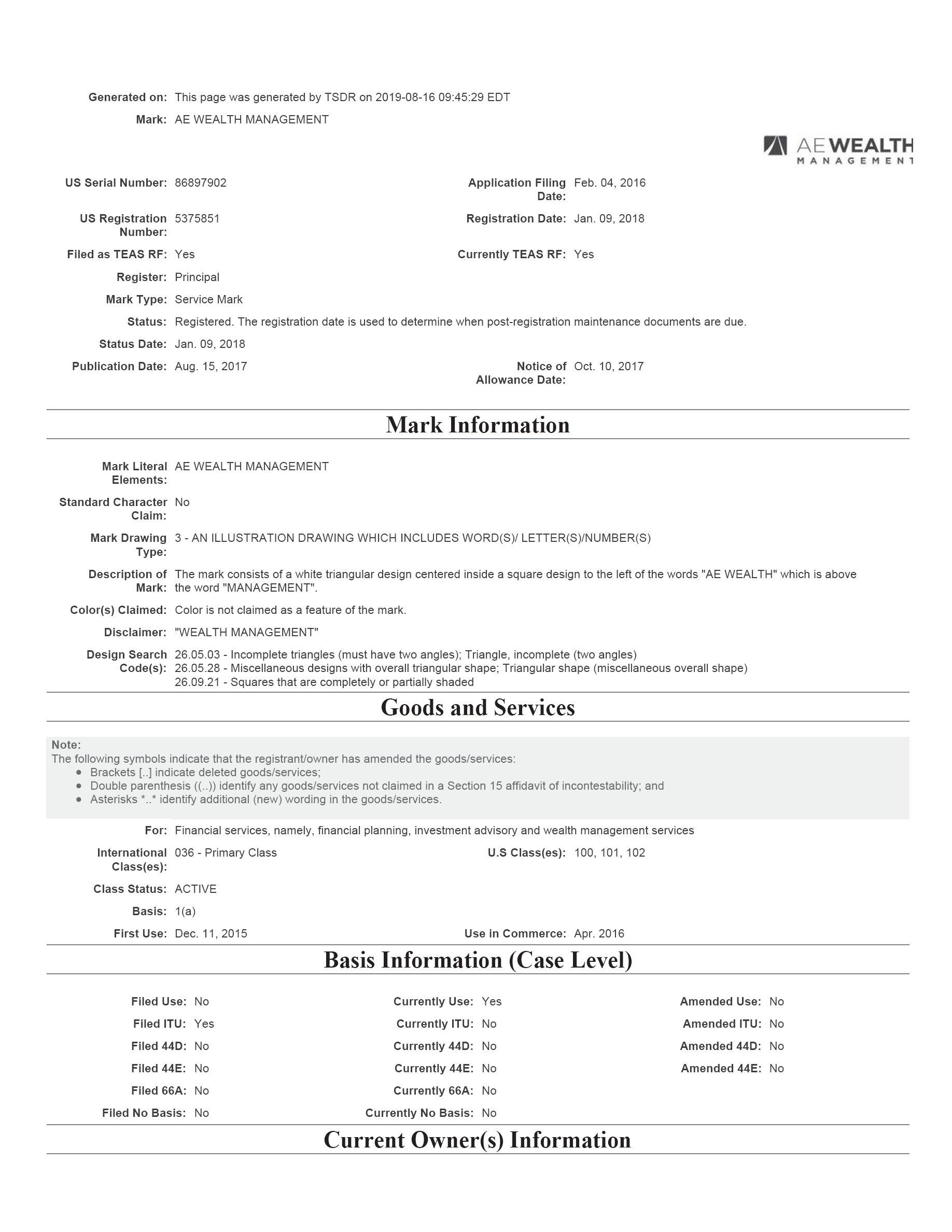

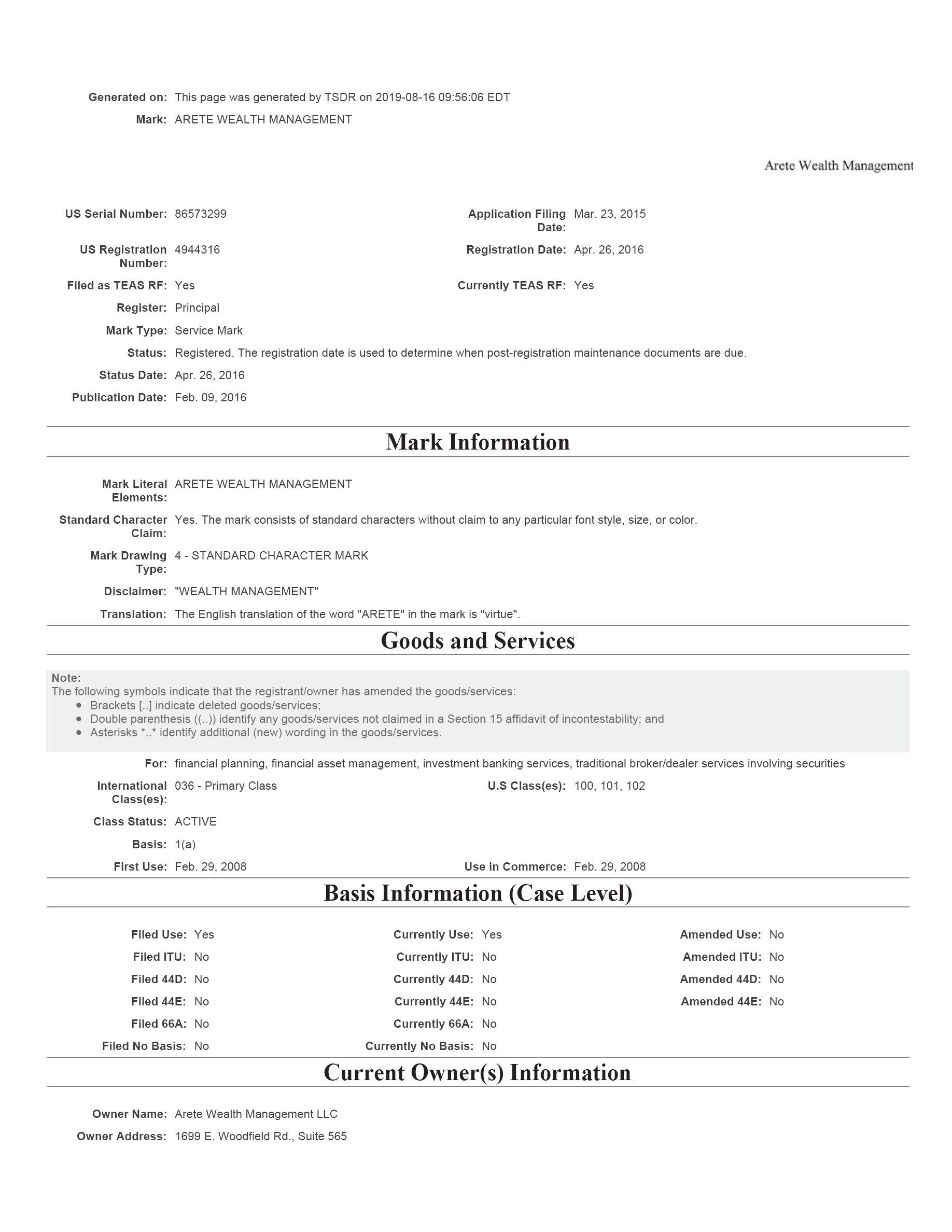

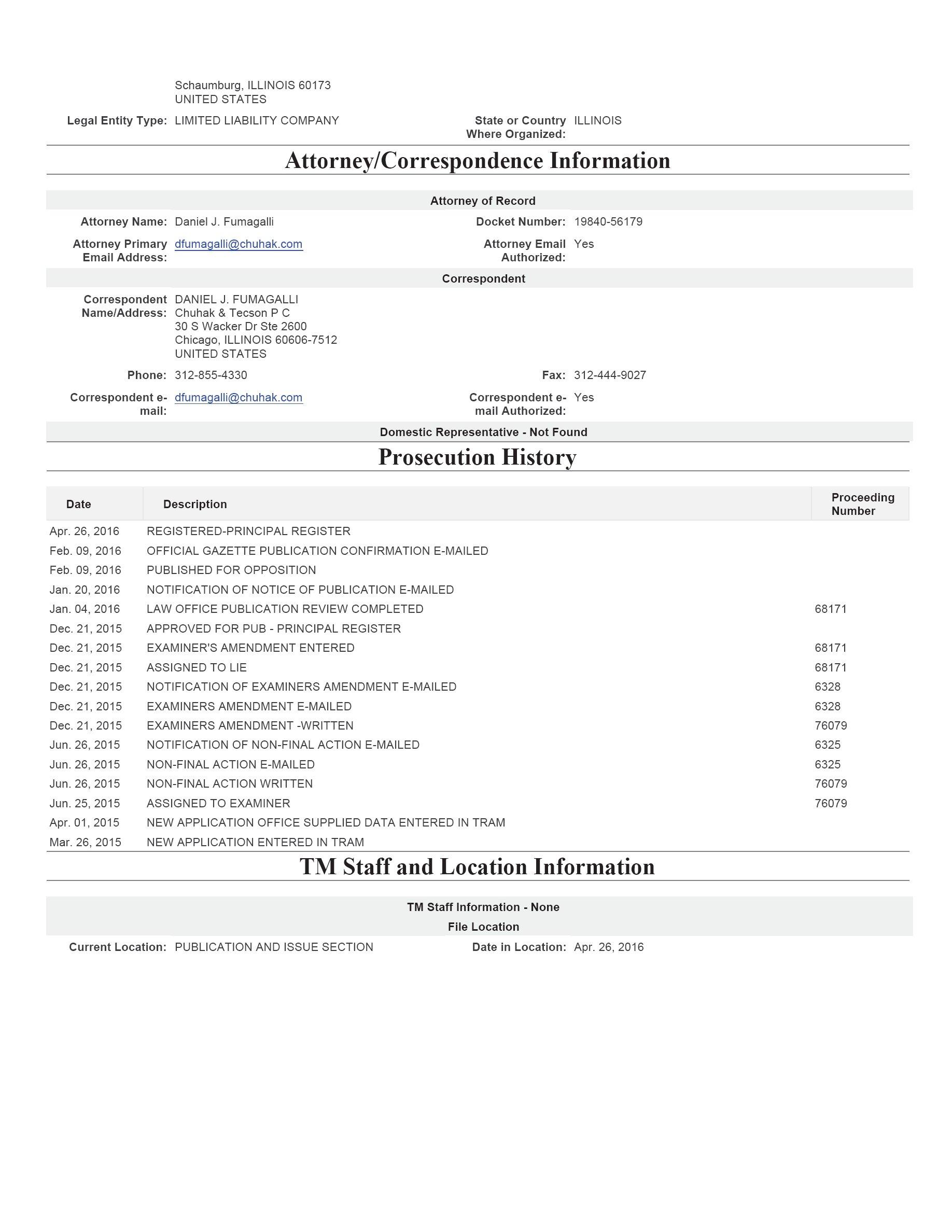

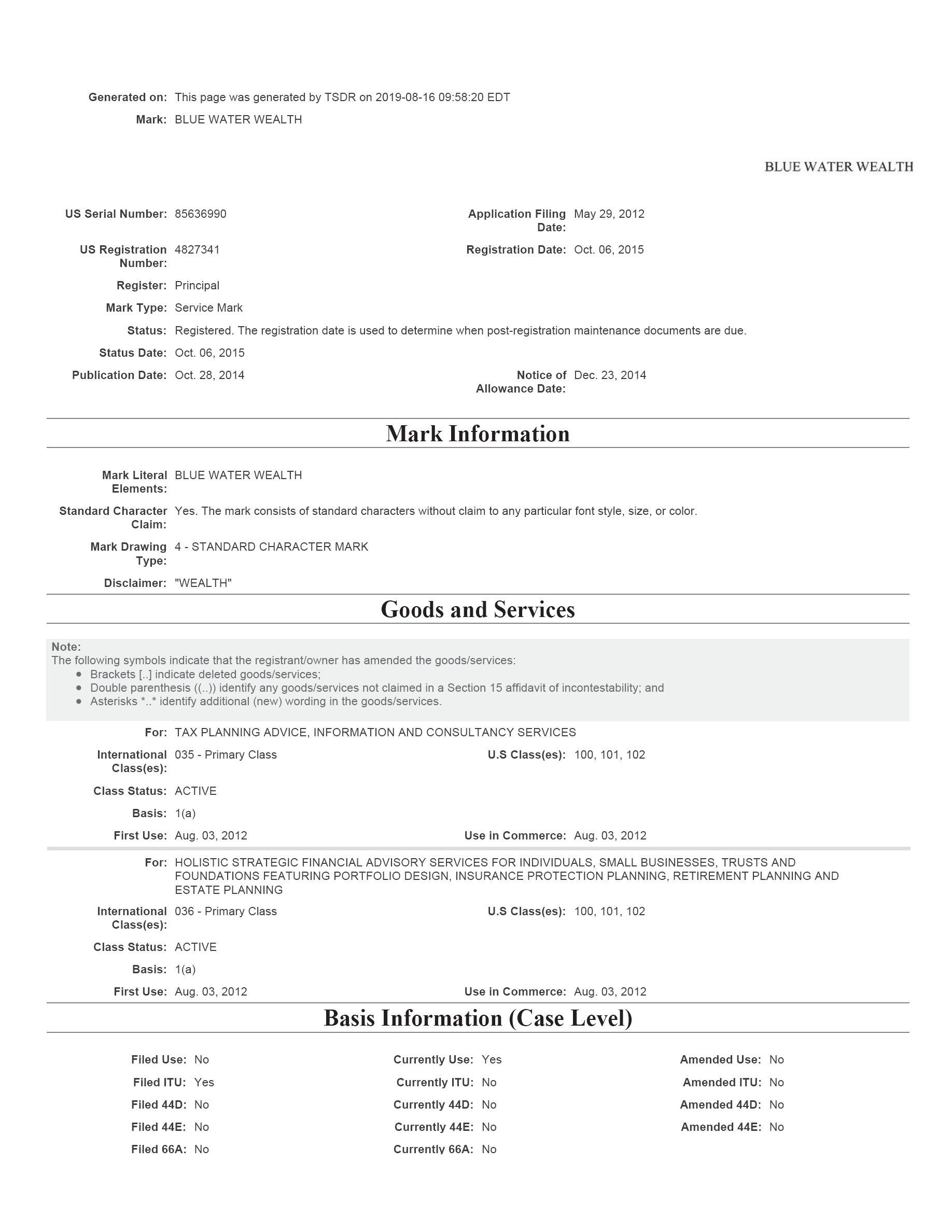

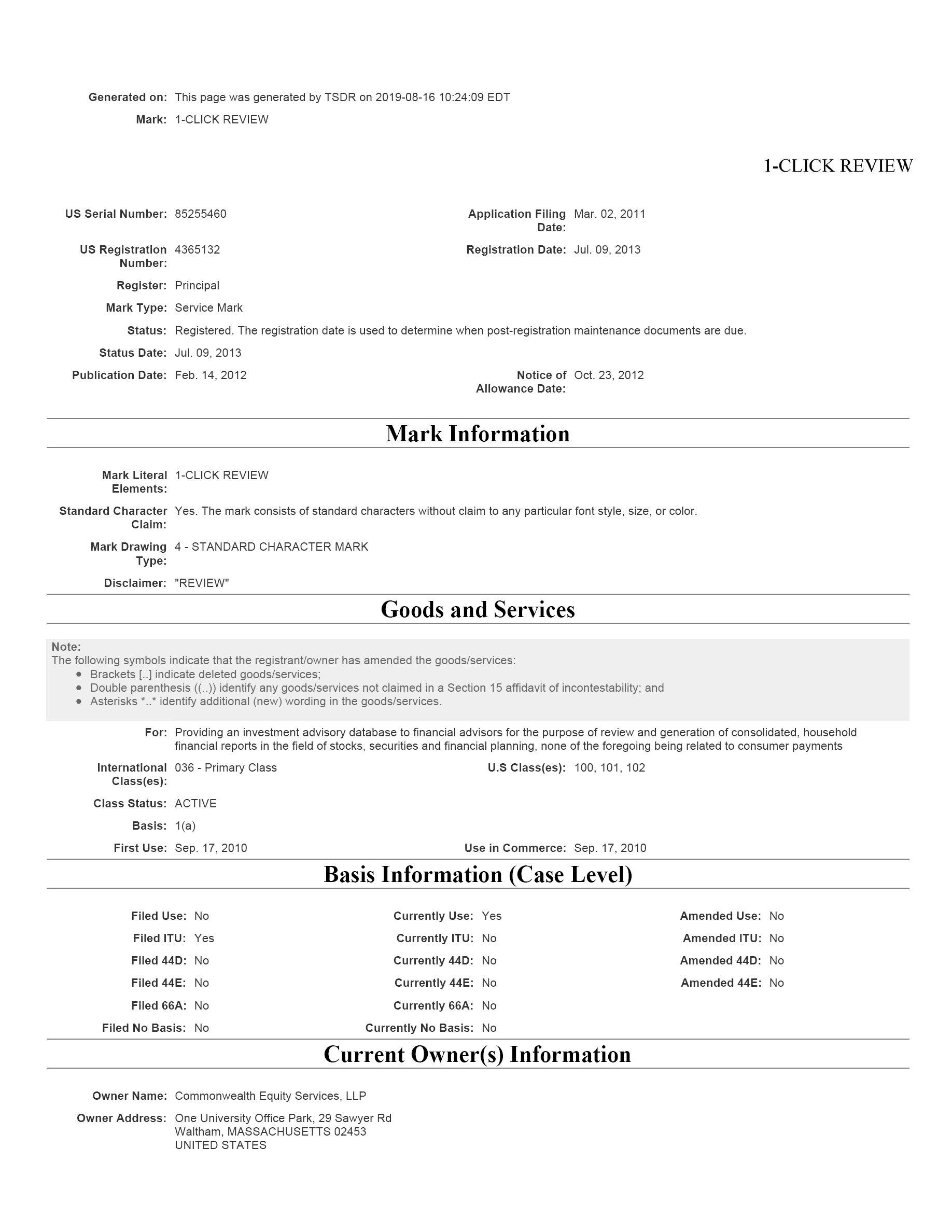

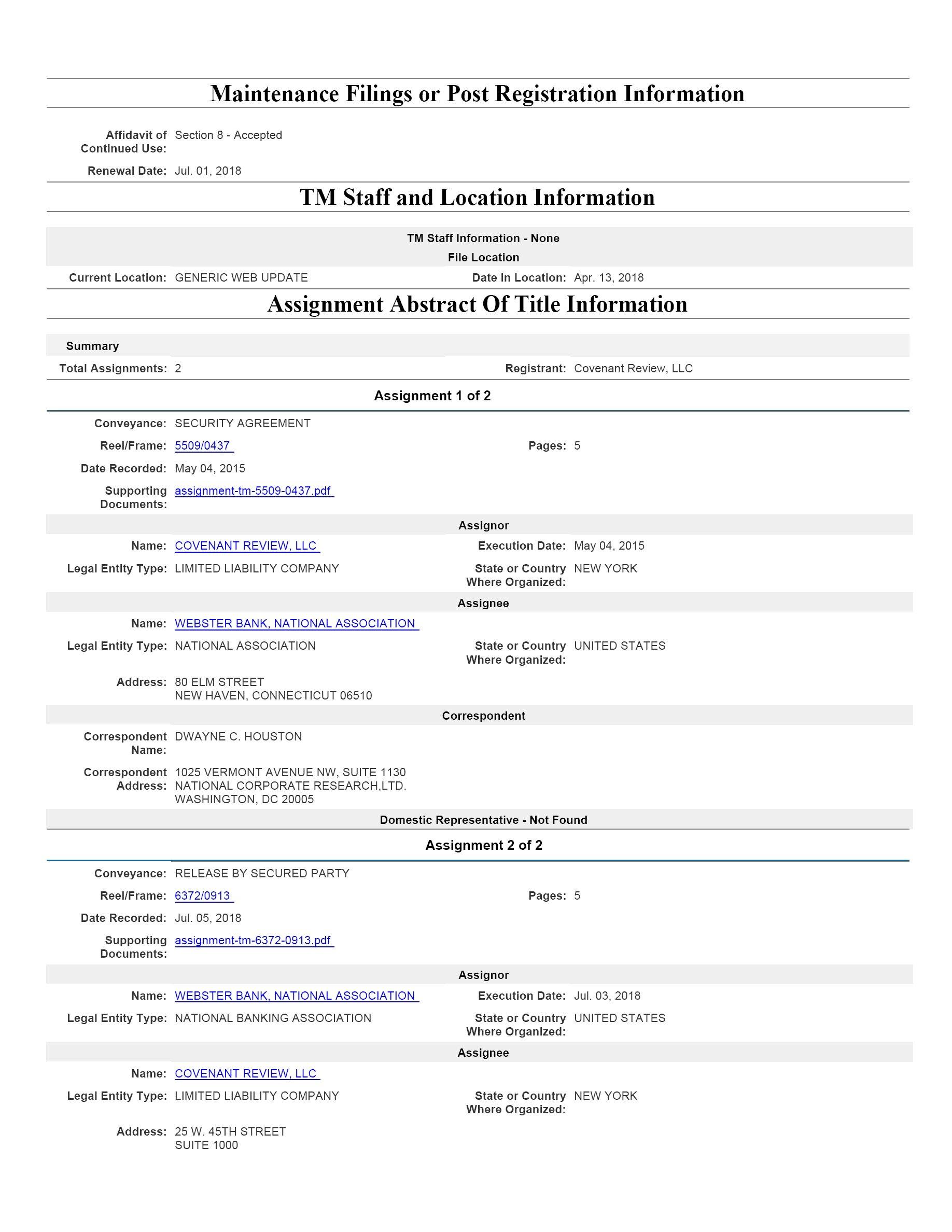

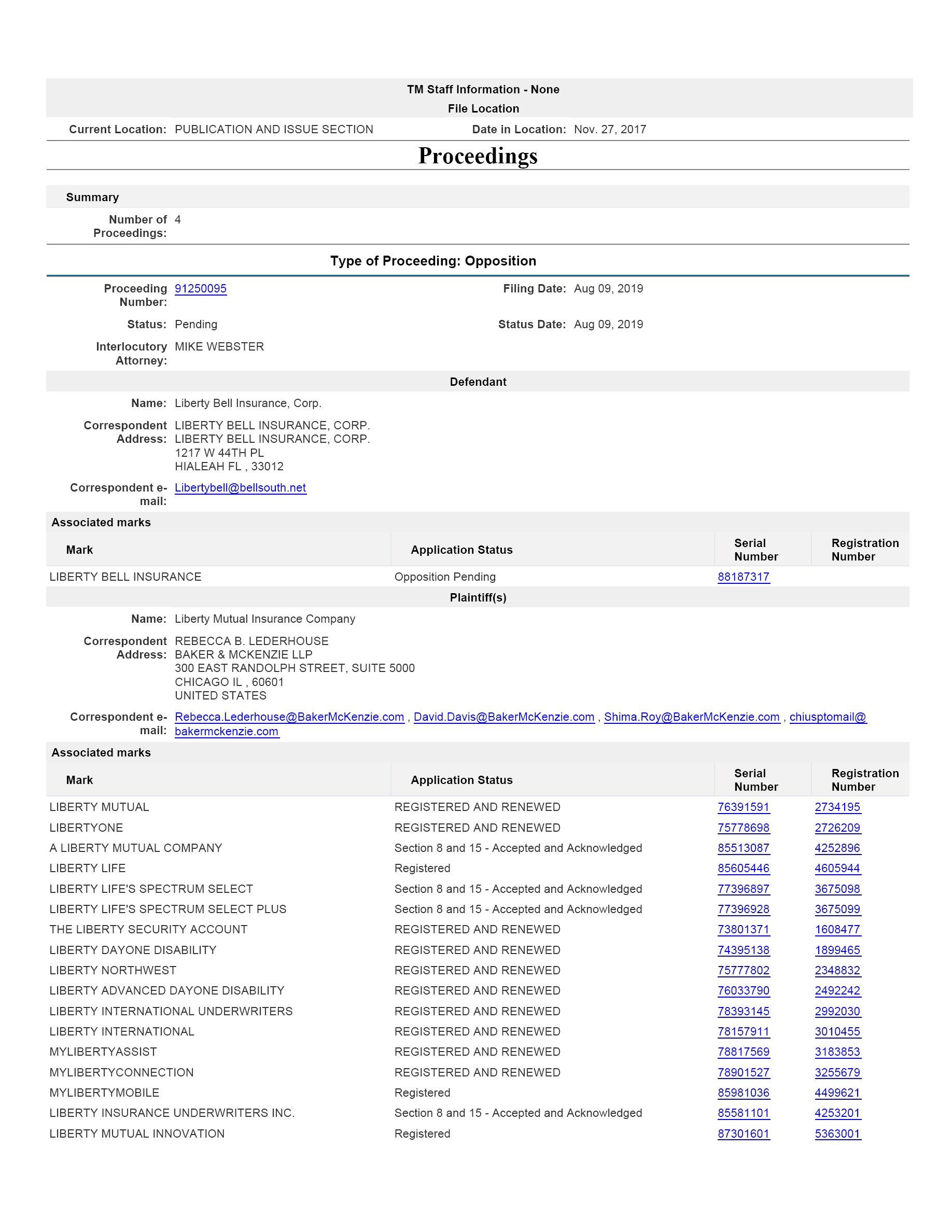

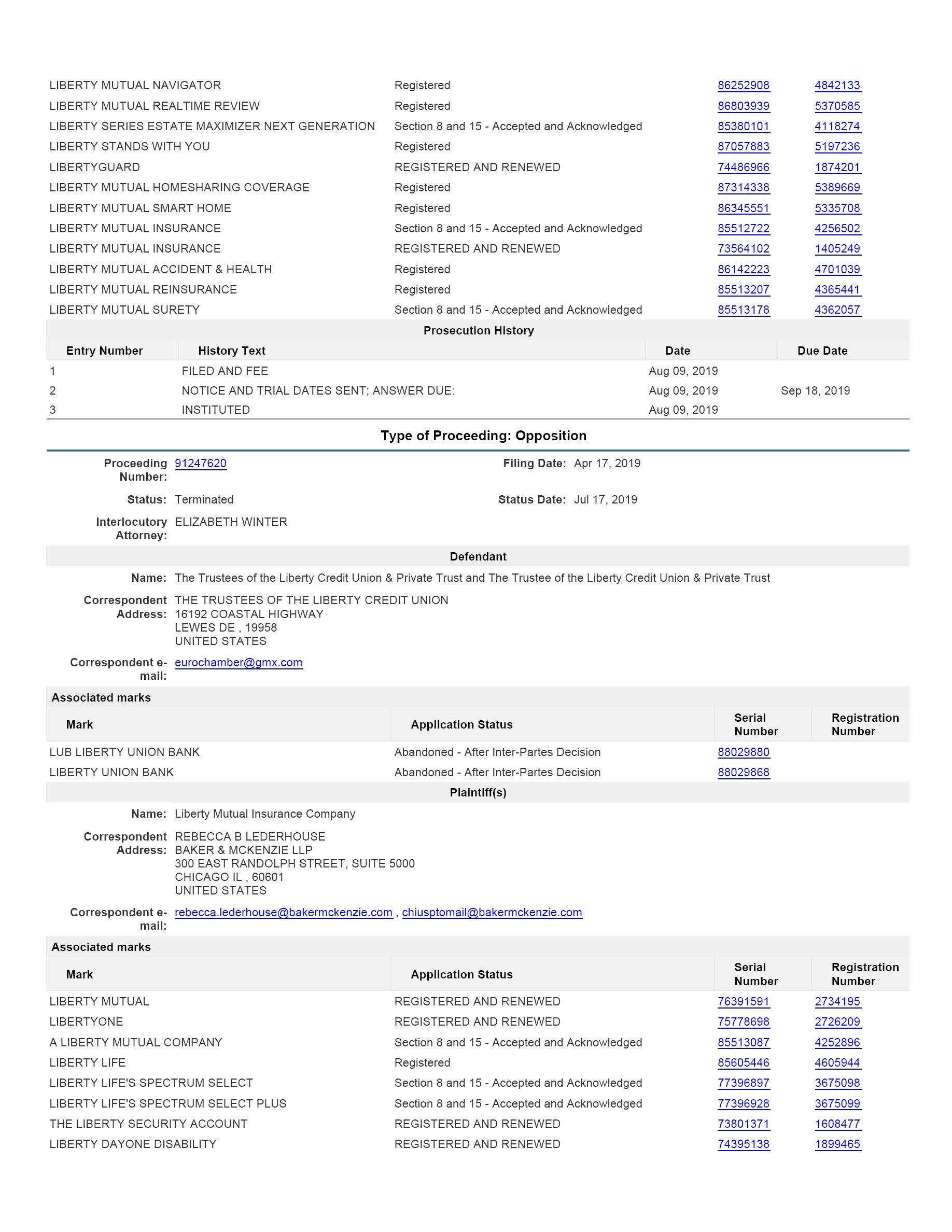

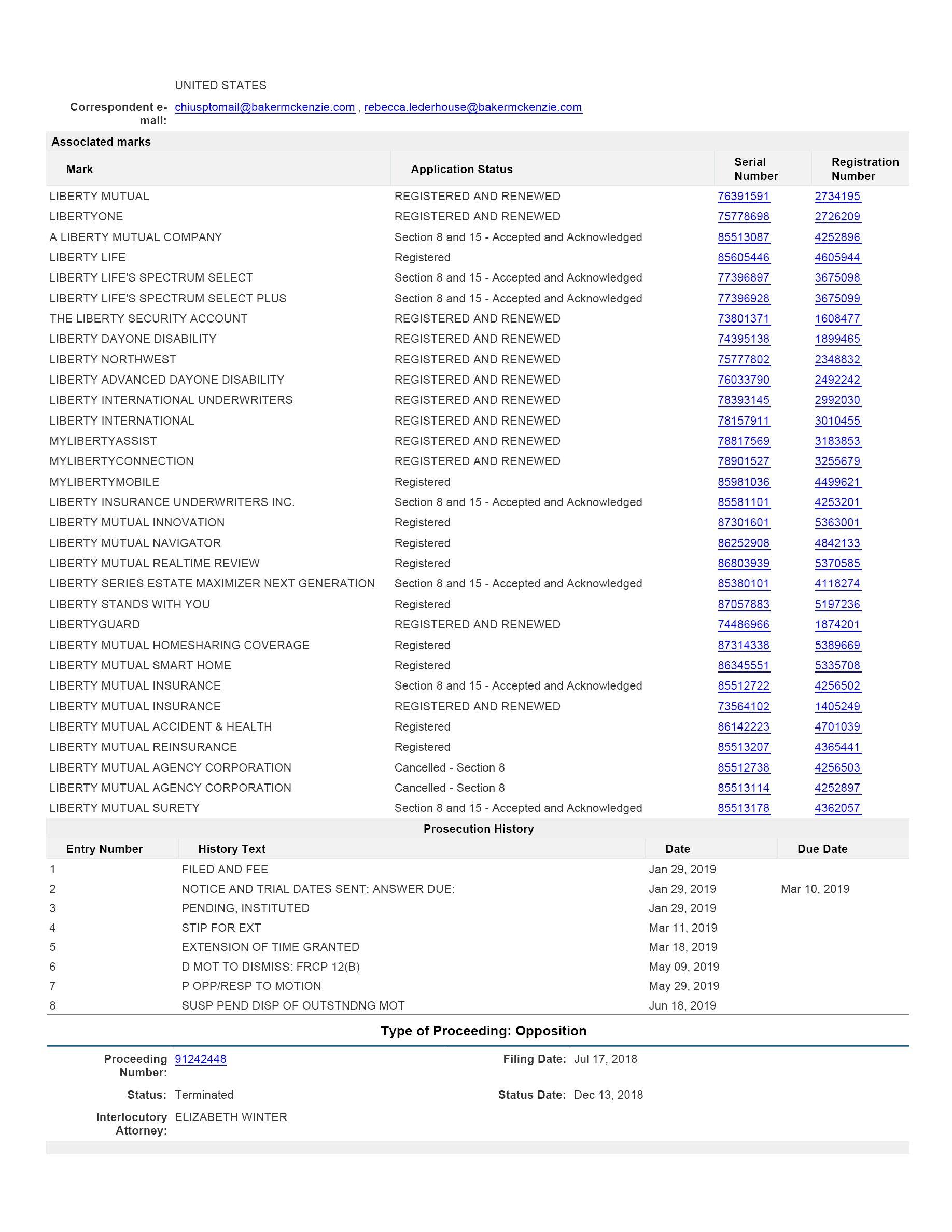

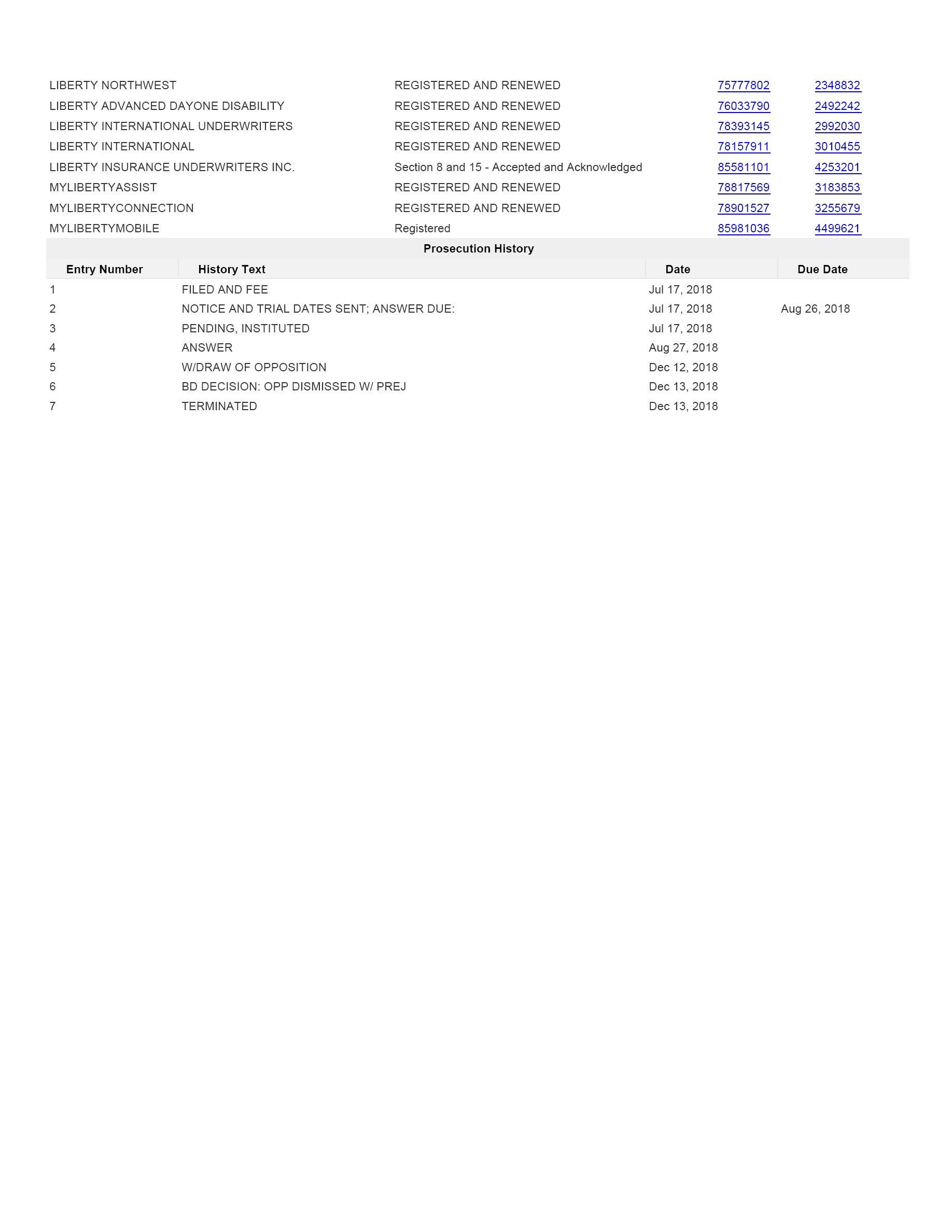

| SERIAL NUMBER | 88200741 |

| LAW OFFICE ASSIGNED | LAW OFFICE 109 |

| MARK SECTION | |

| MARK FILE NAME | http://uspto.report/TM/88200741/mark.png |

| LITERAL ELEMENT | YOURWEALTH REVIEW |

| STANDARD CHARACTERS | NO |

| USPTO-GENERATED IMAGE | NO |

| COLOR(S) CLAIMED (If applicable) |

Color is not claimed as a feature of the mark. |

| DESCRIPTION OF THE MARK (and Color Location, if applicable) |

The mark consists of the wording YOURWEALTH REVIEW positioned inside a shaded, elongated oval overlaid on a circular-shaped cross-hatch design. |

| ARGUMENT(S) | |

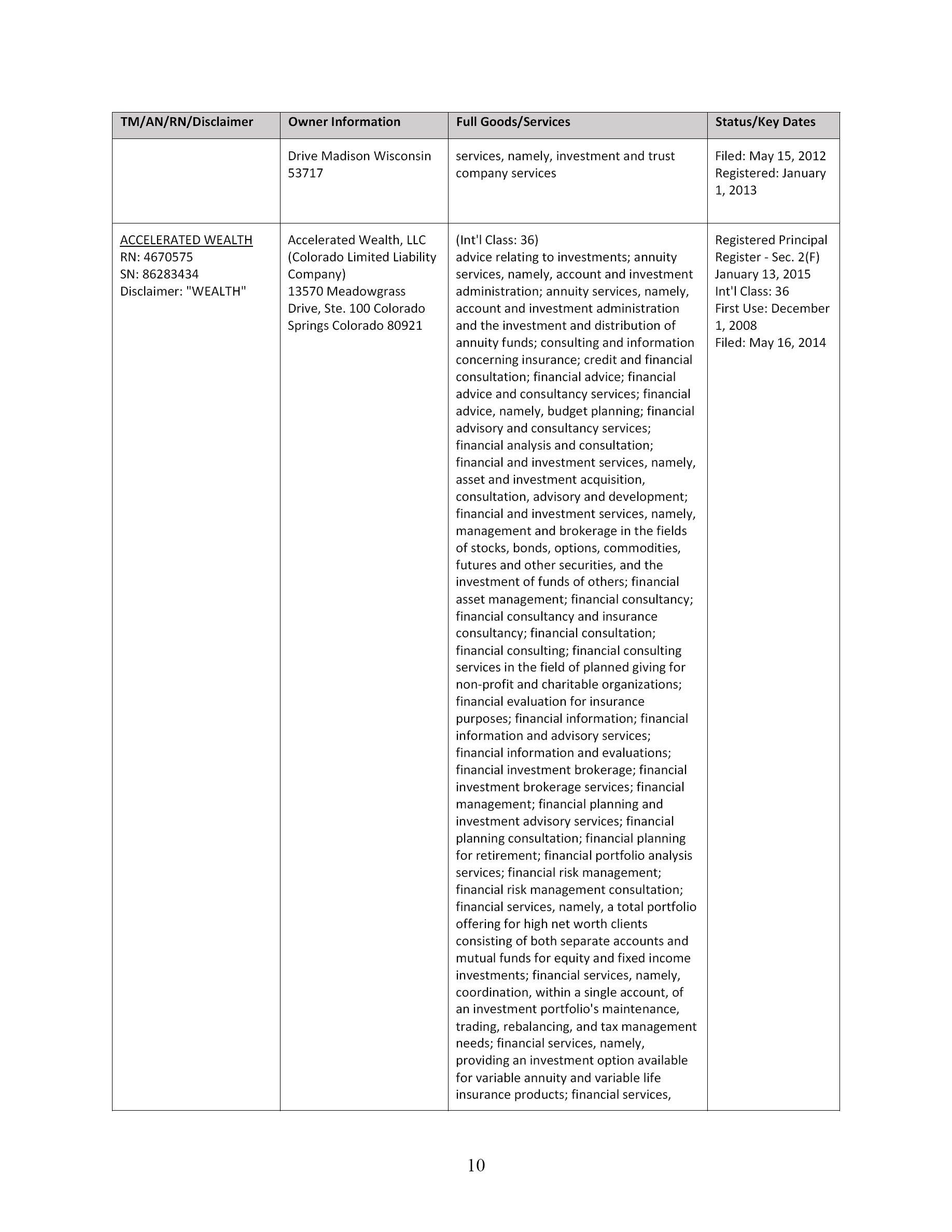

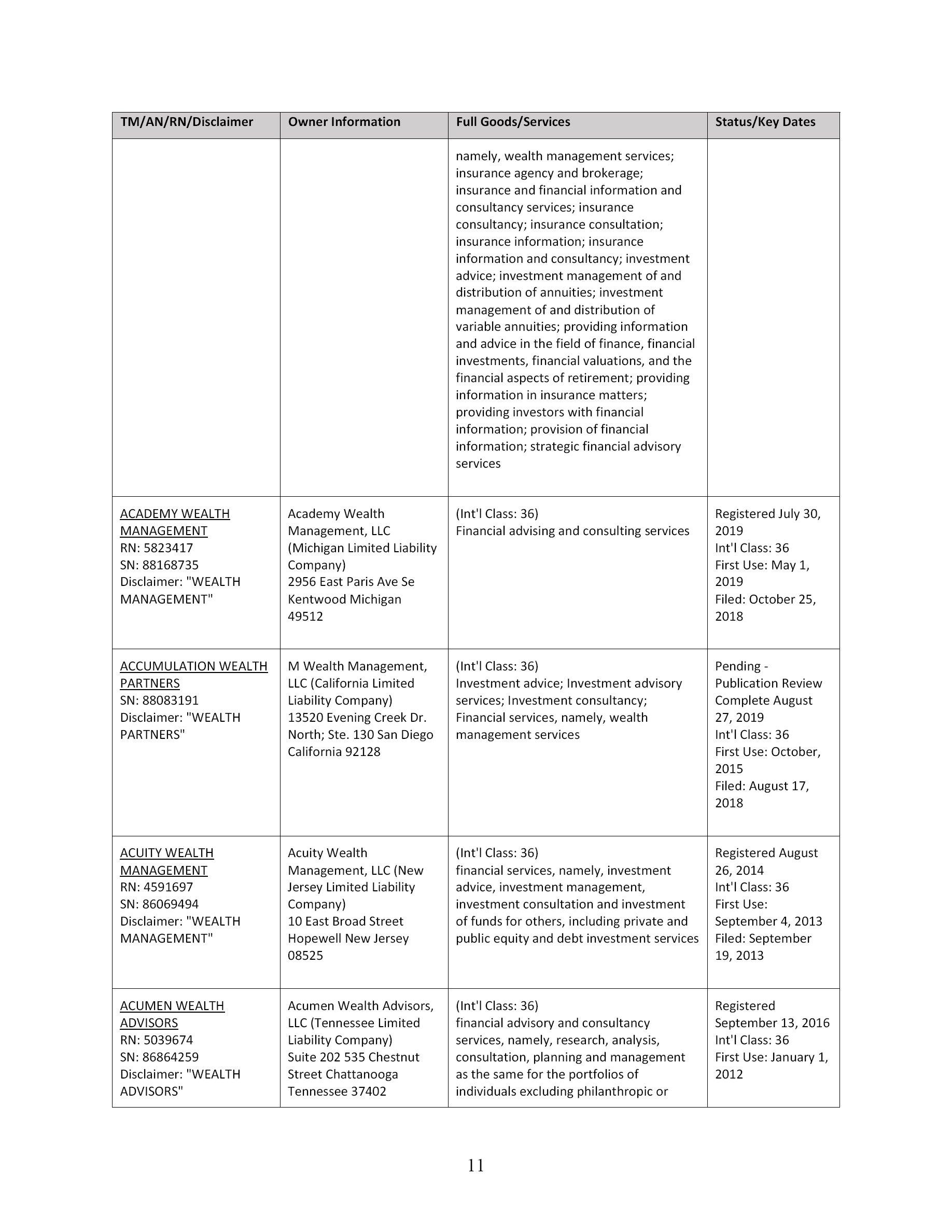

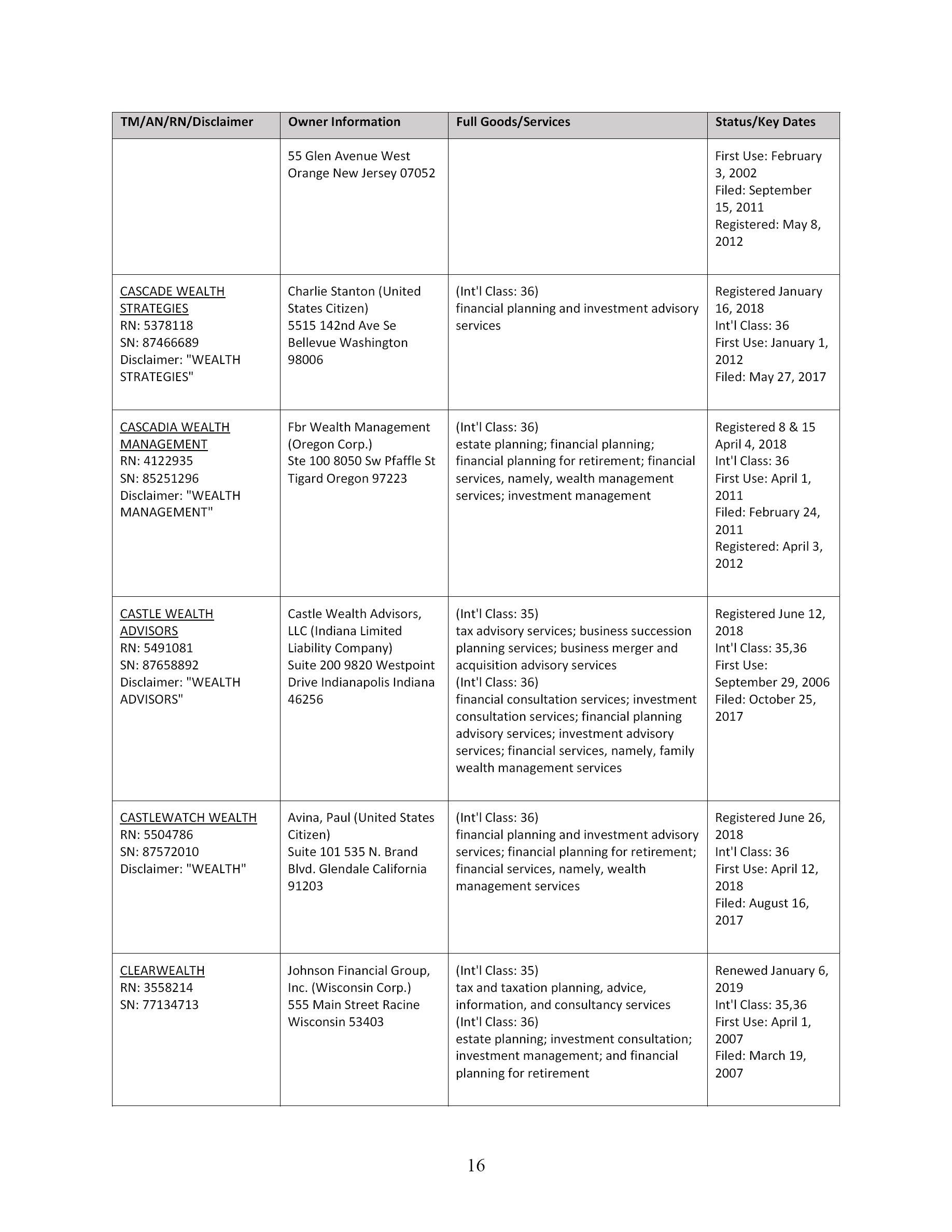

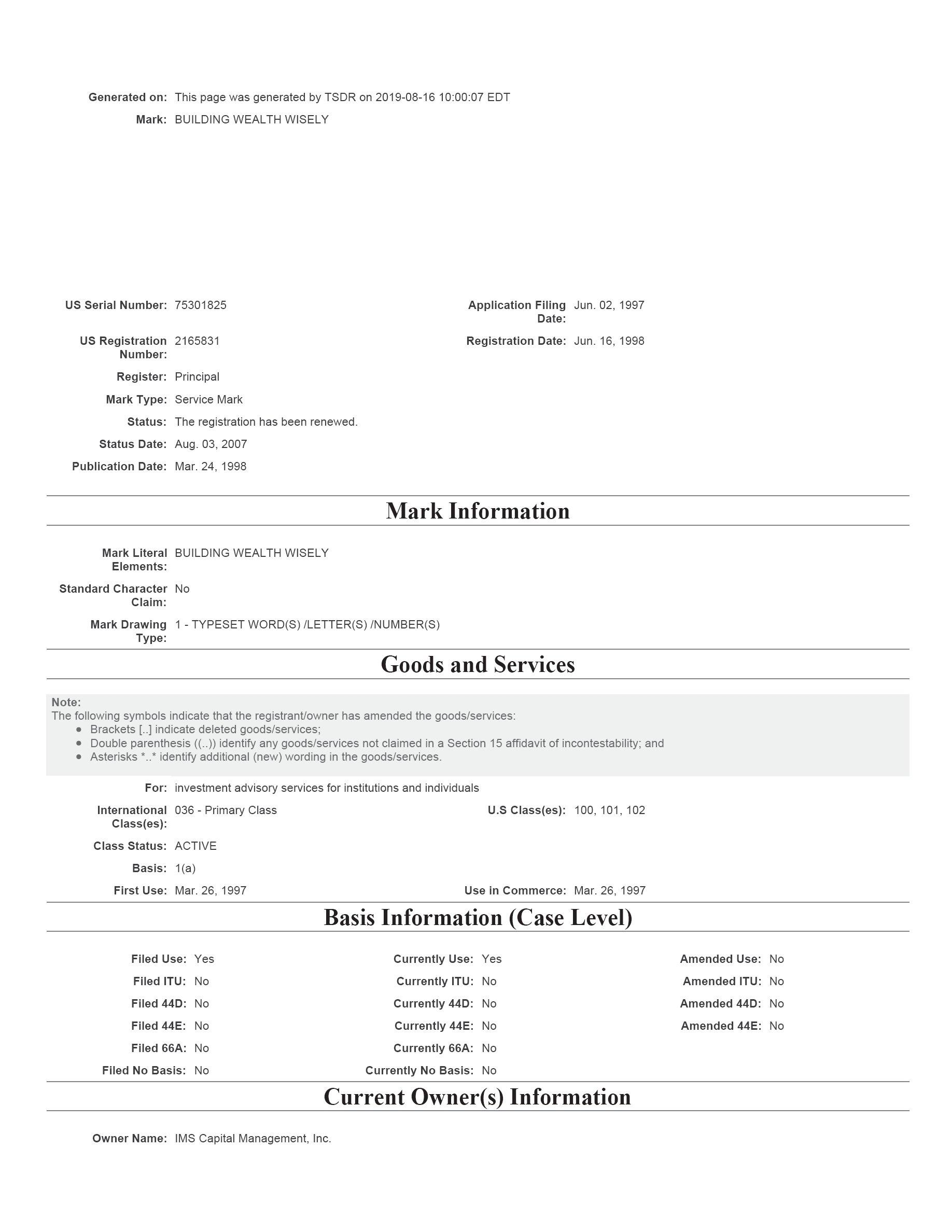

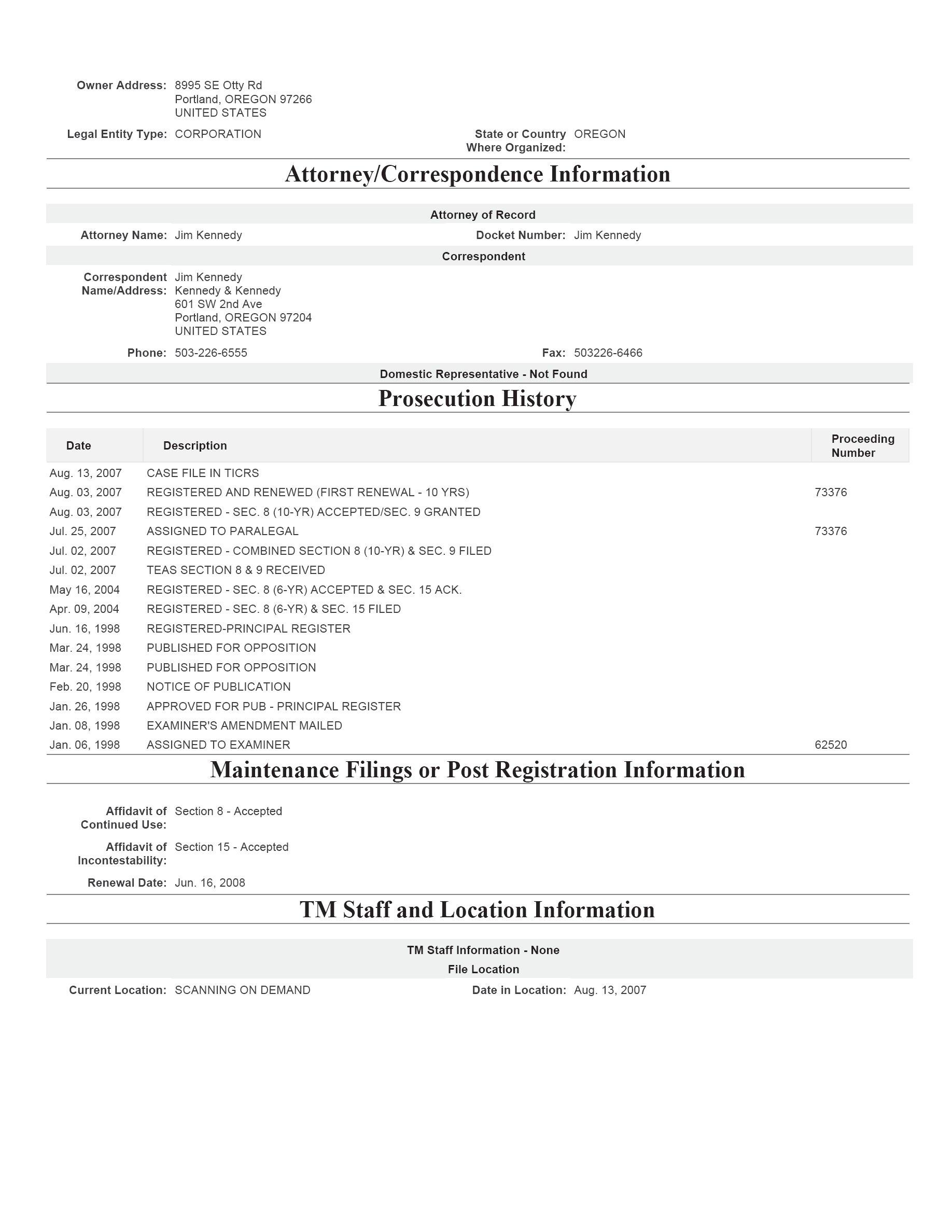

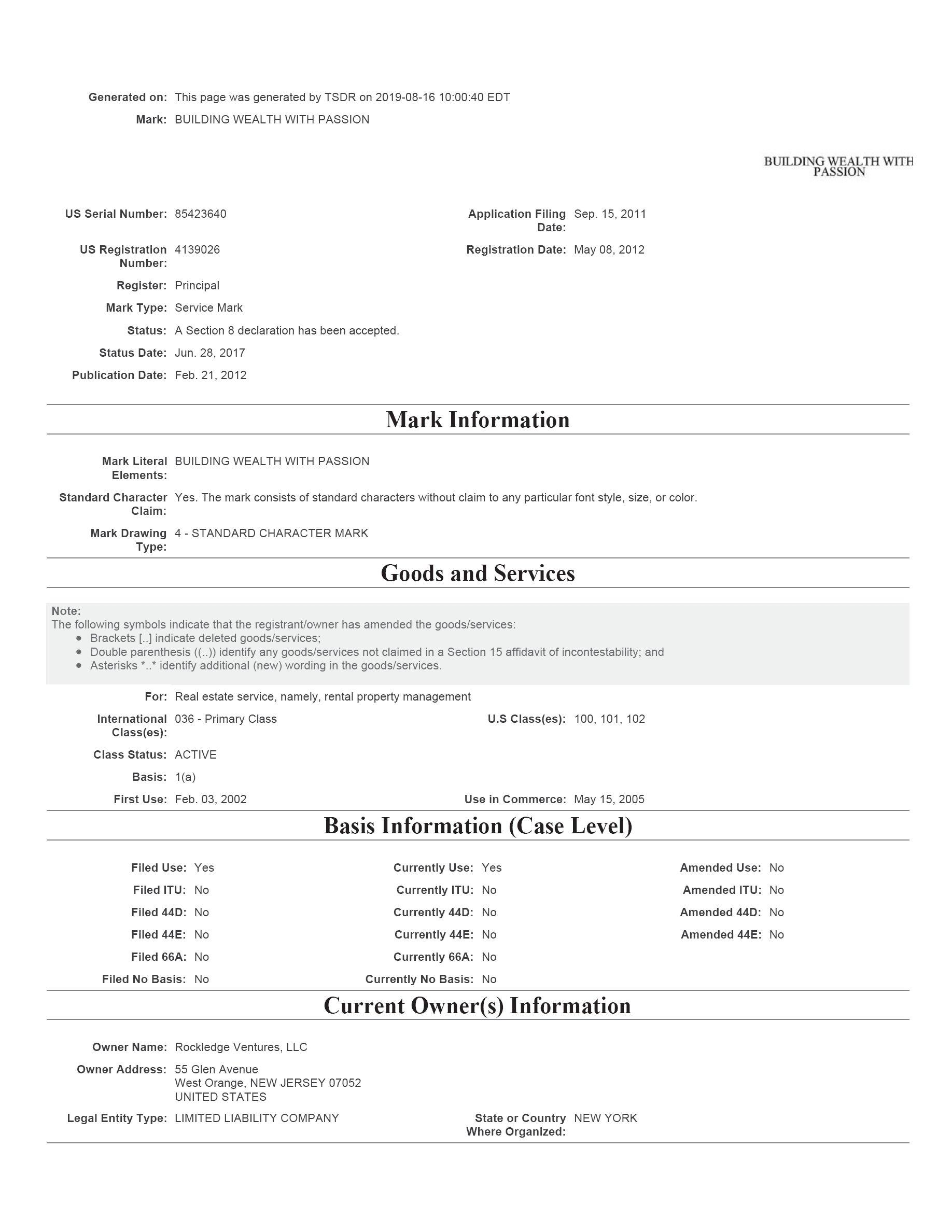

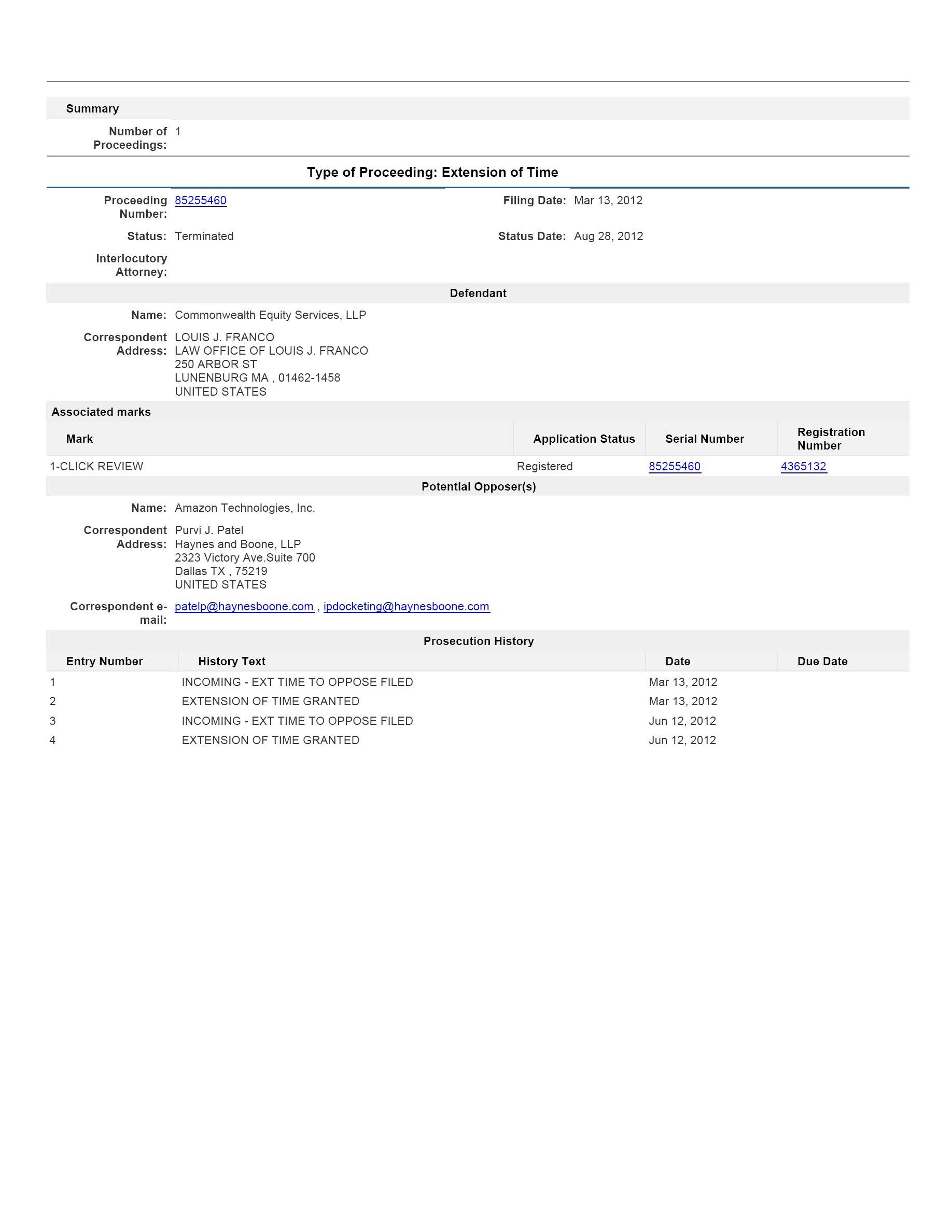

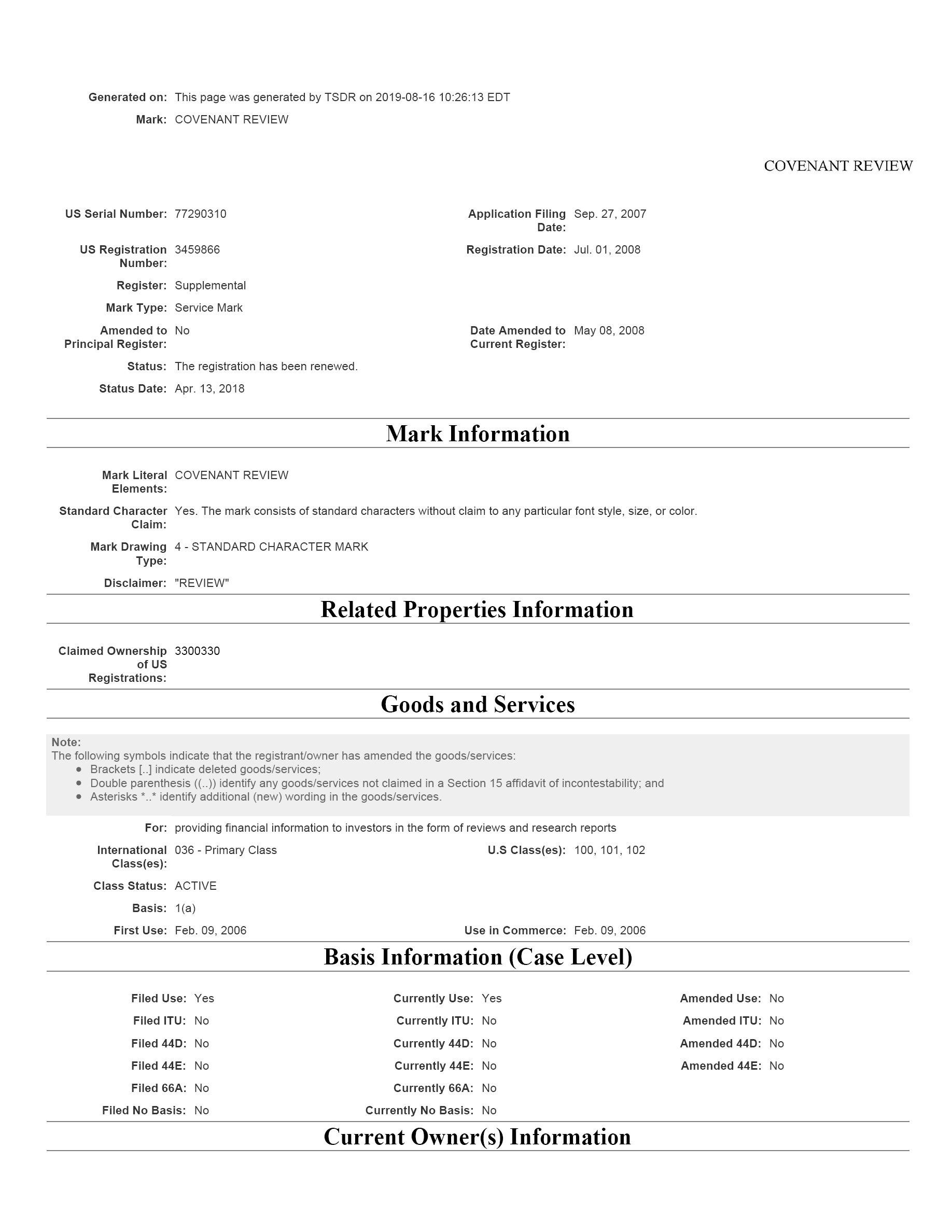

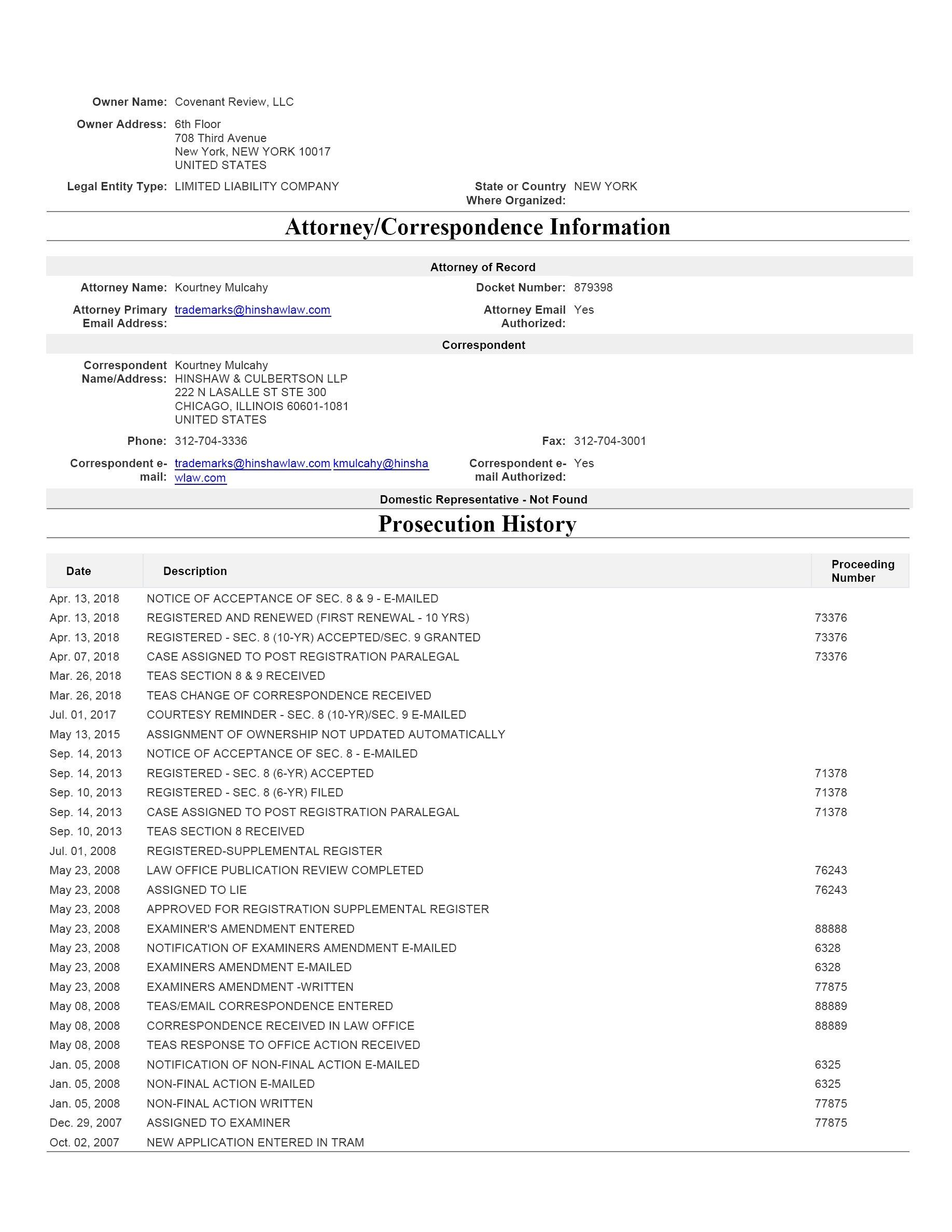

| ARGUMENT On 1 March 2019, the Examining Attorney refused registration of Serial No. 88/200741, YOURWEALTH REVIEW and design, on the grounds of a likelihood of confusion with Registration No. 2674776, THE WEALTH REVIEW. For the reasons set forth below, Applicant respectfully disagrees with the Examining Attorney and asserts that: (1) the design element is the dominant element of Applicant's mark and should be given due weight in the analysis; (2) the cited mark THE WEALTH REVIEW is entitled to only a narrow scope of protection, and Applicant's mark falls outside that scope of protection; and (3) Applicant's YOURWEALTH REVIEW is not similar to the cited THE WEALTH REVIEW mark. I. The design element is the dominant element of Applicant's mark and should be given due weight in the analysis. The Court of Appeals for the Federal Circuit has provided the following guidance with regard to determining and articulating likelihood of confusion: The basic principle in determining confusion between marks is that marks must be compared in their entireties . . . (citations omitted). It follows from that principle that likelihood of confusion cannot be predicated on dissection of a mark, that is, on only part of a mark (footnote omitted). On the other hand, in articulating reasons for reaching a conclusion on the issue of confusion, there is nothing improper in stating that, for rational reasons, more or less weight has been given to a particular feature of a mark, provided the ultimate conclusion rests on consideration of the marks in their entireties (footnote omitted). Indeed, this type of analysis appears to be unavoidable. In re National Data Corp., 753 F.2d 1056, 1058, 224 USPQ 749, 750-51 (Fed. Cir. 1985). It is especially important to consider composite marks, which contain a design element combined with words, in their entireties. See, TMEP Sec. 1207.01(c)(ii). That said, it is appropriate to accord greater importance to the more distinctive elements in the marks. In re Covalinski , 2014 TTAB LEXIS 353, *6, 113 U.S.P.Q.2D (BNA) 1166, 1168 (Trademark Trial & App. Bd. December 18, 2014). Although the word element is often accorded great weight, there is no general rule that the letter portion of the mark will form the dominant portion of the mark. In re Viterra Inc., 671 F.3d 1358, 1362 (Fed. Cir. 2012); In re Electrolyte Labs., Inc., 929 F.2d 645, 647 (Fed. Cir. 1990). Instead, the comparison of composite marks is done on a case-by-case basis, without reliance on mechanical rules of construction. See, e.g., In re Covalinski, 113 USPQ2d 1166 (TTAB 2014). A disclaimer is a concession that the disclaimed part of the mark is descriptive. In re DNI Holdings Ltd., 2005 TTAB LEXIS 515, *25, 77 U.S.P.Q.2D (BNA) 1435, 1442 (T.T.A.B. Dec. 6, 2005) ("[I]t has long been held that the disclaimer of a term constitutes an admission of the merely descriptive nature of that term, as applied to the goods or services in connection with which it is registered, and an acknowledgment of the lack of an exclusive right therein at the time of the disclaimer"). Accordingly, this admission justifies giving less weight to that element when determining likelihood of confusion. J. Thomas McCarthy, McCarthy on Trademarks and Unfair Competition, Sec. 19:65 p. 19-242 (5th ed. 2018). The Examining Attorney failed to consider the dominance of the design element of the Applicant's mark. Applicant respectfully asserts that the likelihood of confusion analysis should not be limited to only the literal portions of the mark. In re National Data Corp., 753 F.2d 1056, 1058, 224 USPQ 749, 750-51 (Fed. Cir. 1985). Instead, the design element should be considered along with the literal elements. In some cases, the design element has been given greater weight than the literal elements. For example, in In re Covalinski, confusion was held to be unlikely between REDNECK RACEGIRL and the registered RACEGIRL due to the design element accompanying "REDNECK RACEGIRL." 2014 TTAB LEXIS 353, 113 U.S.P.Q.2D (BNA) 1166 (TTAB December 18, 2014). Similarly, in Steve's Ice Cream, Inc. v. Steve's Famous Hot Dogs the applicant's design element evidenced differences in the two marks, which in turn supported a lack of likelihood of confusion. 1987 TTAB LEXIS 53, *7, 3 U.S.P.Q.2D (BNA) 1477, 1479 (Trademark Trial & App. Bd. June 23, 1987). The holdings in In re Covalinski and Steve's Ice Cream are significant because, like the present case, lack of confusion was found even though the registered marks were in standard character form while the applicants' marks were composite marks. 2014 TTAB LEXIS 353, 113 U.S.P.Q.2D (BNA) 1166 (TTAB December 18, 2014); 1987 TTAB LEXIS 53, *7, 3 U.S.P.Q.2D (BNA) 1477, 1479 (Trademark Trial & App. Bd. June 23, 1987). Additionally, the design element should be given greater weight because it will not be disclaimed. In other words, once the disclaimer is entered, Applicant will have conceded that the literal elements of its mark are descriptive. This admission justifies giving greater weight to the design element, which will not be disclaimed. In cases where all the literal elements of the mark are descriptive, the design element is considered the dominant element. For instance, in Outdoor Kids, the design element was afforded great weight. Outdoor Kids, Inc. v. Parris Mfg. Co., 385 F. App'x 992 (Fed. Cir. 2010) (holding no likelihood of confusion between OUTDOOR KIDS AND KID'S OUTDOORS). There, the Federal Circuit Court of Appeals upheld the Board's reasoning that "when the words at issue are highly descriptive or suggestive, or common in the trade, the presence of a design may be a more significant factor." Id. At 995. Like Outdoor Kids, the literal elements of Applicant's mark are considered descriptive. Moreover, the cited mark disclaimed "WEALTH" from its mark. Both marks, like the marks in Outdoor Kids, are therefore descriptive of the services, and the design element in the Applicant's mark should be considered the dominant element. II. Cited mark THE WEALTH REVIEW has a narrow scope of protection and Applicant?s mark falls outside that scope of protection If the common element of two marks is "weak" in that it is generic, descriptive, or highly suggestive of the named goods or services, it is unlikely that consumers will be confused unless the overall combinations have other commonality. See, e.g., In re Bed & Breakfast Registry, 791 F.2d 157, 229 USPQ 818 (Fed. Cir. 1986) (BED & BREAKFAST REGISTRY for making lodging reservations for others in private homes held not likely to be confused with BED & BREAKFAST INTERNATIONAL for room booking agency services). See also, TMEP Sec. 1207.01(b)(viii). Therefore, marks that are descriptive or highly suggestive are entitled to a narrower scope of protection than arbitrary or fanciful marks. Juice Generation, Inc. v. GS Enters. LLC, 794 F.3d 1334, 1339 (Fed. Cir. 2015). By extension, the "weaker an opposer's mark, the closer an applicant's mark can come without causing a likelihood of confusion and thereby invading what amounts to its comparatively narrower range of protection." Id. at 1338. Third-party registrations may be relevant to show that the mark or a portion of the mark is descriptive, suggestive, or so commonly used that the public will look to other elements to distinguish the source of the goods or services. See, e.g., AMF Inc. v. American Leisure Products, Inc., 474 F.2d 1403, 1406, 177 USPQ 268, 269-70 (C.C.P.A. 1973); Plus Products v. Star-Kist Foods, Inc., 220 USPQ 541, 544 (TTAB 1983). In those instances, marks containing similar elements may coexist on the Principal Register because the remaining poritons of the various marks are sufficient to distinguish between the marks. In re Hamilton Bank, 1984 TTAB LEXIS 163, *6, 222 U.S.P.Q. (BNA) 174, 178 (TTAB Mar. 6, 1984). Evidence of third-party use falls under the sixth du Pont factor-- the "number and nature of similar marks in use on similar goods." In re E. I. du Pont de Nemours & Co., 476 F.2d 1357, 1361, 177 USPQ 563, 567 (C.C.P.A. 1973). If the evidence establishes that the consuming public is exposed to third-party use of similar marks on similar goods, this evidence "is relevant to show that a mark is relatively weak and entitled to only a narrow scope of protection." Palm Bay Imports, Inc. v. Veuve Clicquot Ponsardin Maison Fondee en 1772, 396 F.3d 1369, 1373, 73 USPQ2d 1689, 1693 (Fed. Cir. 2005). Indeed, dilution on the Principal Register has been found with few instances. For example, in In re Hamilton Bank, the Board found that twenty registered marks illustrated that the term "KEY" had been widely adopted in the financial field due to its suggestive nature. 1984 TTAB LEXIS 163, *5, 222 U.S.P.Q. (BNA) 174, 178 (Trademark Trial & App. Bd. March 6, 1984). Thus, the inclusion of the term "KEY" was held to be an improper basis to find a likelihood of confusion. Id. Applicant has applied to register YOURWEALTH REVIEW and design for "financial services, namely, wealth management services" in Class 36. The Examining Attorney has cited THE WEALTH REVIEW for "Financial planning and investment consulting services; Insurance brokerage services and estate planning services for individuals" in Class 36 owned by The Company Coach. Within the shared Class 36, Applicant asserts that "WEALTH" and "REVIEW" are weak elements in the financial services industry. First, this is evidenced by the disclaimers required of both the cited mark and the Applicant's mark. As stated above, the cited mark disclaimed "WEALTH," and the Applicant will herein disclaim "YOUR WEALTH REVIEW." Second, the third party registrations listed below for WEALTH-formative and REVIEW-formative marks in Class 36 demonstrate both elements are heavily diluted in the financial services industry. There are 2,338 WEALTH-formative marks and 117 REVIEW-formative marks coexisting on the Principal Register in Class 36. Contained in Exhibit A is a sample of the WEALTH-formative marks for financial services. Accompanying that exhibit is Exhibit C, which contains evidence of use of these marks, and Exhibit E, which contains the soft copies of these registrations from the TSDR, which are hereby made of record. Likewise, contained in Exhibit B are REVIEW-formative marks for financial services. This exhibit is also accompanied by Exhibit D, which contains evidence of use of these marks, and Exhibit F, which contains the soft copies of these registrations from the TSDR, which are hereby made of record. The coexistence of the marks cited in the attached exhibits demonstrate that the terms, "WEALTH" and "REVIEW" have little source-identifying significance as applied to financial services, generally, in Class 36; rather, the words and designs that accompany "WEALTH" and "REVIEW" are the elements that are crucial for differentiation purposes. For instance, BUILD YOUR WEALTH WITH US, BUILDING WEALTH WISELY, AND BUILDING WEALTH WITH PASSION all coexist on the Register even though they share "WEALTH" and "BUILD." Thus, Applicant asserts that the inclusion of "WEALTH" and "REVIEW" cannot by itself serve as a basis for likelihood of confusion between the Applicant?s mark and the cited mark. The dilution of both terms on the Principal Register also demonstrates the relative weakness of the WEALTH and REVIEW elements of the cited mark. As there are no other distinctive elements in the cited mark, Applicant asserts that the cited mark is weak and is entitled to a limited scope of protection. In other words, Applicant's mark may come closer to the cited mark without causing a likelihood of confusion than it might with a stronger mark. From that standpoint, the fact that Applicant's YOURWEALTH REVIEW is so different from the cited THE WEALTH REVIEW mark will make it extremely easy for consumers to perceive the differences between Applicant's mark and the cited mark. III. Applicant's YOURWEALTH REVIEW is not similar to the cited THE WEALTH REVIEW mark In In re E. I. du Pont de Nemours & Co., 476 F.2d 1357, 177 USPQ 563 (C.C.P.A. 1973), the Court of Customs and Patent Appeals discussed the factors relevant to a determination of likelihood of confusion. In ex parte examination, the issue of likelihood of confusion typically revolves around the similarity or dissimilarity of the marks and the relatedness of the goods or services. See, TMEP ? 1207.01. The other factors listed in du Pont may be considered only if relevant evidence is contained in the record. In this case, the following factors are the most relevant: - The similarity or dissimilarity of the marks in their entireties as to appearance, sound, connotation and commercial impression. - The number and nature of similar marks in use on similar goods. The points of comparison for a word mark are appearance, sound, meaning, and commercial impression. Palm Bay Imports, Inc. v. Veuve Clicquot Ponsardin Maison Fondee en 1772, 396 F.3d 1369, 73 USPQ2d 1689, 1691 (Fed. Cir. 2005), citing In re E. I. du Pont de Nemours & Co., 476 F.2d 1357, 1361, 177 USPQ 563, 567 (C.C.P.A. 1973). Similarity of the marks in one respect -- sight, sound, or meaning -- will not automatically result in a finding of likelihood of confusion even if the goods are identical or closely related. See also, TMEP Sec. 1207.01(b)(i). It is a general rule that likelihood of confusion is not avoided between otherwise confusingly similar marks merely by adding or deleting matter that is descriptive or suggestive of the named goods or services. Exceptions to this general rule may arise if: (1) the marks in their entireties convey significantly different commercial impressions; or (2) the matter common to the marks is not likely to be perceived by purchasers as distinguishing source because it is merely descriptive or diluted. See, e.g., Shen Mfg. Co. v. Ritz Hotel Ltd., 393 F.3d 1238, 73 USPQ2d 1350 (Fed. Cir. 2004) (RITZ and THE RITZ KIDS create different commercial impressions). Unitary marks create a commercial impression separate and apart from any unregisterable component. See, TMEP Sec. 1213.02, 1213.05. Such marks are unitary when the elements are so merged together that they cannot be regarded as separable elements. In re EBS Data Processing, Inc., 1981 TTAB LEXIS 110, *4, 212 U.S.P.Q. (BNA) 964, 966 (Trademark Trial & App. Bd. December 28, 1981). This may occur when two words are combined to make a compound word. Id. In other cases, the possessive form of a word may merge the wording so as to add to the commercial impression of a unitary phrase or slogan. See, TMEP Sec. 1213.05(b)(ii)(D). Although the possessive form does not, by itself, create unitariness, the combination of a possessive and another consideration may result in a unitary phrase. Id. Moreover, any aspect of a mark may be a consideration to create a unitary mark if the aspect creates a distinct meaning or commercial impression that is more than its constituent parts. See, TMEP Sec. 1213.05(b)(iii). Applicant's mark falls under both exceptions: (1) the marks in their entireties convey significantly different commercial impressions; and (2) the matter common to the marks is not likely to be perceived by purchasers as a distinguishing source because it is merely descriptive or diluted. Additionally, Applicant?s mark is not similar to the cited mark, THE WEALTH REVIEW, when compared against the literal elements and design elements of the Applicant's mark, YOURWEALTH REVIEW and design. Under the first du Pont factor, the points of comparison for a word mark are appearance, sound, meaning, and commercial impression. First, even without considering the design element, the literal elements of the Applicant mark look dissimilar to the cited mark. The leading literal element, "YOUR," is unique to Applicant's mark and is connected to "WEALTH" as a unitary element. This element is unitary because it is displayed as a compound word and functions similar to a possessive. Both aspects together are typically enough to find that an element is unitary and therefore carries a distinct commercial impression. As the leading element, this element would likely capture the most attention while reading the mark without altering the fact that the design component of Applicant's mark should be considered "dominant" as set forth in Parts I and II of Applicant's argument. Moreover, when the design element is given due weight in the analysis, it further distinguishes the appearance of the Applicant's mark. Second, the sound of the Applicant's mark is different because "YOURWEALTH" is pronounced as a single word with the emphasis on "YOUR." Third, including YOUR in the Applicant mark gives it a different meaning and commercial impression because it connotes individualized service. Additionally, YOURWEALTH is a unitary phrase and provides a distinct meaning. Here, it would be interpreted as a turnkey service as opposed to the general wealth management services that the cited mark connotes. CONCLUSION For the foregoing reasons, Applicant respectfully submits that Serial No. 88/200741, YOURWEALTH REVIEW & design, is now in condition for publication. Such favorable action is respectfully requested. | |

| EVIDENCE SECTION | |

| EVIDENCE FILE NAME(S) | |

| ORIGINAL PDF FILE | evi_207250694-20190816141959315391_._Exhibit_A.pdf |

| CONVERTED PDF FILE(S) (10 pages) |

\\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0002.JPG |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0003.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0004.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0005.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0006.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0007.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0008.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0009.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0010.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0011.JPG | |

| ORIGINAL PDF FILE | evi_207250694-20190816141959315391_._Exhibit_B.pdf |

| CONVERTED PDF FILE(S) (4 pages) |

\\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0012.JPG |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0013.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0014.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0015.JPG | |

| ORIGINAL PDF FILE | evi_207250694-20190816141959315391_._Exhibit_C.pdf |

| CONVERTED PDF FILE(S) (4 pages) |

\\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0016.JPG |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0017.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0018.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0019.JPG | |

| ORIGINAL PDF FILE | evi_207250694-20190816141959315391_._Exhibit_D.pdf |

| CONVERTED PDF FILE(S) (2 pages) |

\\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0020.JPG |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0021.JPG | |

| ORIGINAL PDF FILE | evi_207250694-20190816141959315391_._Exhibit_E.pdf |

| CONVERTED PDF FILE(S) (76 pages) |

\\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0022.JPG |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0023.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0024.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0025.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0026.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0027.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0028.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0029.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0030.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0031.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0032.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0033.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0034.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0035.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0036.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0037.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0038.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0039.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0040.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0041.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0042.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0043.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0044.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0045.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0046.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0047.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0048.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0049.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0050.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0051.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0052.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0053.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0054.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0055.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0056.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0057.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0058.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0059.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0060.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0061.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0062.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0063.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0064.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0065.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0066.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0067.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0068.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0069.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0070.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0071.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0072.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0073.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0074.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0075.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0076.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0077.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0078.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0079.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0080.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0081.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0082.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0083.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0084.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0085.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0086.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0087.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0088.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0089.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0090.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0091.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0092.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0093.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0094.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0095.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0096.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0097.JPG | |

| ORIGINAL PDF FILE | evi_207250694-20190816141959315391_._Exhibit_F.pdf |

| CONVERTED PDF FILE(S) (36 pages) |

\\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0098.JPG |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0099.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0100.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0101.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0102.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0103.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0104.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0105.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0106.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0107.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0108.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0109.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0110.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0111.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0112.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0113.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0114.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0115.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0116.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0117.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0118.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0119.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0120.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0121.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0122.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0123.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0124.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0125.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0126.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0127.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0128.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0129.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0130.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0131.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0132.JPG | |

| \\TICRS\EXPORT17\IMAGEOUT17\882\007\88200741\xml7\ROA0133.JPG | |

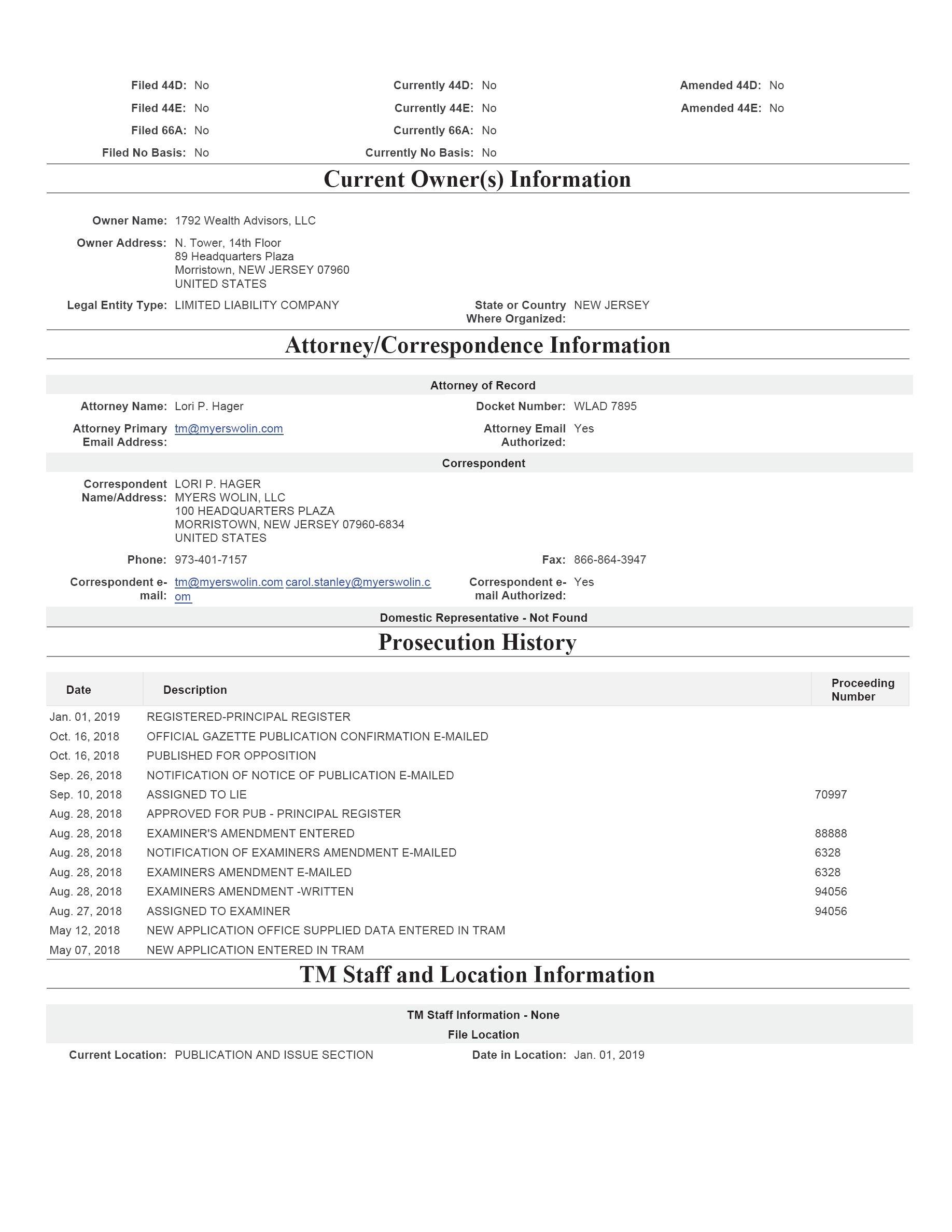

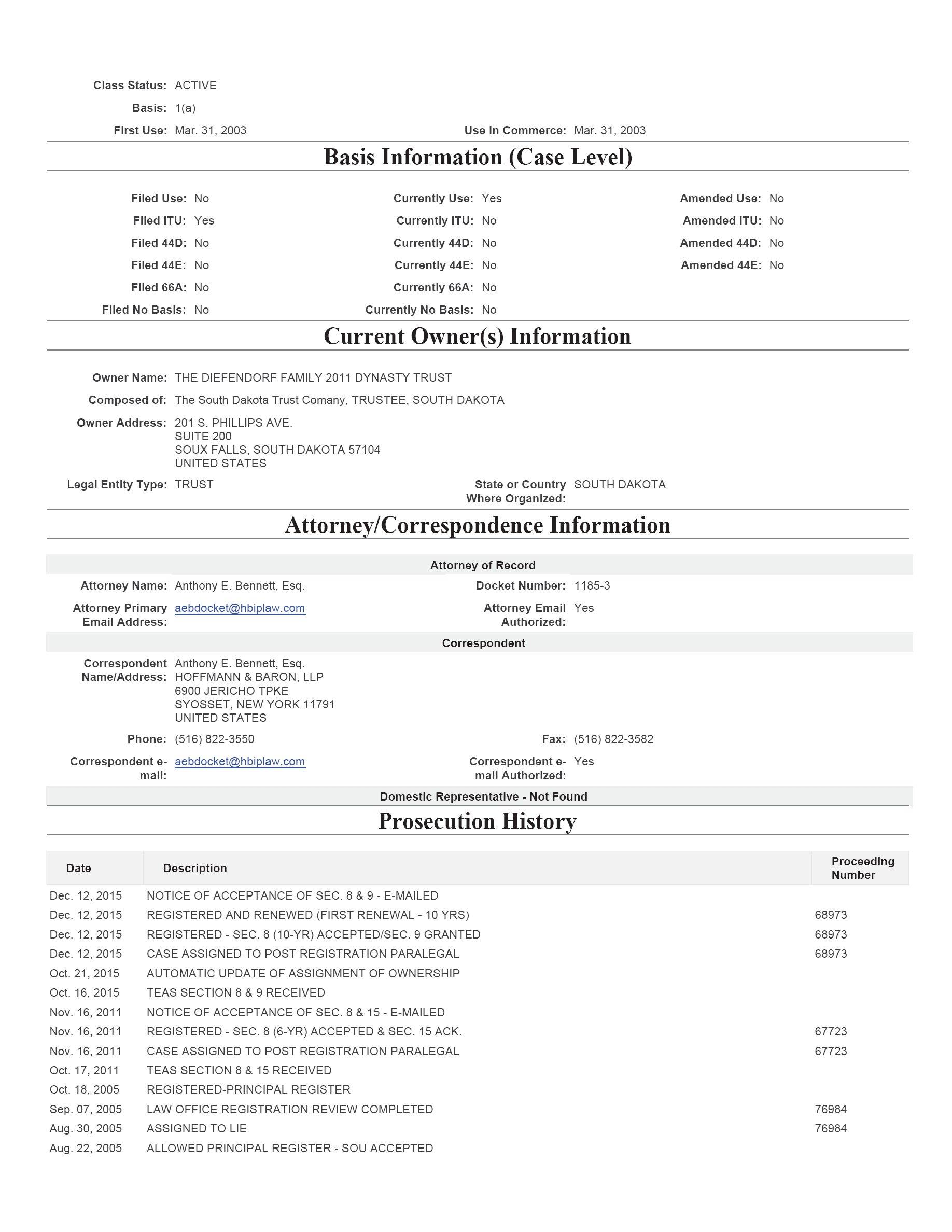

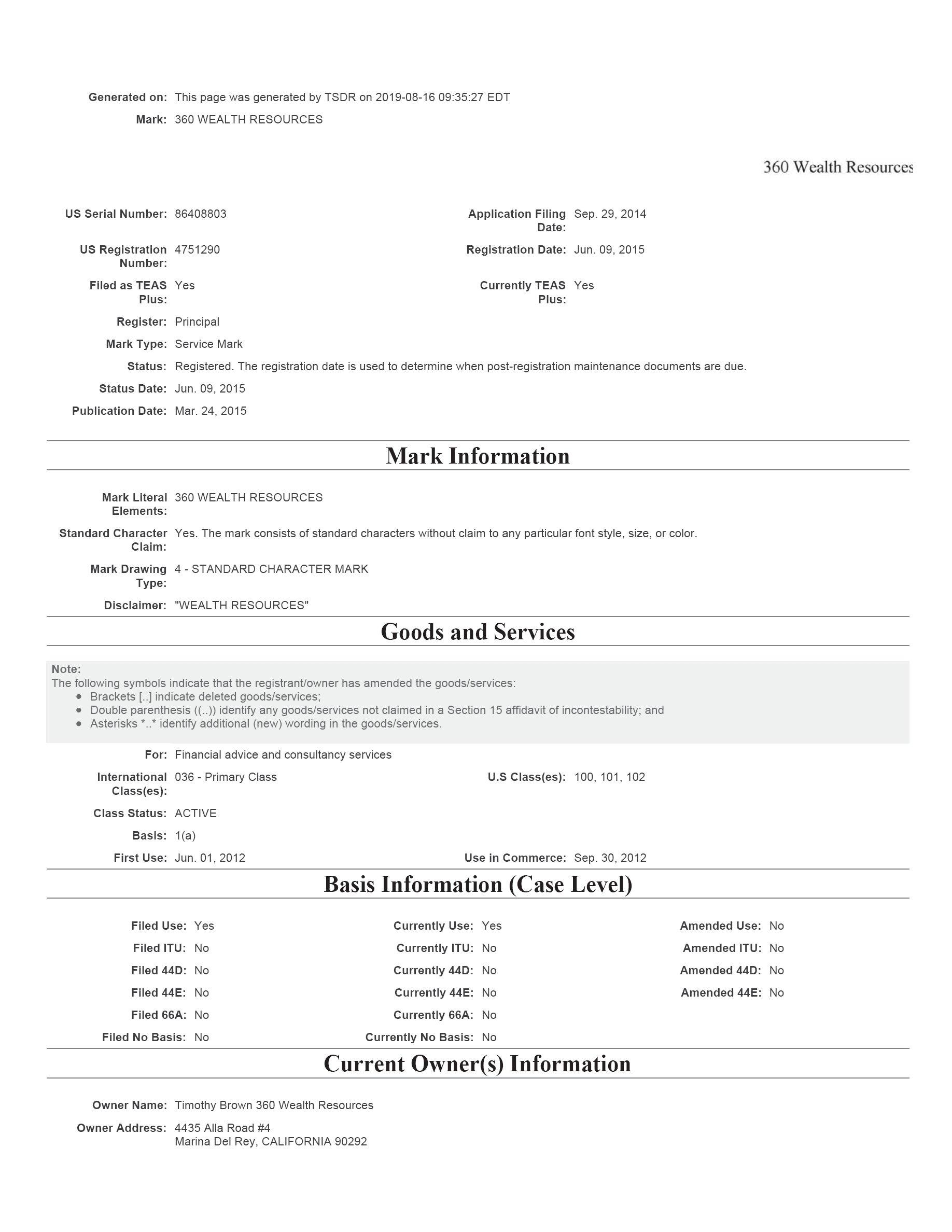

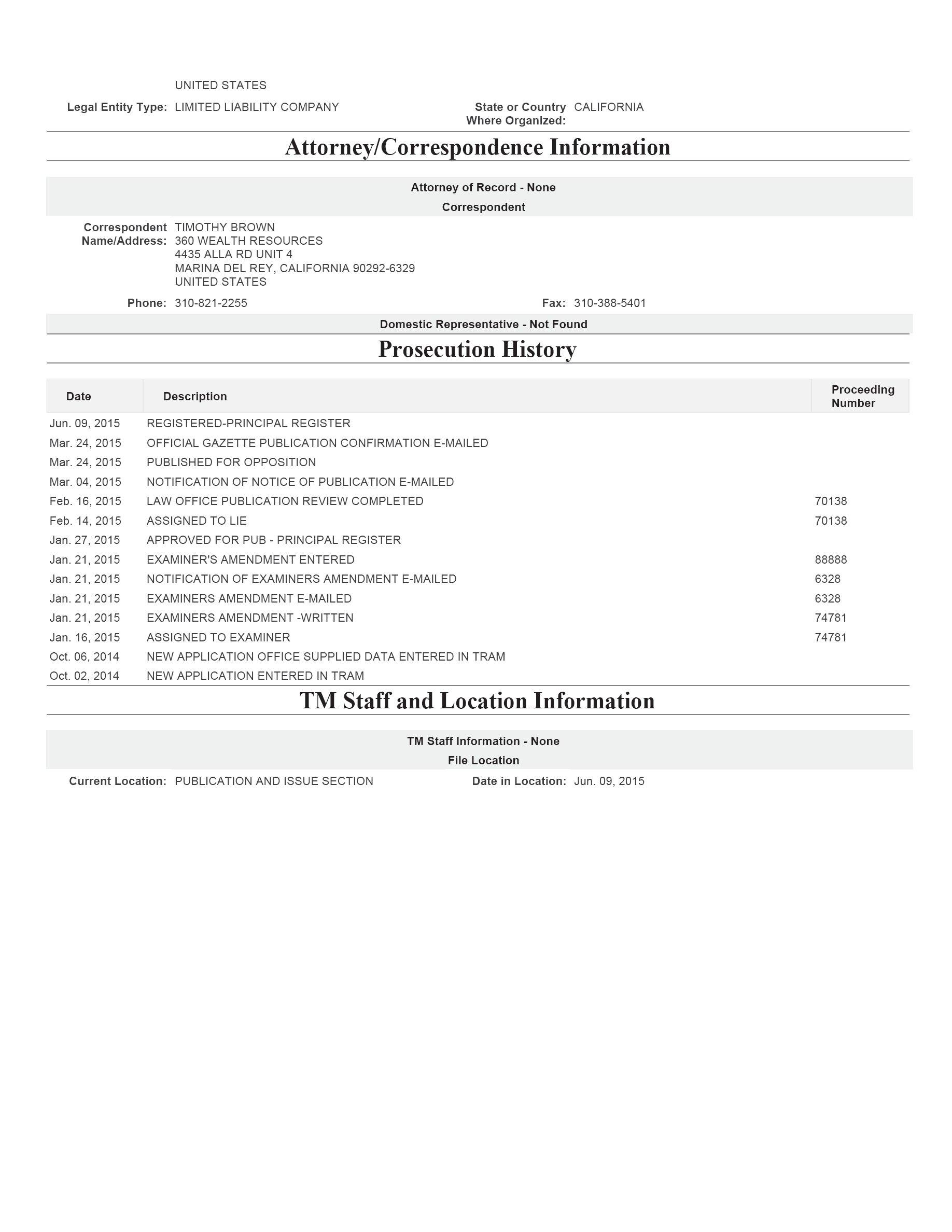

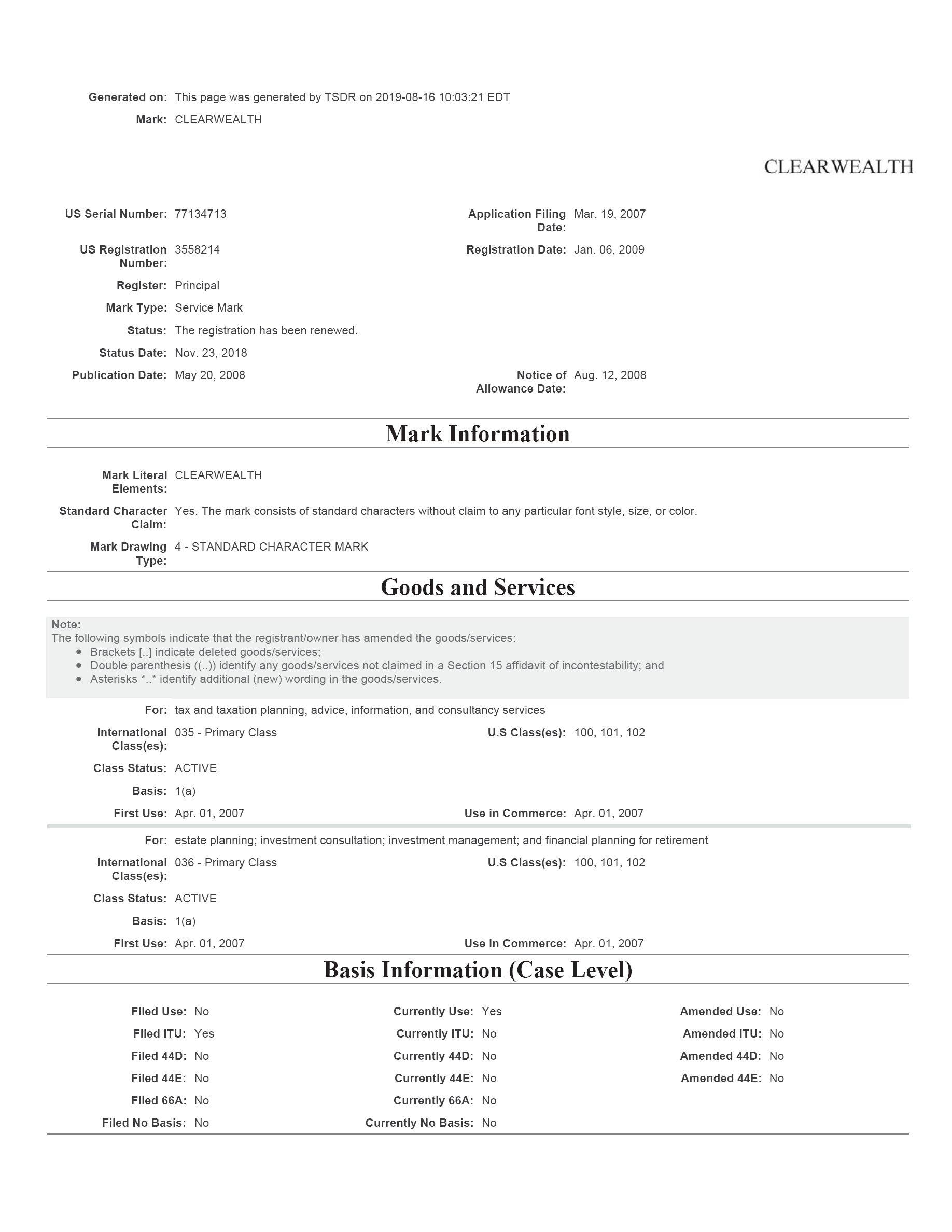

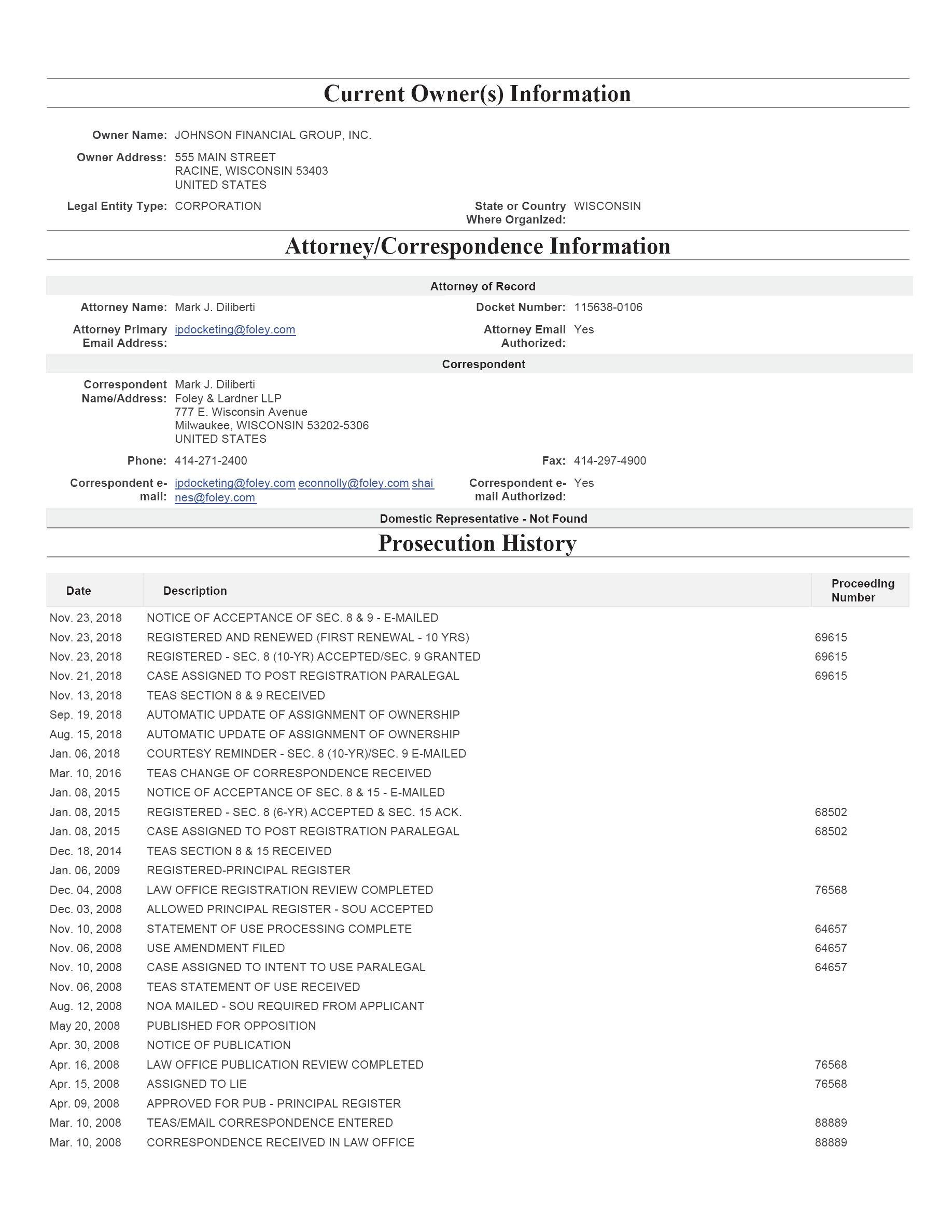

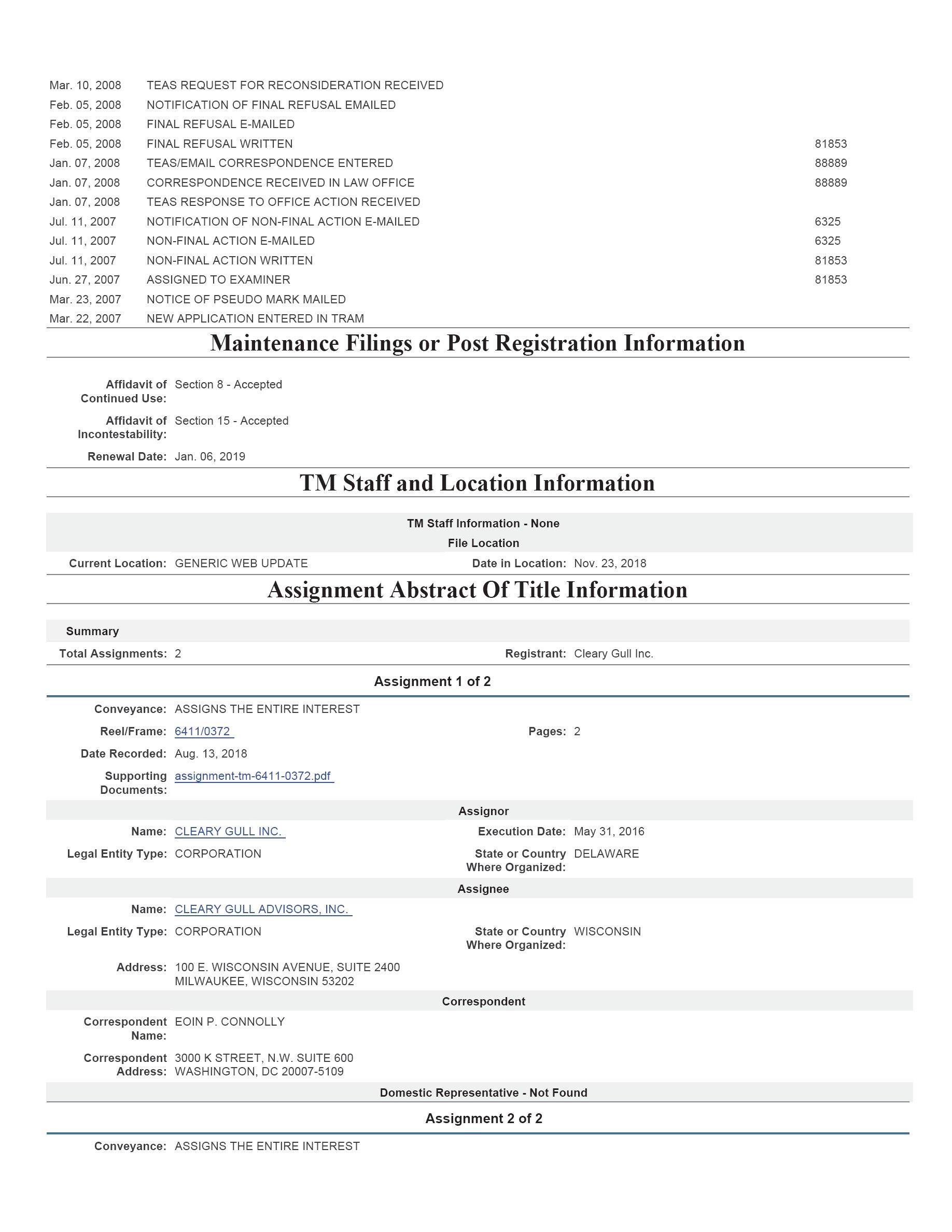

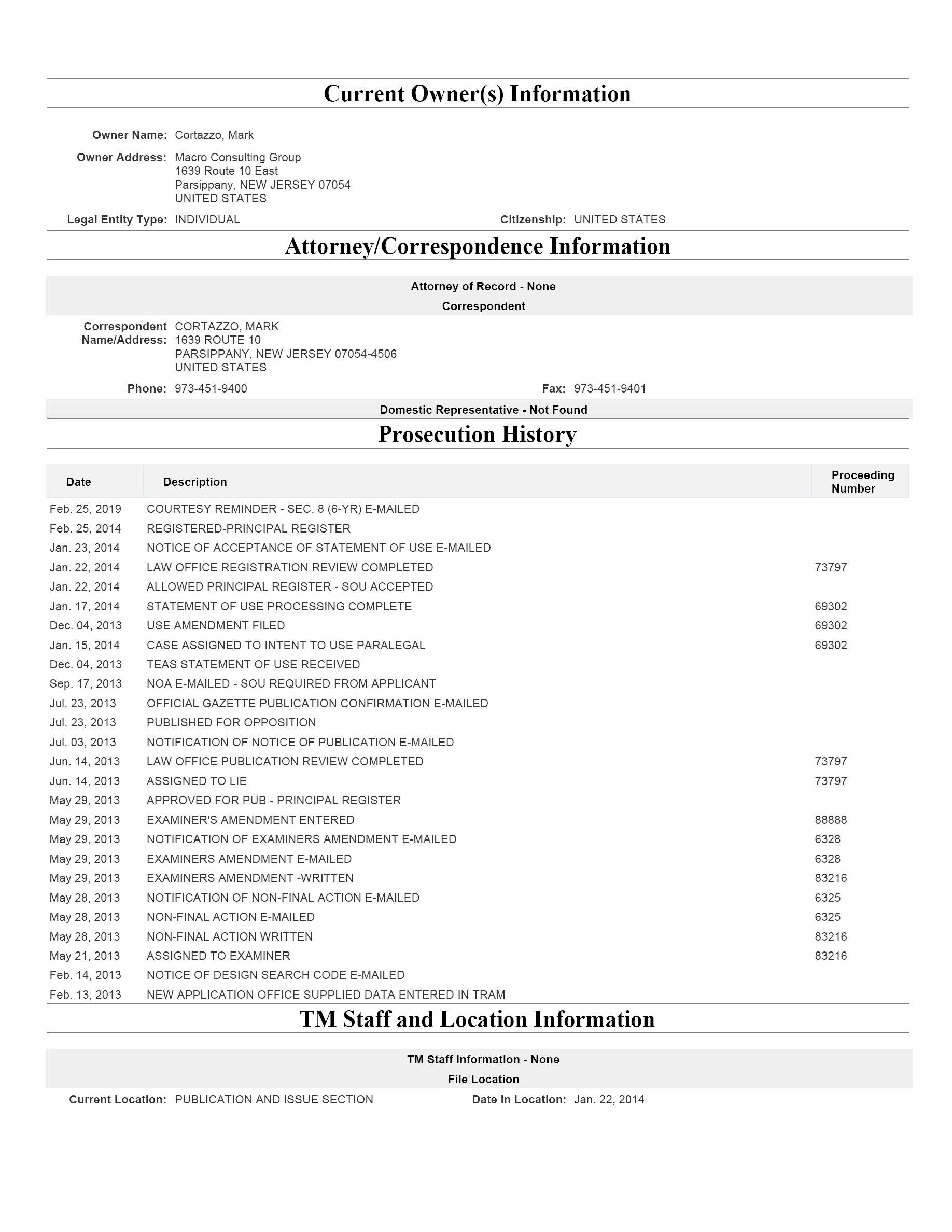

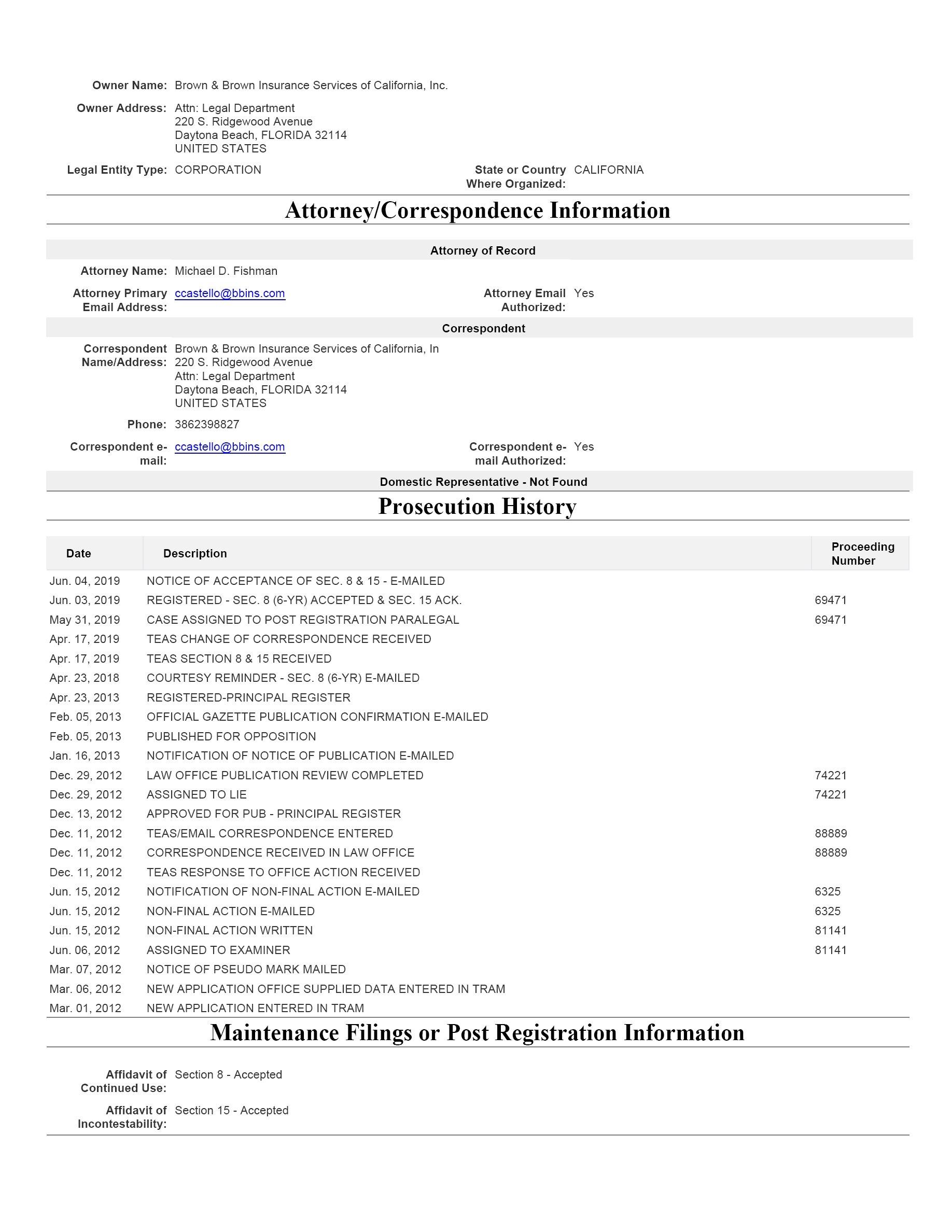

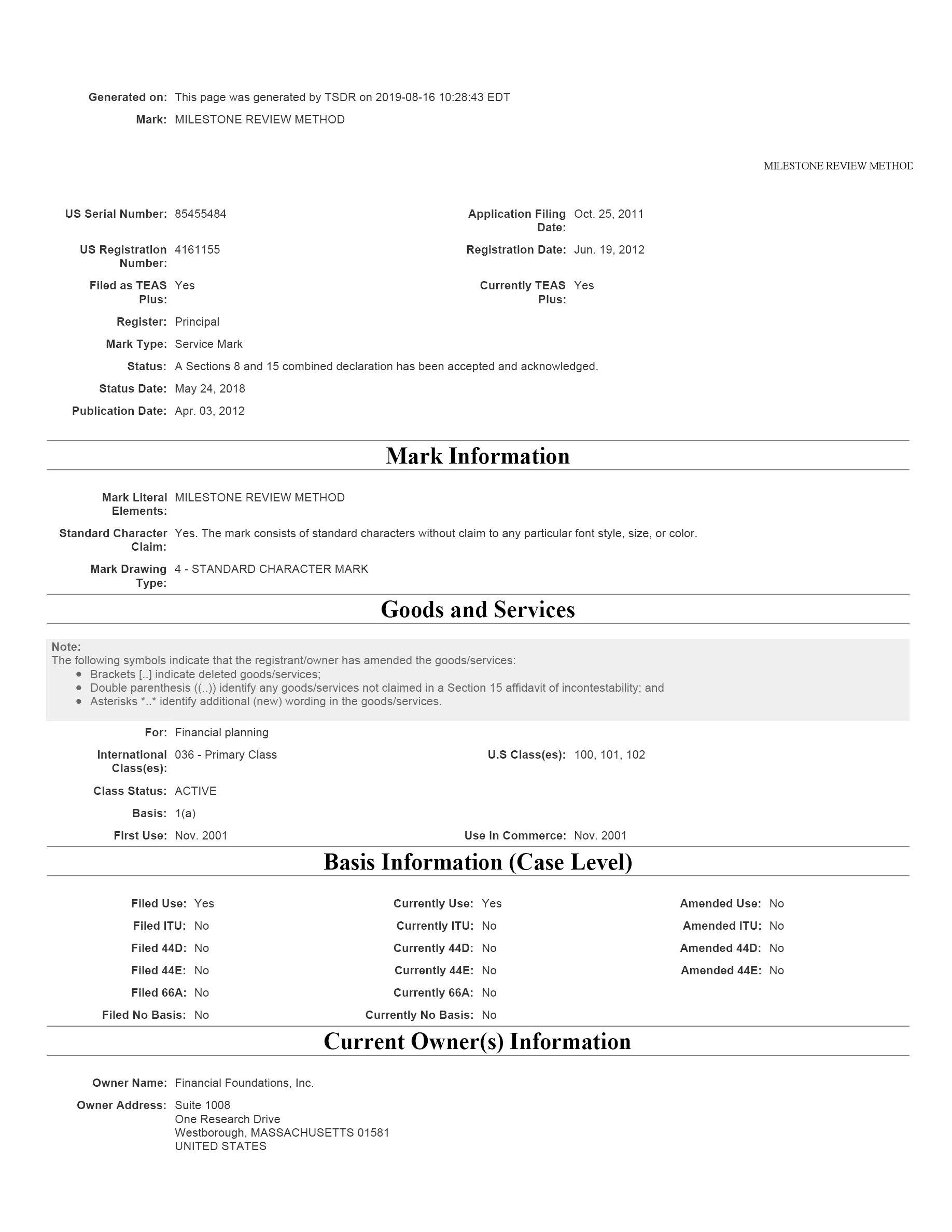

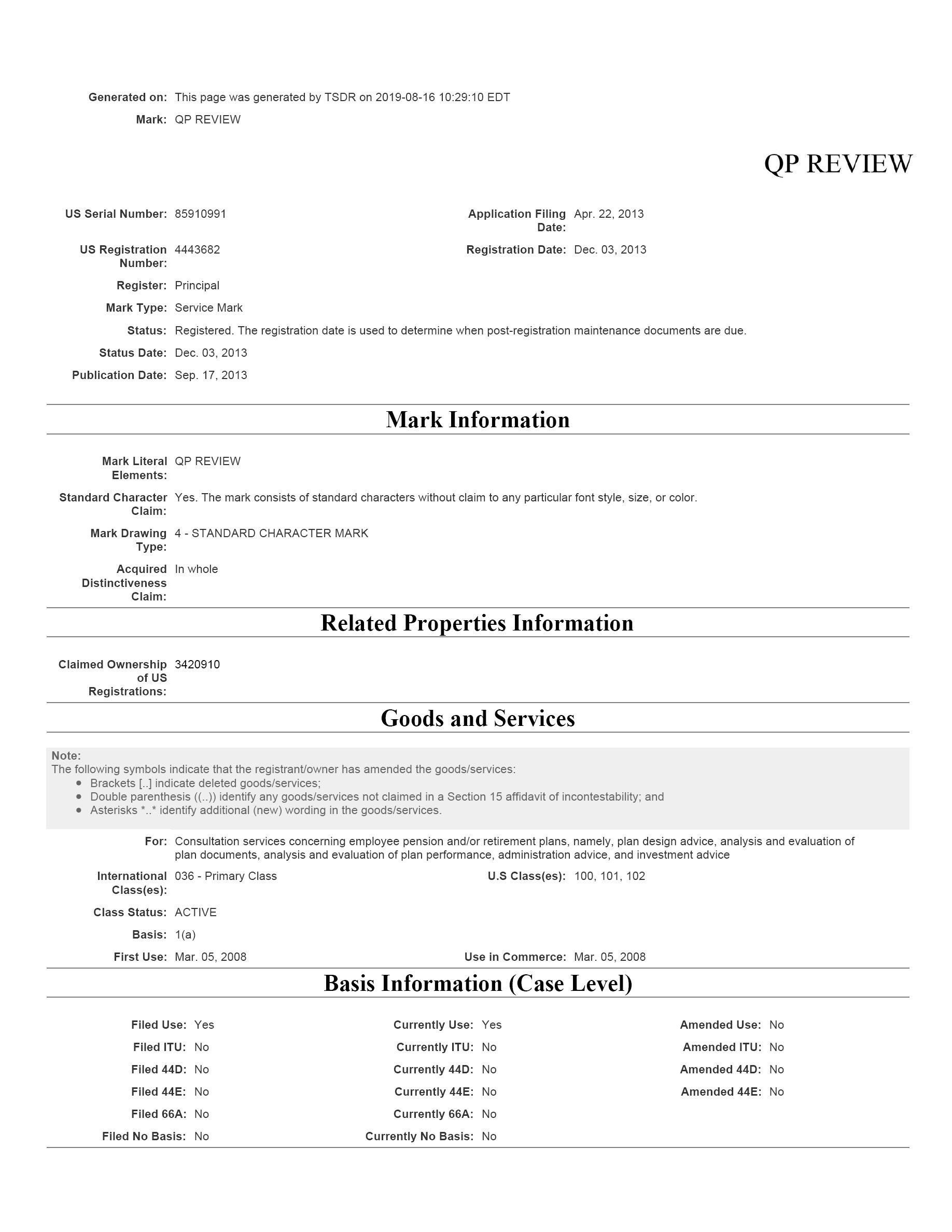

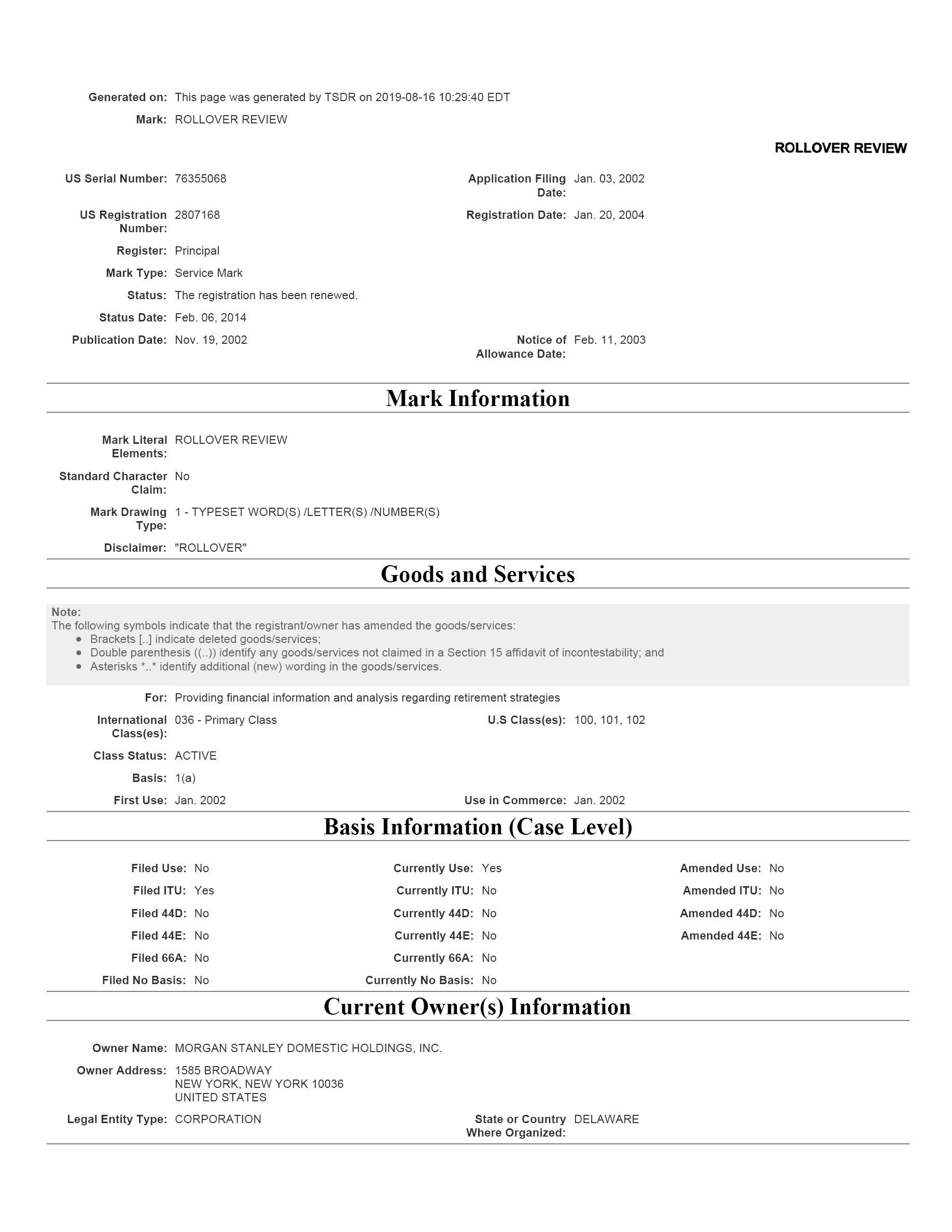

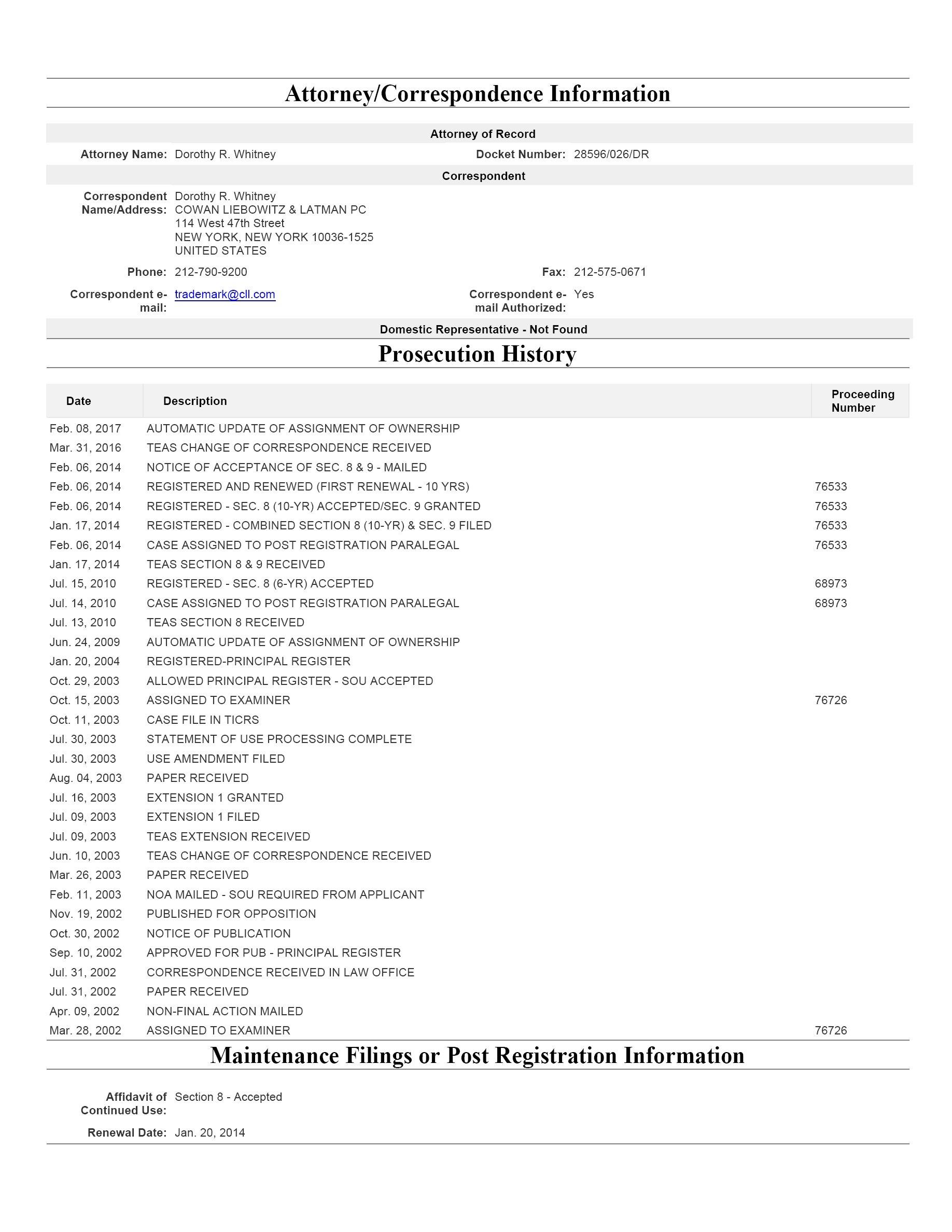

| DESCRIPTION OF EVIDENCE FILE | Exhibit A: WEALTH-Formative Mark Registrations Exhibit B: REVIEW-Formative Mark Registrations Exhibit C: Evidence of WEALTH-Formative Marks in Use Exhibit D: Evidence of REVIEW-Formative Marks In Use Exhibit E: WEALTH-Formative Mark TSDR Status Exhibit F: REVIEW-Formative Mark TSDR Status |

| ADDITIONAL STATEMENTS SECTION | |

| DISCLAIMER | No claim is made to the exclusive right to use YOUR WEALTH REVIEW apart from the mark as shown. |

| ATTORNEY SECTION (current) | |

| NAME | J. Michael Hurst |

| ATTORNEY BAR MEMBERSHIP NUMBER | NOT SPECIFIED |

| YEAR OF ADMISSION | NOT SPECIFIED |

| U.S. STATE/ COMMONWEALTH/ TERRITORY | NOT SPECIFIED |

| FIRM NAME | KEATING MUETHING & KLEKAMP PLL |

| STREET | ONE EAST FOURTH STREET, SUITE 1400 |

| CITY | CINCINNATI |

| STATE | Ohio |

| POSTAL CODE | 45202 |

| COUNTRY | US |

| PHONE | 513-562-1401 |

| FAX | 513-579-6547 |

| mhurst@kmklaw.com | |

| AUTHORIZED TO COMMUNICATE VIA EMAIL | Yes |

| DOCKET/REFERENCE NUMBER | JO2585IP0001 |

| ATTORNEY SECTION (proposed) | |

| NAME | J. Michael Hurst |

| ATTORNEY BAR MEMBERSHIP NUMBER | XXX |

| YEAR OF ADMISSION | XXXX |

| U.S. STATE/ COMMONWEALTH/ TERRITORY | XX |

| FIRM NAME | KEATING MUETHING & KLEKAMP PLL |

| STREET | ONE EAST FOURTH STREET, SUITE 1400 |

| CITY | CINCINNATI |

| STATE | Ohio |

| POSTAL CODE | 45202 |

| COUNTRY | United States |

| PHONE | 513-562-1401 |

| FAX | 513-579-6547 |

| mhurst@kmklaw.com | |

| AUTHORIZED TO COMMUNICATE VIA EMAIL | Yes |

| DOCKET/REFERENCE NUMBER | JO2585IP0001 |

| OTHER APPOINTED ATTORNEY | J. Michael Hurst, Mark E. Musekamp, Margaret M. Johnson, and Keating Muething & Klekamp, PLL |

| CORRESPONDENCE SECTION (current) | |

| NAME | J. MICHAEL HURST |

| FIRM NAME | KEATING MUETHING & KLEKAMP PLL |

| STREET | ONE EAST FOURTH STREET, SUITE 1400 |

| CITY | CINCINNATI |

| STATE | Ohio |

| POSTAL CODE | 45202 |

| COUNTRY | US |

| PHONE | 513-562-1401 |

| FAX | 513-579-6547 |

| mhurst@kmklaw.com | |

| AUTHORIZED TO COMMUNICATE VIA EMAIL | Yes |

| DOCKET/REFERENCE NUMBER | JO2585IP0001 |

| CORRESPONDENCE SECTION (proposed) | |

| NAME | J. Michael Hurst |

| FIRM NAME | KEATING MUETHING & KLEKAMP PLL |

| STREET | ONE EAST FOURTH STREET, SUITE 1400 |

| CITY | CINCINNATI |

| STATE | Ohio |

| POSTAL CODE | 45202 |

| COUNTRY | United States |

| PHONE | 513-562-1401 |

| FAX | 513-579-6547 |

| mhurst@kmklaw.com | |

| AUTHORIZED TO COMMUNICATE VIA EMAIL | Yes |

| DOCKET/REFERENCE NUMBER | JO2585IP0001 |

| SIGNATURE SECTION | |

| RESPONSE SIGNATURE | /J. Michael Hurst/ |

| SIGNATORY'S NAME | J. Michael Hurst |

| SIGNATORY'S POSITION | Attorney for Applicant |

| DATE SIGNED | 08/16/2019 |

| AUTHORIZED SIGNATORY | YES |

| FILING INFORMATION SECTION | |

| SUBMIT DATE | Fri Aug 16 15:00:16 EDT 2019 |

| TEAS STAMP | USPTO/ROA-XXX.XXX.XX.X-20 190816150016479634-882007 41-61092742954aea41598aa5 c10503e65bc237cfd6db831c3 f98d0b5523cb7921068-N/A-N /A-20190816141959315391 |

| Under the Paperwork Reduction Act of 1995 no persons are required to respond to a collection of information unless it displays a valid OMB control number. PTO Form 1957 (Rev 10/2011) |

| OMB No. 0651-0050 (Exp 09/20/2020) |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}